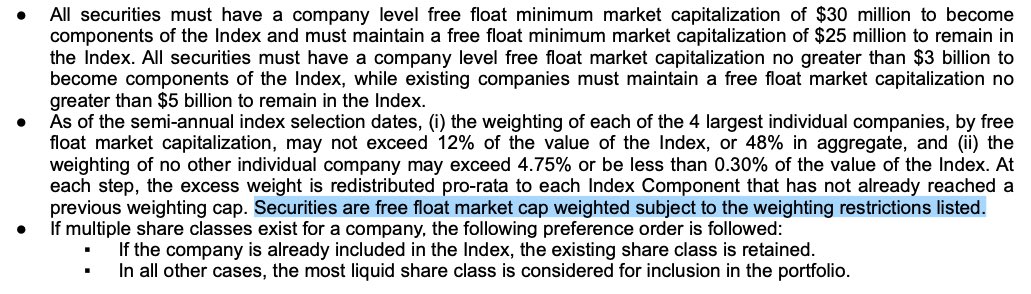

Joined April 2020

- Tweets 852

- Following 801

- Followers 152

- Likes 12,500

11 Photos and videos

prosenstrom retweeted

May 30

President Trump is unleashing the American Nuclear Renaissance—aiming to have multiple nuclear reactors critical by July 4th on our nation's 250th anniversary.

@SecretaryWright: “This summer you will see multiple next generation nuclear reactors running...America is back!"

130

664

3,541

282,142

May 3

⚛️ San'ao 2 just cleared hot functional testing — another practical step in China's reactor buildout, not a headline-grabbing one, but the kind that matters for future uranium demand. $IMAGE world-nuclear-news.org/artic…

Hot tests simulate operating temperatures before fuel loading and verify key coolant and safety systems. CGN says San'ao 2 completed the stage 51.9 months after first concrete, following cold tests in October.

Commissioning milestones are where nuclear growth moves from policy slide deck to actual fuel-loading queue. 📋

#uranium #nuclear #China

1

52

May 3

⚛️ Bangladesh has started fuel loading at Rooppur Unit 1, moving its first nuclear power plant into the startup phase. world-nuclear-news.org/artic…

This is the moment a project stops being just concrete, steel and long timelines, and starts becoming part of the power system.

Fuel loading is expected to take ~45 days, followed by minimum controllable power, staged testing, and ramp-up. Another data point for the bigger uranium story: new reactors are still entering the fleet, especially in growth markets where reliable baseload power is not optional.

For the fuel cycle, every new core matters. Initial loads are large, recurring reloads follow, and demand gets a little less theoretical. 📊

$SAID $IMAGE #uranium #nuclearenergy

23

May 3

⚛️ $AEC keeps moving JD-8 from 'nice optionality' toward actual restart potential: permit amendment submitted after addressing DOE Colorado DRMS comments. anfieldenergy.com/anfield-en…

Target remains potential approval/mobilization in mid-2026, with restart aimed for H2 2026. The interesting part is the hub-and-spoke setup: JD-8 material would feed Shootaring Canyon, one of just three licensed conventional uranium mills in the U.S.

In this sector, pounds matter. But permitted infrastructure and regulatory sequencing matter first. 📋

#uranium #nuclear #U3O8

55

May 3

📋 $AEC gets lender consent from Extract for the proposed B.R.S. acquisition, paying 50k shares 500k warrants at C$12.50 expiring Sept. 2028. anfieldenergy.com/anfield-en…

Not a thesis-changing headline by itself, but worth noting: the credit facility stays central to Anfield’s capital structure, and any warrant exercise proceeds go back toward repaying principal while the facility is outstanding.

Small-cap uranium development is often less about one big catalyst and more about financing mechanics, asset consolidation, and keeping optionality alive. This is one of those plumbing updates. ⚛️

#uranium #nuclear #U3O8

64

May 3

⚛️ Anfield $AEC is moving SM-18 toward underground drilling in Colorado, with the NOI now submitted and a Plan of Operations targeted later this year.

The key here is not a flashy discovery headline. It is permitting resource verification reuse of existing underground infrastructure.

