Investing in a concentrated portfolio of the highest quality companies in the world. All opinions my own. Not financial advice.

Joined July 2022

- Tweets 8,693

- Following 1,188

- Followers 9,926

- Likes 16,837

1,057 Photos and videos

Pinned Tweet

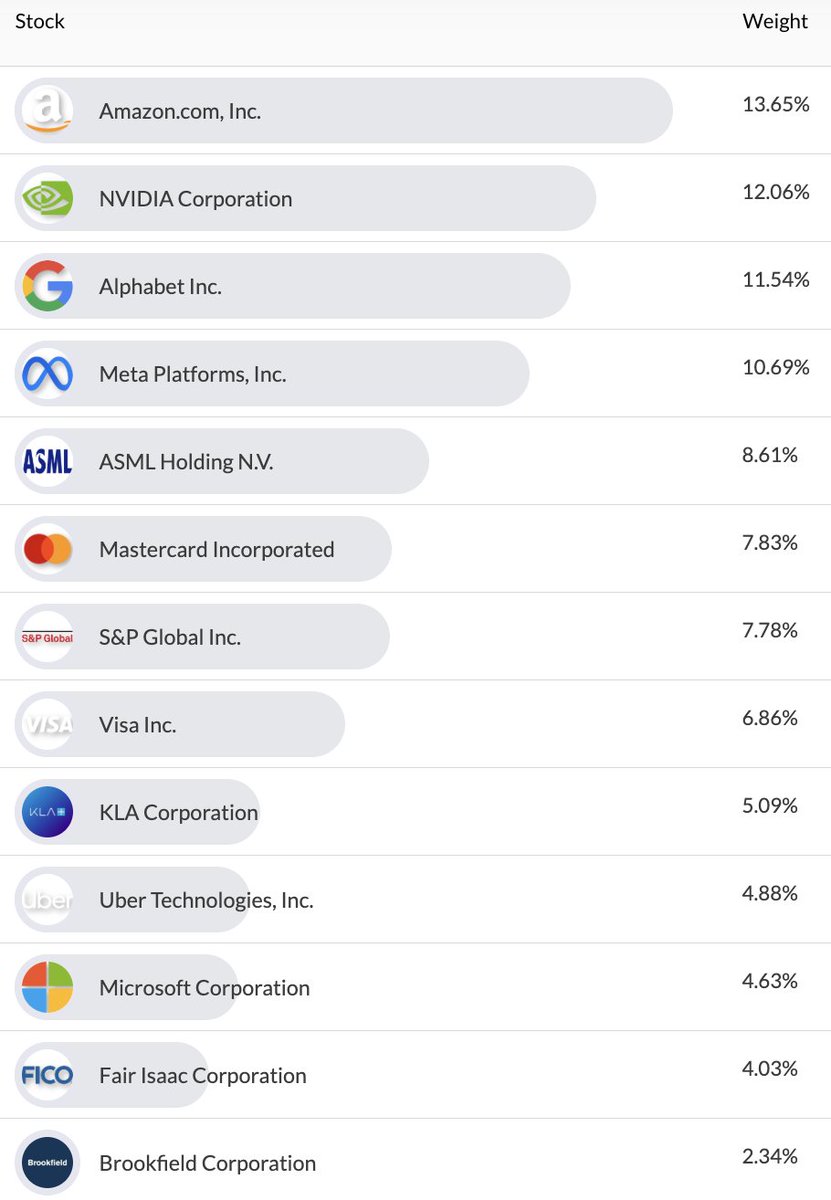

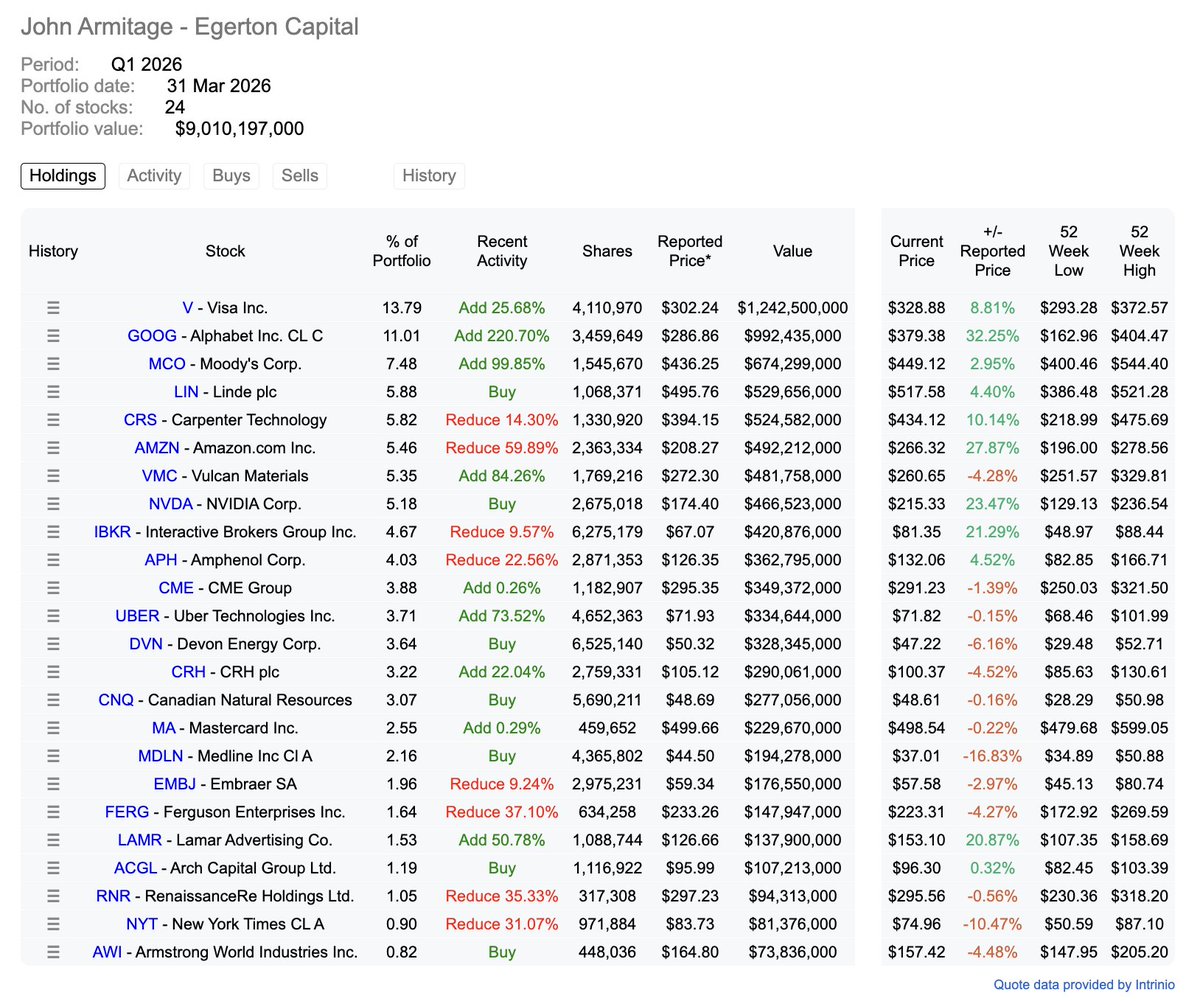

End of May 2026 portfolio update.

My portfolio contains exceptional, world-class businesses. I avoid speculative junk, and instead focus on dominant leaders with massive competitive moats, high returns on capital, and long runways for growth.

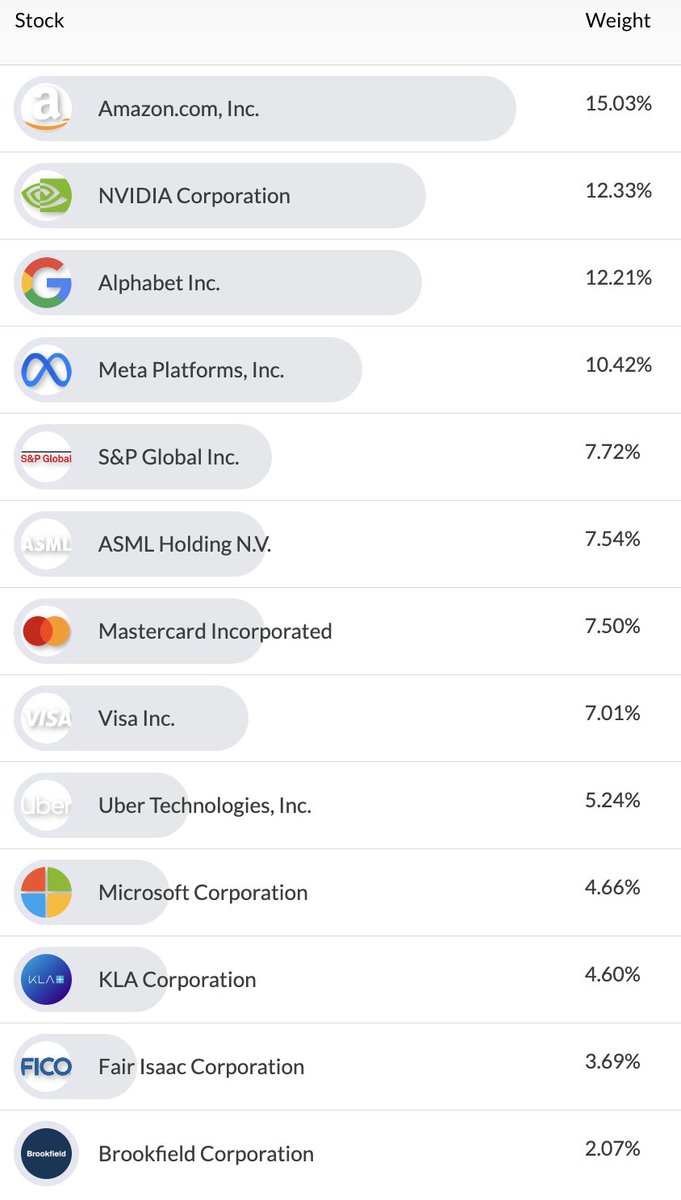

At the core, I own unbeatable monopolies and toll-booth businesses. Visa and Mastercard act as toll booths on global spending, while S&P Global and FICO dominate the essential data and credit-rating markets. These companies require very little cash to run, giving them immense pricing power and elite profitability.

I'm also heavily backed by the ultimate tech and AI infrastructure. ASML and KLA are literal gatekeepers for semiconductor manufacturing. Advanced chips can't be made without them. Meanwhile, Microsoft, Alphabet, Meta, and Amazon control the digital real estate and cloud networks that power the modern global economy. Nvidia is the undisputed king of AI computing infrastructure. Structural tailwinds makes these companies incredible long-term compounders.

Brookfield is a masterclass in capital allocation. They invest in hard, essential assets (infrastructure, renewable energy, real estate), and have a long history of compounding value for shareholders.

