takes time

Joined January 2020

- Tweets 1,758

- Following 224

- Followers 119

- Likes 1,043

21 Photos and videos

Nowhere retweeted

May 29

Copper. Zinc. Germanium. Platinum. Palladium. Nickel. Rhodium. Gold.

Each plays a critical role in defence, electrification, and semiconductor supply chains. And each is produced across our three mining operations. Governments and industries are racing to secure critical mineral supply.

We've got three tier-one operations producing all of them - today.

Learn more: ivanhoemines.com

2

14

83

5,291

Nowhere retweeted

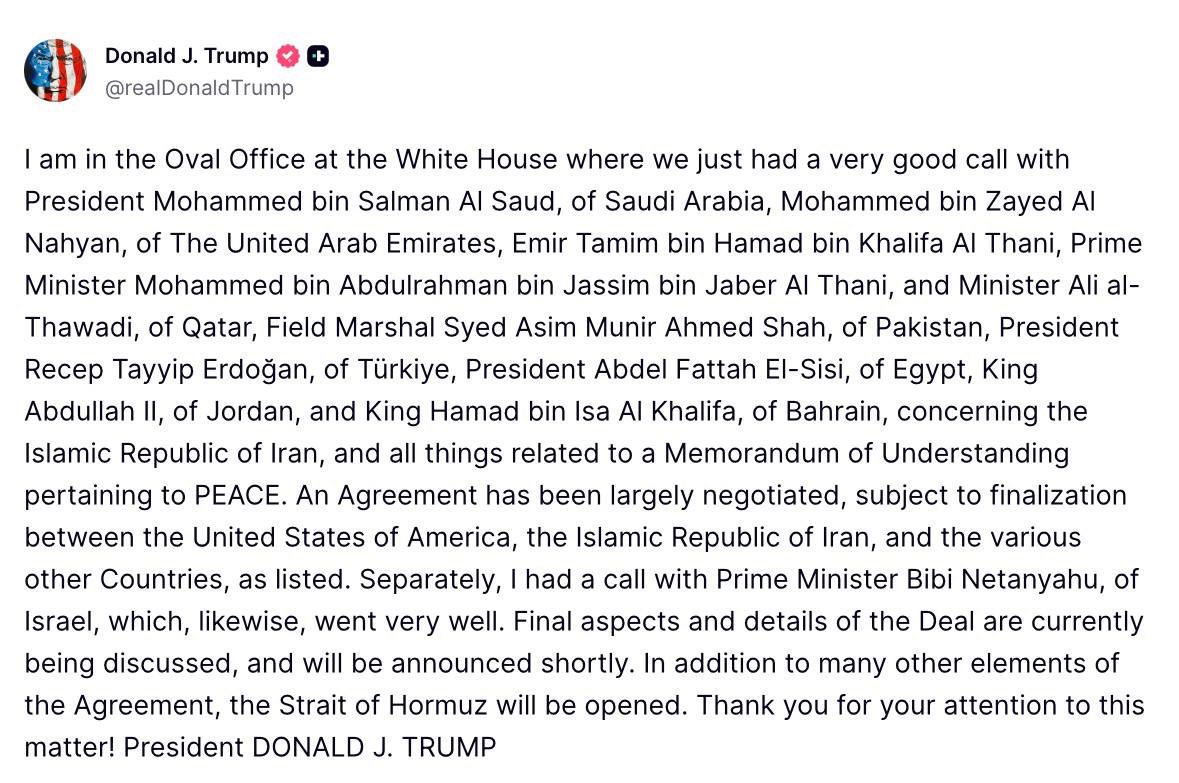

BREAKING: President Trump says an agreement with Iran has been “largely negotiated” and will be announced shortly.

Trump says the Strait of Hormuz will be reopened under the agreement.

735

1,888

12,212

3,750,698

29 Dec 2025

29 Dec 2025

What a garbage award! This company has done nothing for shareholders in the past 5 years while gold is hitting all time high. Overpaid Sabina for the mine in harsh location, gold prepayment and cutting dividends in a super gold bull market!

5

890

29 Dec 2025

29 Dec 2025

Joke of the year? Look at the share price - this company has done nothing for shareholders. Unnecessary gold prepayment and cutting dividends while gold is in a super bull market. Many companies that they could purchase but they chose to overpay Sabina in the harsh location.

