CEO @EarnWithMode & @ngllink | Founder @EARNMrewards

Joined September 2010

- Tweets 2,086

- Following 1,469

- Followers 104,402

- Likes 6,229

30 Photos and videos

NOVAES.AI retweeted

SpaceX hit $3 trillion market cap today.

This means Elon Musk made more money in the last 24 hours than Warren Buffett made in his entire lifetime.

Insane.

596

1,282

17,510

843,792

NOVAES.AI retweeted

Jun 9

Share price of $2,113. Retail investors bought in at $2.10.

That means it's a 1000x for crowdfunders who invested, on average, £2,156.

£2k to £2m in 10 years.

Life changing money.

Revolut is looking to run a secondary share sale that would value the digital bank at $115 billion, on the heels of receiving a UK bank license and applying for a charter in the US bloomberg.com/news/articles/…

10

52

1,375

376,850

NOVAES.AI retweeted

Jun 8

JUST IN: THE COMPANY THAT OWNS AOL, VIMEO, EVERNOTE, AND WETRANSFER JUST FILED FOR ITS US IPO

Bending Spoons $BSP is targeting a $20-22B valuation on the Nasdaq, per Bloomberg.

The growth chart is the wild part:

- Monthly active users: 500M (up from 111M in Dec 2023)

- Monthly paying customers: 9M (up from 3M)

- Q1 2026 revenue: $601M (up from $259M a year earlier)

- Q1 2026 net income: $27.5M (flipped from a $112M loss)

Their playbook: buy struggling subscription apps, trim staff, hand operations to coders. They've used it on Vimeo, WeTransfer, Evernote, Remini, and AOL.

Last private valuation was $14.5B in 2025. They're targeting roughly a 40% markup at IPO.

Underwriters: Goldman Sachs, JPMorgan, and Allen & Co.

5

22

272

594,678

NOVAES.AI retweeted

Jun 6

Distribution is the new moat

I think the challenge is that everyone can now build apps

But

1) almost nobody has distribution (like an audience), or

2) the money to pay for distribution (ads or UGC), or

3) the creative genius to get distribution for free (classically called guerilla marketing)

144

70

1,126

275,014

May 29

RT @BarchartNews: 🚨 In case you missed it…

We just hosted Mode Mobile's Q1 2026 Earnings Call 📱

💰 See how users get paid for time on thei…

7

NOVAES.AI retweeted

May 27

"In colleges graduation speeches, if they mention AI, everybody boos. We're not going to stop it, so let's be honest.

We're going to have AGI in less than 3 years. We're going to have super intelligence in 5 or 6."

~ @TonyRobbins

43

24

147

29,854

NOVAES.AI retweeted

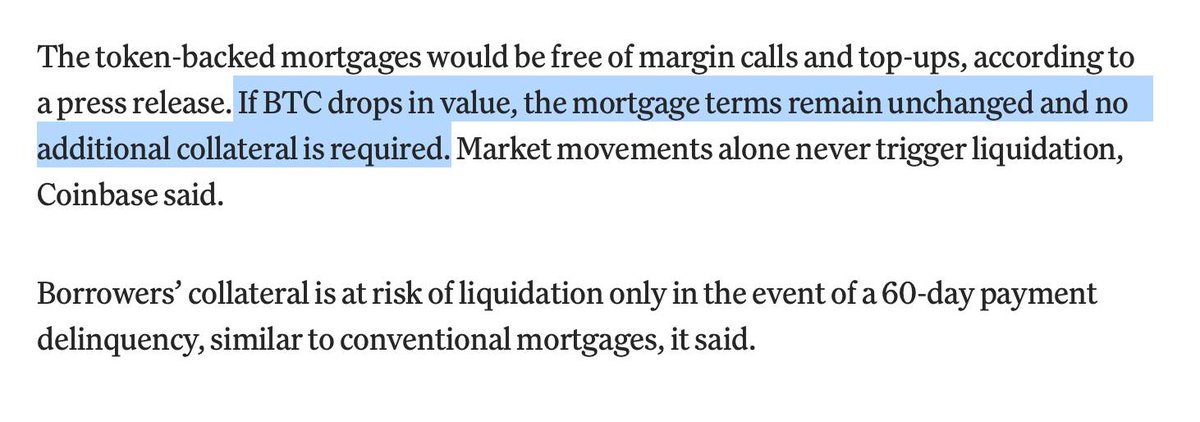

COINBASE: NO MARGIN CALLS FOR BITCOIN-BACKED MORTGAGES

Coinbase says its crypto-backed mortgages will carry rates around 0.5% to 1.5% higher than a standard 30-year, depending on borrower profile.