This past month, I continued to add to Meta, Mastercard, S&P Global, and Brookfield.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep dive equity research into my holdings (as well as other compounding machines), and highly relevant thematic trends shaping today's markets. Link here and in bio: qualityequities.substack.com

$GOOG

$META

$NVDA

$AMZN

$V

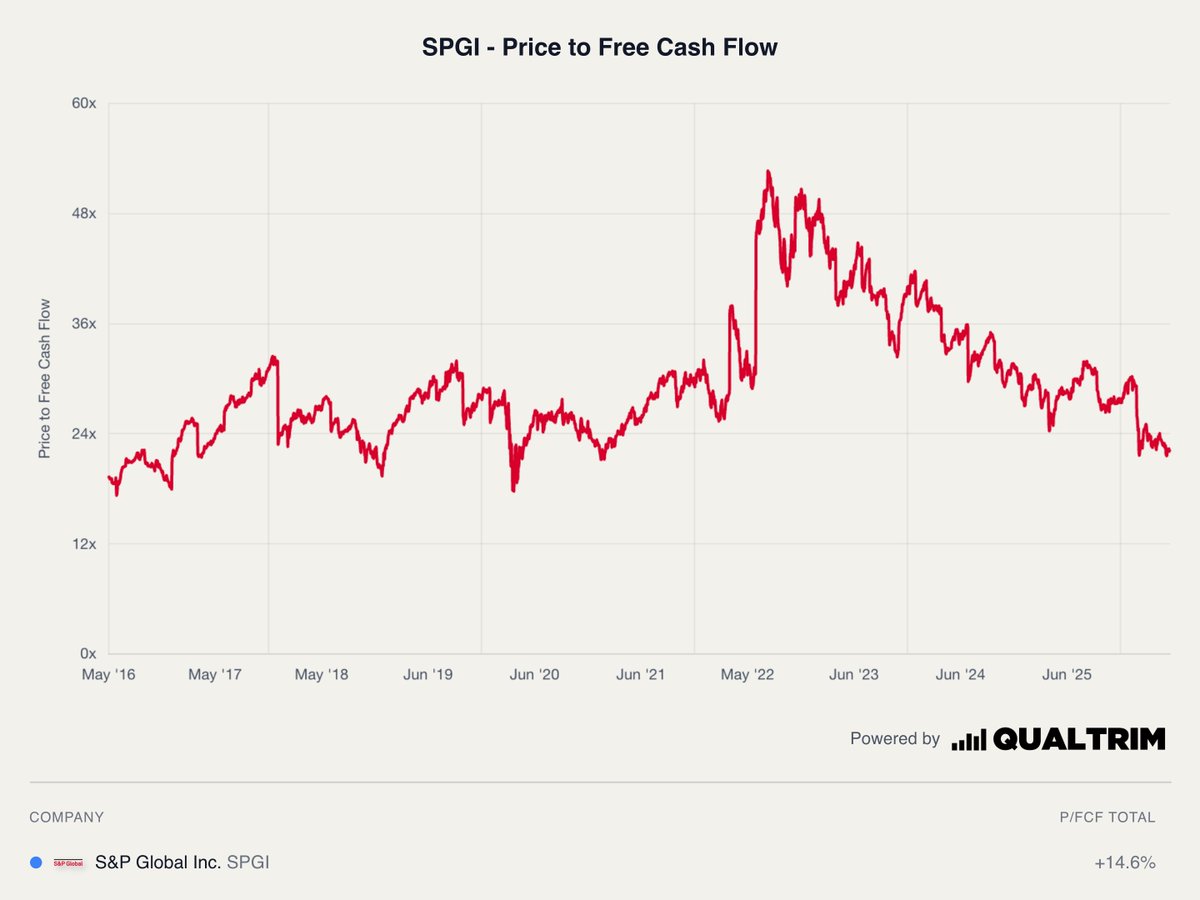

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

Minor changes to the portfolio in April 2026.

Added to $META Meta, $MA Mastercard, $AMZN Amazon, $BN Brookfield, and $FICO FICO.

Only buys.

The portfolio is built around some of the world’s strongest, highest‑moat platforms, with a heavy tilt toward scalable, asset‑light, data and network effects businesses.

These companies benefit from immense economies of scale, proprietary infrastructure, pricing power, and data advantages that reinforce their moats as they grow. Their revenue bases skew toward recurring or highly repeat‑purchase models (cloud subscriptions, advertising, developer and enterprise contracts, etc.) with strong operating leverage, making incremental margins very attractive as utilization increases.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep equity research into my holdings (as well as other compounding machines) and highly relevant thematic trends shaping today's markets. Link here and in bio: qualityequities.substack.com

