Quantitative Trader| Product Manager @AlgoTest_in | Failed Founder.

Joined November 2025

- Tweets 391

- Following 557

- Followers 185

- Likes 556

83 Photos and videos

Pinned Tweet

27 Nov 2025

I try to make complex things like — volatility, Greeks, data, Backtest, Options Trading— simple enough for the Mango Man without dumbing them down.

1

1

5

673

Jun 13

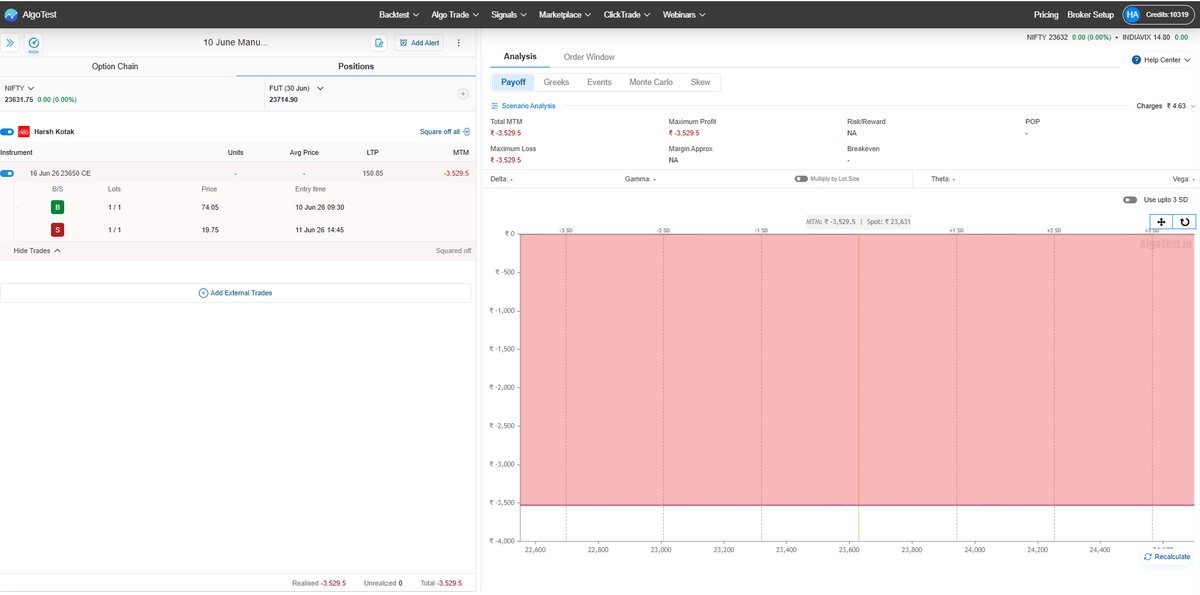

Update - Closed this manual trade on 11 June with the loss...

#algo #algotrading #StockMarket #money #expiry #options #optionstrading

Jun 10

Took a long trade in the opening in Nifty today. Let's see where it close...