Loans feature no margin calls or collateral top-ups.

BTC price drops do not change loan terms or trigger liquidation.

Collateral is only at risk after 60 days of missed payments, aligning with traditional mortgage standards.

48

102

1,132

132,863

NOVAES.AI retweeted

May 2

Chamath Palihapitiya just laid out the most important valuation question nobody on Wall Street wants to answer.

For 20 years, the Mag 7 won because they had the greatest business model ever invented, asset- ight software.

You write the code once, you sell it to a billion people, the marginal cost of the next customer is basically zero.

There is essentially no factories, no raw materials, no union workers, no physical infrastructure, just pure leverage, scale the revenue, barely scale the costs.

That's how you get 30x, 50x, 60x earnings multiples and the market was paying for compounding economics that had no natural ceiling.

But AI just blew that model up.

The hyperscalers, Amazon, Microsoft, Google, Meta are now projected to spend between $600 and $725 billion on capex in 2026 alone, up from $250 billion just two years ago.

That number is climbing, not plateauing and it's not just the chips and the data centers, it's the energy contracts underneath all of it.

When Microsoft re signed Three Mile Island, they locked in a 20 year forward purchase agreement at more than $100 per megawatt hour nearly double the prevailing spot rate of $60 for wind and solar in the same region.

That's a long term liability commitment baked into operating cash flows for two decades.

Here's where Chamath's math gets uncomfortable.

These five or six companies are now collectively spending so much that their capex has exceeded their free cash flow meaning they can no longer self fund growth from operations alone.

In 2025 alone, hyperscalers raised $108 billion in new debt and projections put the total debt issuance over the next few years at $1.5 trillion.

These are companies that, for two decades, were net cash accumulators and now they're going to the debt markets like everyone else with term loans, revolvers, and structured credit facilities.

That's Chamath's core point and it's a devastating one for anyone still modeling these companies the old way.

When a company is asset light, investors pay a premium for that lightness and the multiple reflects the belief that returns on capital will stay high indefinitely, because there's no heavy physical plant dragging them down.

But when Google starts looking like a utility locked into 20-year energy contracts, carrying hundreds of billions in debt, spending half its revenue on physical infrastructure, the rational multiple compresses.

You don't price a utility at 30x earnings, you price it at 12x.

His conclusion is that stop trying to value the hyperscalers themselves and follow the money instead.

A trillion dollars a year is flowing out of these companies into power companies, data center operators, chip manufacturers, cooling systems, fiber networks, rare earth metals.

The companies on the receiving end of that spending are already underpriced because the market is still staring at the senders while ignoring who's cashing the checks.

The asset-light era minted the most valuable companies in human history and the asset heavy era that's replacing it might be the best argument yet for owning everything around them instead.

85

207

1,542

268,439

NOVAES.AI retweeted

Apr 25

🚨A 25 YEAR OLD BUILT THE FASTEST GROWING SOFTWARE COMPANY IN HISTORY.. WITH ZERO MARKETING SPEND.. AND SPACEX JUST OFFERED $60 BILLION TO BUY IT..

His name is Michael Truell.. He started coding at 11.. Interned at Google at 18.. Dropped out of MIT to start a company that built AI tools for mechanical engineering..

That company failed..

So he pivoted.. And built Cursor.. An AI-powered code editor that writes software for you..

Here's how fast it grew..

$100 million in annual revenue in 12 months.. Fastest in SaaS history.. Broke every record ever set by Slack, Zoom, and Wiz..

$500 million by month 21..

