ER

Joined March 2019

- Tweets 93

- Following 185

- Followers 597

- Likes 1,071

39 Photos and videos

2h

HDD: ms tmtb pounding the table

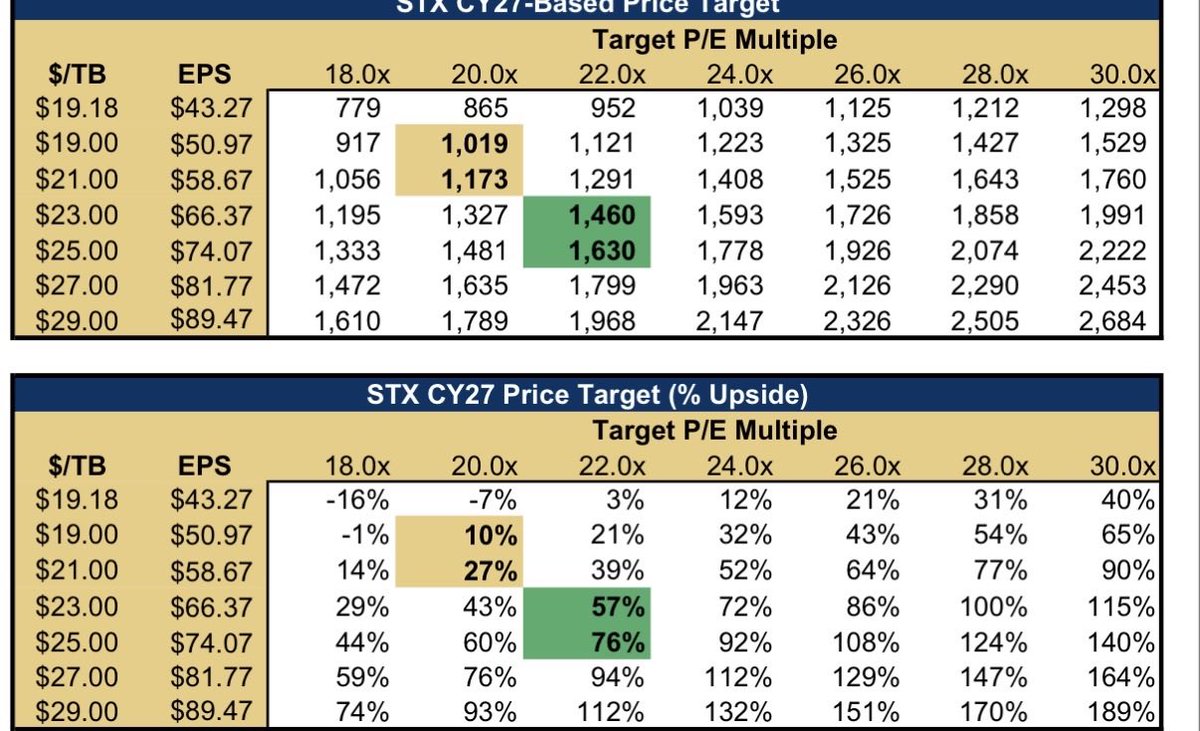

1. HDD pricing checks continue to strengthen. Industry contacts are pointing to CY27 nearline HDD pricing reaching ~$25–30/TB, with incremental demand being sold at 25% premiums to contracted pricing. Non-hyperscaler customers are already paying $30 /TB in the spot market.

2. The key driver is that hyperscalers still have no economically viable alternative to HDDs for cold storage, while the TCO advantage of HDD vs. NAND is widening. As a result, the market could see 30% YoY HDD price increases in 2027.

3. Checks suggest Seagate is not aggressively locking customers into LTAs because management believes supply-demand dynamics give them pricing power. That is incrementally positive for future earnings leverage.

4. If HDD pricing reaches ~$30/TB by CY28 (vs. Street assumptions still below $20/TB), earnings power could be materially higher:

$WDC: potential for $70 EPS

$STX: potential for ~$100 EPS

5.Structural thesis remains intact: unlike compute, storage demand compounds over time because every AI-generated token/output must be stored. Even if AI compute spending eventually moderates, storage spending can continue growing independently. The report views HDDs and NAND as two of the most attractive AI infrastructure segments today, with HDD stocks potentially having more near-term upside as investors adjust to improving pricing data points.

1

1

113

Jun 5

A lot of noise re: NVDA/Rubin SOCAMM content cut from the @SemiAnalysis_ article.

The actual article was saying that Nvidia is reducing Rubin NVL72 SOCAMM DRAM capacity per rack by roughly 50% b/c of severe DRAM supply constraint. It's also a deliberate effort to optimize Rubin’s memory configuration around BOM cost and deployment economics.

