🧾Crypto Tax Adviser & CASP CEO | Co-Founder @Validvent | @DAAA_at Board Member | Former Law Faculty Member @univienna | tweet about Bitcoin, DeFi, Art & Gaming

Joined June 2009

- Tweets 3,387

- Following 791

- Followers 1,012

- Likes 4,107

323 Photos and videos

Pinned Tweet

Apr 16

YESSS - we did it 🇪🇺

Validvent is officially a MiCAR CASP 🚀🚀🚀

And yes - this one is personal.

Robby Schwertner [CryptoRobby]🦋 and I started back in 2018 - no licenses, no big structure, just curiosity and conviction.

Researching, teaching, speaking about blockchain when most people still thought it was a niche topic.

Advising on crypto tax, classifying millions of transactions, representing crypto matters in court, leading defense audits, executing OTC deals, curating digital art exhibitions, transforming museums into hubs of innovation and building trust step by step.

Hosting meetups, supporting projects, taking advisory and board roles along the way.

No financing round. We followed the market - through the ups and downs. Kept building.

Today we are:

👉 a European independent Crypto Asset Advisory firm

Not a platform.

Not an exchange.

Not here to shill anyone‘s tokens.

We believe in self-hosted investing.

We believe that everybody should have FULL control over their assets.

We believe in financial sovereignty. Resilience. Freedom. 🕊️

MiCAR is a milestone - not the finish line. A big step for the industry and a major boost for the ecosystem.

But what matters more:

We stayed true to the original idea of Bitcoin.

No intermediaries.

No custody lock-ins.

Just independent advice.

Big thanks to everyone who was part of this journey - the team, our partners and families, clients and everyone who supported us along the way 🙏

The future is decentralized 🧢

Apr 16

We just got the MiCAR CASP license 🇪🇺

Europe’s first independent Crypto Asset Advisory firm, not a platform. Self-hosted investing. No intermediaries. The future is decentralized.🚀

4

1

16

761

Georg Brameshuber 🧢 retweeted

Jun 12

Bitcoin Pizza Day Vienna 2026 was one for the books 🍕

340 attendees. Countless conversations. Great people, great pizza, and a fantastic atmosphere throughout the evening.

Thank you for joining us 🫶

📸 Relive the event and browse all photos:

validvent.com/global-bitcoin…

4

14

297

Georg Brameshuber 🧢 retweeted

Welche Krypto-Steuer-Frage brennt euch schon immer unter den Nägeln? 🔥

Postet sie auf Reddit! @FlorianWimmerAT (CEO von Blockpit) & @pyth_brc (Georg Brameshuber, Krypto-Steuerberater bei Validvent) beantworten sie dort heute von 18 bis 19 Uhr schriftlich.

Hier geht's zum Thread 👉reddit.com/r/FinanzenAT/comm…

Wir freuen uns auf spannende Fragen!

May 26

We’re joining r/FinanzenAT tomorrow for an AMA on crypto taxes in Austria together with @blockpit_io 🇦🇹

📅 May 27 | 18:00–19:00

We’ll discuss:

• Tax return 2025

• DAC8 reporting

• Crypto documentation

• DeFi & staking

• Austria’s growing role as a European crypto hub

1

3

463

May 26

AMA on Crypto Taxes tomorrow 18:00-19:00

May 26

We’re joining r/FinanzenAT tomorrow for an AMA on crypto taxes in Austria together with @blockpit_io 🇦🇹

📅 May 27 | 18:00–19:00

We’ll discuss:

• Tax return 2025

• DAC8 reporting

• Crypto documentation

• DeFi & staking

• Austria’s growing role as a European crypto hub

1

8

310

May 26

Ahead of @btcplusplus in Vienna this week you might have read Green’s critique of Bitcoin. While Green raises some valid points he is fundamentally wrong about Bitcoin’s appeal "fix the money".

Here is a thorough read on the points where most of us would probably agree with Green and a detailed outline of where we definitely do not. It's also a great roll down on why Bitcoin (M0) "Needs" Bitcredit (M1)

blog.bitcr.org/p/michael-gre…

1

8

531

May 19

GM everyone!

Next Tuesday, 26 May, from 2 pm to 5 pm, we are holding a group testing session for the new @bitcr_org wallet at weXelerate in 1020 Vienna.

We need 20 volunteers. The reward is €50 in BTC free drinks and pizza.

Please fill in this form and, if you are selected, we will contact you next Monday. cryptpad.fr/form/#/2/form/vi…

1

3

159

May 18

Great discussions today at the Crypto Compliance & Legal Roundtable in Vienna hosted by @Solidus_Labs and @EY & @EYLaw during the Vienna Blockchain Conference.