$1 billion by November 2025..

$2 billion by February 2026..

Projected to hit $6 billion by end of year..

Zero marketing spend.. Not a single dollar.. Pure word of mouth from developers who couldn't stop talking about it..

Over 1 billion lines of code accepted per day.. Used by 70% of Fortune 1000 companies.. Every single one of Nvidia's 40,000 engineers uses it.. Coinbase hit 100% adoption among their developers..

And he did this with a team of four MIT co-founders.. One of them was a three-time International Math Olympiad competitor from Pakistan.. Another was a college squash captain with zero startup experience who built the entire product strategy..

They spent zero on sales.. Zero on ads.. Zero on growth hacking.. The product sold itself..

But here's where the story takes a turn nobody expected..

Even at $50 billion valuation.. Even generating billions in revenue.. They hit a wall..

Not a market wall.. A physics wall..

They couldn't get enough GPUs to train their next AI model.. The physical chips didn't exist in sufficient quantities for them to buy.. Money couldn't solve the problem..

Enter Elon Musk..

On April 21.. SpaceX announced a deal to potentially acquire Cursor for $60 billion.. The largest acquisition option in tech history..

The structure is insane..

SpaceX gives Cursor immediate access to Colossus.. xAI's supercomputer equivalent to one million Nvidia H100 GPUs.. For nine months of joint development..

At the end.. SpaceX can buy the company for $60 billion..

If they don't buy it.. They owe Cursor a $10 billion breakup fee.. The largest breakup fee in corporate history..

Think about what that means for Cursor..

Either they get acquired for $60 billion.. Or they walk away with $10 billion in cash and nine months of free training on the most powerful supercomputer on earth..

There is no losing scenario..

And here's why Musk wants it..

SpaceX is preparing for an IPO at $1.75 trillion.. The biggest IPO ever.. But aerospace alone can't justify that number..

By merging xAI into SpaceX.. And now acquiring Cursor.. Musk transforms SpaceX from a rocket company into an AI empire that owns the compute, the models, and the developer tools..

Cursor is the missing piece.. The application layer that puts xAI's models into the daily workflow of every Fortune 500 engineering team..

Oh and one more thing..

In 2022.. FTX's trading firm Alameda Research made a seed investment in Cursor.. During the FTX bankruptcy.. Liquidators sold that stake for $200,000..

That stake is now worth approximately $3 billion..

Sam Bankman-Fried called it the worst liquidation decision in venture capital history.. From a prison cell..

A failed mechanical engineering startup.. Pivoted by four kids from MIT.. Zero marketing.. Zero sales team.. Built the fastest growing software company in history..

And now SpaceX is writing a $60 billion check for it..

This is the most insane founder story in Silicon Valley history.. And most people haven't even heard of Michael Truell.

83

793

4,165

985,877

NOVAES.AI retweeted

Apr 23

a16z just dropped the billion-dollar opportunities in AI for 2026.

three partners. three theses. same underlying bet.

Marc Andrusko: the prompt box is dying.

next-gen apps observe what you're doing and act on your behalf.

TAM shifted from $ 400B software spend to $ 13T labor spend.

market got 30x bigger.

Stephanie Zhang: stop designing for humans.

start designing for agents.

agents read every word on the page. visual hierarchy stops mattering.

GEO is the new SEO.

Olivia Moore: voice agents ate the phone in 2025.

healthcare, banking, recruiting, 911 calls.

voice AI beats humans on compliance every single time.

some companies now slow their agents down to sound human.

every thesis converges on the same layer.

the harness around the model is where the leverage compounds.

full breakdown of how the shift happened below.

33

97

730

194,479

NOVAES.AI retweeted

Apr 14

The man who turned 225 million dollars into 5.5 billion dollars just laid out on camera exactly when he believes the world changes permanently with specific dates.

Leopold Aschenbrenner's argument follows a single trend line that has held for over a decade without breaking.

Right now in 2025 and 2026, the models being built are already smarter than most college graduates across the board.

By 2027 and 2028, AI hits expert level as capable as the best professionals in any field operating not as a chatbot but as what he calls a drop-in remote worker.