$GOOG

$META

$NVDA

$AMZN

$V

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

8

3

49

5,096

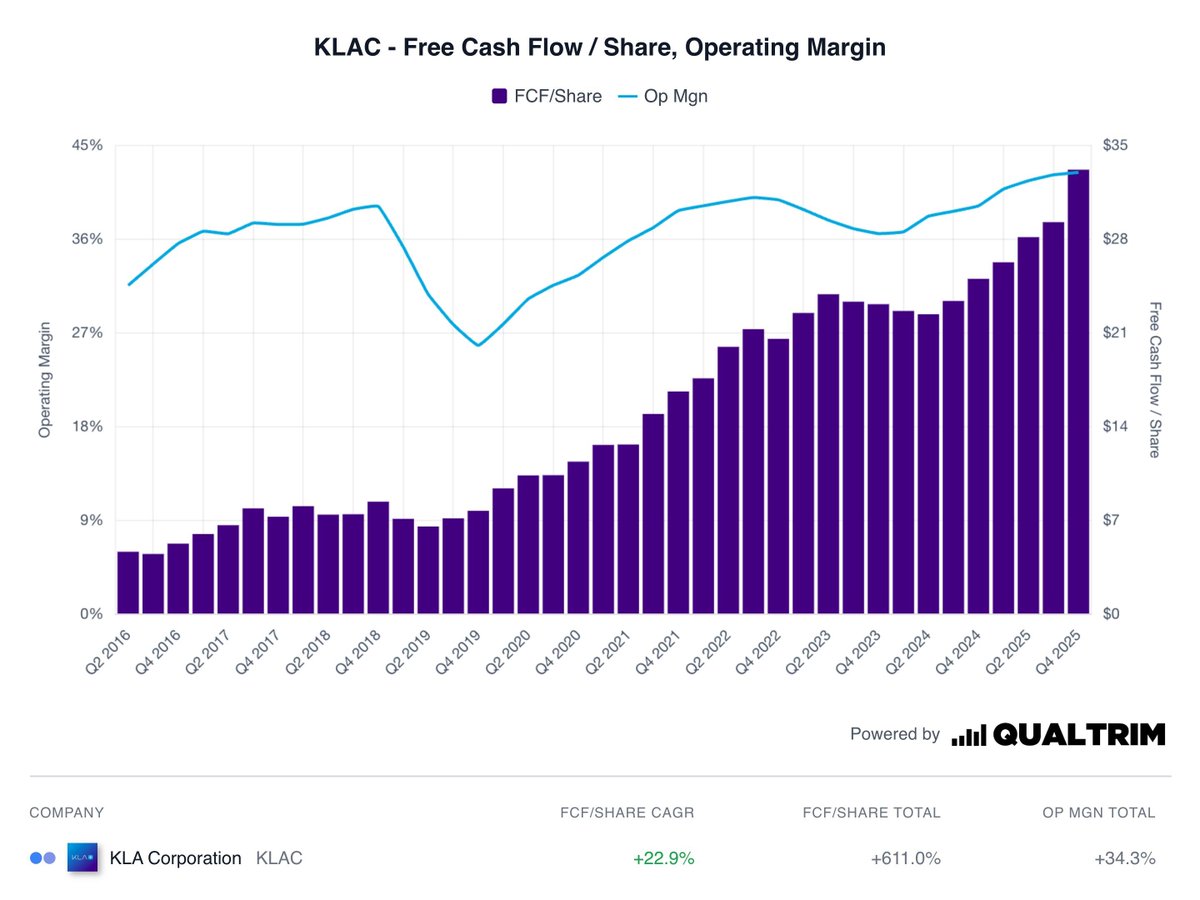

$KLAC KLA is an elite, asset-light royalty business on human technological progress. You are not betting on which specific AI application or smartphone brand wins; you are betting that as long as humanity demands smaller, faster, and more powerful microchips, manufacturers will have to pay the KLA toll to ensure those chips actually work.

Deep-dive coming tomorrow morning.

Feb 24

Alongside $ASML ASML, $KLAC KLA operates as another toll booth of the semiconductor industry.

They dominate the niche of process control, providing the essential inspection tools that ensure microchips actually work.

As chips become more complex due to the AI revolution, the margin for error narrows, making KLA’s services indispensable.

With over 50% market share and operating margins exceeding 40%, the company is a high-quality compounding machine.

Their massive moat is reinforced by a high-margin service business that generates steady, recurring cash flow regardless of economic cycles.

Keep Looking Ahead.

1

3

468

Jun 14

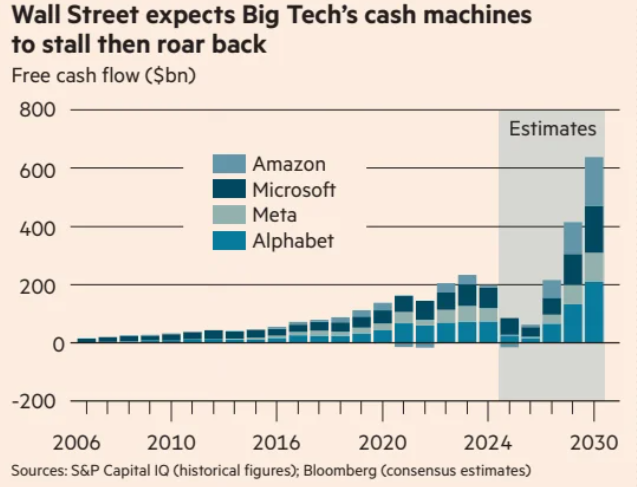

"Wall Street analysts’ projection for future free cash flow at the four hyperscalers we started with. It is expected to bottom out in 2027 — and then grow at a rate much faster than anything in the companies’ history."

$AMZN $MSFT $META $GOOG $GOOGL

Jun 13

AI is revolutionising the stock market ft.trib.al/N5fExVY

1

5

21

4,458

Jun 14

The decision to exit a position is the most consequential and least-discussed decision a long-term investor makes. The case for owning quality compounders has been made elsewhere. This piece addresses the harder question: when to stop owning them.

Read for free today: open.substack.com/pub/qualit…

Jun 13

What makes you sell a stock?

8

1,461

$TDG TransDigm deep-dive out now: open.substack.com/pub/qualit…

$TDG TransDigm sells the small, boring, mission-critical parts that keep aircraft flying...and owns the economics of those parts like almost no other industrial business.

The parts are cheap relative to the airplane but indispensable to it. ~90% of sales are proprietary, often sole-source, locked in by FAA certification. Once a part is designed onto a platform, it stays for the life of the aircraft — 25-30 years of high-margin aftermarket demand, ~55% of revenue.

On top sits a private-equity-style engine: acquire niche sole-source suppliers, apply value-based pricing, run lean and decentralized, fund it with leverage. The result — Q2 FY26: $2.54B sales, 52.6% EBITDA margin.

The same pricing power that drives the returns is the risk. DoD audits and "price gouging" accusations follow a business this good at extracting price.

Full deep-dive coming this Tuesday. Subscribe at: qualityequities.substack.com…

3

2

3

1,004

When the fundamentals accelerate but the market panics, quality investors pay attention.

Look at $FICO FICO:

Revenue growth has surged to a roaring 23%.

Meanwhile, its P/E multiple compressed from a peak of ~120x down to ~36x—well below its 5-year median of ~53x.

A strong moat with organic growth, wrapped in a rare valuation de-rating. Growth is accelerating, yet the price tag just got a lot cheaper.

2

17

4,856

BlackRock claims mega forces are reshaping investing.

Here's a summary:

Traditional investment methods are losing their edge. Long-term structural shifts—like the AI boom, changing demographics, global political tensions, and the energy transition—are reshaping the financial landscape. To navigate this, investors need to review their major portfolio decisions more frequently and always have a backup plan ready.