SM-18 would be the fourth mine in Anfield's hub-and-spoke plan alongside Velvet-Wood, Slick Rock and JD-8. For a uranium-vanadium developer, that portfolio sequencing matters. Optionality is good; permitted, drill-ready optionality is better. 📋

Still early-stage execution risk, but this is the kind of incremental de-risking the market should track closely.

#Uranium #NuclearEnergy #Vanadium

anfieldenergy.com/anfield-en…

71

May 3

⚛️ $JAGU has dropped its April 2026 investor deck, giving the market a fresh look at Jaguar Uranium’s positioning on the NYSE American. jaguaruranium.com/wp-content…

For early-stage uranium stories, the deck is usually less about today’s cash flow and more about land package, technical credibility, funding path, and how management frames the cycle. Worth reading with the usual filter: presentation claims are inputs, not conclusions. 📋

#uranium #nuclear #investing

119

May 3

⚛️ $MYRUF brings in Eric Miller as Strategic Advisor for U.S. critical minerals policy, aiming to push Copper Mountain through the increasingly relevant maze of DPA Title III, DOE programs, permitting reform, and state/federal support.

For a Wyoming uranium project, technical geology is only part of the equation. Accessing the policy toolkit now forming around domestic nuclear fuel supply may matter just as much.

The U.S. wants more secure uranium supply. Companies that can actually navigate the agency, funding, and permitting channels will have an edge. Dry, bureaucratic stuff. Also potentially very valuable. 📋

#Uranium #NuclearEnergy #CriticalMinerals

myriaduranium.com/myriad-ura…

56

May 3

⚛️ $MYRUF bringing in Eric Miller is a policy-side move, not a geology headline. investingnews.com/myriad-ura…

Copper Mountain sits in Wyoming, in a uranium market where U.S. supply security is moving from talking point to budget line item. DPA Title III, DOE programs, permitting reform, interagency coordination — these are dry acronyms, but they matter when domestic pounds are scarce.

For a junior, the question is whether the right advisor can turn policy tailwinds into actual project momentum. That is the part to watch. 📋

#uranium #nuclear #criticalminerals

51

May 3

⚛️ Ur-Energy has started capturing uranium-bearing solution from Mine Unit 1 at Shirley Basin. For $UREN, this is the key transition: from permitted project buildout to active ISR operations in Wyoming.

Loaded resin is expected to move to Lost Creek this summer, pending final inspection/approval. That matters because it leverages existing downstream infrastructure instead of waiting on a full standalone processing build.

Small step in global supply terms, meaningful step for US domestic uranium capacity. 📊

#uranium #nuclear #mining

world-nuclear-news.org/artic…

52

May 3

⚛️ $TCEC tightens up the earn-in terms at South Falcon East and lines up up to 2,500m of follow-up drilling at Fraser Lakes B for late summer 2026.

Not a discovery headline yet, but it is the kind of capital-efficiency improvement that matters for junior explorers: better path to the initial 51% interest, same total consideration for the full 75% earn-in, and more flexibility to put dollars into the ground.

In the Athabasca Basin, structure plus disciplined drilling is where the signal starts. Now the next data point is the summer program. 🔍

#Uranium #AthabascaBasin #NuclearEnergy

investingnews.com/terra-clea…

25

May 3

⚛️ Uranium spot held firm at $86.45/lb last week, up from $85.00, even as Friday activity cooled. That’s not a market falling apart. That’s a market digesting gains. purepoint.ca/spot-pricing-re…

15 spot deals. Just over 1.2M lbs U3O8 traded. $SPUT raised $118M in roughly two weeks and bought another 1M lbs since April 16.

The more interesting signal may be forward pricing: 3-year at $101 and 5-year at $108. Utilities are not just watching the spot screen anymore; the term curve is starting to show the same structural tightness.

