Football, Financial markets & Data Analytics.

Joined September 2011

- Tweets 7,659

- Following 841

- Followers 168

- Likes 9,308

104 Photos and videos

Prateek retweeted

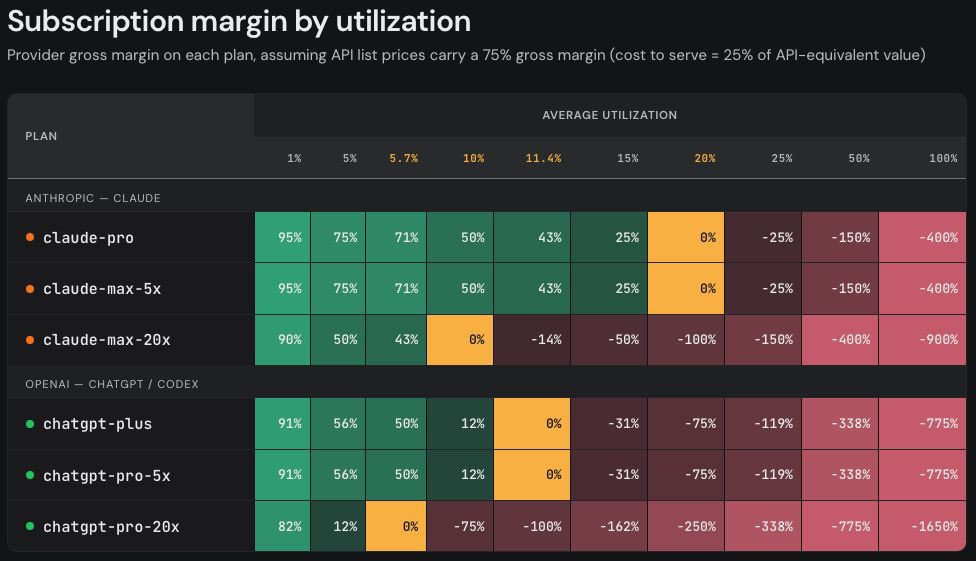

This chart from SemiAnalysis highlights one of the most misunderstood aspects of the AI industry today: revenue growth does not necessarily translate into profitability.

The market often assumes that a $20-200 monthly AI subscription is an extraordinarily high-margin software product. Historically that would be true. Traditional SaaS companies might generate 70-90% gross margins because serving an additional user costs almost nothing. Frontier AI is different. Every query consumes expensive GPUs, power, networking, and inference capacity.

The chart suggests that profitability is highly sensitive to user behavior. At low utilization levels, both OpenAI and Anthropic generate exceptional gross margins. However, as users increasingly rely on AI for coding, research, agent workflows, and long-context reasoning, margins deteriorate rapidly and can even turn deeply negative.

This is particularly important because AI adoption appears to be following a familiar pattern. Most users initially experiment lightly, but power users tend to expand usage dramatically over time. The more useful models become, the more inference they consume. Ironically, better products can create margin pressure rather than margin expansion.

The chart also helps explain why the industry is racing toward usage-based pricing, rate limits, premium tiers, and agent-specific subscriptions. Unlimited access sounds attractive from a marketing perspective, but frontier reasoning models can burn enormous amounts of compute. If a small percentage of users consume orders of magnitude more tokens than average, subscription economics quickly become challenging.

From an investment perspective, the biggest takeaway is that AI may not resemble traditional software economics. The winners may not be the companies with the highest subscription growth, but the companies that can continually reduce inference costs faster than user demand grows.

This is why every frontier lab is simultaneously pursuing two objectives: building smarter models and making them dramatically cheaper to run. Intelligence improvements alone are insufficient if inference costs grow faster than monetization.

The chart also reinforces why the infrastructure layer remains so attractive. Whether OpenAI, Anthropic, Google, xAI, DeepSeek, or someone else wins the model race, every additional query ultimately translates into demand for GPUs, HBM memory, networking equipment, power infrastructure, and data center capacity.