153

Jun 13

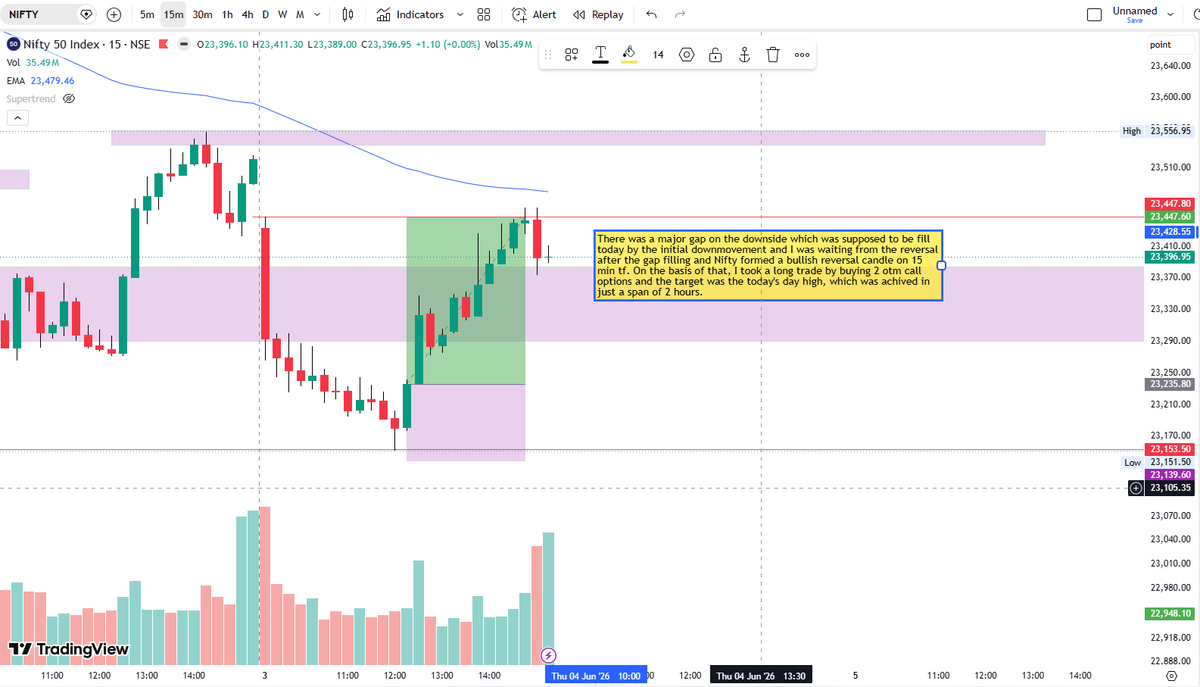

The moment headlines around a potential Iran-US peace deal hit the market, buyers stepped in aggressively.

Caught the move with a Sensex long call and decided to carry it into Monday.

Risk is defined.

Conviction is high.

Now the market gets the final vote. 📈

#Sensex #OptionsTrader #StockMarket #IndianMarkets #TradingJourney #PriceAction

"Would you carry this trade over the weekend?

or am I being too optimistic?

1

2

651

Jun 12

Kill the monster

before he tell you his story,

otherwise you will start loving him to...