2

226

May 6

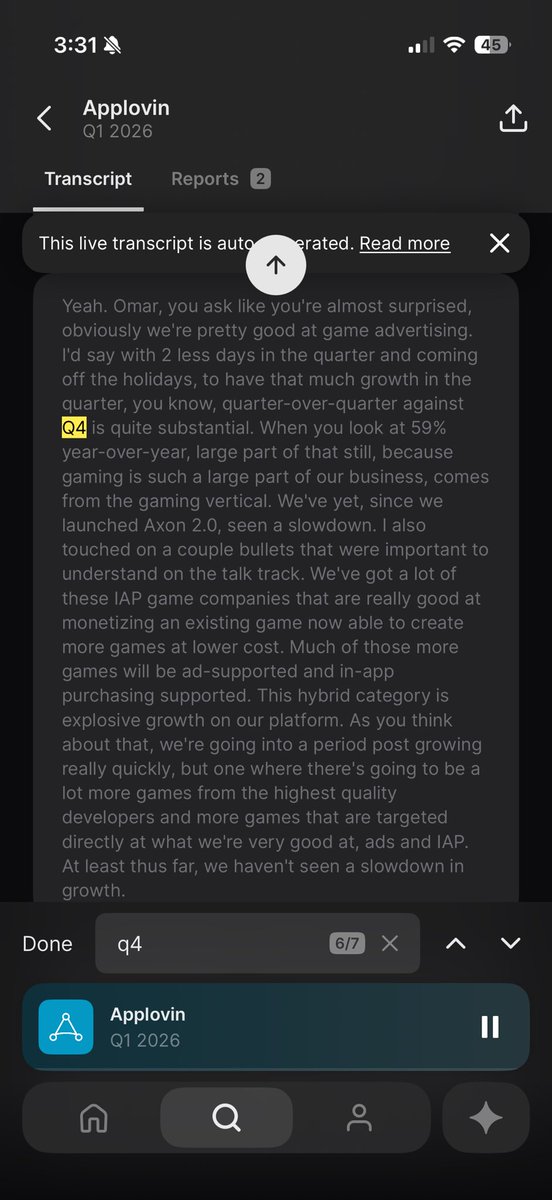

I don’t really understand the $APP fade here. Some key quotes from call just now:

1. "we saw a big acceleration going exiting the quarter. And then April. Q two. Bigger than any quarter that we had in Q4, which as you know, most advertising businesses, I don't know of another advertising business actually that can grow Q1 over Q4, but when you're in e-commerce, normally the first half of the year is a huge drop against Q4. So already being ahead of where we were in Q4 prior to opening up, the platform gets us really excited"

2. “When you look at 59% year-over-year, large part of that still, because gaming is such a large part of our business, comes from the gaming vertical. We've talked about 20%-30% long-term growth in the games category. I think we mentioned that maybe 6-8 quarters ago. We've never had a single quarter that's come closeto those growth numbers.”

Two things matter here 1) gaming biz still strong and provides a great foundation for long term growth. Company has guided Q1 and Q2 this year on the higher end of the company’s historical 3-5 % growth. Ofc the company beats every q due to their typical conservative guidance so 5-7% annualized is roughly 20-30% on an already high base.

2. Now compound the foundation of the optionally in DTC which still haven’t GA yet. The company said that they are growing dtc rev faster than any month in q4 last year which is absurd because q4 historically benefits enormously from seasonality due to Black Friday and Christmas. It really shows how the underlying biz is re-accelerating.

Stock likely trading <20x fwd pe for a company that did 120% eps cagr over the last 3 years with best in class margin and growth performance.

4

6

54

5,827

May 4

Regathering my thoughts on $APP before its earnings on May 6 and GA launch of DTC on the horizon.