2

639

6 Oct 2025

It’s just a freaking bubble. Similar to $nvda, they played with their own to get their market cap pumped. This market will not end well.

6 Oct 2025

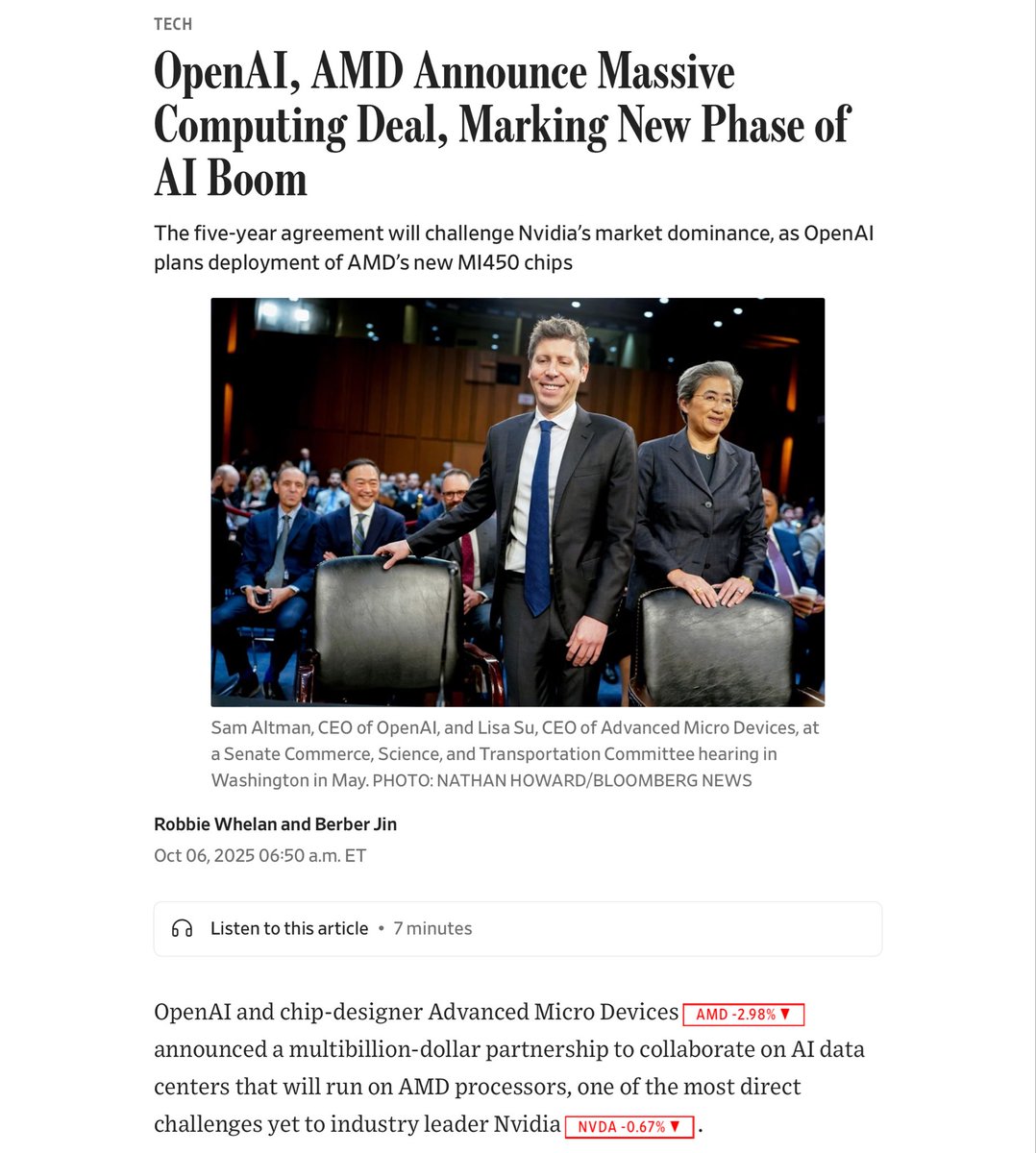

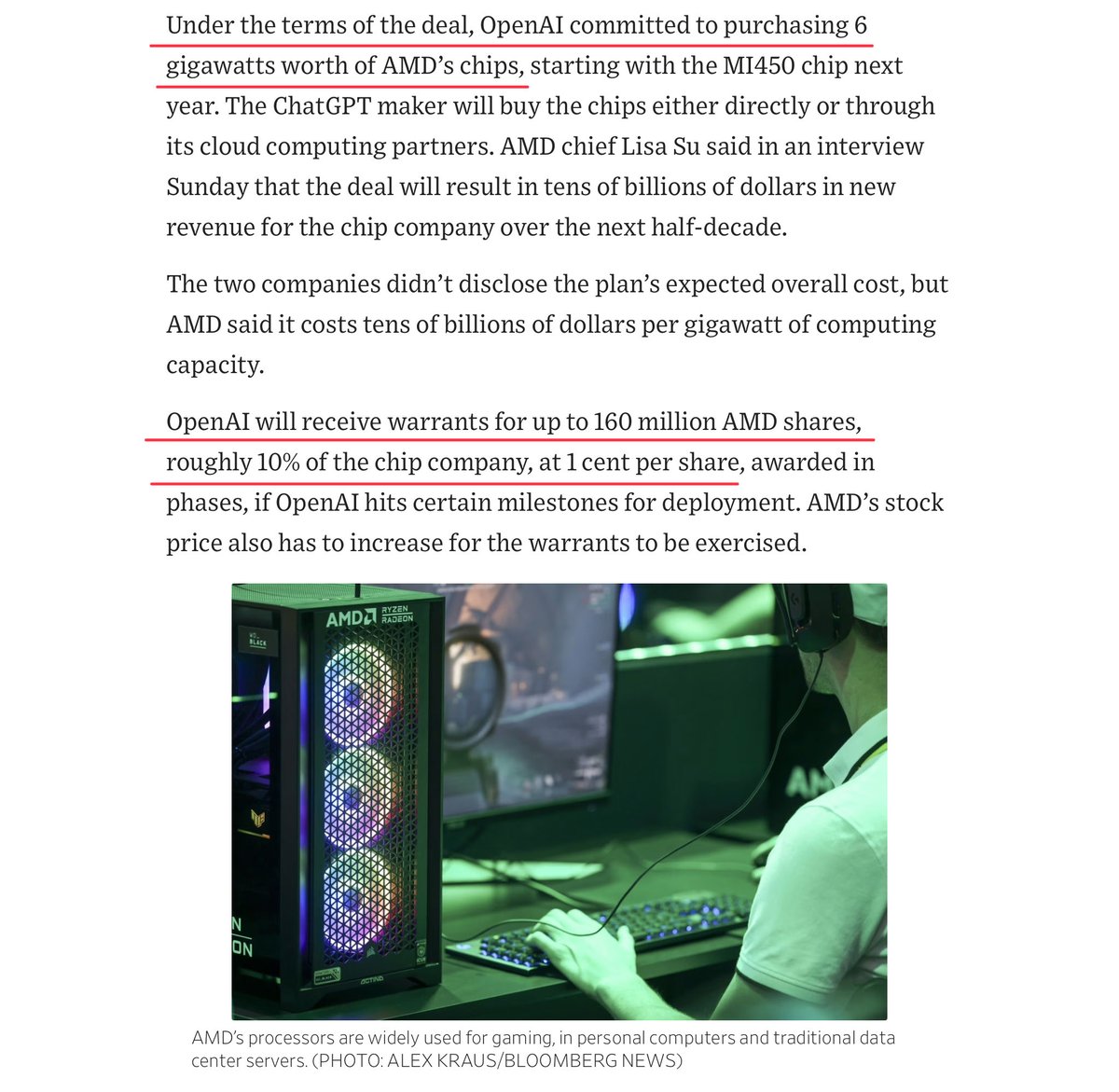

$AMD giving OpenAI 10% of its stock (worth roughly $35bn pre-market) so OpenAI can buy 6 GW of AMD chips over the next few years. Stock 27% pre-market.

“I give you stock, you give me money, my stock goes up. Everyone gets rich.” The circular AI economy powers on.