Friedrich Nietzsche

1

47

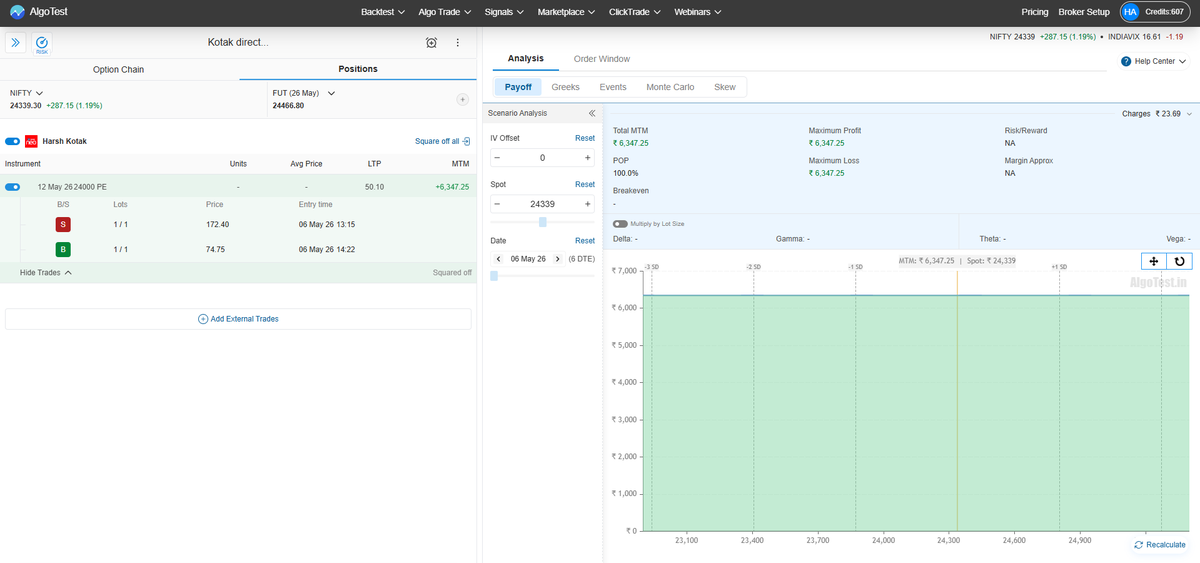

Jun 12

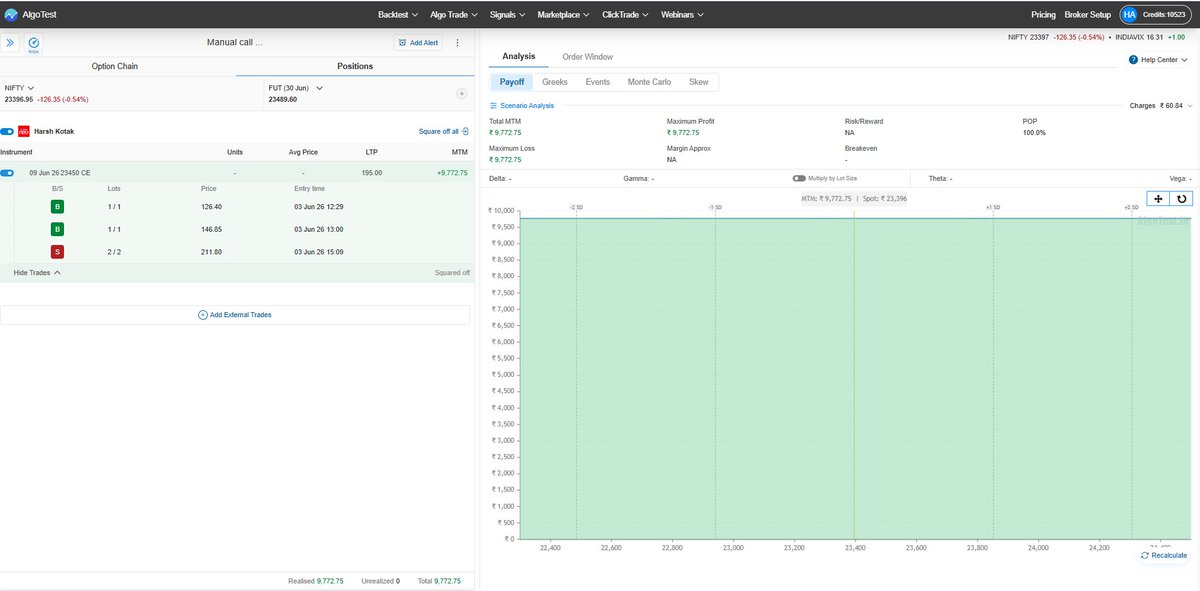

Finally a good day!!

See my MTM graph in action, powered by @AlgoTest_in robust trading engine. algotest.in/share/mtm-graph/…

#algo #algotrading #StockMarket #money #expiry #options #optionstrading

1

1

12

1,945

Jun 12

4

131

Harsh_Malhotra retweeted

Jun 11

Trump: I’m attacking Iran. I’m not attacking Iran. I’m attacking Iran. I’m not attacking Iran.

Markets:

1,353

13,124

74,039

3,989,235

Jun 11

Join us tomorrow at 1pm if you wanna learn how AI can help in building Trading systems..

🚨 LIVE TOMORROW | AI Trading Strategy with Claude AI

What if you could turn a trading idea into a backtested strategy using AI?

Join us tomorrow at 1 PM as we showcase Signals AI, our latest feature that helps you create and backtest indicator-based trading strategies with the power of Claude AI.

✅ Build strategies using plain English

✅ Backtest indicator-based setups instantly

✅ See how AI can accelerate your trading workflow

Set your reminder now 👇

youtube.com/live/dNBR1tqkNgU

#AlgoTest #AITrading #ClaudeAI #TradingStrategy #AlgoTrading

1

591

Jun 11

Most 0 DTE strategies stop working when the market starts trending.

So I tested a different approach.

➡️ Sell a 40 Delta Strangle

➡️ Use a 30 Delta Stop Loss (not premium SL)

➡️ If one leg hits SL, exit the other leg

➡️ Re-enter a fresh 40 Delta Strangle

The result surprised me 👇

This strategy was built using the new Delta-based Stop Loss feature in the 920 Product.