open.substack.com/pub/deepdi…

2

5

22

6,483

Mar 26

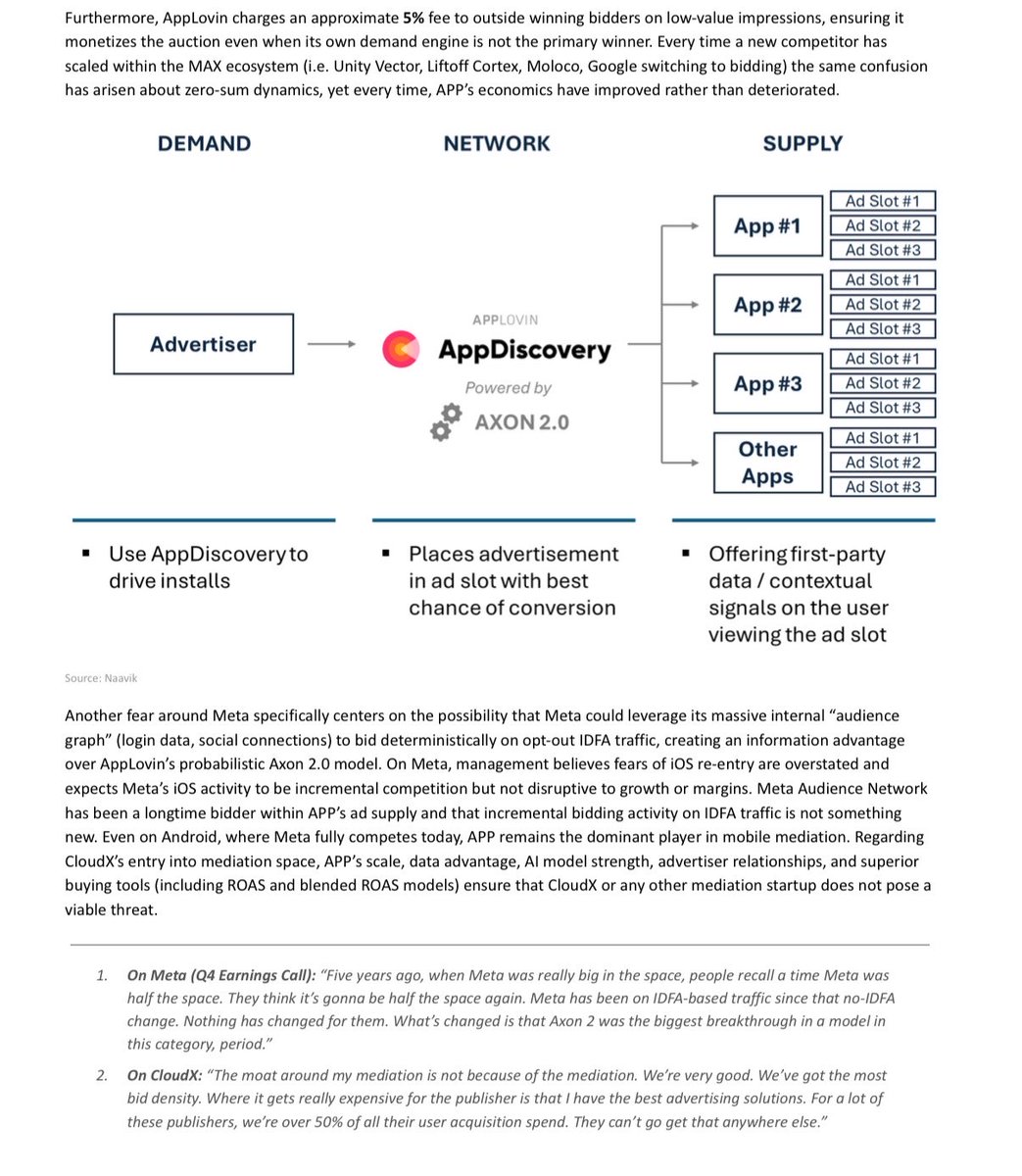

Ultimately $APP still debating two things here: (1) how real the competitive risk is around the core gaming business, and (2) how much incrementality DTC actually brings.

