Founder & CEO of Crossover Research

Joined September 2021

- Tweets 2,406

- Following 308

- Followers 12,267

- Likes 5,274

790 Photos and videos

Pinned Tweet

Apr 17

In August I wrote a thesis I never published. The funds I was warning were key Crossover Research clients, so I stayed quiet. Since then, 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗺𝘂𝗹𝘁𝗶𝗽𝗹𝗲𝘀 𝗮𝗿𝗲 𝗱𝗼𝘄𝗻 𝟱𝟬% . Salesforce $CRM, ServiceNow $NOW, Adobe $ADBE, Workday $WDAY all off 40% from highs. Thomson Reuters $TRI dropped 16% in a single session on the Anthropic legal agent launch. The SaaSpocalypse arrived. So here's the follow-up. Not commentary on what happened, but where I think this goes next.

Most vertical SaaS companies aren't underperforming because their software is bad. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲𝘆 𝗻𝗲𝘃𝗲𝗿 𝗯𝘂𝗶𝗹𝘁 𝘁𝗵𝗲 𝘀𝗲𝗰𝗼𝗻𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀. And the first business is under attack. For twenty years, one of the biggest SaaS moats was engineering complexity: deep technical talent, long roadmaps, compounding codebases that were genuinely hard to replicate. 𝗔𝗜 𝘂𝗽𝗲𝗻𝗱𝗲𝗱 𝘁𝗵𝗮𝘁 𝗮𝗹𝗺𝗼𝘀𝘁 𝗼𝘃𝗲𝗿𝗻𝗶𝗴𝗵𝘁.

Product development is democratizing to operators with no code background but strong product vision. Look at Anthropic: they've built the engine and are shipping lookalike products at a cadence that would have taken a legacy SaaS vendor three years of roadmap, with a fraction of the headcount. That pace can kill legacy businesses overnight.

𝗜𝗳 𝘁𝗵𝗲 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗺𝗼𝗮𝘁 𝗶𝘀 𝗴𝗼𝗻𝗲, 𝗳𝗼𝘂𝗿 𝗺𝗼𝗮𝘁𝘀 𝗿𝗲𝗺𝗮𝗶𝗻: 𝗱𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻, 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮, 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄 𝗯𝗿𝗲𝗮𝗱𝘁𝗵, 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗶𝗼𝗻. The first three are moats the company builds. The fourth is a moat the company captures, and it's the one most resistant to AI disruption.

𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗰𝗼𝗺𝗽𝗹𝗲𝘅𝗶𝘁𝘆 𝗰𝗿𝗲𝗮𝘁𝗲𝘀 𝘀𝘄𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝗰𝗼𝘀𝘁𝘀 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗲 𝗻𝗼𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗱𝗼 𝘄𝗶𝘁𝗵 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗾𝘂𝗮𝗹𝗶𝘁𝘆. Once a vendor is embedded in a compliance workflow, ripping them out means re-attesting, re-auditing, and re-certifying every downstream process. The buyer isn't paying for software, they're paying for the accumulated paper trail. Tyler Technologies ($TYL) is the clearest version of the pattern. State and local government software across courts, public safety, assessment, and ERP. Every module is married to statutory process, FIPS, CJIS, audit trails, and procurement cycles that take years. TYL is down 42% TTM and 2026 guidance came in soft, but the moat didn't break. Revenue still compounded, and government procurement runs on five-year cycles, not five-week news cycles. Veeva is the sharper version. Revenue up 16% in FY26, Q4 beat, the stock still down 25%. The market is selling execution, not weakness. Guidewire in P&C insurance, where regulatory filings and rate approvals anchor the stack, sits in the same setup: still compounding ARR, still winning cloud conversions, multiple reset anyway. Same pattern across all three: multiples compressed, fundamentals intact. The moat is the regulatory surface area itself, and it compounds because the rules get more complex, not less.

𝗜 𝘄𝗮𝘀 𝗹𝗼𝗻𝗴 𝗣𝗮𝗹𝗮𝗻𝘁𝗶𝗿 𝗮𝘁 $𝟭𝟯 (read that here: x.com/blyons151/status/17920…). 𝗡𝗼𝘁 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗺𝗼𝗱𝗲𝗹 𝗼𝗿 𝘁𝗵𝗲 𝘁𝗼𝗼𝗹𝗶𝗻𝗴. 𝗕𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗼𝗻𝘁𝗼𝗹𝗼𝗴𝘆. Palantir is the proprietary-data version of the regulatory thesis. Once Palantir sits between the customer and their own data, ripping it out means rebuilding the data model from scratch. Snowflake and Databricks never had that entrenchment layer. AIP bootcamps then turned the data moat into a distribution moat: 660 bootcamps in a single quarter, 94% y/y US customer deal growth, bookings at 1.9x sales. Own the data, ship functional AI on top of it, let the GTM compound. Every vertical incumbent has a version of this available. The question is whether they'll build it before a challenger does.

But regulatory insulation is necessary, not sufficient. Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade.

𝗧𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗳𝗼𝗿𝗺𝘂𝗹𝗮 𝗶𝘀 𝗱𝗮𝘁𝗮 𝗼𝗿 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝘀𝘂𝗿𝗳𝗮𝗰𝗲 𝗮𝗿𝗲𝗮 𝗽𝗹𝘂𝘀 𝗳𝘂𝗻𝗰𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜, 𝗻𝗼𝘁 𝗼𝗻𝗲 𝗼𝗿 𝘁𝗵𝗲 𝗼𝘁𝗵𝗲𝗿. Look at why Claude is winning. Anthropic isn't competing on model benchmarks, they're competing on functional workflow. Building for the user, not the leaderboard. That's the playbook vertical incumbents need to run. Take the moat you already have, whether it's regulatory or data-entrenchment, layer genuine workflow AI on top, and the challenger can't catch you. The vendors that do both win the decade. The ones that rely on inertia alone get caught. The ones that ship AI without an anchor get commoditized. You need both.

𝗧𝗵𝗲 𝗯𝘂𝘆𝗲𝗿 𝗶𝘀 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗵𝗶𝘀 𝗽𝗹𝗮𝗶𝗻𝗹𝘆. A study we ran with Battery Ventures on AI adoption in the Office of the CFO (battery.com/blog/first-codin…) surveyed 129 finance leaders at companies from $50M to $5B in revenue. 77% said they want to uplevel existing systems with AI from new vendors that layer onto existing systems. Only 15% want to replace their current system of record with an AI-native platform. The incumbent wins if they ship AI. The AI-native challenger wins only if the incumbent doesn't.

The signal shows up in our VoC data too. In regulated verticals, mission criticality scores cluster above 9, and NPS doesn't track satisfaction, it tracks switching friction. Customers will tell you the product is mediocre and still score it 9 on "would not switch" because the compliance team vetoes any alternative. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝘁𝘂𝗿𝗲 𝗼𝗳 𝗮 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲-𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗻𝗱𝗼𝗿, 𝗮𝘀 𝗹𝗼𝗻𝗴 𝗮𝘀 𝘁𝗵𝗮𝘁 𝘃𝗲𝗻𝗱𝗼𝗿 𝗶𝘀 𝗮𝗰𝘁𝗶𝘃𝗲𝗹𝘆 𝘀𝗵𝗶𝗽𝗽𝗶𝗻𝗴 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝘁𝗵𝗲 𝗔𝗜 𝗰𝘂𝗿𝘃𝗲.

Which brings us back to the second business for everyone outside the regulated or data-entrenched moat. Seat ARR got them to $100M. But with the shift to agentic workforce structures, partial human capital replacement, and pricing pressure compressing margins, the traditional SaaS model has to transform fast. The next $500M comes from monetizing the installed base: marketplace rake on demand they generate for their own customers, capital products underwritten by their own transaction data, supplier monetization, brand partnerships, group buying. The assets are already sitting there. Captive SMB audience. Proprietary transaction and behavioral data. A distribution pipe (the UI itself) that delivers new products at near-zero CAC.

𝗪𝗵𝗮𝘁'𝘀 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 𝗶𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘄𝗶𝗹𝗹. Monetizing the installed base requires a different org than the one that got you to scale. Different GTM, P&L optics, and talent. Founders and boards under-invest because year one looks worse before it looks better, and public markets punish any SaaS multiple that starts to look like fintech or marketplace. So the second business never ships. The round prices in the optionality. The multiple compresses. The exit underwhelms.

𝗧𝗵𝗿𝗲𝗲 𝗱𝗶𝗹𝗶𝗴𝗲𝗻𝗰𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴:

𝟭. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗰𝗼𝗺𝗲𝘀 𝗳𝗿𝗼𝗺 𝘀𝗼𝘂𝗿𝗰𝗲𝘀 𝗼𝘁𝗵𝗲𝗿 𝘁𝗵𝗮𝗻 𝘀𝘂𝗯𝘀𝗰𝗿𝗶𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗽𝗿𝗼𝗰𝗲𝘀𝘀𝗶𝗻𝗴? Under 5%, they haven't started. 10 to 20%, thesis is live. Over 20%, it's working.

𝟮. 𝗛𝗼𝘄 𝗵𝗮𝗿𝗱 𝘄𝗼𝘂𝗹𝗱 𝗶𝘁 𝗯𝗲 𝘁𝗼 𝗿𝗲𝗰𝗿𝗲𝗮𝘁𝗲 𝘁𝗵𝗶𝘀 𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗮𝘁𝗰𝗵 𝘄𝗶𝘁𝗵 𝗔𝗜 𝘁𝗼𝗱𝗮𝘆? If a well-funded team with Claude and six engineers could rebuild the functional product in nine months, the software isn't the moat. The moat has to live somewhere else: proprietary data, a network, integrations, or regulatory surface area the challenger can't clear. If you can't point to at least one, you're underwriting a melting ice cube.

𝟯. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗯𝘂𝘆𝗲𝗿'𝘀 𝘀𝘁𝗶𝗰𝗸𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆, 𝗮𝗻𝗱 𝘄𝗵𝗶𝗰𝗵 𝘄𝗮𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗿𝘂𝗹𝗲 𝘀𝗲𝘁 𝗺𝗼𝘃𝗶𝗻𝗴? A regulatory moat evaporates if the regulation simplifies. Underwrite the direction of travel, not just the current state.

𝗔𝗻𝗱 𝘁𝗵𝗲 𝗰𝗹𝗼𝗰𝗸 𝗶𝘀 𝘁𝗶𝗴𝗵𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲. Retention in enterprise SaaS has largely been defined by the pain of systems replacement, not genuine moat. If the stickiness isn't backed by proprietary data, a harvesting flywheel, or regulatory surface area, those vendors are about to get disrupted. Pure seat-based pricing is dying unless vendors embrace agent-seat models, and LLM providers have been subsidizing the market on token cost, with recent pricing shifts signaling cash reserves aren't infinite.

𝗛𝗲𝗿𝗲'𝘀 𝘁𝗵𝗲 𝘂𝗻𝗱𝗲𝗿𝗮𝗽𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗲𝗱 𝗽𝗼𝗶𝗻𝘁: 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘄𝗼𝗿𝘀𝗲 𝗴𝗿𝗼𝘀𝘀 𝗺𝗮𝗿𝗴𝗶𝗻𝘀 𝘁𝗵𝗮𝗻 𝗦𝗮𝗮𝗦 𝗶𝗻𝗰𝘂𝗺𝗯𝗲𝗻𝘁𝘀, 𝗻𝗼𝘁 𝗯𝗲𝘁𝘁𝗲𝗿. Inference costs haven't collapsed, and burning VC cash to subsidize unit economics is a bridge, not a business model. The incumbents should be winning on P&L. They're losing on product velocity and AI-readiness. That's a solvable problem if the board has the will to ship. Vendors without a second business, without a data moat, and without regulatory insulation will still lose, despite having better margins than their AI-native challengers. Customers switch on features and speed, not on unit economics.

𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗿𝘁𝗶𝗰𝗮𝗹𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝗹𝗮𝘀𝘁 𝘀𝗮𝗳𝗲 𝗵𝗮𝗿𝗯𝗼𝗿, 𝗮𝗻𝗱 𝗼𝗻𝗹𝘆 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝗱𝗮𝘁𝗮 𝗯𝗿𝗲𝗮𝗱𝘁𝗵 𝗮𝗻𝗱 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲. Everywhere else, the premium is about to get competed away. Any fund underwriting vertical SaaS exposure right now should be asking the second-business question before the next check clears. DM me, email me brad@crossoverresearch.com, or let's chat about your portfolio/underwriting process (book.crossoverresearch.com).

Crossoverresearch.com

19 May 2024

$PLTR | Palantir

> Sentiment remains universally upbeat (consistent with read inflection in early January) as AIP traction fuels commercial segment outperformance ( 68% y/y in 1Q24 ex-SPAC revenue).

> The company continues to lean heavily into AIP bootcamps as a GTM strategy (hosted 660 in 1Q alone) and recent results are a testament of the effectiveness of this strategy: US customer deal growth 94% y/y (136 deals closed vs. 70 in 1Q23), bookings at 1.9x of sales ( 131% y/y), customer count 69% y/y.

> While it’s still too early to extrapolate initial bootcamp conversion metrics for bookings and revenue, the initial success is convincing. The AIP customer feedback we’ve picked up in our own checks supports view that bookings momentum can be sustained in the near-term.

> Partners on our checks have reported an overwhelming pace of YTD business with most seeing activity that is pacing significantly above (2x ) available capacity as well as internal growth targets.

> Palantir is in the early stages of building its channel program. The solution is an attractive GSI solution and can trigger a rich set of integration and customization services. As PLTR rolls out across GSIs, it should help to sustain the company's 20% growth targets.

> We had previously highlighted some concerns that PLTR's opportunity was limited to G2K firms with outsized analytics budgets and those who prefer to build on top of Databricks's open platform. We have since learned that PLTR’s data abstraction and ontology model, which is considered a critical component, creates a compelling competitive moat vs. SNOW and Databricks.

My thoughts... While valuation concerns cannot be written off at these levels, underlying business trends look healthy enough to support the premium multiple. Commercial momentum seems unlikely to slow given the success of PLTR’s AIP bootcamp GTM approach (mgmt. guided to 40% growth in 2024, pointing to 560 bootcamps completed across 465 orgs) and our internal checks suggest existing customer growth is on the horizon (in our 1/8 survey, >70% of PLTR customers suggested that AI-related initiatives would have a significant impact on PLTR spend by 2H’24). The government segment remains challenged and a wildcard to monitor, but mgmt’s guide to a 2024 reacceleration can be considered a positive.

Customer feedback on AIP Bootcamps...

The concept and framework of it seems like a really strong approach to me, not just for AI-based applications but honestly the intensive boot camp method seems like a good approach for a number of other use cases as well. This intensive approach aligns better with more Agile development methods where a boot camp approach, coupled with another week or so of follow up effort, might actually result in delivery within a very short period of time (even if limited in scope) which might help build more momentum and get a lot more hours of focus driving value than picking away at something over a more extended engagement. - Chief Data Officer at Government Agency

We have participated in AIP bootcamps; they are a good approach to bring a team together to test an idea. The bootcamps are well organized with the Palantir team available to support and enable the team to develop a solution. - Director of Data Engineering at National Health Provider

64

210

1,633

821,295

May 27

Crazy how well this trade has worked out.

Sept 25, 2023: “grid constraints forcing their hands to use nuclear.”

The basket since:

• Talen 670%

• Vistra 370%

• Oklo 360% (post-IPO)

• Constellation 170%

• NuScale 140%

• Cameco 100%

S&P 500 same period: 73%.

25 Sep 2023

Believe so, heard the same intentions from another big player as well - grid constraints forcing their hands to use nuclear. Here was project I received:

1

9

2,997

May 11

$NTDOY - was cycling through old charts I've done and the Nintendo price action I mapped out in 2023 panned out exactly as technicals were suggesting. Pairing fundamentals with chart framework = a good way to improve win rate.

9 Aug 2023

$NTDOY - been talking about this one for about 12 months; the technical positioning and fundamental moat of Nintendo is too attractive to overlook at these levels. Multi-bagger setup > I'm projecting a move to $22 by 2H'25 as momentum comes into the picture.

Stock tends to have massive expansion cycles (see 3 prior moves). 1P content slate, new hardware, margin expansion opportunities.

Off my initial post we got a 25% move to primary resistance with expected pullback as I show on the chart. On a retest, this should start to expand in a much more meaningful capacity.

1

1

12

3,487

May 3

Revenue segmentation is the whole game. ARR isn’t ARR if 40% sits in the exposed bucket, and the multiple shouldn’t treat it like it is.

The cut that matters for any software name you own:

Non mission critical (engagement layer): massive trouble. Easiest to displace with an agent or thin wrapper. No data gravity, no compliance moat. Net retention is the tell, watch it quarterly.

Enterprise systems of record: insulated, in some cases growing with AI add-ons. Rip-and-replace cycles run 18 to 36 months, and CIOs prefer AI from the incumbent over a new vendor relationship. Pricing power holds.

Mid market: price chasing. AI-native challengers undercut on seat price, and customers use those quotes to negotiate incumbents down even when they don’t switch. Margin compresses either way, and consensus models aren’t pricing it.

SMB: huge risk. Lowest switching costs, no procurement friction, free or cheap AI tools clear the bar. Logo churn shows up first, then ARPU.

System of record vs system of engagement is the frame. Engagement layer is exposed. Record layer is sticky.

This is what bears get wrong. Public software is heavily biased towards the best companies.

There are thousands of little tools that you’ve never heard of, but they rarely make it to IPO. When CIOs say they’re replacing software, they’re almost always talking about the latter.

1

1

6

3,964

May 1

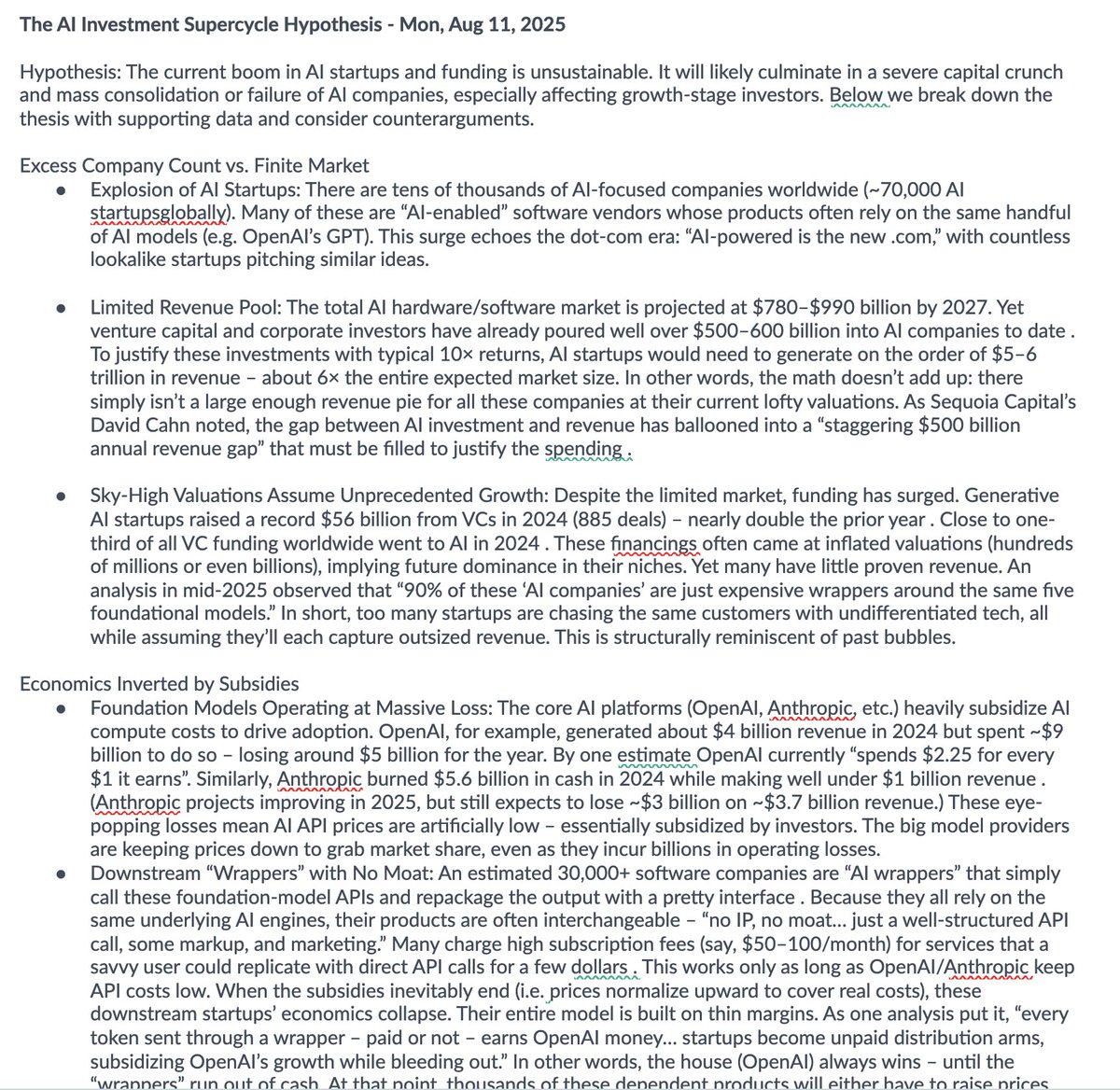

The AI Investment Supercycle Hypothesis

Here is my original post from August 11, 2025. Releasing the full version after multiple requests.

Since I wrote this the math has only gotten worse.

The thesis in one line: the current AI boom cannot clear its capital stack. We are heading into a severe crunch and a mass consolidation event. Growth equity will absorb most of the damage.

In slightly longer form:

Too many companies for the available spend.

Too much capital chasing too small a market.

Too much dependency on unprofitable infrastructure.

Something has to give. What gives is the middle of the cap table.

This is not a thesis against AI. The technology is revolutionary. The mistake is assuming every AI company is.

Growth equity is going to take the worst of it. The investors who wrote the largest checks at the highest valuations will be the ones marking down hardest. Most LPs do not yet know how exposed they are.

The era of indiscriminate AI hype investment is winding down. What follows will separate the enduring players from the rest.

The math has the final say. It always does.

And here is the case, broken down...

1. Too many companies, not enough market

> ~70,000 AI startups globally. Most are "AI-enabled" software vendors riding the same handful of foundation models.

> The total AI hardware and software market is forecast at $780B to $990B by 2027.

> Venture and corporate investors have already deployed $500B to $600B into AI companies.

> To clear typical 10x return hurdles, those companies would need to generate $5T to $6T in revenue, roughly 6x the entire expected market.

> Sequoia's David Cahn pegged the gap between AI capex and AI revenue at a "staggering $500 billion" annual hole that has to be filled to justify the spend.

> AI-powered is the new .com. The structural setup looks like 1999.

The math doesn't add up. There is not a pie large enough to justify the cap table.

2. Funding has surged into a market that cannot absorb it

> Generative AI startups raised a record $56B from VCs in 2024 across 885 deals, nearly double the prior year.

~33% of all global VC funding in 2024 went to AI.

> Most of those rounds priced in future dominance with little proven revenue.

> One mid-2025 read: 90% of "AI companies" are just expensive wrappers around the same 5 foundational models.

> Too many startups, same customers, undifferentiated tech, all assuming each captures outsized share.

3. The economics are inverted by subsidy

The core platforms are running at massive operating losses to grab share, and that is what is keeping the rest of the stack alive.

