founder & CEO @Maximor_AI - enterprise finance AI // 2x founder, formerly @Microsoft, @IITMadras

Joined February 2015

- Tweets 1,515

- Following 1,820

- Followers 1,282

- Likes 6,704

82 Photos and videos

Pinned Tweet

29 Sep 2025

🚀 We’ve raised a $9M seed to power Maximor – the AI-powered finance team that fixes the back-end grind.

💡 Finance is broken. And the solution isn’t another ERP.

A quick 🧵

39

38

312

117,050

Uff.. another banger! Here's another macro shift happening:

If intelligence is a priced resource, then the CFO becomes the most important person at the company – the one allocating spend & analyzing ROI across the only 4 inputs that matter:

customers, employees, vendors, and now.. tokens.

That allocation problem is unsolved. We've already figured it out for all of finance.

For 20 years IT/engineering decided what companies bought. AI hands that power to the CFO.

It's the CFO's turn to take it. We're arming them. @maximor_ai 🫡

1

3

36

20,223

May 27

Day 1 at Gartner Finance Symposium cooked!🔥One question kept coming up:

"We've got people building agents in Claude, Vertex, Codex – how do we govern all of this?"

The worry is real. Finance teams are vibecoding fast with DIY agents, but nobody has an answer for what happens when you have hundreds running with no audit trail, no policy layer, and no way to know if they're still doing the right thing when your processes change next quarter.

And even if you get an agent working today, it's trained on a snapshot of right now. Transaction patterns shift. Policies update. New subs come in. If the agent can't learn and adapt with you, you're just building technical debt with better branding.

This is what we built @maximor_ai to solve – agents that don't just automate a frozen process, but continuously learn from your team's judgment and evolve as your business does. One policy layer. Full audit trail. Human in the loop for the exceptions.

Best part of today – these weren't 2-minute booth drive-bys. CFOs and controllers pulling up chairs, going deep on AI strategy, and at one point I'm explaining how context graphs differ from knowledge graphs. At a finance conference. Who would have expected!! (h/t @JayaGup10 🫡)

If you're at the Gartner Xpo tomorrow, come find us at Booth 109!

1

12

3,302

May 9

Huge congrats to @ramkris from Maximor on two stellar CFO conferences this week. Very few people are so technically deep in AI and context engineering along with prior exposure to the messy world of enterprise transformations. 🚀🚀🚀

1

4

322

why does the wifi NEVER work on United/Alaska.. 6 frickin hours nyc -> sf

1

3

240

Apr 24

Great write on the neuro-elasticity aspect of being AI-first!

This line really hits close to the meaning of ‘experience’ (how tied one’s identity is to their accumulation)

“It narrows partly through accumulation: reputation, ego, fear, dependents, the decisions you have tied your identity to. But mostly through environment.”