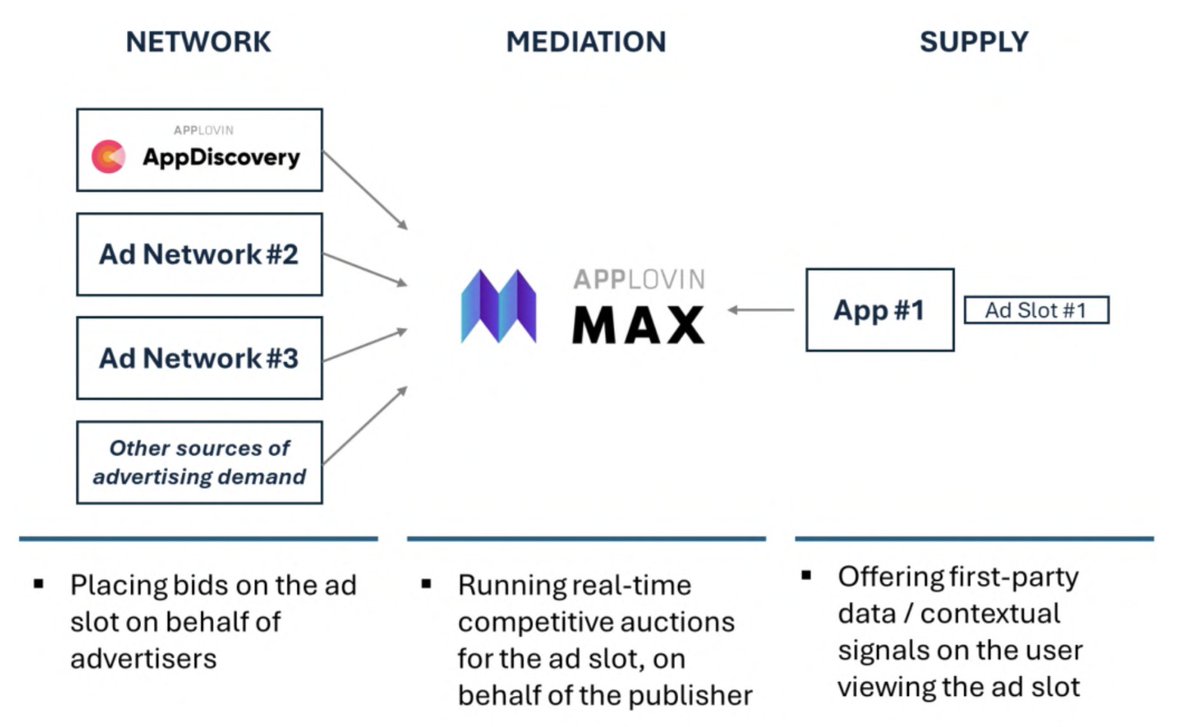

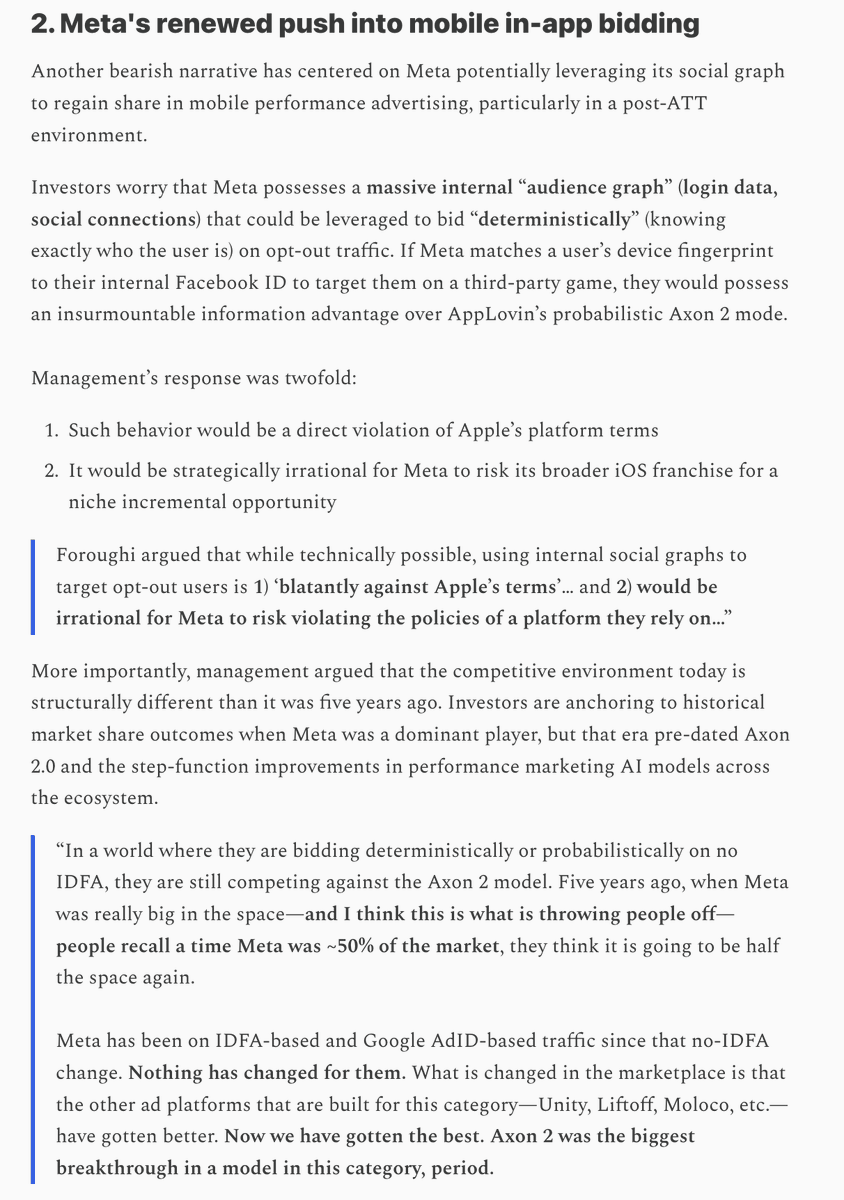

On 1), investors are still too anchored to the idea that APP is just another bidder competing head-on with Meta, when the more important point is that APP controls both sides of mobile advertising: the mediation layer through MAX; and the demand layer through Axon.

When bid density increases through the entry of additional demand sources (including Meta), the total value of the auction “pie” expands. Meta Audience Network has been a longtime bidder within APP’s ad supply and that incremental bidding activity on IDFA traffic is not something new. Even on Android, where Meta fully competes today, APP remains the dominant player in mobile mediation. So more competition in the auction is not automatically zero-sum for APP. The real question is whether that competition starts to show up in MAX share loss / weaker ROAS / slower gaming growth, and I do not think the evidence is there yet.

Regarding demand side moat, Axon observes the full competitive landscape in real time (i.e. which bids win, which lose, at what price, and against which inventory) across 2 million auctions / second. No pure demand-side player, including Meta Audience Network, has access to that signal. Meta sees only its own bids and its own wins; while Applovin’s Axon sees everyone's. That data asymmetry compounds over time because every auction generates incremental training data that makes the model marginally smarter, which improves ROAS.