> OpenAI: ~$4B revenue in 2024 against ~$9B in spend. Around $5B in losses for the year.

> One read on the unit economics: OpenAI spends $2.25 for every $1 it earns.

> Anthropic: $5.6B cash burn in 2024 against well under $1B in revenue. Projected ~$3B loss on ~$3.7B revenue in 2025.

> API prices are artificially low. Investors are subsidizing AI compute to drive adoption.

When the subsidy ends, the entire downstream collapses with it.

4. The wrapper economy is built on sand

> An estimated 30,000 companies are "AI wrappers" that call foundation model APIs, repackage the output, and resell it.

> Same engines means interchangeable products. No IP, no moat, just a well-structured API call, some markup, and marketing.

> Many charge $50 to $100 per month for what a power user could replicate with direct API calls for a few dollars.

> Every token sent through a wrapper, paid or not, earns OpenAI money.

> Wrapper startups are effectively unpaid distribution arms, subsidizing OpenAI's growth while bleeding out.

The house always wins. Until the wrappers run out of cash.

5. The commoditization spiral

The vicious circle for everyone except the foundation model leaders:

> Same models everywhere means undifferentiated products.

> No real differentiation means pricing wars. GPT-4 price cuts already undercut Anthropic by up to 7x on cost per token in some configurations, forcing the industry to match.

> Lower price per customer means collapsed gross margins for any startup reselling AI.

> Lower revenue makes it impossible to support previous valuations or absorb still-rising compute and energy costs.

> Unit economics flip upside down. More users actually means more losses.

> These companies cannot operate without continual investor subsidy.

A race to the bottom is great for end users in the short term. It is lethal for thousands of me-too vendors.

6. Growth equity is the most exposed pool of capital

This is the part the LP letters are not yet ready to write.

> Growth funds wrote $25M to $100M checks at $400M valuations on the assumption of 1 or 2 failures out of 10.

> Most companies funded during the 2021 to 2023 boom had 18 to 36 months of capital. Many will run dry by late 2025 or early 2026.

> Industry observers now predict 90% of AI startups fail within 5 years.

> Conservative scenario, 60% to 70% failure: ~$400B of the ~$600B deployed gets wiped.

> Realistic scenario, 80% to 90% failure: $500B in losses.

> PitchBook already shows AI deal count down 42% in 2024 as reality starts to filter in.

> A growth fund with 40% of its book in AI could see an 80% write-down on that slice. That would be historic.

Early-stage VC tolerates 6 or 7 losses out of 10. Growth equity does not. The model breaks.

7. The exit window is closing too

> The 2025 IPO window for tech is selective at best, and the listings that have priced are not delivering exit multiples that clear late-stage entry.

> M&A is the realistic outcome, but acquirers will wait until valuations crumble.

> A $50M check at a $500M post will recoup pennies in a fire sale.

8. Timeline: from bubble to shakeout

2021 to 2023, build-up: GPT-3, DALL-E, generative AI breakthroughs trigger a flood of startup creation. AI is the new electricity. FOMO drives indiscriminate funding.

2024, peak froth: $56B into genAI. Headlines everywhere. Cracks underneath: GPU bottlenecks, startups with negligible traction, and Big Tech racing ahead. Even the leaders are unprofitable. OpenAI doubles ARR from $6B to $12B in H1 2025, still expects ~$14B loss for the year.

2025, saturation: Every vertical is crowded. Sales cycles lengthen as CIOs get fatigued by the 50th similar pitch. CAC climbs. Big Tech bundles AI into existing platforms, often free, undercutting standalones. Investors get selective.

Late 2025 to 2026, the crunch: Boom-era runways exhaust. Funding environment is harder. LPs are nervous about AI overexposure. Sharp pullback for everyone except the top 5%. Down rounds and outright failures pile up. Sentiment flips from FOMO to caution. The mere mention of AI no longer secures a premium.

2027, mass extinction: The global liquidity squeeze hits. Growth equity and crossover capital largely retreat. Thousands of AI startups fold in a 12 to 18 month window. Direct analog to the 2000 to 2001 dot-com collapse.

2028 to 2029, reset: Survivors fall into two camps. Foundation model and infrastructure leaders. Specialists with truly defensible domain or data moats. With less crazy competition, pricing power returns. API rates rise to profitable levels. A few big winners emerge with public-market validation. Many VC funds report poor returns on the bubble cohort.

9. The endgame

Three things hit at once:

> Valuation collapse. Multiples compress dramatically. AI startups that raised at 100x forward revenue trade at 5 to 10x if they survive at all. Private valuations could fall 70% to 90% before finding a floor.

> Mass closures. Not dozens. Thousands of companies disappear in a short window. Talent and IP get absorbed by larger players.

> Industry reset. Survivors capture larger shares. Pricing rises as subsidies fade. Focus narrows from gimmick AI features to core uses that deliver real ROI. A handful of mega-winners dominate and finally make money on AI.

The truly useful AI applications and companies remain and thrive under more rational economics. The middle of the cap table does not.

Apr 17

In August I wrote a thesis I never published. The funds I was warning were key Crossover Research clients, so I stayed quiet. Since then, 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗺𝘂𝗹𝘁𝗶𝗽𝗹𝗲𝘀 𝗮𝗿𝗲 𝗱𝗼𝘄𝗻 𝟱𝟬% . Salesforce $CRM, ServiceNow $NOW, Adobe $ADBE, Workday $WDAY all off 40% from highs. Thomson Reuters $TRI dropped 16% in a single session on the Anthropic legal agent launch. The SaaSpocalypse arrived. So here's the follow-up. Not commentary on what happened, but where I think this goes next.

Most vertical SaaS companies aren't underperforming because their software is bad. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲𝘆 𝗻𝗲𝘃𝗲𝗿 𝗯𝘂𝗶𝗹𝘁 𝘁𝗵𝗲 𝘀𝗲𝗰𝗼𝗻𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀. And the first business is under attack. For twenty years, one of the biggest SaaS moats was engineering complexity: deep technical talent, long roadmaps, compounding codebases that were genuinely hard to replicate. 𝗔𝗜 𝘂𝗽𝗲𝗻𝗱𝗲𝗱 𝘁𝗵𝗮𝘁 𝗮𝗹𝗺𝗼𝘀𝘁 𝗼𝘃𝗲𝗿𝗻𝗶𝗴𝗵𝘁.

Product development is democratizing to operators with no code background but strong product vision. Look at Anthropic: they've built the engine and are shipping lookalike products at a cadence that would have taken a legacy SaaS vendor three years of roadmap, with a fraction of the headcount. That pace can kill legacy businesses overnight.

𝗜𝗳 𝘁𝗵𝗲 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗺𝗼𝗮𝘁 𝗶𝘀 𝗴𝗼𝗻𝗲, 𝗳𝗼𝘂𝗿 𝗺𝗼𝗮𝘁𝘀 𝗿𝗲𝗺𝗮𝗶𝗻: 𝗱𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻, 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮, 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄 𝗯𝗿𝗲𝗮𝗱𝘁𝗵, 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗶𝗼𝗻. The first three are moats the company builds. The fourth is a moat the company captures, and it's the one most resistant to AI disruption.

𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗰𝗼𝗺𝗽𝗹𝗲𝘅𝗶𝘁𝘆 𝗰𝗿𝗲𝗮𝘁𝗲𝘀 𝘀𝘄𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝗰𝗼𝘀𝘁𝘀 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗲 𝗻𝗼𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗱𝗼 𝘄𝗶𝘁𝗵 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗾𝘂𝗮𝗹𝗶𝘁𝘆. Once a vendor is embedded in a compliance workflow, ripping them out means re-attesting, re-auditing, and re-certifying every downstream process. The buyer isn't paying for software, they're paying for the accumulated paper trail. Tyler Technologies ($TYL) is the clearest version of the pattern. State and local government software across courts, public safety, assessment, and ERP. Every module is married to statutory process, FIPS, CJIS, audit trails, and procurement cycles that take years. TYL is down 42% TTM and 2026 guidance came in soft, but the moat didn't break. Revenue still compounded, and government procurement runs on five-year cycles, not five-week news cycles. Veeva is the sharper version. Revenue up 16% in FY26, Q4 beat, the stock still down 25%. The market is selling execution, not weakness. Guidewire in P&C insurance, where regulatory filings and rate approvals anchor the stack, sits in the same setup: still compounding ARR, still winning cloud conversions, multiple reset anyway. Same pattern across all three: multiples compressed, fundamentals intact. The moat is the regulatory surface area itself, and it compounds because the rules get more complex, not less.

𝗜 𝘄𝗮𝘀 𝗹𝗼𝗻𝗴 𝗣𝗮𝗹𝗮𝗻𝘁𝗶𝗿 𝗮𝘁 $𝟭𝟯 (read that here: x.com/blyons151/status/17920…). 𝗡𝗼𝘁 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗺𝗼𝗱𝗲𝗹 𝗼𝗿 𝘁𝗵𝗲 𝘁𝗼𝗼𝗹𝗶𝗻𝗴. 𝗕𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗼𝗻𝘁𝗼𝗹𝗼𝗴𝘆. Palantir is the proprietary-data version of the regulatory thesis. Once Palantir sits between the customer and their own data, ripping it out means rebuilding the data model from scratch. Snowflake and Databricks never had that entrenchment layer. AIP bootcamps then turned the data moat into a distribution moat: 660 bootcamps in a single quarter, 94% y/y US customer deal growth, bookings at 1.9x sales. Own the data, ship functional AI on top of it, let the GTM compound. Every vertical incumbent has a version of this available. The question is whether they'll build it before a challenger does.

But regulatory insulation is necessary, not sufficient. Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade.

𝗧𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗳𝗼𝗿𝗺𝘂𝗹𝗮 𝗶𝘀 𝗱𝗮𝘁𝗮 𝗼𝗿 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝘀𝘂𝗿𝗳𝗮𝗰𝗲 𝗮𝗿𝗲𝗮 𝗽𝗹𝘂𝘀 𝗳𝘂𝗻𝗰𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜, 𝗻𝗼𝘁 𝗼𝗻𝗲 𝗼𝗿 𝘁𝗵𝗲 𝗼𝘁𝗵𝗲𝗿. Look at why Claude is winning. Anthropic isn't competing on model benchmarks, they're competing on functional workflow. Building for the user, not the leaderboard. That's the playbook vertical incumbents need to run. Take the moat you already have, whether it's regulatory or data-entrenchment, layer genuine workflow AI on top, and the challenger can't catch you. The vendors that do both win the decade. The ones that rely on inertia alone get caught. The ones that ship AI without an anchor get commoditized. You need both.

𝗧𝗵𝗲 𝗯𝘂𝘆𝗲𝗿 𝗶𝘀 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗵𝗶𝘀 𝗽𝗹𝗮𝗶𝗻𝗹𝘆. A study we ran with Battery Ventures on AI adoption in the Office of the CFO (battery.com/blog/first-codin…) surveyed 129 finance leaders at companies from $50M to $5B in revenue. 77% said they want to uplevel existing systems with AI from new vendors that layer onto existing systems. Only 15% want to replace their current system of record with an AI-native platform. The incumbent wins if they ship AI. The AI-native challenger wins only if the incumbent doesn't.

The signal shows up in our VoC data too. In regulated verticals, mission criticality scores cluster above 9, and NPS doesn't track satisfaction, it tracks switching friction. Customers will tell you the product is mediocre and still score it 9 on "would not switch" because the compliance team vetoes any alternative. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝘁𝘂𝗿𝗲 𝗼𝗳 𝗮 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲-𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗻𝗱𝗼𝗿, 𝗮𝘀 𝗹𝗼𝗻𝗴 𝗮𝘀 𝘁𝗵𝗮𝘁 𝘃𝗲𝗻𝗱𝗼𝗿 𝗶𝘀 𝗮𝗰𝘁𝗶𝘃𝗲𝗹𝘆 𝘀𝗵𝗶𝗽𝗽𝗶𝗻𝗴 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝘁𝗵𝗲 𝗔𝗜 𝗰𝘂𝗿𝘃𝗲.