When it comes to AI, the smartest move isn't guessing which software company will win the race. Instead, focus on the "picks and shovels" that power the expansion. Companies providing semiconductors, data centers, and power systems are poised to win regardless of which tech giant comes out on top.

Geography matters less than business models. Instead of focusing on where a company's stock is listed, look deeply at what the company actually does and where its revenue comes from. High-quality businesses with strong earnings growth, particularly in the U.S. and in emerging markets that manufacture critical AI components, remain highly attractive.

On the bond side, avoid long-term government debt like U.S. Treasurys and Japanese government bonds. Rising inflation risks and heavy government borrowing make long-term government bonds a poor risk-reward trade. If you want income, look toward higher-yielding alternatives like U.S. agency mortgage-backed securities or emerging-market debt tied to strong commodities.

Finally, long-term private markets offer compelling opportunities. Infrastructure equity and private credit are seeing massive demand driven by the AI buildout and global supply chain shifts. However, selectivity is critical here, as the gap between the best and worst-performing private investments is widening.

1

4

983

Bernstein believes that quantum computing is the next major frontier in technology, acting as a specialized accelerator alongside traditional computer chips.

Instead of one company dominating the entire industry, the market will likely have multiple winners because different quantum technologies excel at different tasks.

While tech giants like $GOOG Google and $MSFT Microsoft are investing heavily, Bernstein highlights two smaller, specialized stocks with great risk-reward potential: $RGTI Rigetti Computing and $INFQ Infleqtion.

Because current stock prices reflect very low expectations for their future market share, any major success could lead to massive upside for investors.

Key Stock Highlights:

- Rigetti Computing: This company focuses on superconducting quantum technology. It is financially stable with roughly $590 million in cash and is making steady progress on its advanced chips. Wall Street analysts see potential for the stock to climb significantly from its recent price of around $21.

- Infleqtion: Operating in neutral-atom technology, Infleqtion is already generating revenue by combining quantum sensing with quantum computing. Analysts are highly optimistic about its future, especially due to a key partnership with Nvidia to integrate quantum tech with AI supercomputers.

Both stocks have shown strong momentum recently, making them attractive, high-upside options for investors looking to gain early exposure to the quantum computing sector.

In my view, this setup is highly speculative, and a disciplined quality investor wouldn't touch either of these stocks right now.

Quality investing is focused on finding companies with deeply entrenched moats (think high switching costs, strong network effects, or irreplaceable intangible assets.

As the Bernstein note explicitly states, it is "far too early...to declare an ultimate winner" and "different modalities bring distinct strengths." This means no one has a moat yet. The technology is in flux, and a competitor could introduce a brand-new architecture tomorrow that renders Rigetti’s or Infleqtion’s current hardware completely obsolete.

Quantum computing is incredibly capital-intensive. These companies must pour millions into R&D and specialized manufacturing just to build a functioning chip. While the note mentions Rigetti has $590 million in cash, that cash isn't profit from operations...it's a runway they are actively burning through. Quality investors want companies that generate cash, not companies that need a massive cash hoard just to survive the next few years.

Think for yourself. For me, it's a pass for now.

2

12

2,597

$BN Great watch for Brookfield investors.

Jun 8

To enable the digitalized economies of the future, we are building the key infrastructure today.

#ICYMI, BAM CEO Connor Teskey sat down with @CNBC Squawk Box Asia to discuss the investment needed in physical assets that support AI use at scale.

Watch the full interview: youtube.com/watch?v=B3oUFgXO…

5

1,562

Quality Equities retweeted

Jun 8

ASML Holding N.V. (NASDAQ: $ASML)

Position Case Study | Status: Core Holding

Total Return to Date: 127.8%

I bought a monopoly at a discount in a year when the stock declined while the broader market rallied. My view was that the near-term weakness in the share price had nothing to do with the fundamentals or the durability of the franchise.

4

2

17

3,307

Quality Equities retweeted

End of May 2026 portfolio update.

My portfolio contains exceptional, world-class businesses. I avoid speculative junk, and instead focus on dominant leaders with massive competitive moats, high returns on capital, and long runways for growth.

At the core, I own unbeatable monopolies and toll-booth businesses. Visa and Mastercard act as toll booths on global spending, while S&P Global and FICO dominate the essential data and credit-rating markets. These companies require very little cash to run, giving them immense pricing power and elite profitability.

I'm also heavily backed by the ultimate tech and AI infrastructure. ASML and KLA are literal gatekeepers for semiconductor manufacturing. Advanced chips can't be made without them. Meanwhile, Microsoft, Alphabet, Meta, and Amazon control the digital real estate and cloud networks that power the modern global economy. Nvidia is the undisputed king of AI computing infrastructure. Structural tailwinds makes these companies incredible long-term compounders.

Brookfield is a masterclass in capital allocation. They invest in hard, essential assets (infrastructure, renewable energy, real estate), and have a long history of compounding value for shareholders.

This past month, I continued to add to Meta, Mastercard, S&P Global, and Brookfield.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep dive equity research into my holdings (as well as other compounding machines), and highly relevant thematic trends shaping today's markets. Link here and in bio: qualityequities.substack.com

$GOOG

$META

$NVDA

$AMZN

$V

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

Minor changes to the portfolio in April 2026.

Added to $META Meta, $MA Mastercard, $AMZN Amazon, $BN Brookfield, and $FICO FICO.

Only buys.

The portfolio is built around some of the world’s strongest, highest‑moat platforms, with a heavy tilt toward scalable, asset‑light, data and network effects businesses.