Vienna continues to position itself as a serious hub for compliant digital asset innovation attracting international players ready to build for the long term 🇦🇹

The list of global leading plattforms with an EU HQ setup in Austria is getting really impressive

Bitpanda

Bybit

Kucoin

Bitget

BingX

Whitebit

OSL

Upbit

Kraken

1

4

167

May 18

🇦🇹 BMF State Secretary says the FinTech Advisory Board and FinTech Sandbox in 2018 was key for success for thriving Austrian Bitcoin & Crypto Ecosystem 6y later

2

128

May 18

Vienna Stock Exchange holds a significant stake in the CZ Prague Stock Exchange

May 18

Opening of the DAAA Diagital Asset Forum Vienna & Vienna Blockchain Week by CEO Boschan Vienna Stock Exchange

4

157

May 18

Opening of the DAAA Diagital Asset Forum Vienna & Vienna Blockchain Week by CEO Boschan Vienna Stock Exchange

5

285

May 17

We’ve had our CASP license for just one month - and already five crypto companies have approached us asking whether we would acquire their stack through an asset or share deal because they will not be MiCA compliant by July 1 and are now looking for some form of exit.

Some developments don’t really come as a surprise. This one didn’t.

MiCA did not “kill” the European crypto industry. What it did was force the market to distinguish between narrative, real technology and sustainable financial infrastructure.

Web3 used to work almost like a utility. You picked a provider, plugged into an API and moved on. It did not really matter where the company was based. Now it does.

Regulation has become local. Supervision is continuous. And the integrations that actually matter with banks, payment providers and merchants go far beyond a simple API connection.

What changed with MiCA is what the market now requires.

Today, local presence matters in a way it never did before. From the few crypto companies left in Europe, even fewer are able to support the full lifecycle properly: euros into crypto, execution, custody, compliance, reporting, governance, payments infrastructure and integrations that actually hold up under scrutiny.

The uncomfortable reality is that the barrier to remain in this industry is becoming extremely high.

Compliance, licensing, governance, cybersecurity, reporting and operational oversight now require enormous amounts of capital and resources. This increasingly means that only heavily capitalized players can survive long enough to scale.

And yet the industry still avoids confronting the core issue: if there is no market, there is no industry.

Tokenization alone does not create value. Without liquidity, interoperability, distribution, market structure and real secondary market access, many tokenized assets are still just more expensive databases wrapped in blockchain infrastructure.

The technology already exists. That is no longer the problem.

MiCA’s original goal was a very good one: protecting customers from rug pulls and insolvent platforms. Investor protection is necessary. Regulatory maturity is necessary.

But does protecting customers really require shutting down hundreds of European crypto companies? Does banning USDT really serve the interests of users?

In my humble opinion, the current implementation of MiCA does not sufficiently serve the needs of European customers, founders or innovation.

Europe is entering a new phase: fewer players, but more specialized, supervised and integrated into the traditional financial system.

That shift was probably inevitable.

The real question is whether Europe will still leave enough room for innovation once the dust settles.

1

9

202

May 17

The longer I work in this industry the more I believe the next phase of Bitcoin & Crypto will be built less on hype - and much more on trust, infrastructure and - yes - "clarity" 😇

1

6

172

Georg Brameshuber 🧢 retweeted

15 years ago, 10,000 BTC bought two pizzas. Next Friday, we celebrate how far we've come. 🍕

@standwithcrypto state chapter presidents and @Pizza_DAO are hosting pizza parties across the U.S. on May 22 for Bitcoin Pizza Day.

Find your city below.

globalpizza.party/#cities

1

12

63

2,711

May 16

🇩🇪 Eine unechte Rückwirkung und damit rückwirkende Abschaffung der Haltefrist ist möglich?

Aber wie geht das und was heißt das genau?

👇Hier am Beispiel einer angenommenen zukünftigen verpflichtenden Besteuerung von (echten) Airdrops beim Zufluss erklärt (Fall der > echten Rückwirkung<) und einem Kauf von BTC nach dem 01.01.2026 (Fall der >unechten Rückwirkung<)