Which brings us back to the second business for everyone outside the regulated or data-entrenched moat. Seat ARR got them to $100M. But with the shift to agentic workforce structures, partial human capital replacement, and pricing pressure compressing margins, the traditional SaaS model has to transform fast. The next $500M comes from monetizing the installed base: marketplace rake on demand they generate for their own customers, capital products underwritten by their own transaction data, supplier monetization, brand partnerships, group buying. The assets are already sitting there. Captive SMB audience. Proprietary transaction and behavioral data. A distribution pipe (the UI itself) that delivers new products at near-zero CAC.

𝗪𝗵𝗮𝘁'𝘀 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 𝗶𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘄𝗶𝗹𝗹. Monetizing the installed base requires a different org than the one that got you to scale. Different GTM, P&L optics, and talent. Founders and boards under-invest because year one looks worse before it looks better, and public markets punish any SaaS multiple that starts to look like fintech or marketplace. So the second business never ships. The round prices in the optionality. The multiple compresses. The exit underwhelms.

𝗧𝗵𝗿𝗲𝗲 𝗱𝗶𝗹𝗶𝗴𝗲𝗻𝗰𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴:

𝟭. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗰𝗼𝗺𝗲𝘀 𝗳𝗿𝗼𝗺 𝘀𝗼𝘂𝗿𝗰𝗲𝘀 𝗼𝘁𝗵𝗲𝗿 𝘁𝗵𝗮𝗻 𝘀𝘂𝗯𝘀𝗰𝗿𝗶𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗽𝗿𝗼𝗰𝗲𝘀𝘀𝗶𝗻𝗴? Under 5%, they haven't started. 10 to 20%, thesis is live. Over 20%, it's working.

𝟮. 𝗛𝗼𝘄 𝗵𝗮𝗿𝗱 𝘄𝗼𝘂𝗹𝗱 𝗶𝘁 𝗯𝗲 𝘁𝗼 𝗿𝗲𝗰𝗿𝗲𝗮𝘁𝗲 𝘁𝗵𝗶𝘀 𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗮𝘁𝗰𝗵 𝘄𝗶𝘁𝗵 𝗔𝗜 𝘁𝗼𝗱𝗮𝘆? If a well-funded team with Claude and six engineers could rebuild the functional product in nine months, the software isn't the moat. The moat has to live somewhere else: proprietary data, a network, integrations, or regulatory surface area the challenger can't clear. If you can't point to at least one, you're underwriting a melting ice cube.

𝟯. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗯𝘂𝘆𝗲𝗿'𝘀 𝘀𝘁𝗶𝗰𝗸𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆, 𝗮𝗻𝗱 𝘄𝗵𝗶𝗰𝗵 𝘄𝗮𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗿𝘂𝗹𝗲 𝘀𝗲𝘁 𝗺𝗼𝘃𝗶𝗻𝗴? A regulatory moat evaporates if the regulation simplifies. Underwrite the direction of travel, not just the current state.

𝗔𝗻𝗱 𝘁𝗵𝗲 𝗰𝗹𝗼𝗰𝗸 𝗶𝘀 𝘁𝗶𝗴𝗵𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲. Retention in enterprise SaaS has largely been defined by the pain of systems replacement, not genuine moat. If the stickiness isn't backed by proprietary data, a harvesting flywheel, or regulatory surface area, those vendors are about to get disrupted. Pure seat-based pricing is dying unless vendors embrace agent-seat models, and LLM providers have been subsidizing the market on token cost, with recent pricing shifts signaling cash reserves aren't infinite.

𝗛𝗲𝗿𝗲'𝘀 𝘁𝗵𝗲 𝘂𝗻𝗱𝗲𝗿𝗮𝗽𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗲𝗱 𝗽𝗼𝗶𝗻𝘁: 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘄𝗼𝗿𝘀𝗲 𝗴𝗿𝗼𝘀𝘀 𝗺𝗮𝗿𝗴𝗶𝗻𝘀 𝘁𝗵𝗮𝗻 𝗦𝗮𝗮𝗦 𝗶𝗻𝗰𝘂𝗺𝗯𝗲𝗻𝘁𝘀, 𝗻𝗼𝘁 𝗯𝗲𝘁𝘁𝗲𝗿. Inference costs haven't collapsed, and burning VC cash to subsidize unit economics is a bridge, not a business model. The incumbents should be winning on P&L. They're losing on product velocity and AI-readiness. That's a solvable problem if the board has the will to ship. Vendors without a second business, without a data moat, and without regulatory insulation will still lose, despite having better margins than their AI-native challengers. Customers switch on features and speed, not on unit economics.

𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗿𝘁𝗶𝗰𝗮𝗹𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝗹𝗮𝘀𝘁 𝘀𝗮𝗳𝗲 𝗵𝗮𝗿𝗯𝗼𝗿, 𝗮𝗻𝗱 𝗼𝗻𝗹𝘆 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝗱𝗮𝘁𝗮 𝗯𝗿𝗲𝗮𝗱𝘁𝗵 𝗮𝗻𝗱 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲. Everywhere else, the premium is about to get competed away. Any fund underwriting vertical SaaS exposure right now should be asking the second-business question before the next check clears. DM me, email me brad@crossoverresearch.com, or let's chat about your portfolio/underwriting process (book.crossoverresearch.com).

Crossoverresearch.com

4

2

16

3,520

Brad Lyons retweeted

Apr 21

The goal of AI isn't to replace software. It's to replace labor

35

34

570

65,270

Apr 19

𝗧𝗛𝗘 𝗔𝗜 𝗣𝗟𝗔𝗬𝗕𝗢𝗢𝗞 𝗙𝗢𝗥 𝗢𝗣𝗘𝗥𝗔𝗧𝗢𝗥𝗦 𝗔𝗡𝗗 𝗜𝗡𝗩𝗘𝗦𝗧𝗢𝗥𝗦

The technical stack matters more than ever. If the vendors in your stack aren't shipping aggressively, your competitors are already outpacing you. Every C-suite and CTO should be running a full evaluation of vendor product development timelines right now. 𝗦𝗽𝗲𝗲𝗱 𝗶𝘀 𝘁𝗵𝗲 𝗳𝗮𝗰𝘁𝗼𝗿 𝘁𝗵𝗮𝘁 𝗺𝗮𝘁𝘁𝗲𝗿𝘀 𝗺𝗼𝘀𝘁, and the delta between internal tooling and your existing vendors is what determines whether you're a 𝗹𝗲𝗮𝗱𝗲𝗿 𝗼𝗿 𝗮 𝗹𝗮𝗴𝗴𝗮𝗿𝗱.

Before I get into it, three questions every founder and C-suite team needs to answer:

1) When did you last audit your vendor stack for shipping velocity?

2) If Anthropic or OpenAI shipped your core capability tomorrow as a native feature, what would you still own?

3) Can you, the CEO, explain your product's AI architecture in under 5 minutes without deferring to your CTO?

𝗔𝗡𝗧𝗛𝗥𝗢𝗣𝗜𝗖 𝗕𝗔𝗦𝗘𝗟𝗜𝗡𝗘

In 30 days: Claude Opus 4.7. Claude Design. Project Glasswing with Mythos Preview. Cowork GA on Mac and Windows. Computer use in Cowork and Claude Code. Interactive apps on mobile. Auto mode and /ultrareview in Claude Code. 𝗠𝗼𝗿𝗲 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗦𝗮𝗮𝗦 𝘃𝗲𝗻𝗱𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘀𝗵𝗶𝗽𝗽𝗲𝗱 𝗶𝗻 𝘁𝘄𝗼 𝘆𝗲𝗮𝗿𝘀. Imagine an Olympian showing up to your after-work sports league. Cool to watch, not a fair fight.

And they sit in the 𝗿𝗶𝘀𝗸-𝗳𝗿𝗲𝗲 𝗶𝗻𝗰𝘂𝗯𝗮𝘁𝗼𝗿 𝘀𝗲𝗮𝘁. Every business building on Anthropic's platform to stay competitive is also showing them which vectors are worth attacking. Claude Design came for Figma the week it shipped. Claude Code came for Cursor. 𝗬𝗼𝘂 𝗯𝘂𝗶𝗹𝗱 𝘁𝗵𝗲 𝗺𝗮𝗿𝗸𝗲𝘁. 𝗔𝗻𝘁𝗵𝗿𝗼𝗽𝗶𝗰 𝗿𝗲𝗮𝗱𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝗹. 𝗧𝗵𝗲𝘆 𝘀𝗵𝗶𝗽 𝗻𝗮𝘁𝗶𝘃𝗲.

Reading the signal only works if you can act on it faster than anyone else, and that's why 𝗔𝗻𝘁𝗵𝗿𝗼𝗽𝗶𝗰'𝘀 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝘀 𝗿𝘂𝗻 𝘄𝗶𝘁𝗵𝗼𝘂𝘁 𝗮 𝘁𝗼𝗸𝗲𝗻 𝗰𝗲𝗶𝗹𝗶𝗻𝗴. The NYT reported one engineer spent over $150,000 on Claude Code in a single month. 𝗧𝗵𝗮𝘁'𝘀 𝗻𝗼𝘁 𝗮 𝗯𝘂𝗴. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝗶𝗻𝗰𝗲𝗻𝘁𝗶𝘃𝗲 𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲. Uber rolled Claude Code to 5,000 engineers and 𝗯𝗹𝗲𝘄 𝗶𝘁𝘀 𝗲𝗻𝘁𝗶𝗿𝗲 𝟮𝟬𝟮𝟲 𝗔𝗜 𝗯𝘂𝗱𝗴𝗲𝘁 𝗶𝗻 𝗳𝗼𝘂𝗿 𝗺𝗼𝗻𝘁𝗵𝘀. CTO Praveen Neppalli Naga: "I'm back to the drawing board, because the budget I thought I would need is blown away already." He's replanning upward, not pulling back. 𝗧𝗵𝗮𝘁 𝗮𝘀𝘆𝗺𝗺𝗲𝘁𝗿𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗴𝗮𝗽: Anthropic ships without a cost ceiling. Every buyer ships with one.

𝗦𝗣𝗘𝗘𝗗 𝗜𝗦 𝗧𝗛𝗘 𝗠𝗢𝗔𝗧

Every SaaS vendor in your stack should be benchmarked against internal dev velocity. If your team with Claude can ship in weeks what your vendors take quarters to deliver, those vendors aren't buying you time anymore. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝗰𝗼𝘀𝘁𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗶𝗺𝗲. The question on every renewal is no longer "is this vendor reliable." It's 𝘄𝗼𝗿𝘁𝗵 𝘁𝗵𝗲 𝘃𝗲𝗹𝗼𝗰𝗶𝘁𝘆 𝗴𝗮𝗽 𝗶𝘁 𝗰𝗿𝗲𝗮𝘁𝗲𝘀. If the answer is no, they're the thing killing you.

