Bitcoin & Consciousness | RarePepe | SOFTWAR | Digital1776 | #Bitcoin5D

Joined April 2009

- Tweets 4,229

- Following 1,706

- Followers 617

- Likes 12,082

106 Photos and videos

John⚡️Dobharchú retweeted

Jun 12

did fifa really add hydration breaks just to run more ads this shit is insane lmao

542

4,415

161,754

4,276,013

John⚡️Dobharchú retweeted

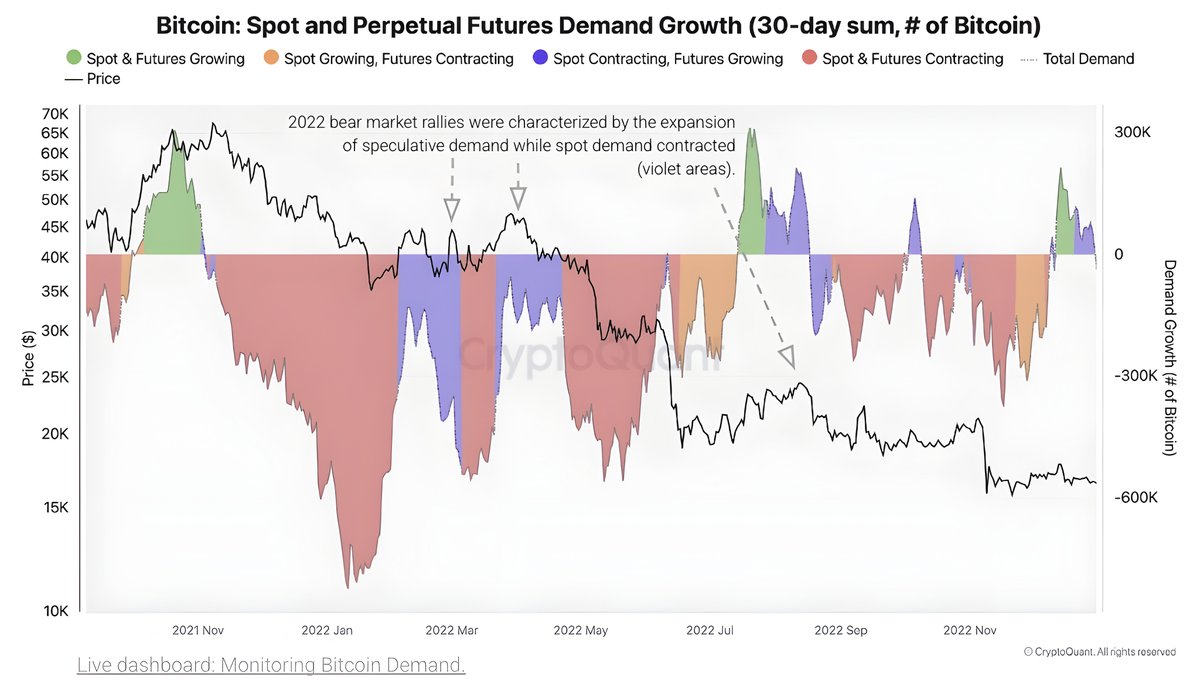

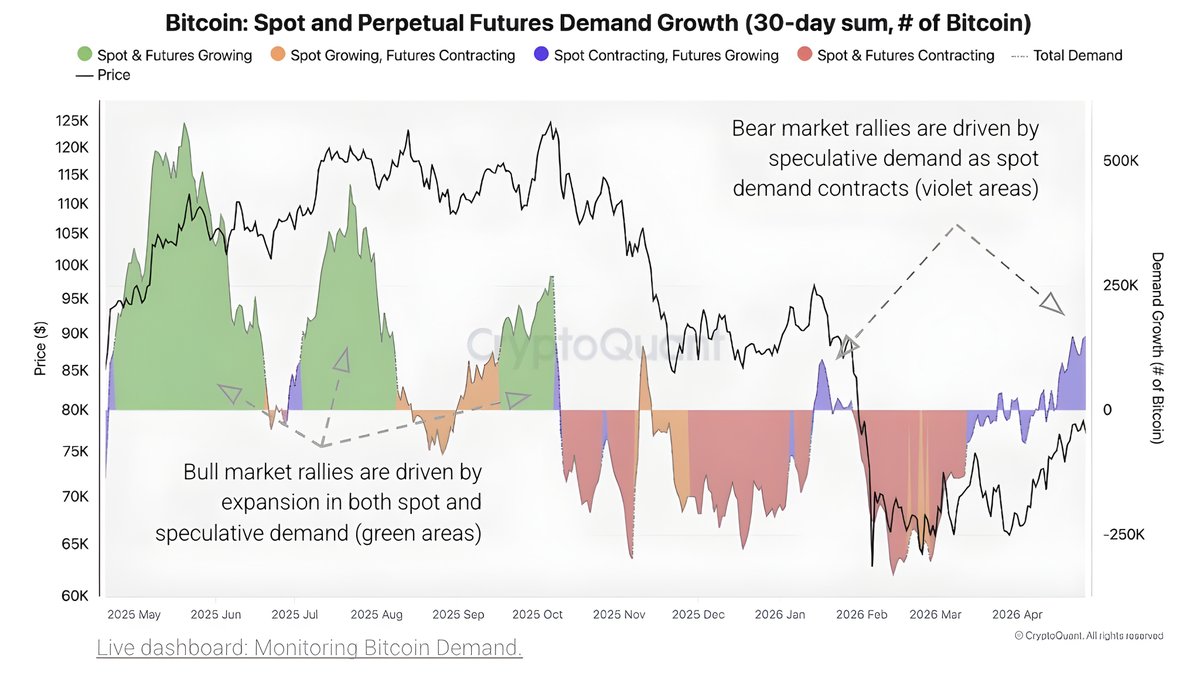

Bitcoin’s current demand structure is showing a divergence that’s worth paying attention to.

Futures (ERP) demand is rising, while spot demand continues to contract.

We’ve seen this before. A very similar setup appeared in early 2022, when the market was being pushed higher by leveraged positioning rather than real spot buying. That imbalance eventually resolved to the downside.

The recent ~20% rally in April seems to follow the same pattern. The move was largely driven by perpetual futures traders, not strong spot accumulation.

When a rally is driven mainly by futures, it’s often less sustainable.

Futures positions are typically leveraged and short-term in nature. They can push price quickly, but they don’t represent real capital flowing into the asset.

Spot buying, on the other hand, means actual demand. Coins are being bought and held, which tends to create a stronger and more stable foundation for price.

In a futures-driven move, the market becomes more fragile:

If momentum slows, leveraged longs can get squeezed

Funding can flip and unwind positions quickly