In many ways, this chart supports a view that AI is currently experiencing a version of Jevons Paradox. Costs per token are collapsing, yet total spending continues to rise because usage is growing even faster. The economic value is increasingly shifting toward those selling compute rather than those consuming it.

The implication is straightforward: the AI leaders may eventually become extraordinarily profitable businesses, but that outcome is not guaranteed. What is guaranteed is that exploding AI usage requires exponentially more infrastructure. That is why the most obvious beneficiaries of the AI boom remain the companies supplying the picks and shovels of the ecosystem.

The question is no longer whether demand exists. The question is who ultimately captures the economic rents generated by that demand. Today, the evidence increasingly suggests that the infrastructure providers are capturing a larger share of those rents than the model providers themselves.

1

8

29

2,121

Prateek retweeted

India's Biggest Economic Challenge Is not Inflation, Oil, or War - It is an Unskilled Population Addicted to Distraction.

Every time oil prices rise, economists panic. Every time a war breaks out in the Middle East or Europe, television studios declare that India's economy is under threat. And yes, both matter. But neither represents India's greatest economic challenge. The real crisis is unfolding much closer to home.

It is a generation that spends more time consuming content than creating value. A workforce that debates geopolitics without mastering spreadsheets, artificial intelligence, coding, welding, precision manufacturing, sales, finance, communication, or even basic problem-solving. An economy where attention has become the most wasted national resource.

India is one of the youngest countries in the world. That should have been our greatest competitive advantage. Instead, we risk turning our demographic dividend into a demographic liability.

The Age of Endless Consumption

Never before has information been so accessible. Yet never before have so many people spent so much time learning so little. Hours disappear into political debates, celebrity gossip, cricket controversies, influencer reels, conspiracy theories, and outrage cycles that have absolutely no impact on an individual's earning potential. Ask someone how many hours they spent on social media last week. Then ask them how many hours they invested in acquiring a new professional skill. For many, the answer is uncomfortable. We have become experts at commenting on the economy while contributing very little to it.

Degrees Are Not Skills

India has no shortage of graduates. It has a shortage of employable graduates. Companies repeatedly report the same problem: vacancies exist, but suitable candidates are difficult to find. Not because people lack certificates. Because many lack practical skills. The world is rewarding competence, not credentials.

- Can you solve problems?

= Can you communicate effectively?

- Can you sell?

= Can you lead a team?

- Can you analyze data?

- Can you use AI to improve productivity instead of merely asking it amusing questions?

- Can you create something that another person is willing to pay for?

Those are the questions that determine economic success. Not the number of degrees hanging on a wall.

Attention Is the New Currency

The biggest theft today is not of money. It is of attention. Every notification fragments concentration. Every endless scroll delays mastery. Every hour spent consuming outrage is an hour not spent building expertise.

Modern economies reward deep work, specialized knowledge, creativity, and disciplined execution. Algorithms reward emotional reactions. Unfortunately, millions choose the algorithm.

The Coming Divide

Artificial intelligence is not replacing everyone. It is replacing people who refuse to learn. The future will belong to workers who continuously upgrade themselves. Those who combine human judgment with technological tools will become dramatically more productive. Those who stop learning will find themselves competing for fewer opportunities at lower wages. The divide will not be between rich and poor. It will increasingly be between skilled and unskilled.

National Growth Begins With Individual Discipline

Governments can build highways. Businesses can build factories. Universities can build campuses. But none of them can force an individual to develop skills. Economic transformation begins with personal responsibility. Spend one less hour arguing online. Spend one more hour learning. Read instead of scrolling. Build instead of complaining. Acquire one valuable skill every year. Become indispensable.

If millions of Indians made that simple choice, the country's economic trajectory would change more profoundly than any fiscal stimulus, any election promise, or any temporary fall in oil prices.

Wars will end. Oil prices will rise and fall. Markets will recover. But a nation that neglects skill development while surrendering its attention to endless distraction will struggle long after those headlines have disappeared.