𝗩𝗜𝗕𝗘 𝗦𝗟𝗢𝗣 𝗜𝗦 𝗔 𝗦𝗞𝗜𝗟𝗟 𝗜𝗦𝗦𝗨𝗘

Most people dismissing AI coding as slop are reacting to bad implementations, not AI itself. The slop they're seeing is real. 𝗜𝘁'𝘀 𝗮 𝘀𝗸𝗶𝗹𝗹 𝗮𝗻𝗱 𝗮𝗿𝗰𝗵𝗶𝘁𝗲𝗰𝘁𝘂𝗿𝗲 𝗽𝗿𝗼𝗯𝗹𝗲𝗺, 𝗻𝗼𝘁 𝗮 𝗺𝗼𝗱𝗲𝗹 𝗽𝗿𝗼𝗯𝗹𝗲𝗺. Good engineers put proper bounds in place: modular architecture, shared layers, fallback patterns, drift detection. 𝗗𝗼𝗻𝗲 𝗿𝗶𝗴𝗵𝘁, 𝘃𝗶𝗯𝗲 𝗰𝗼𝗱𝗶𝗻𝗴 𝗶𝘀 𝟭𝟬𝘅 𝗹𝗲𝘃𝗲𝗿𝗮𝗴𝗲. The architecture you build on determines whether AI compounds or corrupts. Proof point: Boris Cherny, head of Claude Code, said Anthropic's AI coded "pretty much all" of Cowork, 𝗯𝘂𝗶𝗹𝘁 𝗶𝗻 𝗿𝗼𝘂𝗴𝗵𝗹𝘆 𝘁𝘄𝗼 𝘄𝗲𝗲𝗸𝘀.

𝗧𝗛𝗘 𝗦𝗧𝗔𝗥𝗧𝗨𝗣 𝗪𝗜𝗡𝗗𝗢𝗪

Startups with no legacy architecture have a 𝗻𝗮𝗿𝗿𝗼𝘄, 𝗿𝗲𝗮𝗹 𝘄𝗶𝗻𝗱𝗼𝘄 𝘁𝗼 𝗵𝗶𝘁 𝗔𝗥𝗥 𝘁𝗵𝗿𝗲𝘀𝗵𝗼𝗹𝗱𝘀 𝗻𝗼 𝗼𝗻𝗲 𝘁𝗵𝗼𝘂𝗴𝗵𝘁 𝗽𝗼𝘀𝘀𝗶𝗯𝗹𝗲. Disadvantage: data breadth. Advantage: data capture design. 𝗔𝗿𝗰𝗵𝗶𝘁𝗲𝗰𝘁 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗳𝗿𝗼𝗺 𝗱𝗮𝘆 𝗼𝗻𝗲 𝗮𝗻𝗱 𝘆𝗼𝘂 𝗰𝗼𝗺𝗽𝗼𝘂𝗻𝗱 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮 𝗳𝗮𝘀𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗲𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲𝘀 𝗰𝗮𝗻 𝗽𝗼𝗿𝘁 𝘁𝗵𝗲𝗶𝗿𝘀.

𝗔𝗜-𝗙𝗜𝗥𝗦𝗧 𝗖-𝗦𝗨𝗜𝗧𝗘𝗦 𝗦𝗛𝗢𝗨𝗟𝗗 𝗕𝗘 𝗔𝗡 𝗨𝗡𝗗𝗘𝗥𝗪𝗥𝗜𝗧𝗜𝗡𝗚 𝗥𝗘𝗤𝗨𝗜𝗥𝗘𝗠𝗘𝗡𝗧

𝗙𝗼𝘂𝗻𝗱𝗲𝗿𝘀 𝗮𝗻𝗱 𝗖-𝘀𝘂𝗶𝘁𝗲𝘀 𝘄𝗵𝗼 𝗱𝗲𝗹𝗲𝗴𝗮𝘁𝗲 𝗔𝗜 𝗳𝗹𝘂𝗲𝗻𝗰𝘆 𝗵𝗮𝘃𝗲 𝗮𝗹𝗿𝗲𝗮𝗱𝘆 𝗹𝗼𝘀𝘁. Secondhand information moves too slowly in a market where architecture decisions compound daily. C-suites set vision, and successful AI deployments come from leaders who can 𝗰𝗼𝗻𝗳𝗶𝗴𝘂𝗿𝗲, 𝗻𝗼𝘁 𝗷𝘂𝘀𝘁 𝗮𝗽𝗽𝗿𝗼𝘃𝗲. If you're deferring to someone more technical than you on strategic AI calls, you're reacting to a market someone else is reading in real time.

𝗪𝗛𝗔𝗧 𝗔𝗖𝗧𝗨𝗔𝗟𝗟𝗬 𝗦𝗟𝗢𝗪𝗦 𝗘𝗡𝗧𝗘𝗥𝗣𝗥𝗜𝗦𝗘𝗦

𝗧𝗵𝗲 𝗿𝗲𝗮𝗹 𝗸𝗶𝗹𝗹𝗲𝗿𝘀: procurement cycles, security review, SOC 2 / HIPAA / FedRAMP regimes, change management, and RAG that doesn't scale to real corpus volume. Most enterprises are managing AI like a side project inside a pre-AI codebase. 𝗧𝗵𝗲 𝗽𝗿𝗼𝗱𝘂𝗰𝘁𝗶𝗼𝗻 𝗯𝗿𝗲𝗮𝗸𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝘀𝘆𝗺𝗽𝘁𝗼𝗺, 𝗻𝗼𝘁 𝘁𝗵𝗲 𝗱𝗶𝘀𝗲𝗮𝘀𝗲.

𝗧𝗵𝗲 𝗳𝗶𝘅 𝗶𝘀𝗻'𝘁 𝗮𝗻𝗼𝘁𝗵𝗲𝗿 𝗽𝗶𝗹𝗼𝘁. Stand up a dedicated AI review track so security and procurement don't restart from zero on every vendor eval. Put a single C-suite owner on AI budget with authority to spend, not a committee. Build AI-native services parallel to the legacy codebase, not bolted onto it.

𝗧𝗵𝗶𝘀 𝗶𝘀 𝘄𝗵𝗲𝗿𝗲 𝗖𝗿𝗼𝘀𝘀𝗼𝘃𝗲𝗿 𝘀𝗽𝗲𝗻𝗱𝘀 𝗺𝗼𝘀𝘁 𝗼𝗳 𝗶𝘁𝘀 𝘁𝗶𝗺𝗲. We score AI Capability and AI Resilience across PE portfolios and operators, and most organizations are further behind than they think.

𝗧𝗛𝗘 𝗪𝗥𝗔𝗣𝗣𝗘𝗥 𝗕𝗟𝗢𝗢𝗗𝗕𝗔𝗧𝗛

The majority of companies marketed as "AI-native" are repackaged base models with a UI on top. 𝗙𝗼𝘂𝗻𝗱𝗲𝗿𝘀 𝗮𝗻𝗱 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗻𝗲𝗲𝗱 𝘁𝗼 𝗴𝗲𝘁 𝗺𝘂𝗰𝗵 𝘀𝗵𝗮𝗿𝗽𝗲𝗿 𝗮𝘁 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘁𝗿𝘂𝗲 𝗺𝗼𝗮𝘁𝘀 𝗳𝗿𝗼𝗺 𝗮 𝗵𝗲𝗮𝗱 𝘀𝘁𝗮𝗿𝘁 𝗱𝗿𝗲𝘀𝘀𝗲𝗱 𝘂𝗽 𝗮𝘀 𝗱𝗲𝗳𝗲𝗻𝘀𝗶𝗯𝗶𝗹𝗶𝘁𝘆. Some wrappers will monetize fast and sell to strategics in the next 2-4 years. Most won't. Two forces compress the field: AI participation costs (infrastructure plus token burn) keep rising, and customer wallet share for AI tooling is finite. Only so many winners emerge per category. 𝗧𝗵𝗲 𝗿𝗲𝘀𝘁 𝗿𝗲𝘁𝘂𝗿𝗻 𝗰𝗮𝗽𝗶𝘁𝗮𝗹 𝗮𝘁 𝗯𝗲𝘀𝘁, 𝘇𝗲𝗿𝗼 𝗮𝘁 𝘄𝗼𝗿𝘀𝘁.

𝗪𝗛𝗢 𝗦𝗨𝗥𝗩𝗜𝗩𝗘𝗦

Three archetypes make it through the cycle.

Vendors with proprietary data, engineered workflows, regulated-vertical lock-in, or hardware-attached integrations deep enough that a native platform release can't replace them. SaaS incumbents that rebuild before their slot gets benchmarked out of the stack. Founders fluent enough to dictate AI strategy, not delegate it. Configured, not approved. 𝗜𝗳 𝘆𝗼𝘂 𝗰𝗮𝗻'𝘁 𝗮𝗿𝘁𝗶𝗰𝘂𝗹𝗮𝘁𝗲 𝗵𝗼𝘄 𝗟𝗟𝗠𝘀 𝗳𝗶𝘁 𝘆𝗼𝘂𝗿 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗶𝗻 𝘂𝗻𝗱𝗲𝗿 𝟱 𝗺𝗶𝗻𝘂𝘁𝗲𝘀, 𝘆𝗼𝘂'𝗿𝗲 𝗻𝗼𝘁 𝗶𝗻𝘃𝗲𝘀𝘁𝗮𝗯𝗹𝗲.

Email brad@crossoverresearch.com with "investor checklist" or "founder checklist" and I'll send you the 20 questions every investor or every founder should be asking right now.

Apr 17

In August I wrote a thesis I never published. The funds I was warning were key Crossover Research clients, so I stayed quiet. Since then, 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗺𝘂𝗹𝘁𝗶𝗽𝗹𝗲𝘀 𝗮𝗿𝗲 𝗱𝗼𝘄𝗻 𝟱𝟬% . Salesforce $CRM, ServiceNow $NOW, Adobe $ADBE, Workday $WDAY all off 40% from highs. Thomson Reuters $TRI dropped 16% in a single session on the Anthropic legal agent launch. The SaaSpocalypse arrived. So here's the follow-up. Not commentary on what happened, but where I think this goes next.

Most vertical SaaS companies aren't underperforming because their software is bad. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲𝘆 𝗻𝗲𝘃𝗲𝗿 𝗯𝘂𝗶𝗹𝘁 𝘁𝗵𝗲 𝘀𝗲𝗰𝗼𝗻𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀. And the first business is under attack. For twenty years, one of the biggest SaaS moats was engineering complexity: deep technical talent, long roadmaps, compounding codebases that were genuinely hard to replicate. 𝗔𝗜 𝘂𝗽𝗲𝗻𝗱𝗲𝗱 𝘁𝗵𝗮𝘁 𝗮𝗹𝗺𝗼𝘀𝘁 𝗼𝘃𝗲𝗿𝗻𝗶𝗴𝗵𝘁.

Product development is democratizing to operators with no code background but strong product vision. Look at Anthropic: they've built the engine and are shipping lookalike products at a cadence that would have taken a legacy SaaS vendor three years of roadmap, with a fraction of the headcount. That pace can kill legacy businesses overnight.

𝗜𝗳 𝘁𝗵𝗲 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗺𝗼𝗮𝘁 𝗶𝘀 𝗴𝗼𝗻𝗲, 𝗳𝗼𝘂𝗿 𝗺𝗼𝗮𝘁𝘀 𝗿𝗲𝗺𝗮𝗶𝗻: 𝗱𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻, 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮, 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄 𝗯𝗿𝗲𝗮𝗱𝘁𝗵, 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗶𝗼𝗻. The first three are moats the company builds. The fourth is a moat the company captures, and it's the one most resistant to AI disruption.

𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗰𝗼𝗺𝗽𝗹𝗲𝘅𝗶𝘁𝘆 𝗰𝗿𝗲𝗮𝘁𝗲𝘀 𝘀𝘄𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝗰𝗼𝘀𝘁𝘀 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗲 𝗻𝗼𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗱𝗼 𝘄𝗶𝘁𝗵 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗾𝘂𝗮𝗹𝗶𝘁𝘆. Once a vendor is embedded in a compliance workflow, ripping them out means re-attesting, re-auditing, and re-certifying every downstream process. The buyer isn't paying for software, they're paying for the accumulated paper trail. Tyler Technologies ($TYL) is the clearest version of the pattern. State and local government software across courts, public safety, assessment, and ERP. Every module is married to statutory process, FIPS, CJIS, audit trails, and procurement cycles that take years. TYL is down 42% TTM and 2026 guidance came in soft, but the moat didn't break. Revenue still compounded, and government procurement runs on five-year cycles, not five-week news cycles. Veeva is the sharper version. Revenue up 16% in FY26, Q4 beat, the stock still down 25%. The market is selling execution, not weakness. Guidewire in P&C insurance, where regulatory filings and rate approvals anchor the stack, sits in the same setup: still compounding ARR, still winning cloud conversions, multiple reset anyway. Same pattern across all three: multiples compressed, fundamentals intact. The moat is the regulatory surface area itself, and it compounds because the rules get more complex, not less.