There’s less “real” demand underneath to support price

That’s why these types of rallies often fade or correct once the leverage unwinds.

Looking at the broader structure:

Sustainable rallies usually happen when both spot and futures demand expand together. Right now, we’re seeing a phase where speculative demand increases while real demand weakens.

This also aligns with other indicators and current Elliott Wave counts.

There is always more than one scenario, but right now multiple data points are pointing in a similar direction.

Simple takeaway:

Upside looks limited here, but this is not confirmed bearish yet.

For a clearer downside scenario, the market still needs structural confirmation. Until then, this remains a leverage-driven move that requires caution.

(Data: CryptoQuant)

8

1

68

6,415

John⚡️Dobharchú retweeted

Apr 24

Men without degrees built this.

2,056

16,375

97,039

1,503,892

John⚡️Dobharchú retweeted

Apr 15

I just finished my taxes. I owe $6,200 to Somalia.

630

712

13,159

193,398

John⚡️Dobharchú retweeted

Apr 12

This should be headline news EVERYWHERE.

A Pfizer insider who was former head of toxicology in Europe has just come out and said something that many "conspiracy theorists" suspected.

He estimates that 20 000 to 60 000 people in Germany have died from the c*vid vaccine.

This was said at a parliamentary enquiry commission in Germany.

So why isn't this massive news being reported everywhere?

Is the mainstream media that has recieved millions in funding from Bill Gates deliberately covering this up... 🤔