On (2), I would frame DTC a bit more carefully. I do not think it is fully de-risked, but I also do not think the stock is pricing in much incrementality today. Street consensus implying decelerating growth from 46% / 29% / 21-24% in 2026–2028 while management explictly pointed out that core biz alone can generate ~20-30% growth going forward. Stock trades at 25x fwd p/e and high teens ev/ebit which is roughly in line w/ low-growth adtech peers. To me, that suggests the market is still mainly underwriting core durability and assigning limited value to DTC beyond optionality.

DTC advertisers remain at a structural disadvantage, with roughly 1,000 creatives per campaign versus 50,000 for mobile game developers, limiting model performance and slowing optimization. @AxonAdsManager is now addressing that bottleneck through its GenAI stack, including multi-agent tools for interactive landing pages, early traction in static image generation, and expected AI video capabilities that should enable higher-volume, higher-performing 15–30 second ads tied to dynamic product catalogs. As that toolset matures, the combination of unskippable full-screen inventory, gaming-like creative scale, and Axon’s closed-loop optimization engine could create a performance marketing channel with a level of efficiency and feedback density that is difficult for peers to replicate.

I'm long $APP because I have a lot of respect for what Adam and the team have built, but more importantly, I think the company’s product quality and execution remain best-in-class. Over a longer horizon, I want to stay focused on the trajectory of the underlying business rather than the day-to-day narrative.

5

8

78

11,110

Mar 26

$APP under pressure pre-market on Cleveland 3P checks

1. eCom spending momentum sounds subdued in 1Q – continued instances of churn. Customer feedback from eCom brands suggests scale has been a common issue, with ROI diminishing as budget move up from low initial levels. We have not seen much new customers momentum to offset the instances of churn we’ve seen in 1Q.

2. Gen-AI creative viewed as removing hurdles for new customers & could improve ROI/scale. Creative challenges have remained a bottleneck for existing & new customers, keeping a lid on media spending or preventing new customers from joining. Feedback was positive on both APP’s new internal tools as providing quality output and solving some of these issues & we’ve also heard partners investing in outside/3P tools to help as well.

4

1

31

27,375

Mar 24

1. 10yr breaking out while inflation expectations reaches 5.2%. Market focused on near-terms headlines re: peace talks but strait of hormuz traffic remained constrained.

2.Every 10% increase in oil prices adds roughly 20 bps to global headline CPI. At this point, the risk to the U.S. economy appears skewed more toward upside inflation risk than labor-market weakness.

3. Near-term conditions are likely to remain choppy, so it still makes sense to run a market-neutral strategy until there is better visibility into the specific terms of any negotiated outcome.

4. Asset-heavy over asset-light continues to outperform, helped by the latest Claude feature set and JPM’s $SAP downgrade.

The terminal value debate is still unresolved, while the absence of a clear positive catalyst for the entire sector remains the primary overhang. At the same time, negative catalysts are plentiful, as frontier labs are highly incentivized to position the enterprise application layer as the key answer to the broader AI ROI debate.