5

1

6

868

Apr 21

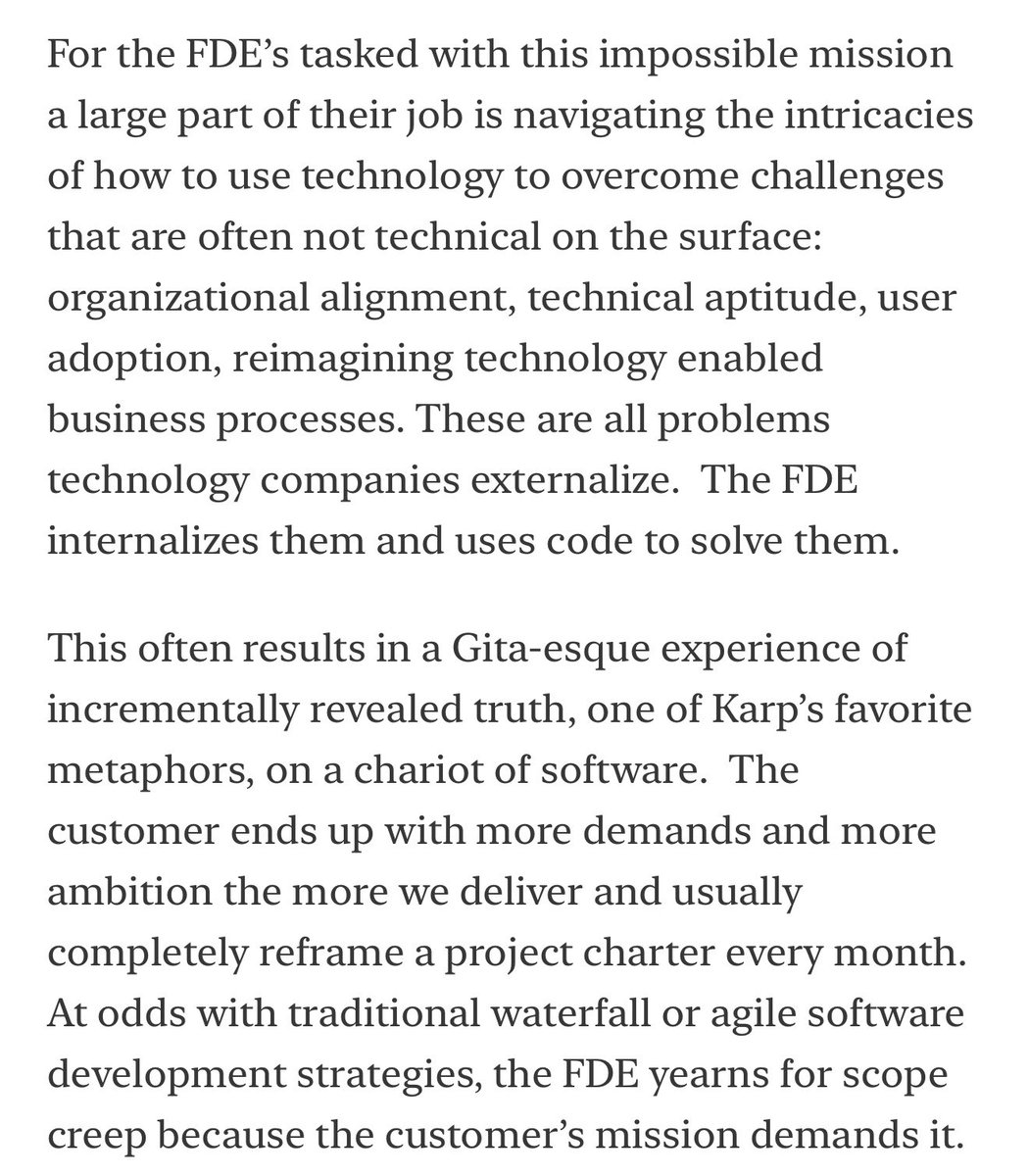

FDE aside, the entire sales process is now true "transformation consulting" based if you're selling a true system-of-action (like us)

brings back so many memories!

yes Palantir is the poster-child of this but what's less known is this was one of the core strategies we employed at Microsoft Azure to outcompete AWS when they had objectively more feature-surface area

1

1

11

4,845

Ramnandan Krishnamurthy retweeted

Apr 19

“Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade.”

^ Respectfully, while it is true that Blackline and Floqast customers are flocking to @maximor_ai , what we’re really building is the Autonomous Finance and Ops Engine. We’re helping our CFOs and the entire Office of the CFO move from being mostly back office to mostly front office. Our contract sizes blow Blackline’s and Floqast’s out of the water precisely because of that - our average ACVs TODAY ( and we’re just about about 8 months post commercialization ) are 3x-4x Floqast’s ( they started in 2012 ) - this is only possible because when CFOs turn to Maximor - they’re doing it for Palantir style transformation for the Finance function but with short implementation timelines ( most of our agents now get implemented in < 2 weeks ) with 99% accuracy with an entire verification layer underpinning our architecture.

Apr 17

In August I wrote a thesis I never published. The funds I was warning were key Crossover Research clients, so I stayed quiet. Since then, 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗺𝘂𝗹𝘁𝗶𝗽𝗹𝗲𝘀 𝗮𝗿𝗲 𝗱𝗼𝘄𝗻 𝟱𝟬% . Salesforce $CRM, ServiceNow $NOW, Adobe $ADBE, Workday $WDAY all off 40% from highs. Thomson Reuters $TRI dropped 16% in a single session on the Anthropic legal agent launch. The SaaSpocalypse arrived. So here's the follow-up. Not commentary on what happened, but where I think this goes next.

Most vertical SaaS companies aren't underperforming because their software is bad. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲𝘆 𝗻𝗲𝘃𝗲𝗿 𝗯𝘂𝗶𝗹𝘁 𝘁𝗵𝗲 𝘀𝗲𝗰𝗼𝗻𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀. And the first business is under attack. For twenty years, one of the biggest SaaS moats was engineering complexity: deep technical talent, long roadmaps, compounding codebases that were genuinely hard to replicate. 𝗔𝗜 𝘂𝗽𝗲𝗻𝗱𝗲𝗱 𝘁𝗵𝗮𝘁 𝗮𝗹𝗺𝗼𝘀𝘁 𝗼𝘃𝗲𝗿𝗻𝗶𝗴𝗵𝘁.