Want to understand exactly how it works?

🎥youtu.be/xzTCTnxQJ-g?si=7rSj…

Want the complete strategy PDF with backtest results?

1️⃣ Repost this tweet

2️⃣ Comment "STRATEGY"

3️⃣ Follow @quant_bandit

I'll DM you the PDF.

Also let me know—what Delta-based strategy should we test next?

#Nifty50 #OptionSelling #DeltaNeutral #AlgoTest #TradingStrategy #OptionsTrading #NiftyExpiry #AlgoTrading

1

5

162

Jun 10

Took a long trade in the opening in Nifty today. Let's see where it close...

1

1

309

Harsh_Malhotra retweeted

Jun 9

Most traders think options trading = expiry day trading.

But this strategy does the exact opposite.

A fully hedged STBT setup designed for both expiry and non-expiry days.

The interesting part wasn't the strategy itself...

it was how much the results changed after adding realistic costs and optimizing DTE selection.

RT Follow Comment "STBT"

I'll DM you the backtest report and my key takeaways from the strategy. (Make sure to follow So I can dm you the insights)

#StockMarket #Trading #OptionsTrading #Nifty #IndianStockMarket

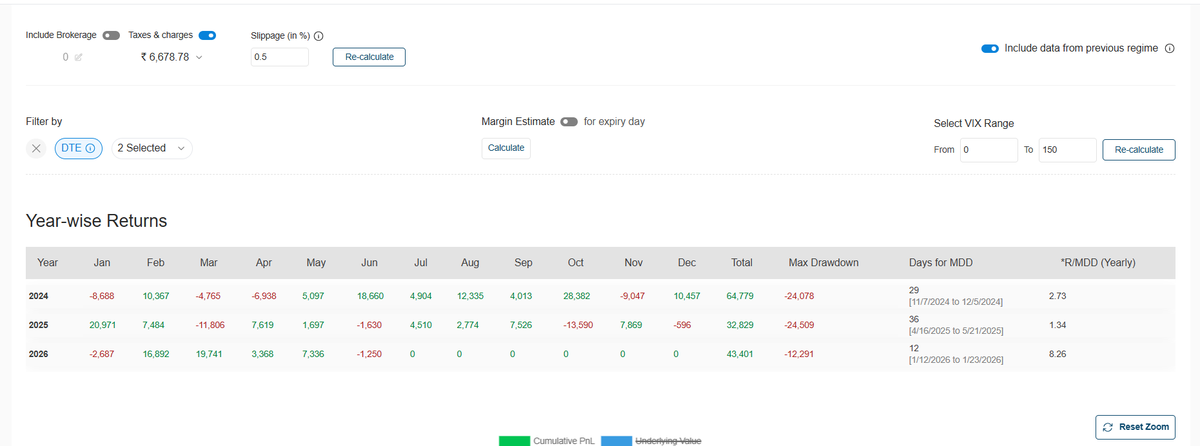

SEBI-registered Research Analyst Vishal Trehan published a fully hedged STBT options strategy on RAAlgos, and we show you exactly how to trade it.

youtube.com/watch?v=vMlgHYjA…

Here's what the video covers:

→ Backtesting the STBT strategy end to end

→ Applying realistic slippage, taxes & charges

→ Using DTE filters

→ Analysing yearly returns & drawdown

→ Forward testing & algo trading directly from AlgoTest

#OptionsTrading #AlgoTrading #AlgoTest #RAAlgos #NiftyOptions #SystematicTrading

1

2

187

Jun 7

Interesting idea from @dhirajsinha sir

Sell 20 Delta Strangle at 9:16 AM.

Exit if either leg reaches 50 Delta (30 pts SL).

We were curious, so we backtested it on NIFTY (0 & 1 DTE) with slippage, taxes & charges included.

Results were surprisingly consistent across multiple years.