4

3,828

Mar 12

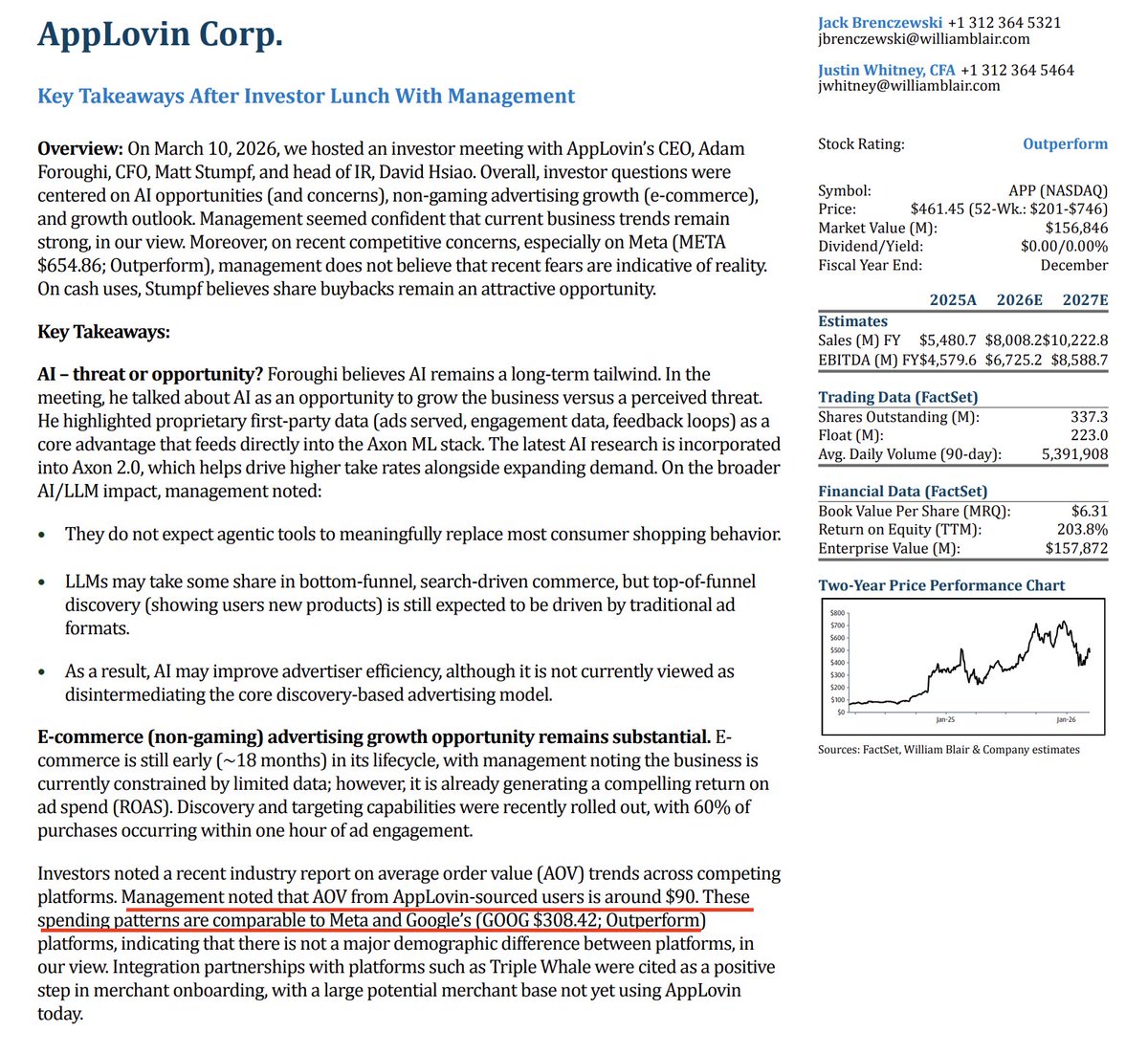

William Blair $APP Note from Investor Lunch Meeting:

1. AI Application in AppLovin Algos

Management’s view is that AI should strengthen Axon’s moat, not weaken it, because APP has proprietary first-party ad-serving, engagement, and feedback-loop data feeding the model stack. That data advantage should make the system better over time and harder to replicate externally.

Regarding agentic purchases and LLM disruption, management’s believes that LLMs may take some bottom-funnel search commerce, but they are unlikely to replace most normal consumer shopping behavior. More importantly, they do not believe LLMs disintermediate top-of-funnel product discovery, which is the core of APP’s advertising product. The implication is that AI is more likely to improve targeting and optimization than to structurally impair demand.

2. DTC / E-commerce

Management said e-commerce is still only about 18 months in, remains somewhat data constrained, but is already showing compelling ROAS. They pointed to partnerships like Triple Whale as helping merchant onboarding and emphasized that there is still a large merchant base not yet using AppLovin. That suggests the demand-side opportunity is not just deeper monetization of existing customers, but also basic customer acquisition. Discovery and targeting products were only recently rolled out, which suggests the business is still early in its optimization curve rather than fully matured.

They highlighted that 60% of purchases happen within one hour of ad engagement, which is important because it suggests the ads are driving real purchase intent rather than low-quality clicks. They also said AOV from APP-sourced users is around $90, roughly comparable to Meta and Google, which implies the underlying user quality is likely similar to other scaled digital advertising platforms.

It is becoming less useful to view the business as strictly gaming versus non-gaming, because the platform is moving toward a more unified auction structure. A unified auction should improve matching efficiency, liquidity, and cross-vertical data flywheel benefits. In other words, management is arguing that this should increasingly operate as one stronger machine, rather than two siloed businesses.

3. Core Gaming Business

While investors are increasingly focused on the e-commerce opportunity, management made clear that the core gaming business remains healthy and is still expected to grow meaningfully. Gaming continues to serve as an important monetization engine and foundational earnings driver for the broader platform.

They also said repeated gaming model releases have allowed APP to grow above underlying industry growth rates, and they continue to believe model improvements can drive roughly 3% to 5% sequential quarter growth in gaming solely. The broader takeaway is that the story does not rely solely on e-commerce emerging successfully. Gaming still appears to be the base business funding and supporting the next leg of growth.