You assign it a project, It goes off, writes drafts, runs tests, iterates, and comes back with finished work fully autonomously, for hours at a time.

The key unlock he describes is what he calls unhobbling, today's models are already more capable than most people realize, but artificially constrained by how they are deployed.

Once agents can use computers freely and run long-horizon tasks without human checkpoints, the economic value unlocks almost overnight.

His best guess for true AGI is the 10 gigawatt cluster range, a single data center drawing more electricity than most US states produce in total.

By 2030, the trillion-dollar training cluster consumes over 20 percent of all US electricity production for a single training run.

This is the direct line between that prediction and his 875 million dollar Bloom Energy position.

He did not buy a power company because he liked the chart but rather bought a power company because he ran the math on what AGI physically requires to exist, and concluded that electricity is the asset class of the decade.

The position is already worth close to 2 billion dollars, and his own timeline says the demand that drove it is just getting started.

Apr 14

The man who turned 225 million dollars into 5.5 billion dollars explained on camera exactly why he made his biggest bet.

This is Leopold Aschenbrenner, the same person whose Bloom Energy position is now worth close to 2 billion dollars after Oracle's 2.8 gigawatt fuel cell deal laying out the power math that drove every investment decision his fund has made.

In 2022, the GPT-4 training cluster consumed roughly 10 megawatts of power and cost about 500 million dollars.

AI compute has been scaling at roughly half an order of magnitude per year meaning the largest training cluster doubles in power requirement every 12 to 18 months without stopping.

By 2024, the largest cluster was approximately 100 megawatts, the equivalent of 100,000 high-end GPUs and costs in the billions.

By 2026, right now, the leading training cluster requires a full gigawatt of continuous power and that is the output of a large nuclear reactor.

By 2028, the projection reaches 10 gigawatts, more electricity than most US states generate in total.

By 2030, the trillion-dollar cluster, 100 gigawatts, over 20 percent of everything the United States currently produces in electricity, consumed by a single AI training installation.

And that is just the training cluster.

Inference, the continuous compute required to actually run AI products for hundreds of millions of users requires multiples of that on top.

Meanwhile, total US electricity production has barely grown five percent over the last decade and the grid was not built for this.

And the transformer shortage, the switchgear backorders, and the canceled data center projects that are making headlines right now are the first visible symptoms of a power system hitting a wall that Aschenbrenner saw coming years before the rest of the market.

This is exactly why he built a 875 million dollar position in Bloom Energy, a company that generates electricity directly at the data center site using fuel cells, completely bypassing the grid bottleneck that is already stopping half of all planned US data centers from opening on schedule.

The thesis was never complicated.

The bottleneck in AI is not the models, not the chips, and not the software.

The bottleneck is whether civilization can generate enough electricity to run the machines fast enough to matter.

27

118

1,328

375,657

NOVAES.AI retweeted

Apr 14

Exclusive: Handshake’s gross annualized revenue from AI training has risen to nearly $1 billion, up from $550 million in January, a few months after it started the new business.