These companies benefit from immense economies of scale, proprietary infrastructure, pricing power, and data advantages that reinforce their moats as they grow. Their revenue bases skew toward recurring or highly repeat‑purchase models (cloud subscriptions, advertising, developer and enterprise contracts, etc.) with strong operating leverage, making incremental margins very attractive as utilization increases.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep equity research into my holdings (as well as other compounding machines) and highly relevant thematic trends shaping today's markets. Link here and in bio: qualityequities.substack.com

$GOOG

$META

$NVDA

$AMZN

$V

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

8

3

49

5,096

$TDG TransDigm sells the small, boring, mission-critical parts that keep aircraft flying...and owns the economics of those parts like almost no other industrial business.

The parts are cheap relative to the airplane but indispensable to it. ~90% of sales are proprietary, often sole-source, locked in by FAA certification. Once a part is designed onto a platform, it stays for the life of the aircraft — 25-30 years of high-margin aftermarket demand, ~55% of revenue.

On top sits a private-equity-style engine: acquire niche sole-source suppliers, apply value-based pricing, run lean and decentralized, fund it with leverage. The result — Q2 FY26: $2.54B sales, 52.6% EBITDA margin.

The same pricing power that drives the returns is the risk. DoD audits and "price gouging" accusations follow a business this good at extracting price.

Full deep-dive coming this Tuesday. Subscribe at: qualityequities.substack.com…

3

29

4,576

May end of month portfolio update coming tomorrow.

Minor changes to the portfolio in April 2026.

Added to $META Meta, $MA Mastercard, $AMZN Amazon, $BN Brookfield, and $FICO FICO.

Only buys.

The portfolio is built around some of the world’s strongest, highest‑moat platforms, with a heavy tilt toward scalable, asset‑light, data and network effects businesses.

These companies benefit from immense economies of scale, proprietary infrastructure, pricing power, and data advantages that reinforce their moats as they grow. Their revenue bases skew toward recurring or highly repeat‑purchase models (cloud subscriptions, advertising, developer and enterprise contracts, etc.) with strong operating leverage, making incremental margins very attractive as utilization increases.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep equity research into my holdings (as well as other compounding machines) and highly relevant thematic trends shaping today's markets. Link here and in bio: qualityequities.substack.com

$GOOG

$META

$NVDA

$AMZN

$V

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

2

30

4,351

Data center developer Switch is in talks to raise billions of dollars at a valuation of at least $50 billion, as it seeks to capitalize on soaring demand for the infrastructure needed to support artificial intelligence, according to people with knowledge of the deal.

Brookfield Asset Management, KKR and other private equity and institutional investors have been in talks to invest in the round, people familiar with the matter said. Their conversations are early and there is no guarantee they will lead to a deal. Terms of the funding round could still change and the discussions could still fall apart.