𝗜 𝘄𝗮𝘀 𝗹𝗼𝗻𝗴 𝗣𝗮𝗹𝗮𝗻𝘁𝗶𝗿 𝗮𝘁 $𝟭𝟯 (read that here: x.com/blyons151/status/17920…). 𝗡𝗼𝘁 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗺𝗼𝗱𝗲𝗹 𝗼𝗿 𝘁𝗵𝗲 𝘁𝗼𝗼𝗹𝗶𝗻𝗴. 𝗕𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗼𝗻𝘁𝗼𝗹𝗼𝗴𝘆. Palantir is the proprietary-data version of the regulatory thesis. Once Palantir sits between the customer and their own data, ripping it out means rebuilding the data model from scratch. Snowflake and Databricks never had that entrenchment layer. AIP bootcamps then turned the data moat into a distribution moat: 660 bootcamps in a single quarter, 94% y/y US customer deal growth, bookings at 1.9x sales. Own the data, ship functional AI on top of it, let the GTM compound. Every vertical incumbent has a version of this available. The question is whether they'll build it before a challenger does.

But regulatory insulation is necessary, not sufficient. Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade.

𝗧𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗳𝗼𝗿𝗺𝘂𝗹𝗮 𝗶𝘀 𝗱𝗮𝘁𝗮 𝗼𝗿 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝘀𝘂𝗿𝗳𝗮𝗰𝗲 𝗮𝗿𝗲𝗮 𝗽𝗹𝘂𝘀 𝗳𝘂𝗻𝗰𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜, 𝗻𝗼𝘁 𝗼𝗻𝗲 𝗼𝗿 𝘁𝗵𝗲 𝗼𝘁𝗵𝗲𝗿. Look at why Claude is winning. Anthropic isn't competing on model benchmarks, they're competing on functional workflow. Building for the user, not the leaderboard. That's the playbook vertical incumbents need to run. Take the moat you already have, whether it's regulatory or data-entrenchment, layer genuine workflow AI on top, and the challenger can't catch you. The vendors that do both win the decade. The ones that rely on inertia alone get caught. The ones that ship AI without an anchor get commoditized. You need both.

𝗧𝗵𝗲 𝗯𝘂𝘆𝗲𝗿 𝗶𝘀 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗵𝗶𝘀 𝗽𝗹𝗮𝗶𝗻𝗹𝘆. A study we ran with Battery Ventures on AI adoption in the Office of the CFO (battery.com/blog/first-codin…) surveyed 129 finance leaders at companies from $50M to $5B in revenue. 77% said they want to uplevel existing systems with AI from new vendors that layer onto existing systems. Only 15% want to replace their current system of record with an AI-native platform. The incumbent wins if they ship AI. The AI-native challenger wins only if the incumbent doesn't.

The signal shows up in our VoC data too. In regulated verticals, mission criticality scores cluster above 9, and NPS doesn't track satisfaction, it tracks switching friction. Customers will tell you the product is mediocre and still score it 9 on "would not switch" because the compliance team vetoes any alternative. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝘁𝘂𝗿𝗲 𝗼𝗳 𝗮 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲-𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗻𝗱𝗼𝗿, 𝗮𝘀 𝗹𝗼𝗻𝗴 𝗮𝘀 𝘁𝗵𝗮𝘁 𝘃𝗲𝗻𝗱𝗼𝗿 𝗶𝘀 𝗮𝗰𝘁𝗶𝘃𝗲𝗹𝘆 𝘀𝗵𝗶𝗽𝗽𝗶𝗻𝗴 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝘁𝗵𝗲 𝗔𝗜 𝗰𝘂𝗿𝘃𝗲.

Which brings us back to the second business for everyone outside the regulated or data-entrenched moat. Seat ARR got them to $100M. But with the shift to agentic workforce structures, partial human capital replacement, and pricing pressure compressing margins, the traditional SaaS model has to transform fast. The next $500M comes from monetizing the installed base: marketplace rake on demand they generate for their own customers, capital products underwritten by their own transaction data, supplier monetization, brand partnerships, group buying. The assets are already sitting there. Captive SMB audience. Proprietary transaction and behavioral data. A distribution pipe (the UI itself) that delivers new products at near-zero CAC.

𝗪𝗵𝗮𝘁'𝘀 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 𝗶𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘄𝗶𝗹𝗹. Monetizing the installed base requires a different org than the one that got you to scale. Different GTM, P&L optics, and talent. Founders and boards under-invest because year one looks worse before it looks better, and public markets punish any SaaS multiple that starts to look like fintech or marketplace. So the second business never ships. The round prices in the optionality. The multiple compresses. The exit underwhelms.

𝗧𝗵𝗿𝗲𝗲 𝗱𝗶𝗹𝗶𝗴𝗲𝗻𝗰𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴:

𝟭. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗰𝗼𝗺𝗲𝘀 𝗳𝗿𝗼𝗺 𝘀𝗼𝘂𝗿𝗰𝗲𝘀 𝗼𝘁𝗵𝗲𝗿 𝘁𝗵𝗮𝗻 𝘀𝘂𝗯𝘀𝗰𝗿𝗶𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗽𝗿𝗼𝗰𝗲𝘀𝘀𝗶𝗻𝗴? Under 5%, they haven't started. 10 to 20%, thesis is live. Over 20%, it's working.

𝟮. 𝗛𝗼𝘄 𝗵𝗮𝗿𝗱 𝘄𝗼𝘂𝗹𝗱 𝗶𝘁 𝗯𝗲 𝘁𝗼 𝗿𝗲𝗰𝗿𝗲𝗮𝘁𝗲 𝘁𝗵𝗶𝘀 𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗮𝘁𝗰𝗵 𝘄𝗶𝘁𝗵 𝗔𝗜 𝘁𝗼𝗱𝗮𝘆? If a well-funded team with Claude and six engineers could rebuild the functional product in nine months, the software isn't the moat. The moat has to live somewhere else: proprietary data, a network, integrations, or regulatory surface area the challenger can't clear. If you can't point to at least one, you're underwriting a melting ice cube.

𝟯. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗯𝘂𝘆𝗲𝗿'𝘀 𝘀𝘁𝗶𝗰𝗸𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆, 𝗮𝗻𝗱 𝘄𝗵𝗶𝗰𝗵 𝘄𝗮𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗿𝘂𝗹𝗲 𝘀𝗲𝘁 𝗺𝗼𝘃𝗶𝗻𝗴? A regulatory moat evaporates if the regulation simplifies. Underwrite the direction of travel, not just the current state.

𝗔𝗻𝗱 𝘁𝗵𝗲 𝗰𝗹𝗼𝗰𝗸 𝗶𝘀 𝘁𝗶𝗴𝗵𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲. Retention in enterprise SaaS has largely been defined by the pain of systems replacement, not genuine moat. If the stickiness isn't backed by proprietary data, a harvesting flywheel, or regulatory surface area, those vendors are about to get disrupted. Pure seat-based pricing is dying unless vendors embrace agent-seat models, and LLM providers have been subsidizing the market on token cost, with recent pricing shifts signaling cash reserves aren't infinite.

𝗛𝗲𝗿𝗲'𝘀 𝘁𝗵𝗲 𝘂𝗻𝗱𝗲𝗿𝗮𝗽𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗲𝗱 𝗽𝗼𝗶𝗻𝘁: 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘄𝗼𝗿𝘀𝗲 𝗴𝗿𝗼𝘀𝘀 𝗺𝗮𝗿𝗴𝗶𝗻𝘀 𝘁𝗵𝗮𝗻 𝗦𝗮𝗮𝗦 𝗶𝗻𝗰𝘂𝗺𝗯𝗲𝗻𝘁𝘀, 𝗻𝗼𝘁 𝗯𝗲𝘁𝘁𝗲𝗿. Inference costs haven't collapsed, and burning VC cash to subsidize unit economics is a bridge, not a business model. The incumbents should be winning on P&L. They're losing on product velocity and AI-readiness. That's a solvable problem if the board has the will to ship. Vendors without a second business, without a data moat, and without regulatory insulation will still lose, despite having better margins than their AI-native challengers. Customers switch on features and speed, not on unit economics.

𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗿𝘁𝗶𝗰𝗮𝗹𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝗹𝗮𝘀𝘁 𝘀𝗮𝗳𝗲 𝗵𝗮𝗿𝗯𝗼𝗿, 𝗮𝗻𝗱 𝗼𝗻𝗹𝘆 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝗱𝗮𝘁𝗮 𝗯𝗿𝗲𝗮𝗱𝘁𝗵 𝗮𝗻𝗱 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲. Everywhere else, the premium is about to get competed away. Any fund underwriting vertical SaaS exposure right now should be asking the second-business question before the next check clears. DM me, email me brad@crossoverresearch.com, or let's chat about your portfolio/underwriting process (book.crossoverresearch.com).

Crossoverresearch.com

2

5

22

6,934

Apr 17

In August I wrote a thesis I never published. The funds I was warning were key Crossover Research clients, so I stayed quiet. Since then, 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗺𝘂𝗹𝘁𝗶𝗽𝗹𝗲𝘀 𝗮𝗿𝗲 𝗱𝗼𝘄𝗻 𝟱𝟬% . Salesforce $CRM, ServiceNow $NOW, Adobe $ADBE, Workday $WDAY all off 40% from highs. Thomson Reuters $TRI dropped 16% in a single session on the Anthropic legal agent launch. The SaaSpocalypse arrived. So here's the follow-up. Not commentary on what happened, but where I think this goes next.

Most vertical SaaS companies aren't underperforming because their software is bad. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲𝘆 𝗻𝗲𝘃𝗲𝗿 𝗯𝘂𝗶𝗹𝘁 𝘁𝗵𝗲 𝘀𝗲𝗰𝗼𝗻𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀. And the first business is under attack. For twenty years, one of the biggest SaaS moats was engineering complexity: deep technical talent, long roadmaps, compounding codebases that were genuinely hard to replicate. 𝗔𝗜 𝘂𝗽𝗲𝗻𝗱𝗲𝗱 𝘁𝗵𝗮𝘁 𝗮𝗹𝗺𝗼𝘀𝘁 𝗼𝘃𝗲𝗿𝗻𝗶𝗴𝗵𝘁.

Product development is democratizing to operators with no code background but strong product vision. Look at Anthropic: they've built the engine and are shipping lookalike products at a cadence that would have taken a legacy SaaS vendor three years of roadmap, with a fraction of the headcount. That pace can kill legacy businesses overnight.

𝗜𝗳 𝘁𝗵𝗲 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗺𝗼𝗮𝘁 𝗶𝘀 𝗴𝗼𝗻𝗲, 𝗳𝗼𝘂𝗿 𝗺𝗼𝗮𝘁𝘀 𝗿𝗲𝗺𝗮𝗶𝗻: 𝗱𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻, 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮, 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄 𝗯𝗿𝗲𝗮𝗱𝘁𝗵, 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗶𝗼𝗻. The first three are moats the company builds. The fourth is a moat the company captures, and it's the one most resistant to AI disruption.

𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗰𝗼𝗺𝗽𝗹𝗲𝘅𝗶𝘁𝘆 𝗰𝗿𝗲𝗮𝘁𝗲𝘀 𝘀𝘄𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝗰𝗼𝘀𝘁𝘀 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗲 𝗻𝗼𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗱𝗼 𝘄𝗶𝘁𝗵 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗾𝘂𝗮𝗹𝗶𝘁𝘆. Once a vendor is embedded in a compliance workflow, ripping them out means re-attesting, re-auditing, and re-certifying every downstream process. The buyer isn't paying for software, they're paying for the accumulated paper trail. Tyler Technologies ($TYL) is the clearest version of the pattern. State and local government software across courts, public safety, assessment, and ERP. Every module is married to statutory process, FIPS, CJIS, audit trails, and procurement cycles that take years. TYL is down 42% TTM and 2026 guidance came in soft, but the moat didn't break. Revenue still compounded, and government procurement runs on five-year cycles, not five-week news cycles. Veeva is the sharper version. Revenue up 16% in FY26, Q4 beat, the stock still down 25%. The market is selling execution, not weakness. Guidewire in P&C insurance, where regulatory filings and rate approvals anchor the stack, sits in the same setup: still compounding ARR, still winning cloud conversions, multiple reset anyway. Same pattern across all three: multiples compressed, fundamentals intact. The moat is the regulatory surface area itself, and it compounds because the rules get more complex, not less.

𝗜 𝘄𝗮𝘀 𝗹𝗼𝗻𝗴 𝗣𝗮𝗹𝗮𝗻𝘁𝗶𝗿 𝗮𝘁 $𝟭𝟯 (read that here: x.com/blyons151/status/17920…). 𝗡𝗼𝘁 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗺𝗼𝗱𝗲𝗹 𝗼𝗿 𝘁𝗵𝗲 𝘁𝗼𝗼𝗹𝗶𝗻𝗴. 𝗕𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗼𝗻𝘁𝗼𝗹𝗼𝗴𝘆. Palantir is the proprietary-data version of the regulatory thesis. Once Palantir sits between the customer and their own data, ripping it out means rebuilding the data model from scratch. Snowflake and Databricks never had that entrenchment layer. AIP bootcamps then turned the data moat into a distribution moat: 660 bootcamps in a single quarter, 94% y/y US customer deal growth, bookings at 1.9x sales. Own the data, ship functional AI on top of it, let the GTM compound. Every vertical incumbent has a version of this available. The question is whether they'll build it before a challenger does.

But regulatory insulation is necessary, not sufficient. Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade.

𝗧𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗳𝗼𝗿𝗺𝘂𝗹𝗮 𝗶𝘀 𝗱𝗮𝘁𝗮 𝗼𝗿 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝘀𝘂𝗿𝗳𝗮𝗰𝗲 𝗮𝗿𝗲𝗮 𝗽𝗹𝘂𝘀 𝗳𝘂𝗻𝗰𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜, 𝗻𝗼𝘁 𝗼𝗻𝗲 𝗼𝗿 𝘁𝗵𝗲 𝗼𝘁𝗵𝗲𝗿. Look at why Claude is winning. Anthropic isn't competing on model benchmarks, they're competing on functional workflow. Building for the user, not the leaderboard. That's the playbook vertical incumbents need to run. Take the moat you already have, whether it's regulatory or data-entrenchment, layer genuine workflow AI on top, and the challenger can't catch you. The vendors that do both win the decade. The ones that rely on inertia alone get caught. The ones that ship AI without an anchor get commoditized. You need both.

𝗧𝗵𝗲 𝗯𝘂𝘆𝗲𝗿 𝗶𝘀 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗵𝗶𝘀 𝗽𝗹𝗮𝗶𝗻𝗹𝘆. A study we ran with Battery Ventures on AI adoption in the Office of the CFO (battery.com/blog/first-codin…) surveyed 129 finance leaders at companies from $50M to $5B in revenue. 77% said they want to uplevel existing systems with AI from new vendors that layer onto existing systems. Only 15% want to replace their current system of record with an AI-native platform. The incumbent wins if they ship AI. The AI-native challenger wins only if the incumbent doesn't.

The signal shows up in our VoC data too. In regulated verticals, mission criticality scores cluster above 9, and NPS doesn't track satisfaction, it tracks switching friction. Customers will tell you the product is mediocre and still score it 9 on "would not switch" because the compliance team vetoes any alternative. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝘁𝘂𝗿𝗲 𝗼𝗳 𝗮 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲-𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗻𝗱𝗼𝗿, 𝗮𝘀 𝗹𝗼𝗻𝗴 𝗮𝘀 𝘁𝗵𝗮𝘁 𝘃𝗲𝗻𝗱𝗼𝗿 𝗶𝘀 𝗮𝗰𝘁𝗶𝘃𝗲𝗹𝘆 𝘀𝗵𝗶𝗽𝗽𝗶𝗻𝗴 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝘁𝗵𝗲 𝗔𝗜 𝗰𝘂𝗿𝘃𝗲.

Which brings us back to the second business for everyone outside the regulated or data-entrenched moat. Seat ARR got them to $100M. But with the shift to agentic workforce structures, partial human capital replacement, and pricing pressure compressing margins, the traditional SaaS model has to transform fast. The next $500M comes from monetizing the installed base: marketplace rake on demand they generate for their own customers, capital products underwritten by their own transaction data, supplier monetization, brand partnerships, group buying. The assets are already sitting there. Captive SMB audience. Proprietary transaction and behavioral data. A distribution pipe (the UI itself) that delivers new products at near-zero CAC.

𝗪𝗵𝗮𝘁'𝘀 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 𝗶𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘄𝗶𝗹𝗹. Monetizing the installed base requires a different org than the one that got you to scale. Different GTM, P&L optics, and talent. Founders and boards under-invest because year one looks worse before it looks better, and public markets punish any SaaS multiple that starts to look like fintech or marketplace. So the second business never ships. The round prices in the optionality. The multiple compresses. The exit underwhelms.

𝗧𝗵𝗿𝗲𝗲 𝗱𝗶𝗹𝗶𝗴𝗲𝗻𝗰𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴:

𝟭. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗰𝗼𝗺𝗲𝘀 𝗳𝗿𝗼𝗺 𝘀𝗼𝘂𝗿𝗰𝗲𝘀 𝗼𝘁𝗵𝗲𝗿 𝘁𝗵𝗮𝗻 𝘀𝘂𝗯𝘀𝗰𝗿𝗶𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗽𝗿𝗼𝗰𝗲𝘀𝘀𝗶𝗻𝗴? Under 5%, they haven't started. 10 to 20%, thesis is live. Over 20%, it's working.

𝟮. 𝗛𝗼𝘄 𝗵𝗮𝗿𝗱 𝘄𝗼𝘂𝗹𝗱 𝗶𝘁 𝗯𝗲 𝘁𝗼 𝗿𝗲𝗰𝗿𝗲𝗮𝘁𝗲 𝘁𝗵𝗶𝘀 𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗮𝘁𝗰𝗵 𝘄𝗶𝘁𝗵 𝗔𝗜 𝘁𝗼𝗱𝗮𝘆? If a well-funded team with Claude and six engineers could rebuild the functional product in nine months, the software isn't the moat. The moat has to live somewhere else: proprietary data, a network, integrations, or regulatory surface area the challenger can't clear. If you can't point to at least one, you're underwriting a melting ice cube.

𝟯. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗯𝘂𝘆𝗲𝗿'𝘀 𝘀𝘁𝗶𝗰𝗸𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆, 𝗮𝗻𝗱 𝘄𝗵𝗶𝗰𝗵 𝘄𝗮𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗿𝘂𝗹𝗲 𝘀𝗲𝘁 𝗺𝗼𝘃𝗶𝗻𝗴? A regulatory moat evaporates if the regulation simplifies. Underwrite the direction of travel, not just the current state.

𝗔𝗻𝗱 𝘁𝗵𝗲 𝗰𝗹𝗼𝗰𝗸 𝗶𝘀 𝘁𝗶𝗴𝗵𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲. Retention in enterprise SaaS has largely been defined by the pain of systems replacement, not genuine moat. If the stickiness isn't backed by proprietary data, a harvesting flywheel, or regulatory surface area, those vendors are about to get disrupted. Pure seat-based pricing is dying unless vendors embrace agent-seat models, and LLM providers have been subsidizing the market on token cost, with recent pricing shifts signaling cash reserves aren't infinite.

𝗛𝗲𝗿𝗲'𝘀 𝘁𝗵𝗲 𝘂𝗻𝗱𝗲𝗿𝗮𝗽𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗲𝗱 𝗽𝗼𝗶𝗻𝘁: 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘄𝗼𝗿𝘀𝗲 𝗴𝗿𝗼𝘀𝘀 𝗺𝗮𝗿𝗴𝗶𝗻𝘀 𝘁𝗵𝗮𝗻 𝗦𝗮𝗮𝗦 𝗶𝗻𝗰𝘂𝗺𝗯𝗲𝗻𝘁𝘀, 𝗻𝗼𝘁 𝗯𝗲𝘁𝘁𝗲𝗿. Inference costs haven't collapsed, and burning VC cash to subsidize unit economics is a bridge, not a business model. The incumbents should be winning on P&L. They're losing on product velocity and AI-readiness. That's a solvable problem if the board has the will to ship. Vendors without a second business, without a data moat, and without regulatory insulation will still lose, despite having better margins than their AI-native challengers. Customers switch on features and speed, not on unit economics.

𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗿𝘁𝗶𝗰𝗮𝗹𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝗹𝗮𝘀𝘁 𝘀𝗮𝗳𝗲 𝗵𝗮𝗿𝗯𝗼𝗿, 𝗮𝗻𝗱 𝗼𝗻𝗹𝘆 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝗱𝗮𝘁𝗮 𝗯𝗿𝗲𝗮𝗱𝘁𝗵 𝗮𝗻𝗱 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲. Everywhere else, the premium is about to get competed away. Any fund underwriting vertical SaaS exposure right now should be asking the second-business question before the next check clears. DM me, email me brad@crossoverresearch.com, or let's chat about your portfolio/underwriting process (book.crossoverresearch.com).

Crossoverresearch.com

19 May 2024

$PLTR | Palantir

> Sentiment remains universally upbeat (consistent with read inflection in early January) as AIP traction fuels commercial segment outperformance ( 68% y/y in 1Q24 ex-SPAC revenue).

> The company continues to lean heavily into AIP bootcamps as a GTM strategy (hosted 660 in 1Q alone) and recent results are a testament of the effectiveness of this strategy: US customer deal growth 94% y/y (136 deals closed vs. 70 in 1Q23), bookings at 1.9x of sales ( 131% y/y), customer count 69% y/y.

> While it’s still too early to extrapolate initial bootcamp conversion metrics for bookings and revenue, the initial success is convincing. The AIP customer feedback we’ve picked up in our own checks supports view that bookings momentum can be sustained in the near-term.

> Partners on our checks have reported an overwhelming pace of YTD business with most seeing activity that is pacing significantly above (2x ) available capacity as well as internal growth targets.

> Palantir is in the early stages of building its channel program. The solution is an attractive GSI solution and can trigger a rich set of integration and customization services. As PLTR rolls out across GSIs, it should help to sustain the company's 20% growth targets.

> We had previously highlighted some concerns that PLTR's opportunity was limited to G2K firms with outsized analytics budgets and those who prefer to build on top of Databricks's open platform. We have since learned that PLTR’s data abstraction and ontology model, which is considered a critical component, creates a compelling competitive moat vs. SNOW and Databricks.

My thoughts... While valuation concerns cannot be written off at these levels, underlying business trends look healthy enough to support the premium multiple. Commercial momentum seems unlikely to slow given the success of PLTR’s AIP bootcamp GTM approach (mgmt. guided to 40% growth in 2024, pointing to 560 bootcamps completed across 465 orgs) and our internal checks suggest existing customer growth is on the horizon (in our 1/8 survey, >70% of PLTR customers suggested that AI-related initiatives would have a significant impact on PLTR spend by 2H’24). The government segment remains challenged and a wildcard to monitor, but mgmt’s guide to a 2024 reacceleration can be considered a positive.

Customer feedback on AIP Bootcamps...