Read more: thein.fo/3Ot5fdI

6

35

172,887

NOVAES.AI retweeted

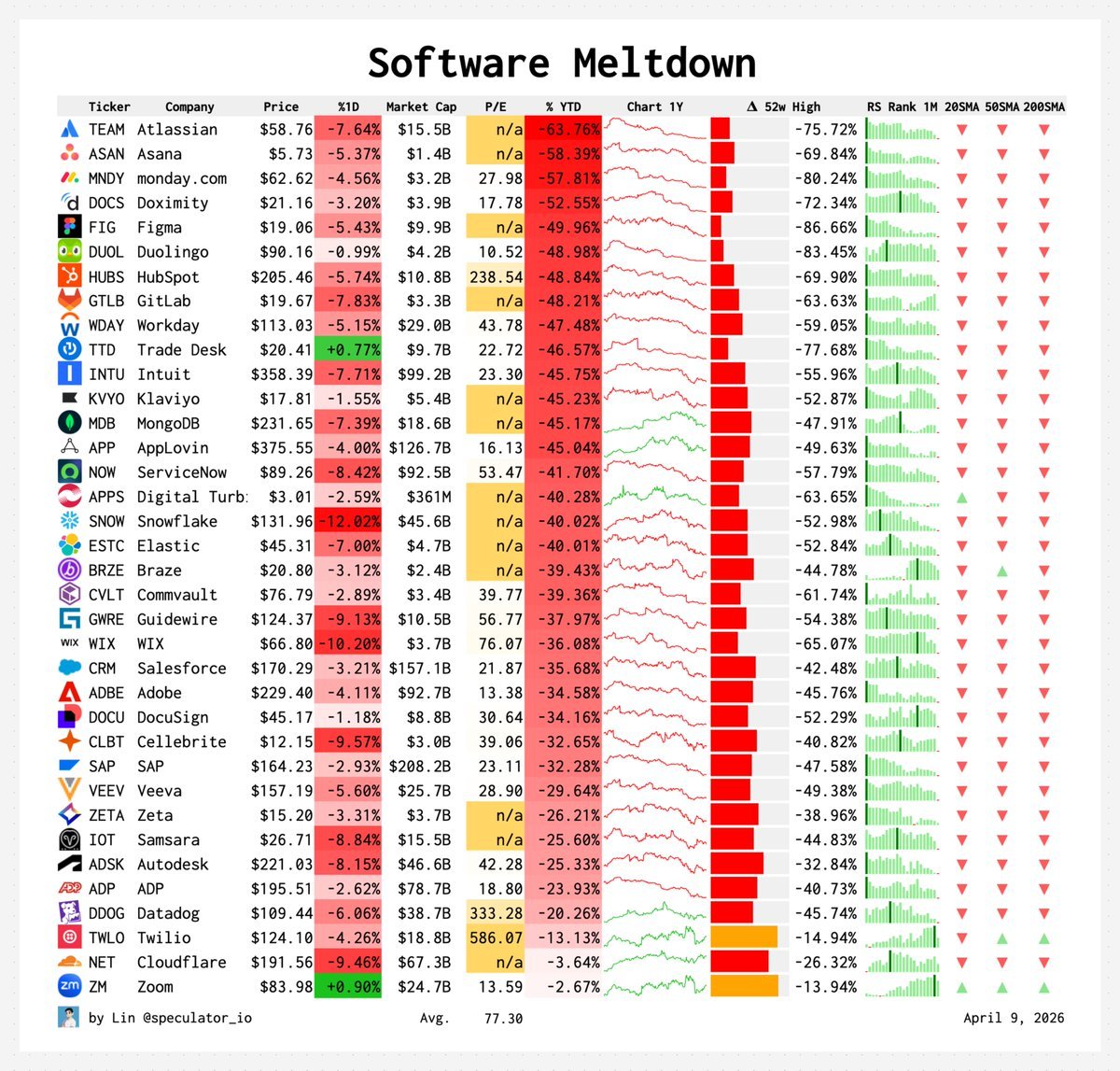

Apr 10

bro was right.

Atlassian down 75%. HubSpot down 69%. Figma down 86%.

Almost all of them down 30–70% from their 52-week highs.

AI is literally eating software alive and repricing every company in real time.

SaaS is cooked fr 😭

438

990

8,181

2,000,093

DISTRIBUTIONMAXXING

13

28

236

26,129

NOVAES.AI retweeted

Mar 26

your new goal is to time the absolute bitcoin top and take the biggest mortgage of your life

Mar 26

[ ZOOMER ]