Product development is democratizing to operators with no code background but strong product vision. Look at Anthropic: they've built the engine and are shipping lookalike products at a cadence that would have taken a legacy SaaS vendor three years of roadmap, with a fraction of the headcount. That pace can kill legacy businesses overnight.

𝗜𝗳 𝘁𝗵𝗲 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗺𝗼𝗮𝘁 𝗶𝘀 𝗴𝗼𝗻𝗲, 𝗳𝗼𝘂𝗿 𝗺𝗼𝗮𝘁𝘀 𝗿𝗲𝗺𝗮𝗶𝗻: 𝗱𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻, 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮, 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄 𝗯𝗿𝗲𝗮𝗱𝘁𝗵, 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗶𝗼𝗻. The first three are moats the company builds. The fourth is a moat the company captures, and it's the one most resistant to AI disruption.

𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗰𝗼𝗺𝗽𝗹𝗲𝘅𝗶𝘁𝘆 𝗰𝗿𝗲𝗮𝘁𝗲𝘀 𝘀𝘄𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝗰𝗼𝘀𝘁𝘀 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗲 𝗻𝗼𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗱𝗼 𝘄𝗶𝘁𝗵 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗾𝘂𝗮𝗹𝗶𝘁𝘆. Once a vendor is embedded in a compliance workflow, ripping them out means re-attesting, re-auditing, and re-certifying every downstream process. The buyer isn't paying for software, they're paying for the accumulated paper trail. Tyler Technologies ($TYL) is the clearest version of the pattern. State and local government software across courts, public safety, assessment, and ERP. Every module is married to statutory process, FIPS, CJIS, audit trails, and procurement cycles that take years. TYL is down 42% TTM and 2026 guidance came in soft, but the moat didn't break. Revenue still compounded, and government procurement runs on five-year cycles, not five-week news cycles. Veeva is the sharper version. Revenue up 16% in FY26, Q4 beat, the stock still down 25%. The market is selling execution, not weakness. Guidewire in P&C insurance, where regulatory filings and rate approvals anchor the stack, sits in the same setup: still compounding ARR, still winning cloud conversions, multiple reset anyway. Same pattern across all three: multiples compressed, fundamentals intact. The moat is the regulatory surface area itself, and it compounds because the rules get more complex, not less.

𝗜 𝘄𝗮𝘀 𝗹𝗼𝗻𝗴 𝗣𝗮𝗹𝗮𝗻𝘁𝗶𝗿 𝗮𝘁 $𝟭𝟯 (read that here: x.com/blyons151/status/17920…). 𝗡𝗼𝘁 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗺𝗼𝗱𝗲𝗹 𝗼𝗿 𝘁𝗵𝗲 𝘁𝗼𝗼𝗹𝗶𝗻𝗴. 𝗕𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗼𝗻𝘁𝗼𝗹𝗼𝗴𝘆. Palantir is the proprietary-data version of the regulatory thesis. Once Palantir sits between the customer and their own data, ripping it out means rebuilding the data model from scratch. Snowflake and Databricks never had that entrenchment layer. AIP bootcamps then turned the data moat into a distribution moat: 660 bootcamps in a single quarter, 94% y/y US customer deal growth, bookings at 1.9x sales. Own the data, ship functional AI on top of it, let the GTM compound. Every vertical incumbent has a version of this available. The question is whether they'll build it before a challenger does.

But regulatory insulation is necessary, not sufficient. Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade.

𝗧𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗳𝗼𝗿𝗺𝘂𝗹𝗮 𝗶𝘀 𝗱𝗮𝘁𝗮 𝗼𝗿 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝘀𝘂𝗿𝗳𝗮𝗰𝗲 𝗮𝗿𝗲𝗮 𝗽𝗹𝘂𝘀 𝗳𝘂𝗻𝗰𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜, 𝗻𝗼𝘁 𝗼𝗻𝗲 𝗼𝗿 𝘁𝗵𝗲 𝗼𝘁𝗵𝗲𝗿. Look at why Claude is winning. Anthropic isn't competing on model benchmarks, they're competing on functional workflow. Building for the user, not the leaderboard. That's the playbook vertical incumbents need to run. Take the moat you already have, whether it's regulatory or data-entrenchment, layer genuine workflow AI on top, and the challenger can't catch you. The vendors that do both win the decade. The ones that rely on inertia alone get caught. The ones that ship AI without an anchor get commoditized. You need both.