Source: The Information

2

770

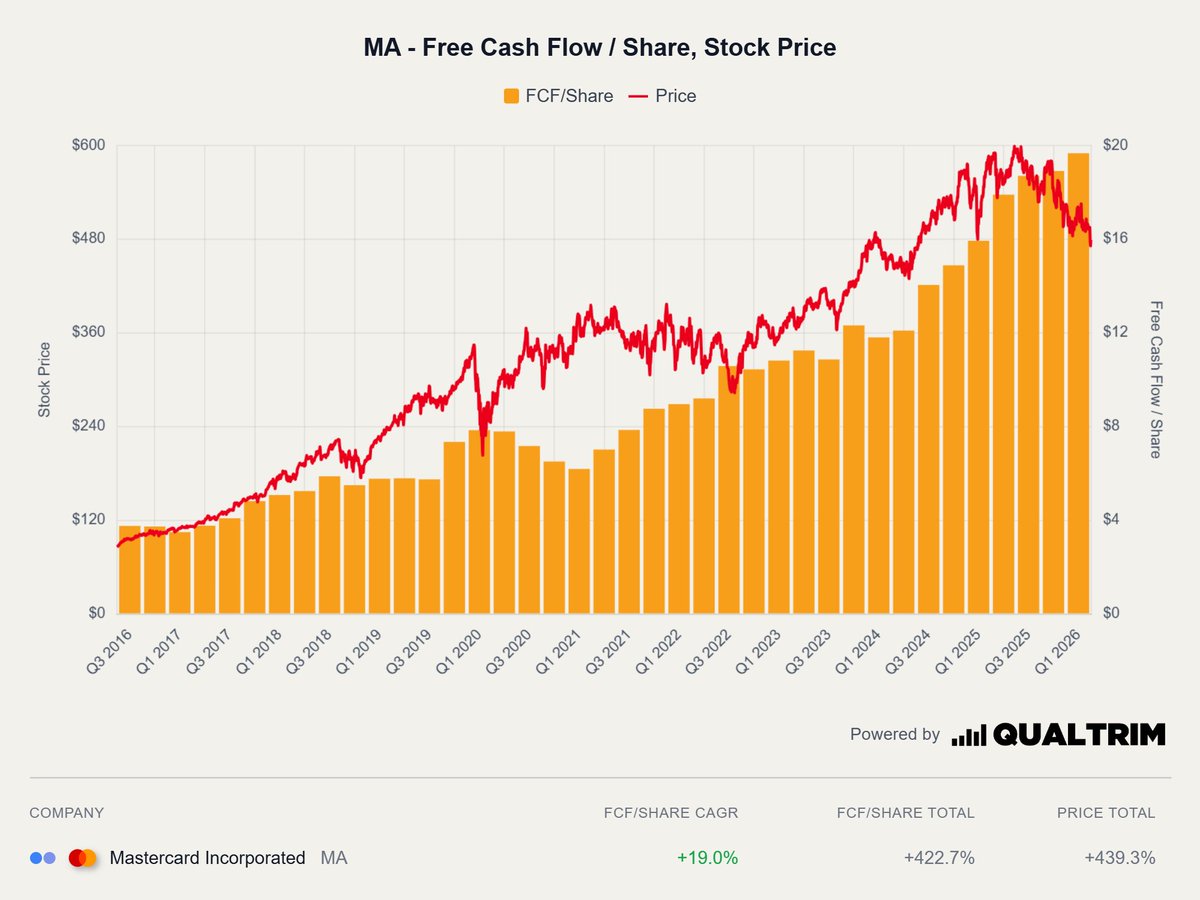

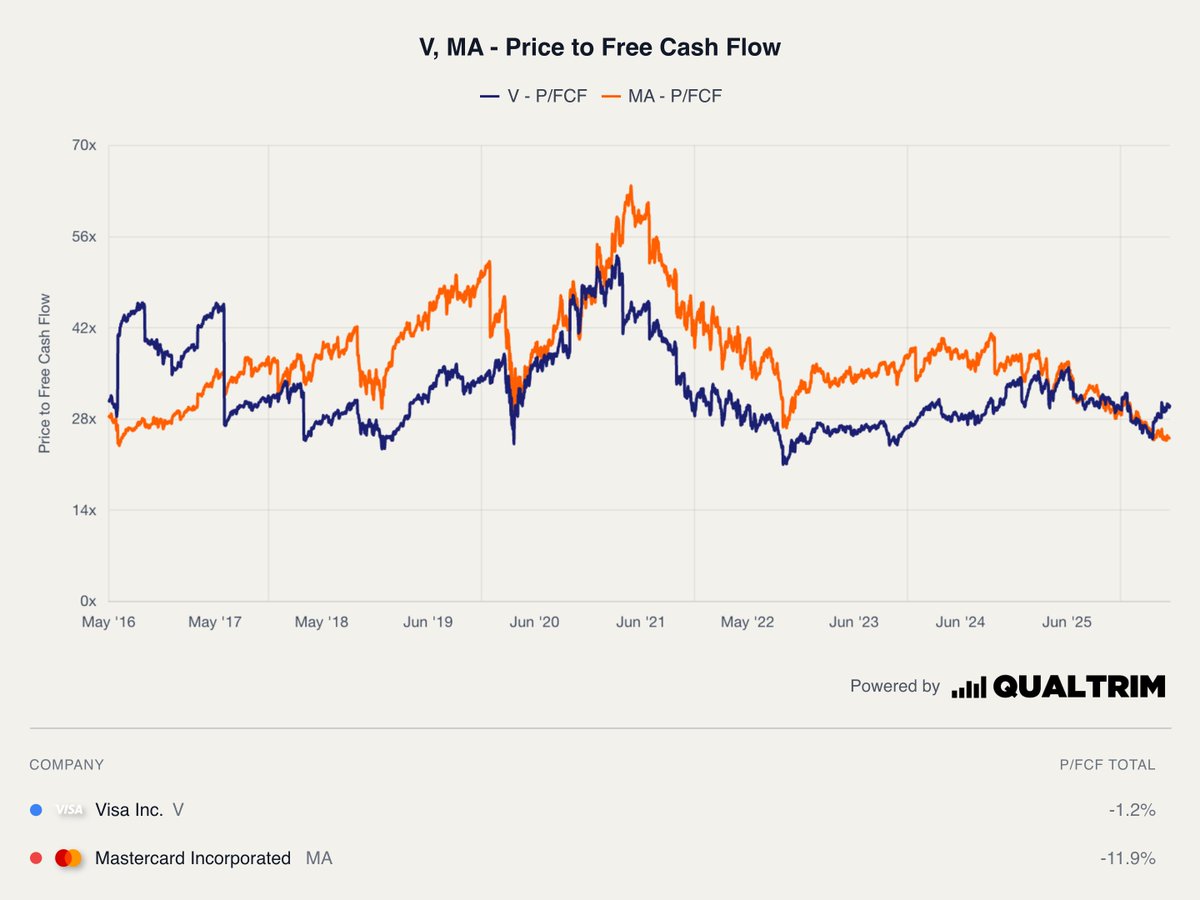

$MA Investing in high-quality companies is all about finding businesses with durable moats that protect them from competition and allow them to earn high returns on capital.

Like a toll bridge on a busy highway, these companies provide essential products or services, possess immense pricing power, and require very little cash to maintain their operations. This capital efficiency allows them to generate mountains of free cash flow, which management can then reinvest back into the business or use to buy back shares.

When you find an elite business capable of doing this year after year, you don't need to trade or timing the market...you simply buy, hold, and let the power of compounding build immense wealth over time.

Mastercard at a 4.18% FCF yield is very attractive.

1

3

26

1,846

Quality Equities retweeted

Jun 4

I just published our latest deep dive on Amphenol $APH.

A boring compounder with exposure to some of the most important long-term trends in the market - data centers, space, robotics, and electrification - yet still trading at a very reasonable valuation.

Hope you enjoy the read. Link in the comments. ⬇⬇

3

3

17

2,619

Return on invested capital identifies the businesses that create value.

Owner earnings measures what owners actually receive.

The moat framework explains why some businesses sustain those returns for decades while competition erodes them for everyone else.

This is the third piece in the free foundational framework, and the answer to the question the ROIC piece raised.