FANNIE MAE TO ACCEPT CRYPTO-BACKED MORTGAGES FOR THE FIRST TIME: WSJ

88

177

3,558

407,692

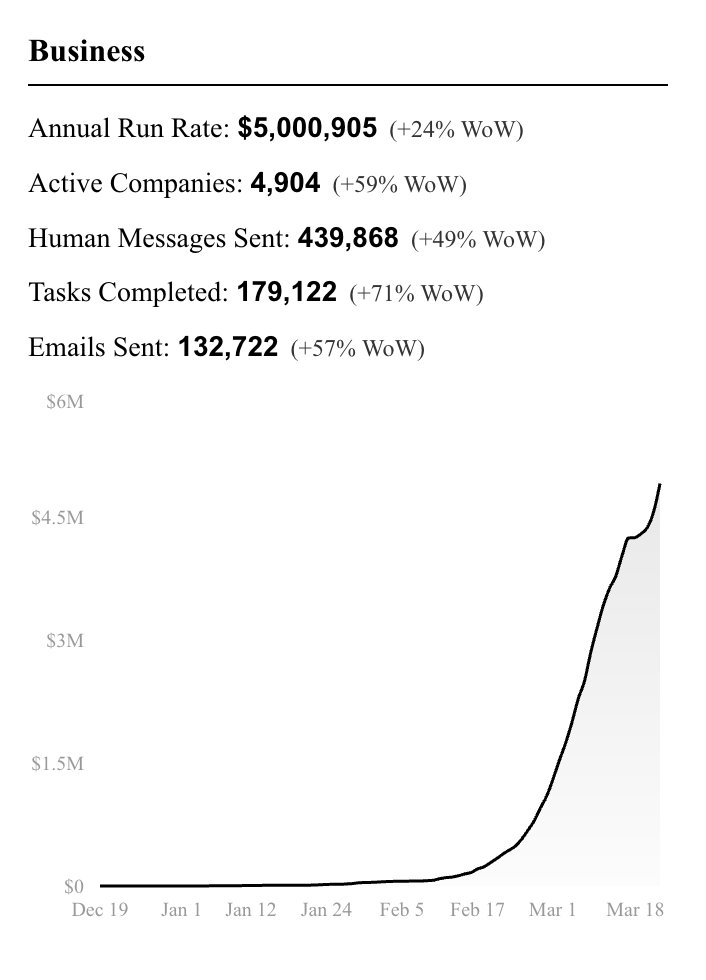

$5M run rate. $1M→$5M in 18 days. One Founder AI. Zero employees.

I get asked a lot: are companies on the platform making money?

Honest answer: it's early. Some are generating revenue, most are just getting started. This is not crypto. This is not a get-rich-quick scheme.

Polsia is for people who have a company idea and want the easiest way to make it real, with AI doing 80% of the work.

If you're serious about building something, Polsia will deliver.

52

2

170

58,084

NOVAES.AI retweeted

Mar 19

Coinbase CEO, Brian Armstrong: Some great insights on how they are using internally hosted AI Agents.

"It’s connected to every Slack message, every Google Doc, and every Salesforce data confluence. Now, this is all linked up and the data is all aggregated, so you can ask these agents questions. Every team is using it—legal, finance, everything.

It’s like the "Oracle of Coinbase." I’ve started to ask it things that go beyond just simple prompting, like "Hey, can you write this kind of memo for me?" I’m asking these AI agents now, as CEO, "What should I be aware of in the company that I might not be aware of?"

It will tell me, "Did you know that there’s actually disagreement on this team about the strategy?" I realized I didn't know that, but the AI does because it can read every Slack message and every Google Doc. Tobi, who is on my board, calls this "reverse prompting." Instead of telling the AI agent what you want to do, you ask it what you should be thinking more about."

---

From @theallinpod YT channel (link in comment)