The strongest economy is not built by the loudest voices. It is built by the most capable people.

#JaiHind

176

756

2,166

134,452

The Complexity of the Semiconductor Global Supply Chain youtu.be/Gj5liYnpTeM?si=dDfj… via @YouTube

5

Prateek retweeted

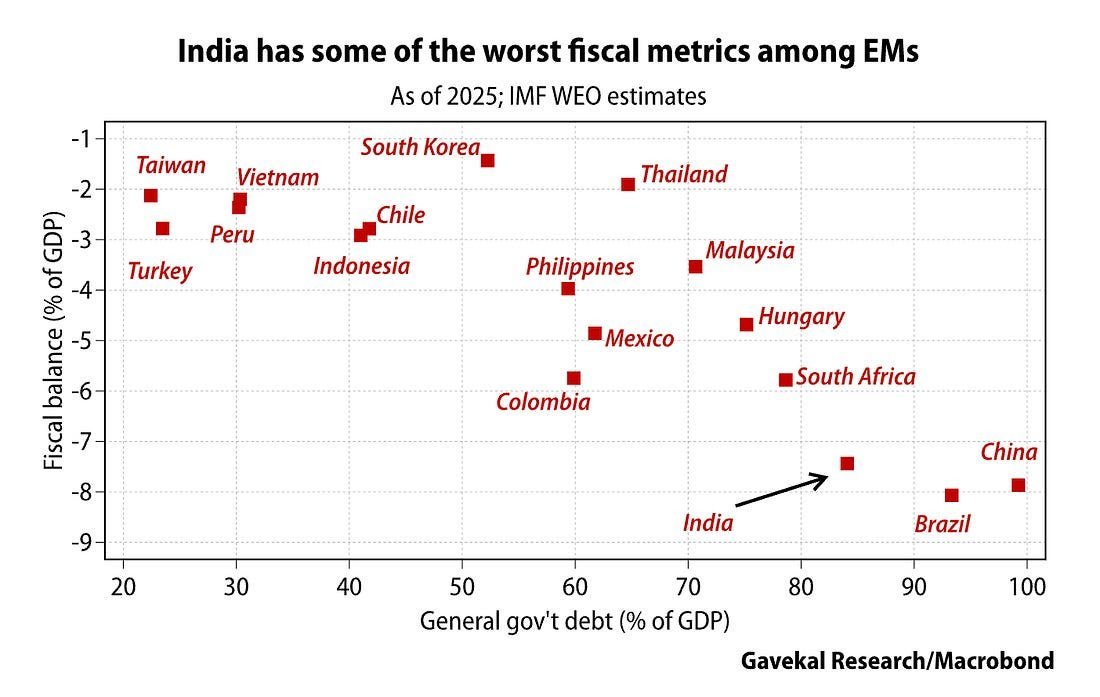

India also has some of the “worst” fiscal metrics of any EM’s and it does not have the trade surplus to “offset” this.

2

1

9

1,464

Indian industry is at a crossroads — it needs to look at longer horizons

indianexpress.com/article/op… via @IndianExpress

1

R&D underspending in India has no one cause. It’s systemic as well as cultural indianexpress.com/article/op… via @IndianExpress