2

8

53

7,925

Mar 10

Some color on $APP drawdown today:

1. Shilsky @ JPM: "CEO meetings in Boston w/ sell-side said that they don't expect DTC revenue to 'hockey stick' ; E-commerce general availability remains on track for a 1H launch (note that this aligns with MGMT tone regarding DTC for quite some time now, nothing new/incremental)

2. Technically, $APP saw a ~30% gain off the lows in 2 weeks, while stock rejected at 50 SMA. Optics / Semi outperforming today likely didn't help funding.. slightly concerned that long hardware / short software trade might be back as GTC conference starts next week

3

1

30

7,664

Mar 4

$APP Summary of the Applovin Fireside Chat at Morgan Stanley's TMT conference this morning

1. Regarding Gaming Ads (Core Business)

The 20-30% growth target from core business established by Matt two years ago was always intended as a floor, not a ceiling, and the company has consistently exceeded it. Management emphasizes the technology is still "very nascent" and directed model enhancements recursive learning from scaling data continue to compound. No signal they're ready to formally raise the target, but the tone was clear that upside to estimates remains. (1/4)

4

11

81

13,636

Mar 4

3. Improving Conversion Rate as a Lever for Growth

The platform currently converts on just 1.3% of the ads it serves, meaning 98.7% of impressions generate no revenue.

The low conversion rate is not a failure of AppLovin's recommendation algorithm, but rather a limitation of its historical advertiser inventory. The system is highly predictive; when it identifies a "high value moment"—a user who is dissatisfied with their current game and primed to churn—the conversion rate already exceeds 5%. The problem is that most users are perfectly happy playing their current game. Because AppLovin historically lacked content diversity outside of gaming, the model was forced to serve "100 gaming ads in a row" to content users, which inevitably leads to ad fatigue and wasted impressions

As advertiser density grows across e-commerce and other categories, the model will be able to serve a different, personalized product in every impression. The model will exclusively reserve gaming ads for those rare, high-value moments where the conversion rate is already >5%, ensuring game developers face no cannibalization and get maximum value. For all other impressions, instead of forcing a gaming ad, the system will seamlessly pivot to serving a highly personalized e-commerce or lead-generation product. Management fully expects conversion rates to exceed 5% as density builds.

A roughly 4x improvement in conversion rate would not translate linearly to 4x revenue because the majority of advertiser spend flows to publishers as payment for ad space, and AppLovin reports the spread as revenue. However, Foroughi argued the outcome could actually be better than 4x to the bottom line if the company's technological lead allows it to capture an expanding spread in the auction. (3/4)

1

1

7

2,768

Mar 4

4. AI-Generated Creative

Gaming advertisers typically run over 50,000 creatives per campaign, while e-commerce advertisers manage around 1,000 at best, a 50x gap that structurally limits e-commerce spend on the platform.

AppLovin is deploying multi-agent AI systems on top of LLMs to generate both static images and video creative. The static image tool is already in pilot with positive early results, and video generation is in development. Foroughi stated that both capabilities should be ready by the GA launch in 1H 2026. Closing this creative density gap should meaningfully unlock higher e-commerce advertiser spend and improve conversion rates on the front end of the ad experience.

The cost discipline story remains firmly intact. Data center costs have been growing at approximately 10% of the rate of overall revenue growth, and are actually trending better than that now. Total headcount sits at roughly 900, but only about 400 are tied to the core ad tech business and back office. The e-commerce business development team is approximately 15 people. Stumpf indicated the company will add "tens of people" to support web advertising, not hundreds, and expects no material change to the cost profile.

12

2,608

Feb 16

$APP I believe investors continuously overestimate E-Commerce and underestimate the strength of the core gaming business, which is the primary driver of the higher-than -expected guidance 2Q ago.

E-commerce only accounts for roughly 200-300M of the 1.6B revenue that Applovin generated in the most recent quarter. While I acknowledge that DTC presents a huge TAM opportunity (~8x current gaming TAM) and presents a 2nd growth curve for the company, to ignore the strength of gaming biz and de-rate a company growing 68% YoY to ~23-25x fwd P/E or ~0.3 PEG ratio is incredibly irrational.

Bears will argue that 1) competitive concerns from Meta and CloudX might creative growth headwinds for gaming biz 2) E-commerce are still very nascent and non-incremental to the company’s growth.

Regarding 1), this argument completely ignores the fact that Applovin owns both the supply and demand layer of app-inventory bidding. In the MAX auction, AppLovin benefits not only when its own bidding model wins but also when competitors win. $APP collect a 5% tax every time a non-applovin bidder wins an impression.

For 2), while it’s true that e-commerce are still in its early stages, the AXON platform is benefiting from the added diversity in advertisements. In the most recent call, Adam mentioned that e-commerce companies are contributing hundreds of thousands of diverse ads at any given point, compared to tens of thousands by gaming companies, representing a much larger opportunity for the model to learn. This will create a flywheel of learning that will boost the AXON algorithm and drive market share growth.

I encourage the $APP community to check my full 4Q deep dive here where I identified the investment setup and extracted key management quotes addressing investor concerns:

open.substack.com/pub/deepdi…

1

2

62

8,480

Feb 13

$APP 2025 Q4 Earnings review

In the article I linked below, I isolated key management responses during earnings call addressing investor concerns surrounding (1) the durability of the core growth engine and 80% EBITDA margin profile, (2) whether Meta/CloudX represent a real structural threat to MAX and Axon’s closed-loop advantage, and (3) E-Commerce progress and details around AXON's 1H global launch.

