Voted “Most Likely To Appear on Wikipedia’s ‘List of Largest Trading Losses’” among graduating class

Joined January 2015

- Tweets 72,546

- Following 508

- Followers 97,219

- Likes 234

7,549 Photos and videos

Pinned Tweet

28 Aug 2020

mfw the margin clerk taps me on the shoulder

19

34

1,078

Alibaba Qwen3.7 slowly fading into irrelevance at the frontier due to proprietary stance.

In it's place we have Minimax M3 and... *checks notes* Rio 3.5 397b, made by the municipal IT company of Rio de Janeiro's city government.

huggingface.co/prefeitura-ri…

1

1

53

5,430

Jun 12

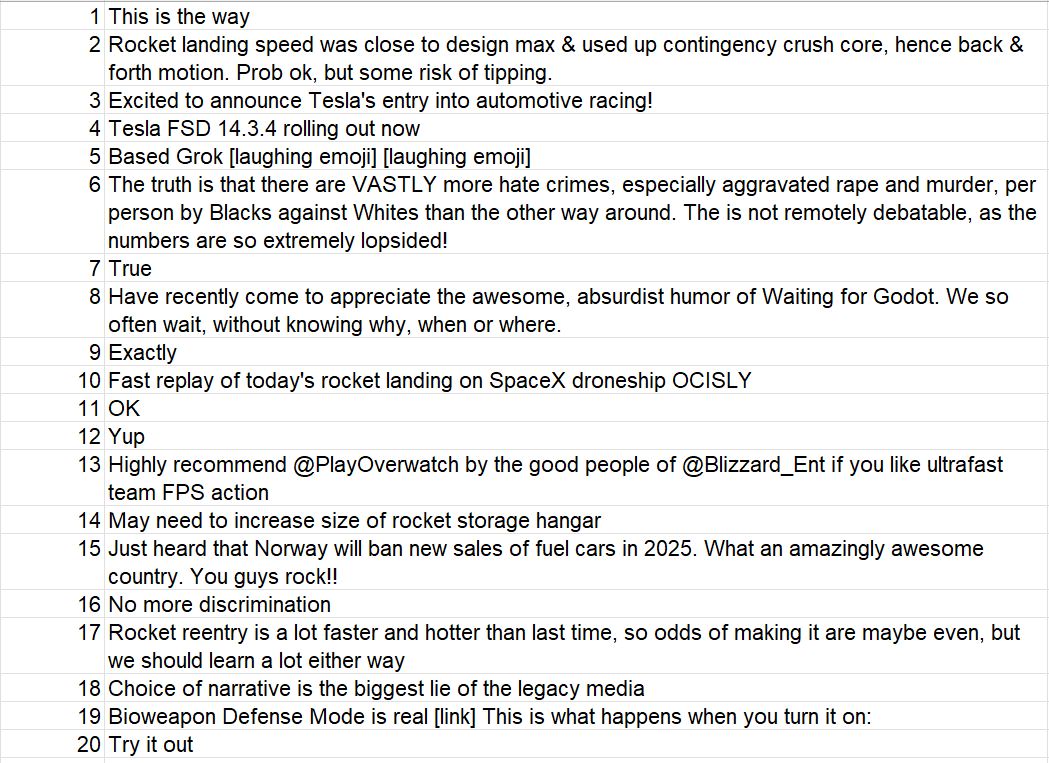

Happy SpaceX IPO day! As a fun game, I randomly selected 10 of Elon's 50 most recent tweets, as well as 10/50 of his tweets 10 years ago and shuffled them together.

Can YOU tell the difference between Elon today and Elon from way back then?

17

51

804

68,761

Jun 12

In case you couldn’t instantly tell, 2, 3, 8, 10, 11 (this one was a fakeout), 13, 14, 15, 17, 19 were old Elon. The rest were current Elon.

Good luck over the next decade, everyone!

29

3,685

Jun 11

They call him 007- 0 product 0 leaks 7 billion scammed from VCs

Jun 10

It really is impressive how tight a ship Ilya runs. We're coming up on two years with basically zero leaks

20

20

1,154

83,235

Jun 11

>we’re doing another three months of fake ceasefire headlines

6

15

441

20,348

Quantіan retweeted

Jun 11

They expect us to believe these results and not ask questions 🙄

76

636

12,037

343,091

Quantіan retweeted

Jun 10

Are we deadass right now

EDITORS' PICK | The statistical impossibility of L.A.'s mayor race trib.al/jNOxJg4

39

456

13,914

585,243

Jun 9

Insane amount of non-ball knowing in the answers here, it’s not remotely close

Who would you rather work for over the next two years if you had a choice - assuming similar comp and location:

15

2

183

97,966

Jun 9

Elevator operator at the conference asked me what AI names I liked

11

14

203

21,959

Jun 9

Listen everybody makes fun of NEOM but the Saudis did in fact have the presence of mind to spend 1% of their cash building a backup pipeline before shit went down in Hormuz, something that apparently didn’t occur to any of the other Gulf states.