Dropping tomorrow at 9am ET: open.substack.com/pub/qualit…

4

835

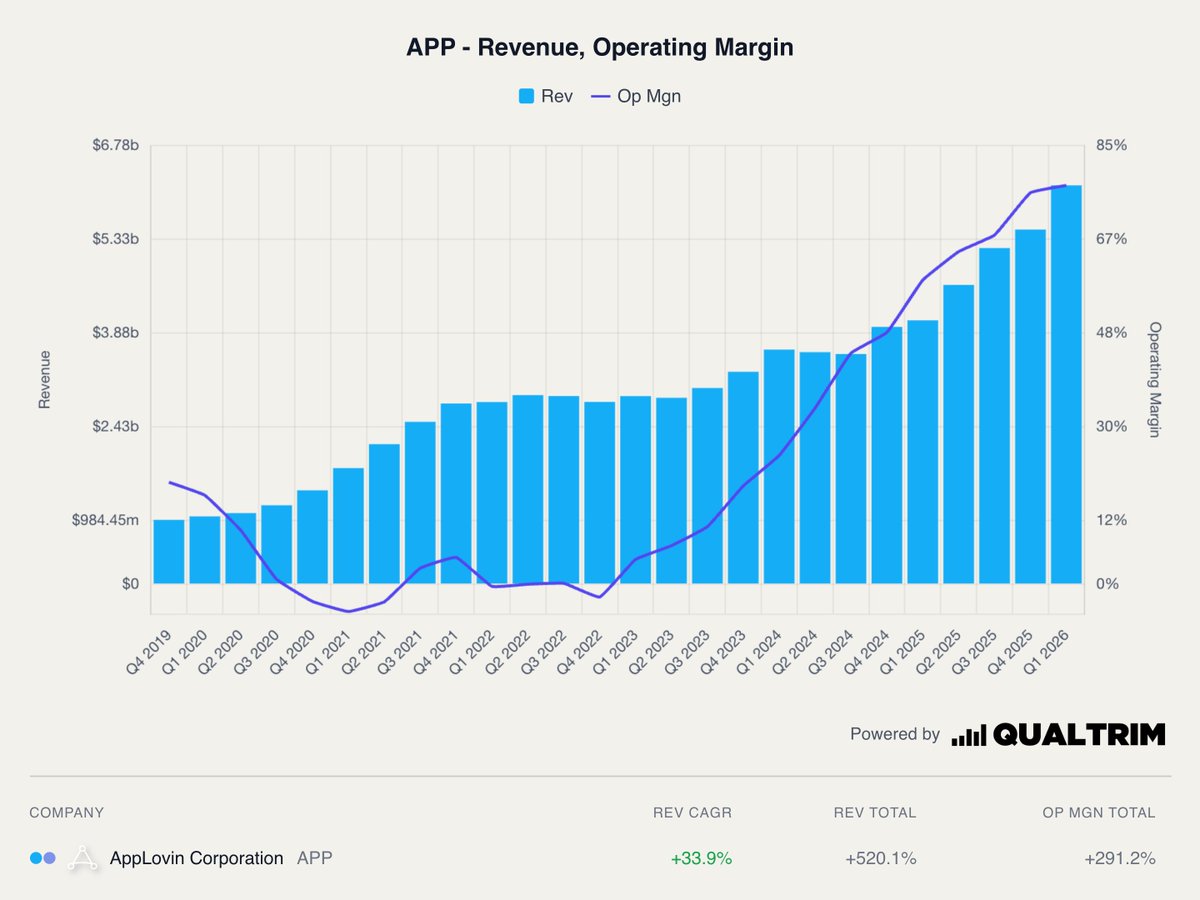

Eighteen months ago, $APP AppLovin was the market’s cleanest expression of the AI-advertising trade: a 700% gain in 2024, a fortress margin profile, and a machine-learning auction engine that appeared to print money.

The narrative in 2026 has inverted. The stock round-tripped from an all-time high near $734 in December to a trough near $320 in early spring, then clawed back to $613.70 (yesterday's close) — all while reporting record results. This is no longer a momentum story; it is a “prove it” year.

What makes AppLovin unusual is that both sides of the debate are internally coherent. The bull case and the bear case each survive serious scrutiny, which is rare in ad-tech, where one side is usually arguing in bad faith.

The question this report answers: does the current price compensate an owner for the durability of the AXON moat — or is it paying a compounder multiple for a business whose compounding is unproven outside one mature vertical?

Read the full bull vs. bear report here: qualityequities.substack.com…

$APP AppLovin is one of the cleanest tests of quality investing in the market right now.

The bull case is textbook compounding. AXON — its machine-learning ad engine — turned cheap mobile-game inventory into a performance network running ~84% EBITDA margins and converting most of it straight to cash. Now it's expanding into e-commerce and connected TV, with a public ad platform launching in 2026.

The bear case is a real fight, not a strawman. The data edge is rented on Apple and Google's rails, mobile gaming is mature, a securities class action and reported regulatory scrutiny hang over its data practices, and the e-commerce story is being extrapolated off a tiny base.

The crux: the market is conflating AXON's proven dominance in gaming with unproven durability outside it — and pricing the e-commerce option as if it's already de-risked at ~41x owner earnings.

A durable, AI-native ad tollbooth, or rented-land ad-tech at the wrong multiple? True quality investing means digging past the noise to verify the moat before paying for it. Our verdict: Watch.

Bull vs. Bear — full breakdown linked below. Available tomorrow at 8:30am ET.

open.substack.com/pub/qualit…

1

7

2,687

$APP AppLovin is one of the cleanest tests of quality investing in the market right now.

The bull case is textbook compounding. AXON — its machine-learning ad engine — turned cheap mobile-game inventory into a performance network running ~84% EBITDA margins and converting most of it straight to cash. Now it's expanding into e-commerce and connected TV, with a public ad platform launching in 2026.

The bear case is a real fight, not a strawman. The data edge is rented on Apple and Google's rails, mobile gaming is mature, a securities class action and reported regulatory scrutiny hang over its data practices, and the e-commerce story is being extrapolated off a tiny base.

The crux: the market is conflating AXON's proven dominance in gaming with unproven durability outside it — and pricing the e-commerce option as if it's already de-risked at ~41x owner earnings.

A durable, AI-native ad tollbooth, or rented-land ad-tech at the wrong multiple? True quality investing means digging past the noise to verify the moat before paying for it. Our verdict: Watch.

Bull vs. Bear — full breakdown linked below. Available tomorrow at 8:30am ET.

open.substack.com/pub/qualit…

May 31

$APP Applovin bull vs. bear deep-dive dropping this Tuesday at 8:30am ET.

Subscribe here: qualityequities.substack.com…

Don't miss it.

6

4,770