APP now trades at ~20x CY26 EV/EBIT and ~23x forward P/E for a Rule-of-150 compounder printing 66% top-line growth and 84% EBITDA margins.

Link to the article ⬇️

open.substack.com/pub/deepdi…

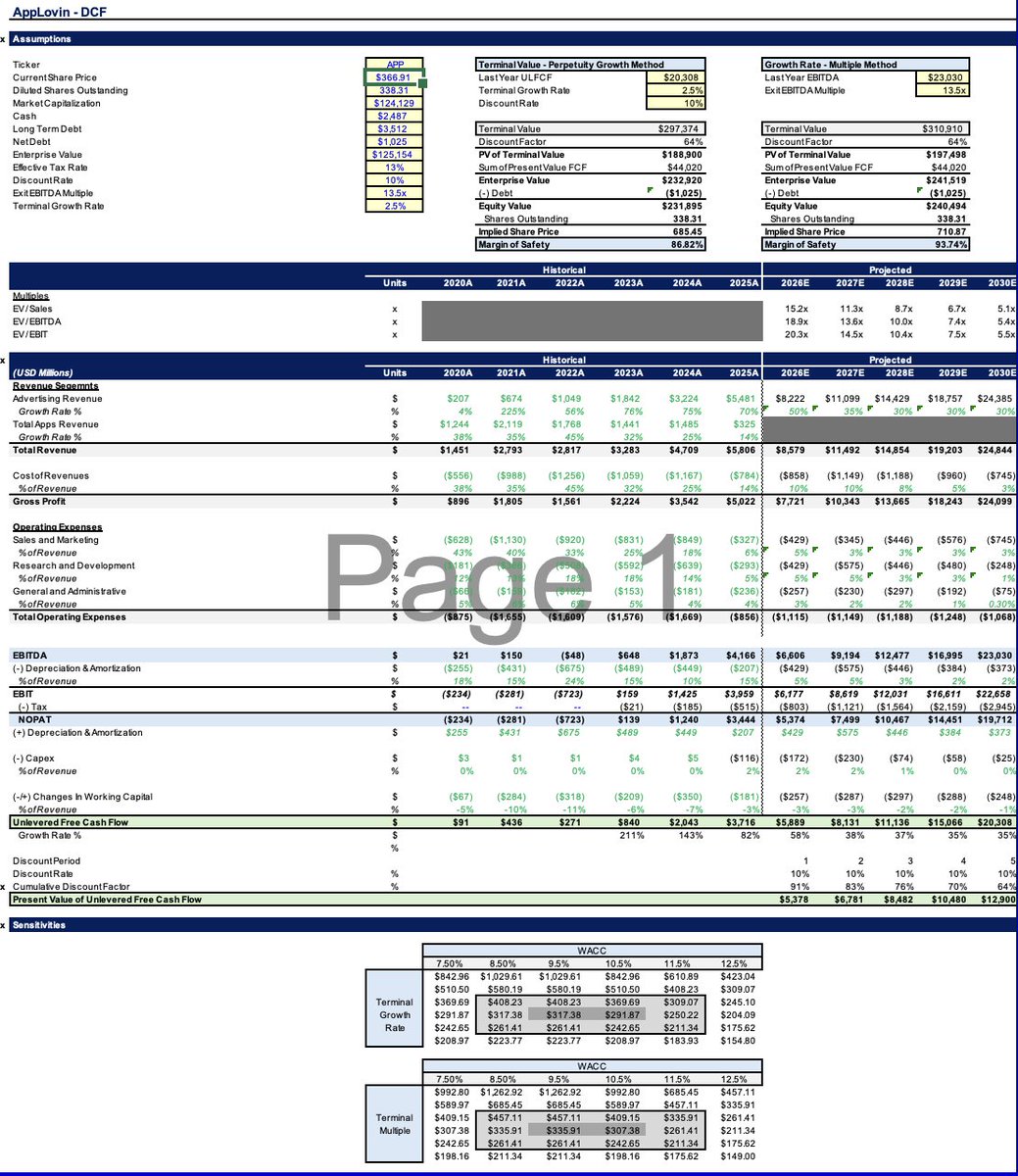

Image 1: Updated modeling

Image 2: Excerpts from the substack article

2

5

23

19,277

Feb 11

$APP slid 3% pre-market on Unity driven weakness

The bear case is that broader mobile gaming weakness is weighing on the complex, so $APP is getting caught in the risk-off rotation alongside other gaming/UA-exposed names. However, $APP's stronger-than-expected guidance last Q was largely driven by expectations of a strong core gaming biz this Q and forward, and several intra-quarter checks as well as $RBLX earnings all present constructive data points for underlying gaming monetization, which undermines the idea that sector momentum are deteriorating.

The remaining alternative (and, in my view, more coherent) explanation is that MAX potentially took mediation share from $U as 4Q ironSource -8% QoQ v. Unity Ads 15% QoQ.

4

2

26

3,797