27

28

933

47,863

Jun 8

KOSPI is at pretty much exactly the levels implied by Friday close in US markets, everything is priced in as always

4

4

203

24,030

Jun 6

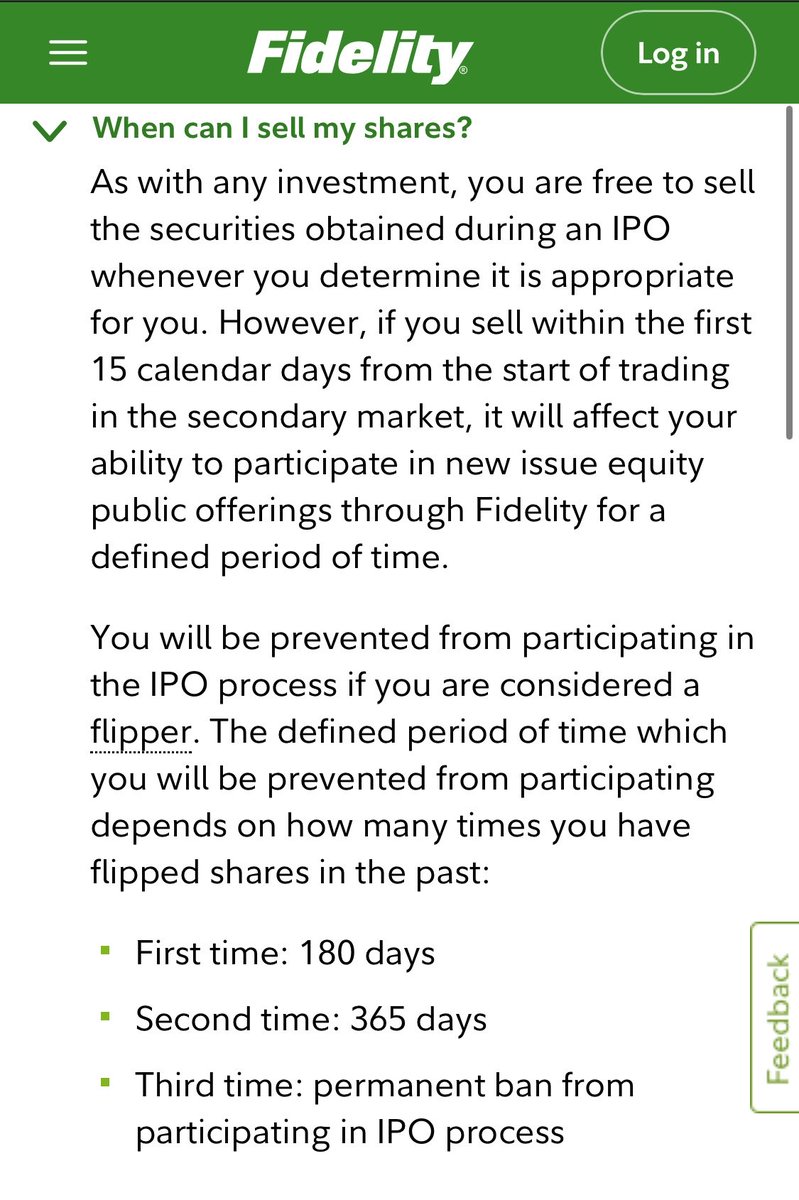

Listen I’m not like a GME MMTLP BBBY type guy but learning that Fidelity will ban you for life if you flip IPOs as a retail client while we have no such restrictions… not a great look, guys.

11

9

326

38,680

Jun 6

Then again maybe retail does have the better deal of having clear rules to decide to follow or break, instead of paying some shit tier bank a ton of commissions only to learn your reward is a 200 share IPO allocation after the fact

1

53

6,510

Quantіan retweeted

"We are cabinet secretaries and we will record as many infomercials as it takes for Sable's stock price to recover."

.@SecretaryWright at the Sable pipeline in Santa Barbara: "These are wells drilled decades ago, just sitting there idle. We used the Defense Production Act to bring that production on. It grew California's oil and gas production by 20% — just turning a valve."

49

73

335

40,753

Jun 5

Markets hitting their all-time high the day of the Left conviction would be quite poetic tbh

2

3

80

14,916

Jun 5

Junior pod shop interview question. You are a risk manager at Exodasnylennium72, and you have just hired 100 PMs away from Citadel. Each one swears they were the top pod and have massive alpha but all actually have random Sharpe from N(0,0.5) and random vol from 10-30%.

May 27

Nice write up.

One point I disagree with is that mechanical drawdown limits have anything to do with momentum. The main hedge you are making with a mechanical drawdown rule is a *hedge against the strategy/PM having stopped working at all* (ie first moment misstating). Secondarily, you are hedging against a risk management failure on the PM’s part (second and higher moment misestimation).

A strategy with a Sharpe of e.g. 1.5 run at X% risk target for Y years should not experience more than Z drawdown, you can back out what X/Y/Z should be, and if the drawdown is hit then either you are in a statistically very rare case, or one of your assumptions (probably the one on the first moment) is wrong.

I also think that mechanical drawdown rules can work for basis type trades (by which I mean: positive carry, and become more attractive as the spread moves against you) except that you don’t cut the positions — you cut the PM and offer their positions to another PM running related strategies. Obviously this only really works in a multi manager setup, not in a single manager fund. The big pod shops do this pretty successfully I think (maybe not in vol, idk, but certainly in rates).

14

14

365

106,154

Jun 5

Hence the classic pod rule, "we cut you if you're down 5% in a month and fire you if you're down 10%". Unless you have a very long tenure, which most managers don't, that corresponds to the expected drawdown you'd see if they were unskilled and negatively skilled, respectively.

3

63

6,817

Jun 5

(Nerd addendum: these curves are a huge pain to calculate numerically since you have to integrate a sum over solutions to tan n =s n, except for the s = 0 case, which has the simple formula of E[MDD(T)] = σ sqrt(πT/2). Easy to fiddle around with for figuring out stop limits!)

1

45

6,039