1

1

2

Prateek retweeted

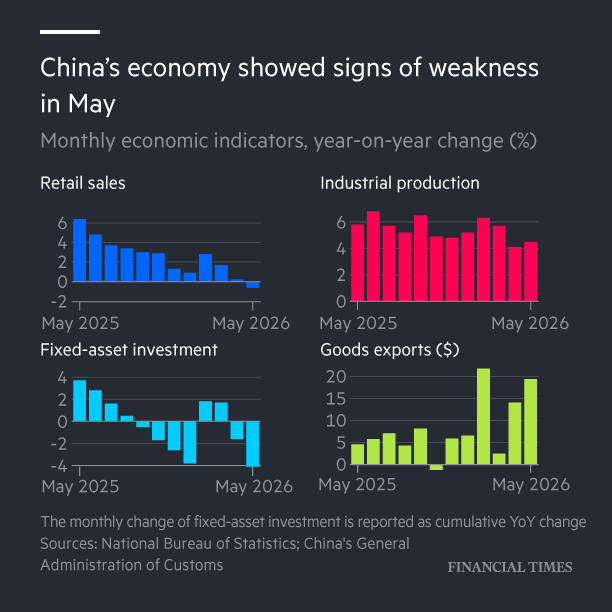

As @Aligarciaherrer has already observed, May's data shows ongoing domestic weakness (even increasing domestic weakness) even as China's exports continue to outperform global trade. It is an explosive combination.

1/

22h

China’s retail sales declined last month for the first time in more than three years and an investment slump deepened, as economic indicators flashed warning signs for the trajectory of the world’s second-biggest economy. ft.trib.al/q7S3gDJ?

ALT Chart showing year-on-year change of China’s monthly economic indicators

9

33

113

45,353

Prateek retweeted

Jun 15

📽️ What is Donald Trump's "Southern Highway"?

Here's the story of the secret trade route funnelling oil out of the Strait of Hormuz. Might it help explain why oil prices never went as stratospheric as some feared?

My latest primer on war in the Persian Gulf👇

16

67

279

49,232

Jun 16

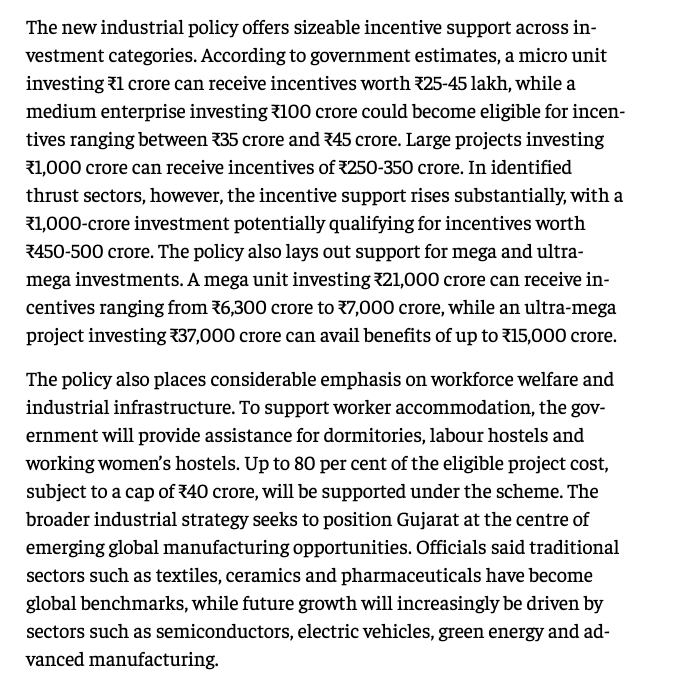

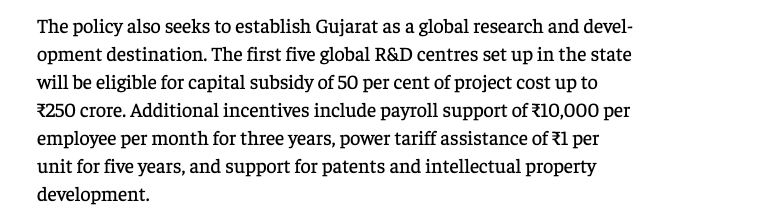

Gujarat’s new industry policy bets on flexibility to attract investors

thehindubusinessline.com/new…

10

Prateek retweeted

Jun 15

📽️I realise it's a bit odd to mark the launch of a podcast with a 13m deep dive screen.

But, well, maybe I'm just a bit odd.

Anyway here's the story of how LEDs saved the world. And why, paradoxically, they might NOT save the world.