May 15

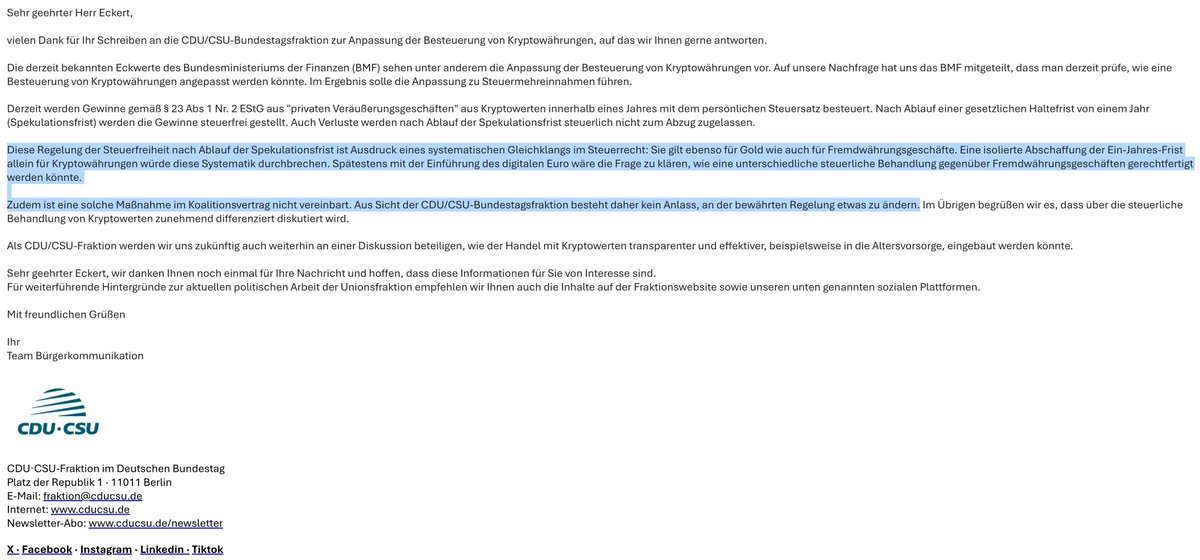

Das dürfte alle Krypto-Anleger interessieren. Die CDU/CSU-Fraktion im Deutschen Bundestag hat auf meine Anfrage geantwortet, wie die Fraktion zur geplanten Abschaffung der Haltefrist steht. Hier ein Auszug aus der Mail:

"Eine isolierte Abschaffung der Ein-Jahres-Frist allein für Kryptowährungen würde diese Systematik durchbrechen. Spätestens mit der Einführung des digitalen Euro wäre die Frage zu klären, wie eine unterschiedliche steuerliche Behandlung gegenüber Fremdwährungsgeschäften gerechtfertigt werden könnte.

Zudem ist eine solche Maßnahme im Koalitionsvertrag nicht vereinbart. Aus Sicht der CDU/CSU-Bundestagsfraktion besteht daher kein Anlass, an der bewährten Regelung etwas zu ändern." (Hervorhebung durch mich)

Team Bürgerkommunikation

CDU·CSU-Fraktion im Deutschen Bundestag

1

5

257

May 15

Everyday's news

May 15

Das dürfte alle Krypto-Anleger interessieren. Die CDU/CSU-Fraktion im Deutschen Bundestag hat auf meine Anfrage geantwortet, wie die Fraktion zur geplanten Abschaffung der Haltefrist steht. Hier ein Auszug aus der Mail:

"Eine isolierte Abschaffung der Ein-Jahres-Frist allein für Kryptowährungen würde diese Systematik durchbrechen. Spätestens mit der Einführung des digitalen Euro wäre die Frage zu klären, wie eine unterschiedliche steuerliche Behandlung gegenüber Fremdwährungsgeschäften gerechtfertigt werden könnte.

Zudem ist eine solche Maßnahme im Koalitionsvertrag nicht vereinbart. Aus Sicht der CDU/CSU-Bundestagsfraktion besteht daher kein Anlass, an der bewährten Regelung etwas zu ändern." (Hervorhebung durch mich)

Team Bürgerkommunikation

CDU·CSU-Fraktion im Deutschen Bundestag

3

222

May 15

LFG 🍕Cannot wait

One week to go 🥳

May 15

🗺️🍕🥳

Just one week until Bitcoin Pizza Day! Find your local event at globalpizza.party 🔍

🇦🇹 Last year's party in Vienna. Hosted by @Tschuuuuly:

8

173

May 15

One Week To Go 🍕

May 15

One week till we celebrate the Global Bitcoin Pizza Party at MAK's Säulenhalle 😋

🕓 16:00 Doors open

🎨 16:00–18:00 Exhibition "Soft Image, Brittle Grounds" by Felix Lenz 🚶

📺 Livestreams from 400 cities worldwide

🍕 Free Pizza & free Drinks 🥤

See you at MAK!

1

3

107

May 14

🇺🇸 Big Day

Congrats to everybody who made that happen

The Clarity Act passed by the Senate Banking Committee is a strong bipartisan compromise to provide the regulatory certainty needed to advance financial innovation. I was proud to work with my colleagues on both sides of the aisle for the past few months, and more work remains in the weeks ahead to make this legislation even better. Let’s get it done.

2

104