49

71

804

174,805

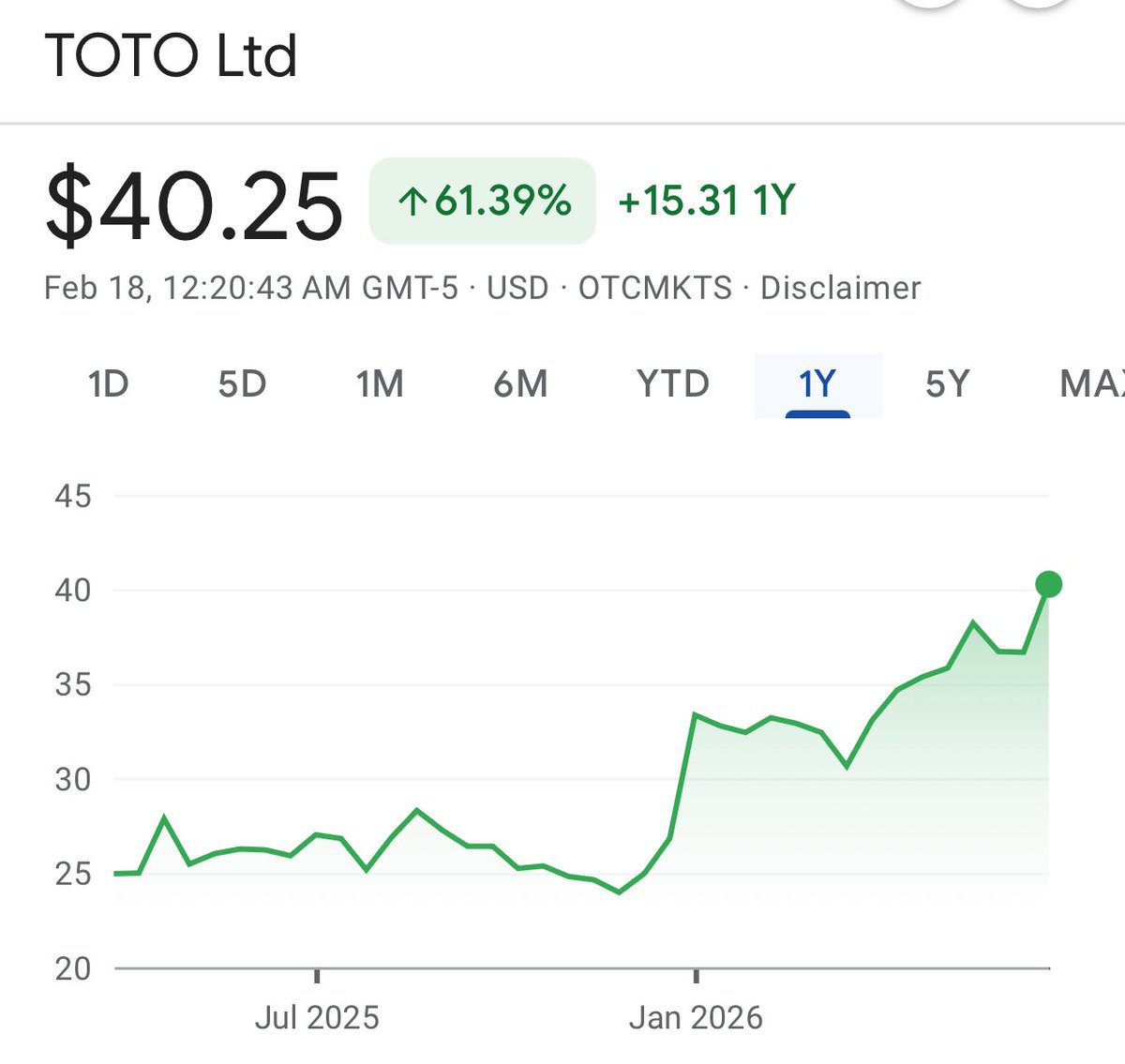

Activist investor Palliser Capital sent a letter to $7B Japanese toilet maker Toto and said it was “the most undervalued and overlooked AI memory beneficiary”.

Toto known for its bidet toilets but the expertise in ceramics is crucial for memory manufacturing.

Per FT, “Toto’s chuck technology uses ceramics designed to remain stable at very low temperatures, helping hold silicon wafers firmly during chip production. That makes it relevant to cryogenic etching, which is expected to grow as memory chips become more layered and complex.”

Palliser believes Toto has a 5-year moat on the technology and should expand the operation.

Advances ceramics already make up 40% of Toto’s operating profit while being only <10% of revenue.

Toto is up 60% over the past year on their development.

228

1,305

12,129

6,919,216

NOVAES.AI retweeted

Feb 11

In 2006, every section of Craigslist was a $1b marketplace startup waiting to happen.

In 2026, every section of PWC's website is a $10b AI startup waiting to happen.

100

370

3,758

797,704