Mind-blowing data on light, energy & more!👇

21

43

237

36,408

Jun 15

Real cost of freebies is the erosion in quality of public spending

business-standard.com/opinio…

3

Prateek retweeted

Jun 13

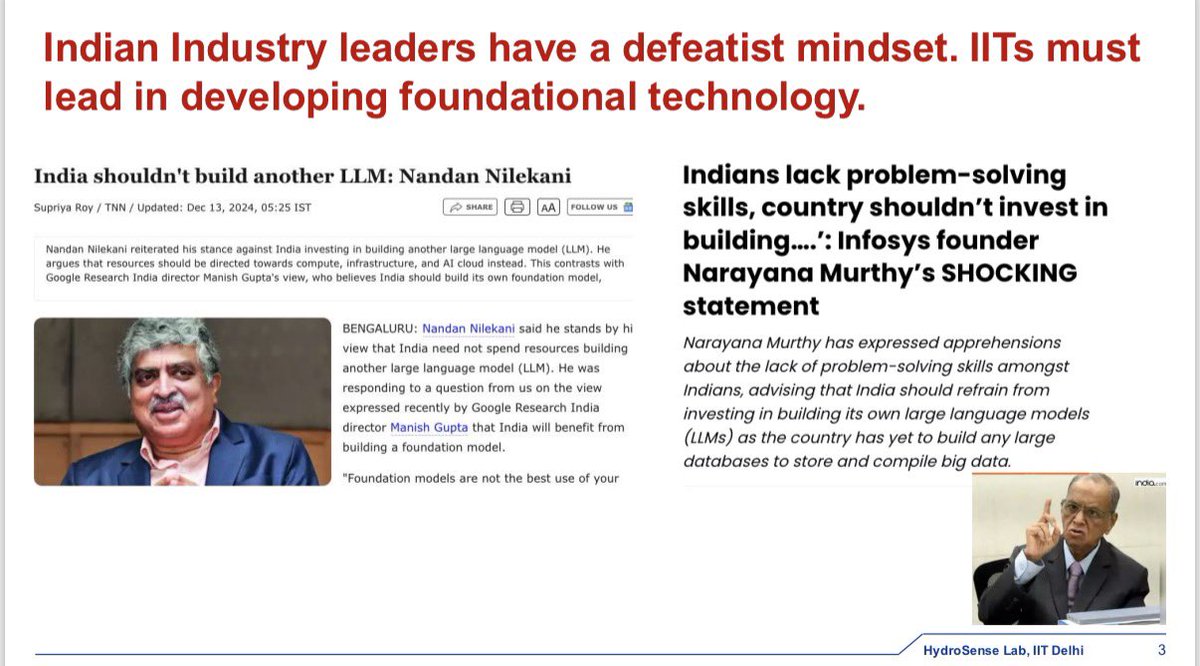

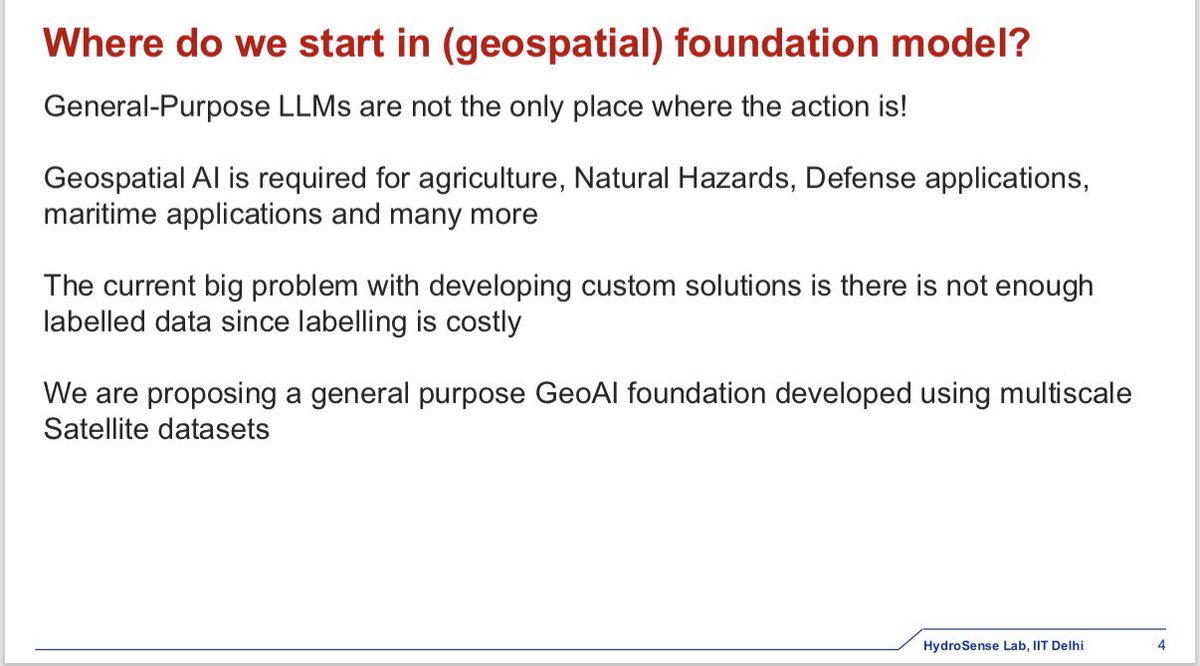

Govt has been incredibly supportive of our AI efforts through the IndiaAI Mission and other schemes. Zero support from any Indian industry. Thanks to NVIDIA, we trained India's first Geospatial Foundation Model (think of it like ChatGPT for satellite data) SLM using ISRO data. Dropping soon!

Apr 29

Last year, I was presenting to an internal team we had put together to develop a SOTA geospatial foundation model and this was a slide from that ppt. We have the talent and ambition, but the only entities that have helped us throughout this journey is govt IndiaAI mission and NVIDIA, who gave us priority compute after seeing our initial results. This is the kind of support that should have come from Indian IT behemoths. A country that can develop nuclear weapons and land on the moon is very well capable of developing SOTA models. But for that, we must first dream to be more than AI coolies.

20

192

820

37,103

Prateek retweeted

Jun 12

Excellent article on R&D Underspending in India.

Indian business caution is not simply a moral weakness or civilizational trait. It has been shaped by colonial disruption, protected markets, financial incentives, and political uncertainty, argues V Anantha Nageswaran.

12

72

220

24,935

Prateek retweeted

Jun 13

Electric car deliveries in India now stretch to as long as 3 months as OEMs struggle to match demand with production.

Waiting periods have widened for high-demand EV models, while automakers continue expanding capacity and localising battery and component supply chains.