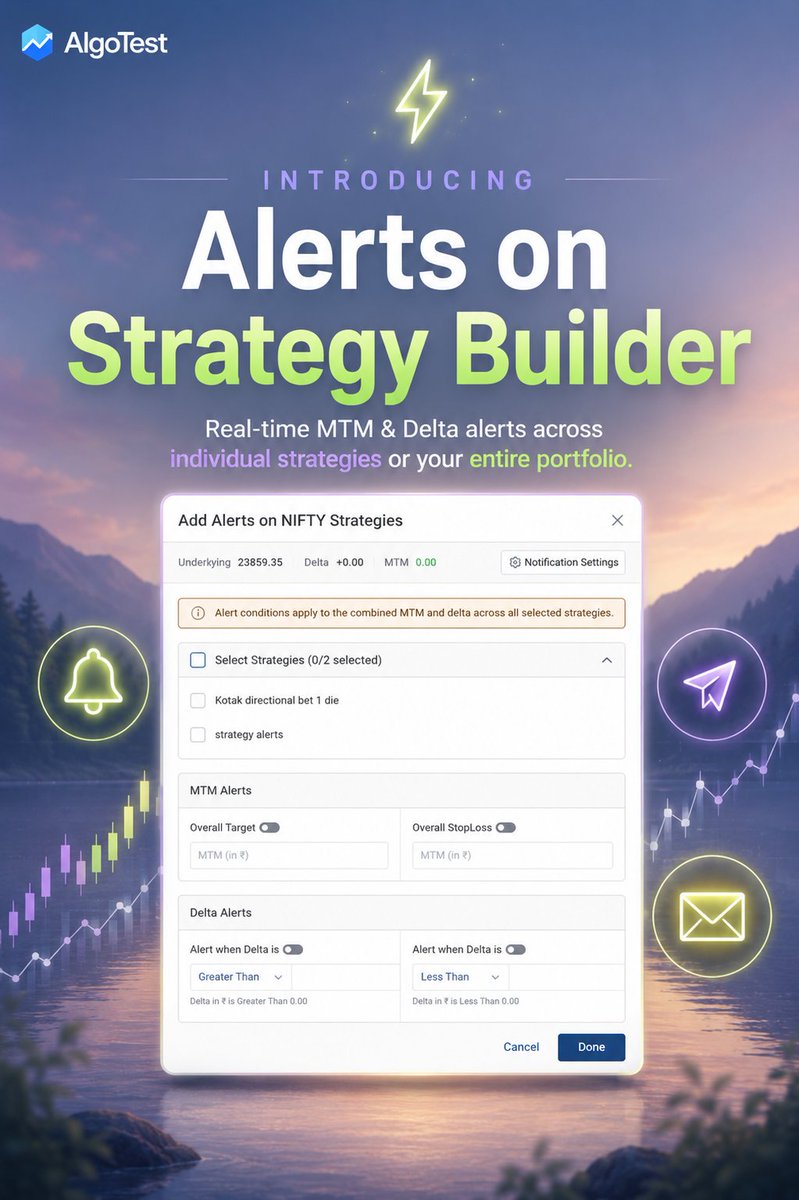

Also, this is exactly why we @AlgoTest_in recently launched Delta Based SL, Target & Trail SL on AlgoTest.

Curious — how many of you manage option positions using Delta instead of premium-based SLs?

Jun 6

Here's an non directional strategy and the formula for deciding the position size.

Strategy - Short strangle, sell 20 delta at 9:16 am with 30 delta SL on each leg (basically exit if a leg becomes ATM). Else exit at 3:25 pm

Win % 64, R:R 0.82

So, as per Kelly, position size is

(0.82*0.64 - 0.36)/0.82 = 0.2

So, 20% of the capital.

In the context of Nifty I will use only 20% of the margin I have to run this strategy. Approx 1 lot for 10 lacs margin.

Disclaimer- strategy is given only to illustrate position size.

9

9

104

18,751

Jun 8

Slippages are already included in the results.

You may opt for broker who doesn't charge brokerage..

The whole point of algo trading is, let the system do it's thing...

Don't interrupt it..

And it's just an starting point on how you can use delta for risk management. You can further optimize it..

1

1

929

Jun 5

See my MTM graph in action, powered by @AlgoTest_in robust trading engine. algotest.in/share/mtm-graph/…

1

5

1,000