𝗧𝗵𝗲 𝗯𝘂𝘆𝗲𝗿 𝗶𝘀 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗵𝗶𝘀 𝗽𝗹𝗮𝗶𝗻𝗹𝘆. A study we ran with Battery Ventures on AI adoption in the Office of the CFO (battery.com/blog/first-codin…) surveyed 129 finance leaders at companies from $50M to $5B in revenue. 77% said they want to uplevel existing systems with AI from new vendors that layer onto existing systems. Only 15% want to replace their current system of record with an AI-native platform. The incumbent wins if they ship AI. The AI-native challenger wins only if the incumbent doesn't.

The signal shows up in our VoC data too. In regulated verticals, mission criticality scores cluster above 9, and NPS doesn't track satisfaction, it tracks switching friction. Customers will tell you the product is mediocre and still score it 9 on "would not switch" because the compliance team vetoes any alternative. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝘁𝘂𝗿𝗲 𝗼𝗳 𝗮 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲-𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗻𝗱𝗼𝗿, 𝗮𝘀 𝗹𝗼𝗻𝗴 𝗮𝘀 𝘁𝗵𝗮𝘁 𝘃𝗲𝗻𝗱𝗼𝗿 𝗶𝘀 𝗮𝗰𝘁𝗶𝘃𝗲𝗹𝘆 𝘀𝗵𝗶𝗽𝗽𝗶𝗻𝗴 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝘁𝗵𝗲 𝗔𝗜 𝗰𝘂𝗿𝘃𝗲.

Which brings us back to the second business for everyone outside the regulated or data-entrenched moat. Seat ARR got them to $100M. But with the shift to agentic workforce structures, partial human capital replacement, and pricing pressure compressing margins, the traditional SaaS model has to transform fast. The next $500M comes from monetizing the installed base: marketplace rake on demand they generate for their own customers, capital products underwritten by their own transaction data, supplier monetization, brand partnerships, group buying. The assets are already sitting there. Captive SMB audience. Proprietary transaction and behavioral data. A distribution pipe (the UI itself) that delivers new products at near-zero CAC.

𝗪𝗵𝗮𝘁'𝘀 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 𝗶𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘄𝗶𝗹𝗹. Monetizing the installed base requires a different org than the one that got you to scale. Different GTM, P&L optics, and talent. Founders and boards under-invest because year one looks worse before it looks better, and public markets punish any SaaS multiple that starts to look like fintech or marketplace. So the second business never ships. The round prices in the optionality. The multiple compresses. The exit underwhelms.

𝗧𝗵𝗿𝗲𝗲 𝗱𝗶𝗹𝗶𝗴𝗲𝗻𝗰𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴:

𝟭. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗰𝗼𝗺𝗲𝘀 𝗳𝗿𝗼𝗺 𝘀𝗼𝘂𝗿𝗰𝗲𝘀 𝗼𝘁𝗵𝗲𝗿 𝘁𝗵𝗮𝗻 𝘀𝘂𝗯𝘀𝗰𝗿𝗶𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗽𝗿𝗼𝗰𝗲𝘀𝘀𝗶𝗻𝗴? Under 5%, they haven't started. 10 to 20%, thesis is live. Over 20%, it's working.

𝟮. 𝗛𝗼𝘄 𝗵𝗮𝗿𝗱 𝘄𝗼𝘂𝗹𝗱 𝗶𝘁 𝗯𝗲 𝘁𝗼 𝗿𝗲𝗰𝗿𝗲𝗮𝘁𝗲 𝘁𝗵𝗶𝘀 𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗮𝘁𝗰𝗵 𝘄𝗶𝘁𝗵 𝗔𝗜 𝘁𝗼𝗱𝗮𝘆? If a well-funded team with Claude and six engineers could rebuild the functional product in nine months, the software isn't the moat. The moat has to live somewhere else: proprietary data, a network, integrations, or regulatory surface area the challenger can't clear. If you can't point to at least one, you're underwriting a melting ice cube.

𝟯. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗯𝘂𝘆𝗲𝗿'𝘀 𝘀𝘁𝗶𝗰𝗸𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆, 𝗮𝗻𝗱 𝘄𝗵𝗶𝗰𝗵 𝘄𝗮𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗿𝘂𝗹𝗲 𝘀𝗲𝘁 𝗺𝗼𝘃𝗶𝗻𝗴? A regulatory moat evaporates if the regulation simplifies. Underwrite the direction of travel, not just the current state.