2

23

124

6,418

Jun 12

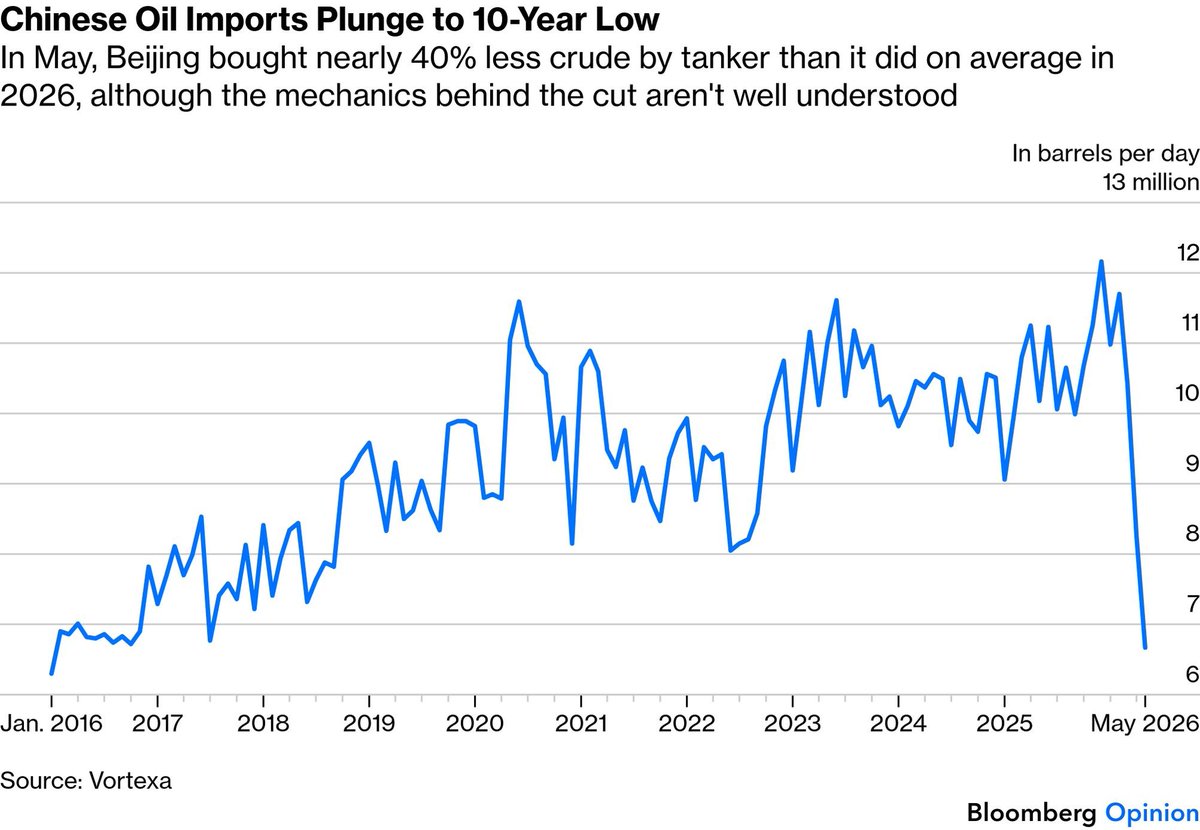

Even as the war in Iran drags on, oil prices have remained well below expectations.

Last month, China imported 6.7 million barrels a day of crude via tanker, down nearly 40% from the 2025 average.

bloomberg.com/opinion/articl…

19

Prateek retweeted

Jun 11

Freebies carry a heavy opportunity cost.

Every rupee spent on politically attractive transfers is a rupee not spent on education, health, infrastructure, contract enforcement, policing, local services, and state capacity.

1

23

95

1,944

Prateek retweeted

Indian States Just Posted Their Slowest Capex Start in Years. The Numbers Are Brutal.

22 states. ₹10.61 trillion capex budget for FY27. Amount spent in April: 1.85%.

Last April it was 2.26%. Actual spending shrank 11% in absolute terms, even as budgets grew 9.3%.

Now the scoreboard:

Kerala spent 22.31% of its annual capex in one month. Haryana 12.92%.

UP, India's largest capex budget at ₹1.94 trillion, spent 0.01%. That is ₹27 crore against a ₹2 lakh crore plan.

Maharashtra, Odisha and Jharkhand posted negative capex. Recoveries exceeded fresh spending. They effectively un-spent money.

Meanwhile the Centre exhausted 15.5% of its capex target in the same month.

The Centre is sprinting. The states are still tying their shoelaces. And states control nearly half of India's public capex engine.

The infra cycle everyone is pricing in runs through state treasuries. April says the engine has not started.

2

1

18

1,166

Prateek retweeted

Stunning images of the upcoming state-of-the-art convention and exhibition hub by 2031 at Bangalore AirPort City. Prestige group is investigating close to ₹1800Cr to build the same.

Development will luxury hotels under the St Regis and Marriott Marquis brands

9

16

294

44,572

Jun 11

Oil market defies predictions of summer supply crunch

The reprieve has been driven largely by China, which traders believe cut its oil imports in May by roughly 5mn barrels a day

ft.com/content/78638fc1-8780… via @ft

5