Soft days happen. Supply discipline and real demand matter more. 📊

#uranium #nuclear #commodities

68

May 3

⚛️ Athabasca juniors are moving from paperwork to drill bits: Skyharbour partner Terra has improved South Falcon East earn-in terms and is lining up Fraser Lakes B follow-up drilling, while Stallion is back turning at Moonlite. $SYH $TCEC $STUD

This is the part of the cycle where optionality gets tested in the field. Improved earn-in economics matter, but the market will ultimately care about meters, targets, assays, and whether these deposits can show scale. Quietly constructive for Athabasca exploration sentiment. 📊

investingnews.com/despatch-o…

72

May 3

🔍 $STUD is back drilling at Moonlite after the April 1 incident, with ~1,900m completed of a planned 4,000m Phase 1 program. investingnews.com/stallion-u…

The useful part: every completed hole so far has hit significant alteration and structure, including ML26-001A cutting multiple fault zones in sandstone and basement rocks.

That is exactly what an early-stage Athabasca explorer needs to see before assays enter the conversation: evidence the plumbing system is there. Still exploration, still high risk, but not a nothingburger. 📊

#Uranium #AthabascaBasin #NuclearEnergy

17

May 3

⚛️ $AEC had the kind of 2025 uranium developers need: NASDAQ uplist, stronger board/finance bench, and key Velvet-Wood approvals moving it closer to U.S. production.

The market will still care about execution, financing, and timelines, but the direction is clear: domestic uranium supply is becoming a policy priority, and companies with permitted U.S. assets are getting more interesting.

Near-term production is where the sector’s PowerPoints meet the paperwork. 📋

#Uranium #NuclearEnergy #EnergySecurity

anfieldenergy.com/anfield-en…

51

May 3

⚛️ Kudankulam Unit 3 just moved into safety system flushing, the final stage before reactor assembly. Small milestone, big signal: India’s nuclear buildout is steadily converting paper GW into steel, systems testing, and eventually fuel demand. $SAID

For uranium investors, these commissioning steps matter because reactor growth is not theoretical once projects enter the cold/hot run sequence. It is slow, procedural, and about as glamorous as rinsing pipes with demineralised water — but this is how baseload capacity gets built. 📋

India remains one of the more important long-cycle demand stories in nuclear: rising power needs, energy security priorities, and a willingness to keep adding reactors despite the usual construction timelines.

world-nuclear-news.org/artic…

95

May 3

⚛️ $AEU is putting real metres into Muntanga: 30,000m across resource growth first-pass discovery targets in Zambia. stockhead.com.au/resources/a…

The base is now 58.8Mlb U3O8 after a 24% resource lift, and this campaign is aimed at testing whether Muntanga is still under-drilled rather than fully defined.

Key points: two rigs, geophysics crews, infill at Chisebuka, and maiden drilling at Namakande Muntanga North. Those targets matter because management says they share similar signatures with known mineralisation.

Exploration metres do not equal pounds, of course. But in uranium, scale plus active drilling is exactly what the market tends to watch when the macro backdrop is supportive. 📊

#uranium #U3O8 #ASX

46

prosenstrom retweeted

May 1

CGN Mining has the kind of uranium headline retail investors want to see: a stronger contract book at $89.20/lb.

But here’s the problem.

The uranium it actually delivered in Q1 settled at just $64.27/lb.

That gap is the whole story.

Better uranium prices are showing up on paper before they show up in clean shareholder earnings. Add Kazakhstan mine friction, acid supply issues, taxes and minority ownership — and this becomes a lot less simple than “uranium up, stock up.”

I broke down what CGN’s 2026 updates really mean, what is improving, and what still has to prove out before the bull case deserves more trust.

Read it before the market turns the headline into a lazy story.

1

5

10

1,284

May 1

⚛️ Strong expansion at the Nova Discovery in the Athabasca Basin. purepoint.ca/purepoint-urani…

Purepoint Uranium has extended the geological contact to approximately 1km in strike length following a 5,210m winter drill program. With peak downhole probe readings of 73,100 cps and previous assays reaching 8.1% U₃O₈, the pending results from this campaign are a key data point to watch.

Next milestones for the Dorado JV:

- Spring: Airborne MobileMT survey

- June: Regional drilling resumes

$PTUUF $ISO #Uranium #Mining #AthabascaBasin

31