6

1,024

14 May 2025

A consistent broken clock

2

253

24 Mar 2025

24 Mar 2025

@MarkJCarney you are disgusting - reverting the evil policies that have been in place by your party in the past decade in your past 10 days as an acting PM and you are making it as a proud news for your election?? YOU are one of them who has destroyed the Canadian economy!

2

261

Nowhere retweeted

19 Mar 2025

Oh I would love to see the Northern Lights someday!

632

14,502

77,263

3,722,491

4 Mar 2025

PoS

187

Nowhere retweeted

8 Jan 2025

$PYPL is on my Wishlist for 2025 to pull back to between $71 and $66

And we rinse and repeat.

10

17

306

91,056

Nowhere retweeted

3 Feb 2025

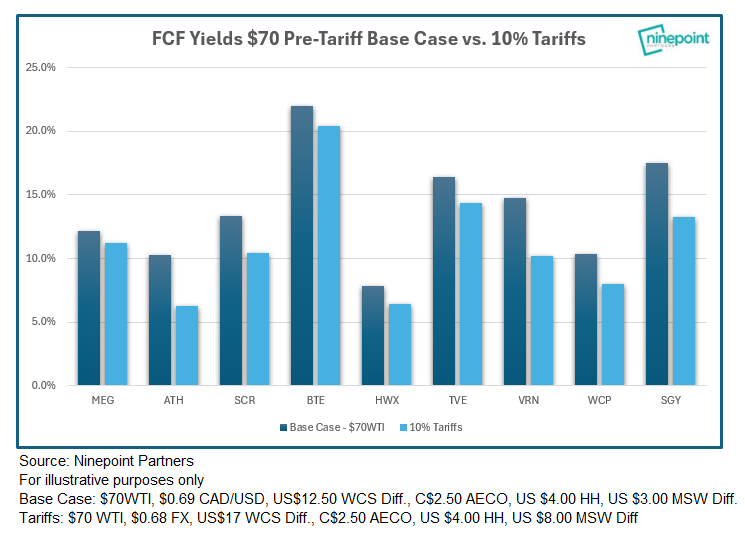

What does a 10% tariff mean for CDN energy stocks?

🛢️assuming tariffs last a full year, average cashflow falls by 7% and free cashflow falls by 20% (includes hedging)

🛢️Base case $70WTI FCF yields = 13.9%. With full tariff this falls to 11.2%, so we would argue that stocks are fully discounting the tariff - no need for panic!

🛢️we believe we are being conservative ($17WCS differential vs. spot $15 and estimates of ~$16)

🛢️a rising oil price falling currency will buffer much of the tariff impact

🛢️we believe most of the tariff on CDN oil will be a complete cost passthrough to the US consumer, yet are not modelling this (would mean lower WCS diff)

🛢️given modest CF impact we do not see production volumes being impacted, though flows on TMX to Asia (and less to US refineries) could ~0.3MM Bbl/d.

🛢️at this point modelling integrated names involved too many unknown variables = low confidence in #'s

🛢️we can never, ever allow ourselves to be treated like this again. More pipelines are the answer, and I'll have more on that soon.

39

86

417

59,788

Nowhere retweeted

2 Feb 2025

This is really what it’s all about. Nothing to do with “border security.” He is a ignorant, vengeful, demented, megalomaniacal narcissist.

4,910

7,018

40,652

2,928,451

16 Jan 2025

The most garbage gold mining company by Clive Johnson and the management team $BTG $BTO.TO @B2GoldCorp @B2G_BackRiver

16 Jan 2025

This is an untrue article. They just intend to do share buyback starting from end of q1 but it doesn’t guarantee that they will actually do. This management team is one of the worst and always lies and make up excuses for the company poor performance @B2GoldCorp

1

2

464

Nowhere retweeted

8 Jan 2025

Don't be alarmed; it gets much worse.

88

63

620

42,415

Nowhere retweeted

7 Jan 2025

By my estimates, the market is assigning a $1.14 trillion valuation to Tesla's FSD, Robotaxis, & Optimus or 86% of its total market cap.

This bubble will burst more spectacularly than any we've seen in our lifetimes.

$TSLA

24

23

173

12,577