4,474

40,839

132,186

64,947,687

John⚡️Dobharchú retweeted

Apr 10

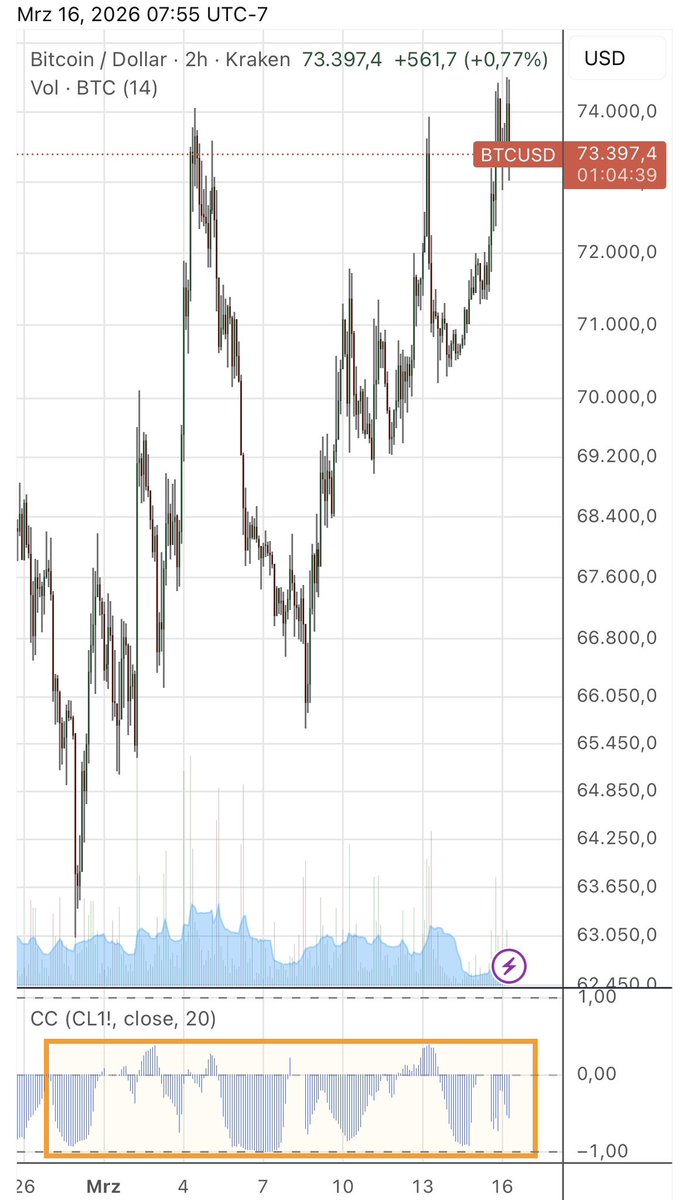

Having defended support for two months, bitcoin is finally about to test a key resistance level around 73.5K.

A breakout here could sent it back to the 90K level

131

253

2,666

569,877

Apr 10

5GW is lit 🔥

46

John⚡️Dobharchú retweeted

Apr 9

Trump's unhinged post works better as a rap song.

391

1,064

6,261

477,399

John⚡️Dobharchú retweeted

Apr 8

Why do seniors get discounts when they’re the ones that have all the money?

1,109

795

28,982

609,057

John⚡️Dobharchú retweeted

Apr 8

🇮🇷 Iran is charging $2M per ship to cross the Strait of Hormuz and they want it in Bitcoin. 😳

At $72,000 per $BTC, each ship = 27.7 BTC.

Pre-crisis, 130 ships crossed daily.

• Daily: 3,611 BTC

• Monthly: 108,333 BTC

• Yearly: 1.3 million BTC

The entire Bitcoin network only mines 450 BTC per day.

Iran would accumulate 8x the monthly mining supply. Every month.

A sanctioned nation building a Bitcoin treasury through a toll booth.

This is the most important geopolitical Bitcoin story nobody is talking about. 🔥

537

1,274

6,143

636,576

John⚡️Dobharchú retweeted

The "experts" are shaking.

They see the "chaos," the 3:00 AM pivots, and the scorched-earth rhetoric and they call it "erratic."

They think he’s losing his grip.

Fools.

They’re busy pearl-clutching while he’s running the most clinical execution of the Madman Theory in history.

Predictability is a death sentence.

When your enemies think you’re crazy enough to burn the house down just to keep them out, they don't fight—they flee.

The "unhinged" persona isn’t a bug; it’s the feature. It’s the fog of war personified.

While the midwits wait for him to "act professional," he’s busy acting like a predator.

He isn't stumbling into the mess—he is the mess, and he’s using it to bury every opponent who's too "sophisticated" to see the play.

Stop whining about the temperament and start watching the scoreboard.

If you think he’s out of control, you’re the one being controlled.

Give em hell..

@realDonaldTrump @SecWar @clif_high @ENERGY @LawrenceLepard @natbrunell @GenFlynn

11

1

22

4,053

John⚡️Dobharchú retweeted

The "Madman" isn't crazy—you’re just reading the wrong script. 🧵

Most people see "erratic" behavior and clutch their pearls. They think it's a breakdown.

They’re wrong.

It’s a high-level sales closing technique played on a global stage.

Here’s why the "Madman" is actually the most disciplined man in the room:

7

23

56

1,636

John⚡️Dobharchú retweeted

Artemis II just dropped their latest Pic.

450

3,274

15,077

370,355

John⚡️Dobharchú retweeted

Apr 4

Bitcoin has won. Global consensus is that $BTC is digital capital. The four-year cycle is dead. Price is now driven by capital flows. Bank and digital credit will determine Bitcoin’s growth trajectory. The biggest risk is bad ideas driving iatrogenic protocol changes.

3,478

4,102

29,406

3,759,593