𝗔𝗻𝗱 𝘁𝗵𝗲 𝗰𝗹𝗼𝗰𝗸 𝗶𝘀 𝘁𝗶𝗴𝗵𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲. Retention in enterprise SaaS has largely been defined by the pain of systems replacement, not genuine moat. If the stickiness isn't backed by proprietary data, a harvesting flywheel, or regulatory surface area, those vendors are about to get disrupted. Pure seat-based pricing is dying unless vendors embrace agent-seat models, and LLM providers have been subsidizing the market on token cost, with recent pricing shifts signaling cash reserves aren't infinite.

𝗛𝗲𝗿𝗲'𝘀 𝘁𝗵𝗲 𝘂𝗻𝗱𝗲𝗿𝗮𝗽𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗲𝗱 𝗽𝗼𝗶𝗻𝘁: 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘄𝗼𝗿𝘀𝗲 𝗴𝗿𝗼𝘀𝘀 𝗺𝗮𝗿𝗴𝗶𝗻𝘀 𝘁𝗵𝗮𝗻 𝗦𝗮𝗮𝗦 𝗶𝗻𝗰𝘂𝗺𝗯𝗲𝗻𝘁𝘀, 𝗻𝗼𝘁 𝗯𝗲𝘁𝘁𝗲𝗿. Inference costs haven't collapsed, and burning VC cash to subsidize unit economics is a bridge, not a business model. The incumbents should be winning on P&L. They're losing on product velocity and AI-readiness. That's a solvable problem if the board has the will to ship. Vendors without a second business, without a data moat, and without regulatory insulation will still lose, despite having better margins than their AI-native challengers. Customers switch on features and speed, not on unit economics.

𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗿𝘁𝗶𝗰𝗮𝗹𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝗹𝗮𝘀𝘁 𝘀𝗮𝗳𝗲 𝗵𝗮𝗿𝗯𝗼𝗿, 𝗮𝗻𝗱 𝗼𝗻𝗹𝘆 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝗱𝗮𝘁𝗮 𝗯𝗿𝗲𝗮𝗱𝘁𝗵 𝗮𝗻𝗱 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲. Everywhere else, the premium is about to get competed away. Any fund underwriting vertical SaaS exposure right now should be asking the second-business question before the next check clears. DM me, email me brad@crossoverresearch.com, or let's chat about your portfolio/underwriting process (book.crossoverresearch.com).

Crossoverresearch.com

1

3

13

1,403

Banger article 🧨

👀 “A finance product built around "help the CFO close the books faster" and a finance product built around "make the month-end close not require a human" are not the same product. They are not the same company. You cannot usually get from the first to the second by iterating. You have to start with the second in mind.”

3

12

151

64,075

Feb 12

I've gotten quite a few pings as well today asking about what Ramp's announcement means.

Love Ramp and we integrate with them. And have common customers including a few they've named in their announcement.

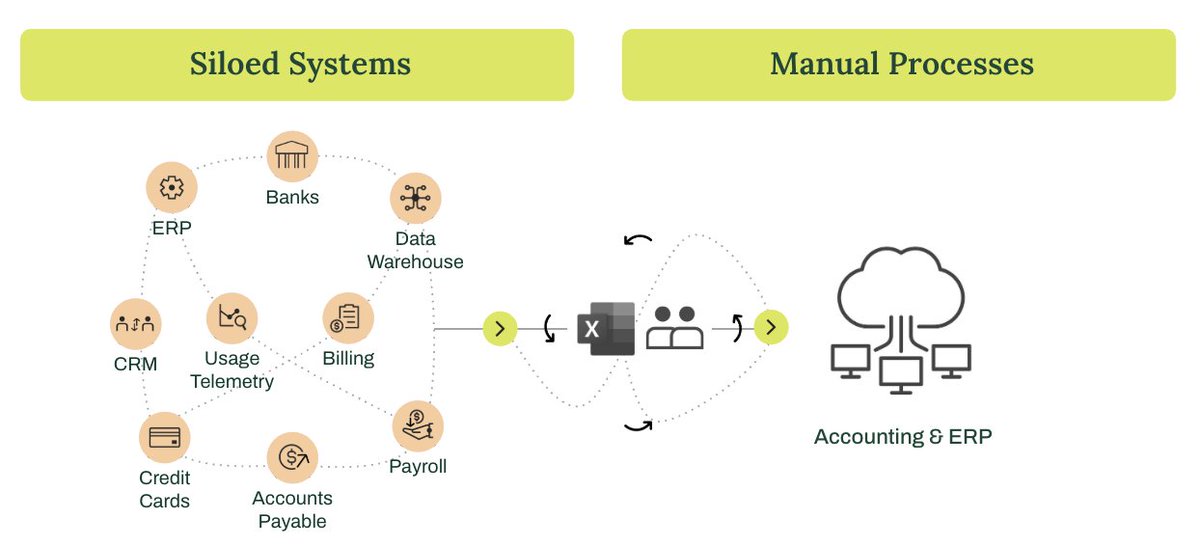

But there is a lot (I mean a LOT) more to operational finance than accounting for expense bills.

