Tech by day, deep value by night.

Joined July 2019

- Tweets 137

- Following 578

- Followers 191

- Likes 257

14 Photos and videos

PBC retweeted

11 Sep 2025

$BGSF BGSF, Inc. Announces Special Cash Dividend of $2.00 Per Share accessnewswire.com/newsroom/…

2

4

9,603

3 Jul 2025

Start pos on $BGSF. Staffing agency undergoing a strat review. Just sold Professional Services bix for $99M, leaving RemainCo (Property Mgmt) at ~$12M pro-forma EV or <1.5x normalized EBITDA of ~$8M. Mgmt is also cutting $9M costs into recovering demand environment. (1/3)

1

238

3 Jul 2025

Property Mgmt segment has generated b/w $13-23M operating income historically (2019-24). Even assuming only 50% of $9M cost savings stick to RemainCo post-divestiture, we get ~$8M normalized EBITDA. At current valuation the discount seems too large. (2/3)

1

131

3 Jul 2025

Granted, property mgmt isn't sexy. But consider: 1) they're cashed up from divestiture, so defensive if economy weakens 3) revenue inflection potential on rate cuts 4) strategic review ongoing = optionality. Risk/reward seems compelling at these levels. (3/3)

1

142

The action is increasing at Lantronixs $LTRX, with a.o. Chain of Lakes Investment reporting a 7.7% stake and pushing for Board changes in order to sell the company.

CoL believes that the company would be sold for ~$6 p/s (compared to $2.3 today).

Also to note the continued open market purchases from insiders.

2

2

16

5,685

16 Oct 2023

What is $VSTO management thinking?! Traded comps at 6x EBITDA and they’re letting the golden goose go for 5x.

1

9

44,103

1 Aug 2023

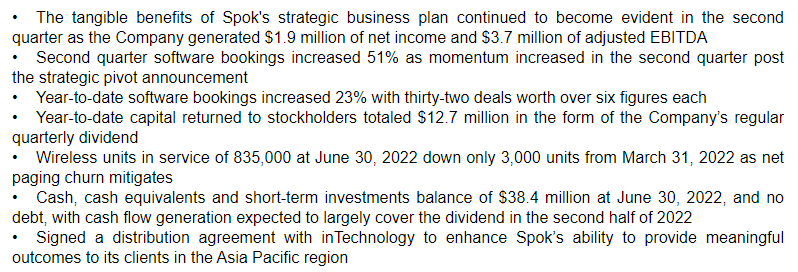

Quick update as my attention has been elsewhere. Out of $SPOK for ~95% gain. Panic sold on the recent pop and left a buck on the table, but I wanted to avoid another round trip if this rally rolls over. Given its yield, I also think there is some underlying sensitivity to rates.

2

2

569

1 Aug 2023

Took a minor bath (-20%) on $NEXS.L. Raw cheapness wasn't able to compensate for its highly vulnerable business model. Moving forward, I need to be far more considerate of HOW value gets unlocked, especially around (and in anticipation of) inflections.

1

305

8 Jun 2023

$SVT. Activist has pulled its nominations and ended the proxy contest. Calling for a strategic review of all assets, not just CPG instead. Note that ATG did ~$5M in EBIT pre-COVID and 737MAX accidents. Current MC of $30M.

1

3

625

PBC retweeted

8 Jun 2023

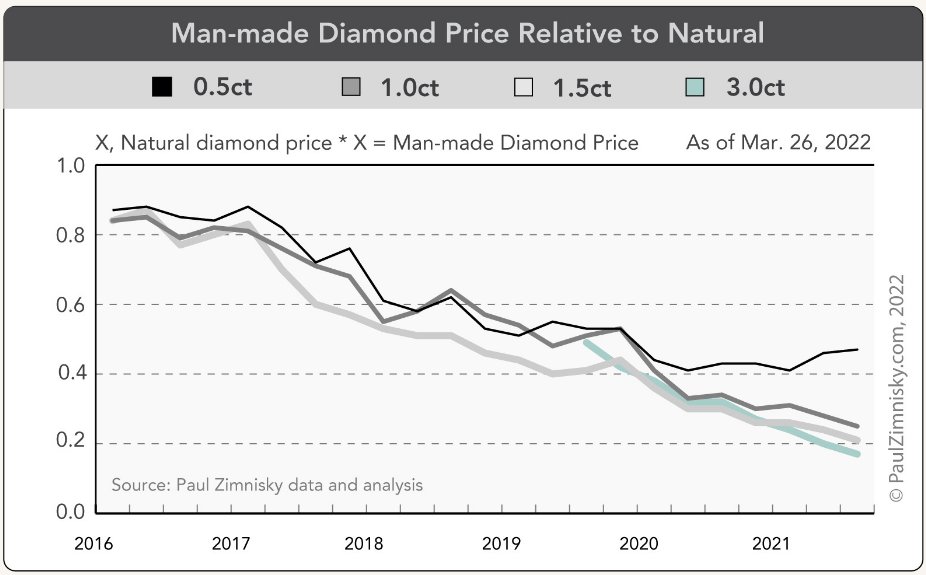

Signet $SIG just quantified that LGD represent <15% of diamond sales…“the majority of our customers still prefer the rarity of buying a natural diamond”

3

6

696

PBC retweeted

14 Apr 2023

A great write-up on Michael O'Keeffe and his contrarian approach to commodities.

$CIA.T $BDM.AX

smh.com.au/business/companie…

6

14

4,334

31 Mar 2023

Have started dabbling in a couple of biotech special sits and picked up some $MGTA. No strong view yet, but found it interesting that strat review advisor gets 1% of transaction value (if consummated) with min fee of $1.5M, implying value of $150M. ~$100M cash unrisked/~$47M MC

1

362

16 Mar 2023

Quick note (my first piece of writing in a while) on how I'm approaching the Nexus Infrastructure ($NEXS.L) tender offer: pointbarcapital.substack.com…

1

435