Another key thing to grok is how different parts of the income statement & balance sheet move together. Solving for treasury accounting requires deep context across AR, AP, Payroll accounts among others

Solving for automating accounting holistically requires a horizontal approach and not starting from one point area (such as AP)

Feb 12

Ramp’s AI agents for expense bills tracked within Ramp platform (typically <5% of overall accounting workflows). Expense bills fall under the AP category (subset of Operating Expenses)

It doesn’t cover Revenue, Cash, Fixed Assets, and other workflows that cover 90%-95% of the income statement & balance sheet

Context graphs >>

2

2

9

1,520

Proud moment today.

What hits different isn’t just the approval. It’s that talented people keep betting on this mission with us.

Excited to keep building with believers.

Feb 7

Finally an “Alien of Extraordinary Ability”! 🇺🇸🇮🇳

Happy to share that my O-1A visa was approved this week, and I’ll be leading AI efforts @maximor_ai from our NYC location.

NYC is an incredible place to build at the intersection of AI × Finance, and I’m excited to build something truly exceptional here.

10

1,022

Jan 21

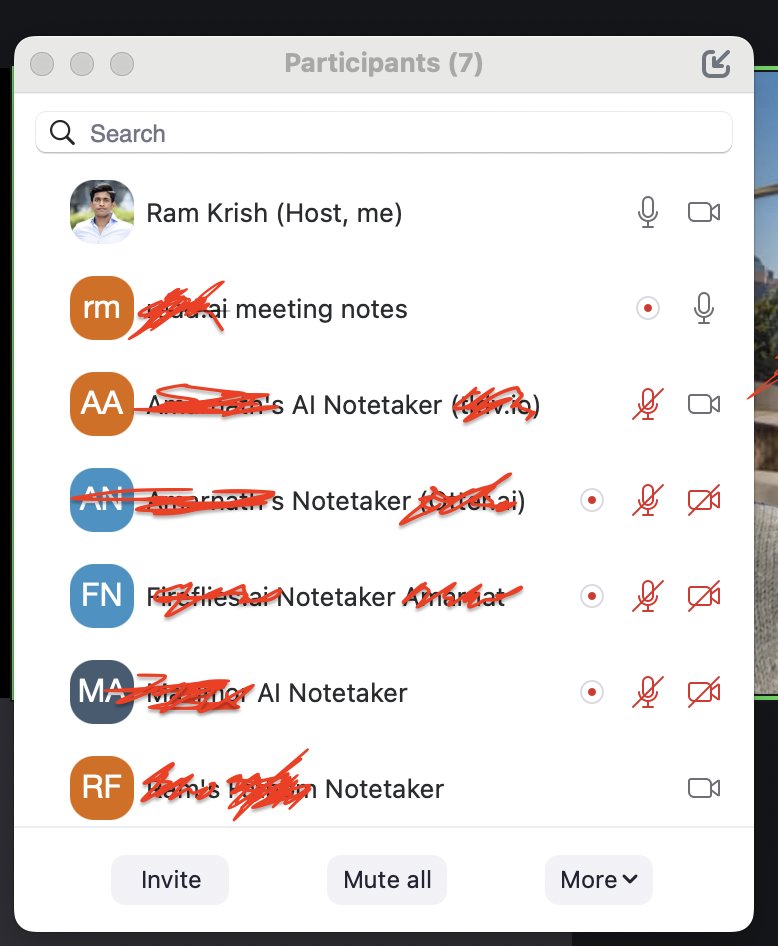

wtf.. was in a lobby alone with 6 AI notetakers today

2

4

193

Jan 19

ive done this mistake too.

letting the “this is who I am ; I need to own it” energy turn into a hurdle and then try to turn the friction against that hurdle into “fuel” than stop to question what is identity vs not

ps. get X to read it out to you if you’re like me and kept delaying reading the whole thing

2

329