The concept and framework of it seems like a really strong approach to me, not just for AI-based applications but honestly the intensive boot camp method seems like a good approach for a number of other use cases as well. This intensive approach aligns better with more Agile development methods where a boot camp approach, coupled with another week or so of follow up effort, might actually result in delivery within a very short period of time (even if limited in scope) which might help build more momentum and get a lot more hours of focus driving value than picking away at something over a more extended engagement. - Chief Data Officer at Government Agency

We have participated in AIP bootcamps; they are a good approach to bring a team together to test an idea. The bootcamps are well organized with the Palantir team available to support and enable the team to develop a solution. - Director of Data Engineering at National Health Provider

64

210

1,633

821,295

Apr 13

$AAOI Up 1000% since I initially wrote the thesis about the dislocation with underlying fundamentals. AAOI is now an optical networking force boasting a $11B market cap.

The Thesis vs. Reality.

800G/1.6T transceiver demand

Thesis: Flagged the overlapping cycles causing undersupply.

Reality: AAOI just received a $200M hyperscaler order for 1.6T transceivers and a customer more than doubled their 800G backlog from $53M to $124M in a matter of weeks.

Hyperscaler contracts

Thesis: Highlighted the $300M Microsoft deal and potential Meta engagement.

Reality: Major business acceleration with both Oracle and Microsoft into 2026.

Revenue projections

Thesis: Projected potential revenue exceeding $500M by 2025 from 800G alone.

Reality: Actual 2025 revenue came in at $455.7M across all segments, and management is now guiding for $1 billion in 2026 - a doubling of the business in a single year.

Vendor consolidation

The shrinking vendor count has played out exactly as predicted --> remaining players like AAOI are capturing outsized share as AI data center buildout accelerates.

--

While my focus has largely been on private markets over the last year , I've been heads down building out what will be the most sophisticated research intelligence engine for institutional investors. More to come by EOM.

6 Jun 2024

I am subscribed to @BLyons151 newsletter, and it is worth the suscribe and read. Here is one of the stocks that I picked up from his analysis and article. I started buying $AAOI here is the breakdown i came up with the newsletter . $AAOI is highlighted as an overlooked small-cap AI play with potential for a significant business turnaround. Key points include:

Optical Transceivers: AAOI is a leading player in the optical transceiver market, with a strong position in the current 400G, 800G, and 1.6TB optical transceiver cycles. The demand for faster networks driven by AI is expected to benefit AAOI significantly.

Market Dynamics: There's a consolidation in the number of vendors, increasing the likelihood that all remaining players, including AAOI, will benefit from the rising demand. The AI surge is causing overlapping cycles of transceiver demand, leading to potential undersupply and strong pricing.

Major Contracts: AAOI's $300 million deal with Microsoft and expected orders from other hyperscalers (potentially Meta) underline its growth prospects. The company aims for significant revenue from 800G products starting in the second half of 2024.

Positive Outlook: Management has provided optimistic guidance for the latter half of the year, with expectations of substantial customer engagement and revenue contributions.

Financial Projections: Analysts predict AAOI could capture a notable market share, with potential revenue exceeding $500 million by 2025 from 800G products alone.

Cable TV Business: Despite being a smaller part of the business, the cable TV segment shows strength, particularly with the transition to DOCSIS 4.0 technology, which could add positively to AAOI's overall performance.

Here is my chart based on it. I have been buying and holding for a few years.

2

17

6,491

Mar 6

No surprise. Infrastructure isn't cheap and available cash is finite. Once AI streamlines operations, labor becomes the easiest lever to pull. Public companies will have no choice but to pursue mass layoffs to fund the infrastructure required to stay competitive. This is just the beginning.

Mar 5

*ORACLE PLANS THOUSANDS OF JOB CUTS AS DATA CENTER COSTS RISE

*ORACLE SAID TO PLAN REDUCTIONS ACROSS THE COMPANY

1

2

14

4,331

Feb 27

Including the full August 2025 tweet that I never posted below.

TLDR: I argued that the AI boom was structurally unsustainable: too much capital, too many undifferentiated “wrappers,” and foundation models burning billions to subsidize usage. Since then, the bubble has inflated even further - AI firms pulled in the majority of global VC in 2025, while leaders like OpenAI blew past a $10–12B revenue run-rate and still lost staggering amounts of money. Yet instead of a disciplined reset, investors have largely doubled down: late‑stage checks are still flowing into capital‑intensive platforms, mediocre app‑layer companies are limping through down‑rounds, and only a thin slice of obviously broken wrappers is being culled. The early shakeout is real, but the capital allocation remains sloppy - far more driven by FOMO around a few brand‑name winners than by rigorous views on unit economics or durable moats.

The AI Investment Supercycle Hypothesis - Mon, Aug 11, 2025

Hypothesis: The current boom in AI startups and funding is unsustainable. It will likely culminate in a severe capital crunch and mass consolidation or failure of AI companies, especially affecting growth-stage investors. Below we break down the thesis with supporting data and consider counterarguments.

Excess Company Count vs. Finite Market

Explosion of AI Startups: There are tens of thousands of AI-focused companies worldwide (~70,000 AI startups globally). Many of these are “AI-enabled” software vendors whose products often rely on the same handful of AI models (e.g. OpenAI’s GPT). This surge echoes the dot-com era: “AI-powered is the new .com,” with countless lookalike startups pitching similar ideas.

Limited Revenue Pool: The total AI hardware/software market is projected at $780–$990 billion by 2027. Yet venture capital and corporate investors have already poured well over $500–600 billion into AI companies to date . To justify these investments with typical 10× returns, AI startups would need to generate on the order of $5–6 trillion in revenue – about 6× the entire expected market size. In other words, the math doesn’t add up: there simply isn’t a large enough revenue pie for all these companies at their current lofty valuations. As Sequoia Capital’s David Cahn noted, the gap between AI investment and revenue has ballooned into a “staggering $500 billion annual revenue gap” that must be filled to justify the spending .

Sky-High Valuations Assume Unprecedented Growth: Despite the limited market, funding has surged. Generative AI startups raised a record $56 billion from VCs in 2024 (885 deals) – nearly double the prior year . Close to one-third of all VC funding worldwide went to AI in 2024 . These financings often came at inflated valuations (hundreds of millions or even billions), implying future dominance in their niches. Yet many have little proven revenue. An analysis in mid-2025 observed that “90% of these ‘AI companies’ are just expensive wrappers around the same five foundational models.” In short, too many startups are chasing the same customers with undifferentiated tech, all while assuming they’ll each capture outsized revenue. This is structurally reminiscent of past bubbles.

Economics Inverted by Subsidies

Foundation Models Operating at Massive Loss: The core AI platforms (OpenAI, Anthropic, etc.) heavily subsidize AI compute costs to drive adoption. OpenAI, for example, generated about $4 billion revenue in 2024 but spent ~$9 billion to do so – losing around $5 billion for the year. By one estimate OpenAI currently “spends $2.25 for every $1 it earns”. Similarly, Anthropic burned $5.6 billion in cash in 2024 while making well under $1 billion revenue . (Anthropic projects improving in 2025, but still expects to lose ~$3 billion on ~$3.7 billion revenue.) These eye-popping losses mean AI API prices are artificially low – essentially subsidized by investors. The big model providers are keeping prices down to grab market share, even as they incur billions in operating losses.

Downstream “Wrappers” with No Moat: An estimated 30,000 software companies are “AI wrappers” that simply call these foundation-model APIs and repackage the output with a pretty interface . Because they all rely on the same underlying AI engines, their products are often interchangeable – “no IP, no moat… just a well-structured API call, some markup, and marketing.” Many charge high subscription fees (say, $50–100/month) for services that a savvy user could replicate with direct API calls for a few dollars . This works only as long as OpenAI/Anthropic keep API costs low. When the subsidies inevitably end (i.e. prices normalize upward to cover real costs), these downstream startups’ economics collapse. Their entire model is built on thin margins. As one analysis put it, “every token sent through a wrapper – paid or not – earns OpenAI money… startups become unpaid distribution arms, subsidizing OpenAI’s growth while bleeding out.” In other words, the house (OpenAI) always wins – until the “wrappers” run out of cash. At that point, thousands of these dependent products will either have to raise prices (driving away customers) or shut down.

The Commoditization Spiral: The combination of ubiquitous tech and underpriced service creates a vicious circle for most AI vendors: (1) If everyone uses the same few AI models, products become undifferentiated. (2) Competing on features is hard, so pricing wars ensue – indeed, OpenAI’s latest GPT-4 price cuts undercut Anthropic by up to 7× on cost per token, forcing others to match or lose business. (3) As prices per customer plummet, so do gross margins for any startup reselling AI. (4) Lower revenues make it impossible to support the previous valuations or to cover the still-high infrastructure costs (AI compute remains expensive, and energy/compute costs are not falling as fast as pricing). (5) With unit economics turned upside-down (more users actually increase losses), these companies cannot sustain operations without continual investor subsidies. This “race to the bottom” on price is great for end-users in the short term, but it’s lethal for the thousands of me-too vendors. It’s analogous to the dot-com era of free services: eventually the money runs out.

Growth-Stage Capital at Extreme Risk

Late-Stage Funding Frenzy: Unlike early-stage VCs who place many small bets, growth equity investors have been writing big checks (often $25–100 million each) into mid-stage AI companies at $400 million valuations. These rounds (Series B, C, D etc.) were justified by lofty growth assumptions and the fear of missing the “next big thing.” However, many of these startups have 8–12 month runways due to high burn rates (expensive ML talent and cloud bills) – meaning they will need another funding round by 2024–2025. For example, in 2023–24 numerous generative AI startups raised funds at unicorn valuations despite minimal revenue, and immediately ramped spending on AI infrastructure. “Most companies funded during the 2021–2023 boom had 18–36 months of capital,” and many will run dry by late 2025 or early 2026 if they can’t refinance . The growth investors who led these big rounds will be left holding the bag if valuations reset.

High Failure Rates = High Write-Downs: Early-stage venture firms expect e.g. 6 or 7 out of 10 startups to fail – their model tolerates it. Growth equity, in contrast, bets on a much lower loss rate (maybe 1 or 2 failures out of 10) because they deploy larger sums per deal. The current AI cycle is likely to betray those expectations. Industry observers predict over 90% of AI startups will fail within five years. Even before the recent frenzy, tech market indices showed sharp private valuation declines in 2022–23 , and many AI firms that raised in 2024 have since missed milestones. If 80–90% of funded AI companies ultimately go under, growth-stage funds with heavy AI exposure could see well over half their portfolio by value written off. In effect, billions in late-stage capital could evaporate. Estimates of the “dead money” vary, but even a conservative scenario of 60–70% startup failure would wipe out ~$400 billion (out of ~$600B invested), and a more realistic 80–90% failure rate implies $500B lost. Indeed, PitchBook data show fundraising for AI has already dropped in 2024 (deal count down 42%) as reality sets in . Growth investors are slamming on the brakes, but it may be too late – the capital is already in these companies, and many are running on fumes.

Compression of Exit Options: Another challenge for growth equity: who will buy or IPO these companies to provide an exit? The IPO window for tech is cautious in 2025, and the few public listings (e.g. Cloud, enterprise AI) have not delivered the kind of multiples needed. M&A is an option – and indeed we may see rapid consolidation in 2025–2027, with stronger players acquiring distressed startups for pennies on the dollar. But most acquirers will wait until valuations crumble. Funds that put $50M into a “next-generation AI SaaS” at a $500M valuation may recoup only a fraction in a fire sale. The timeline looks grim: 2025 will likely still see some aggressive fundraising and peak company counts, but by mid-2026 signs of saturation (slowing growth, rising customer-acquisition costs) will be undeniable. By 2027, as startups exhaust their last cash, we could witness a mass shutdown wave – potentially thousands of AI companies closing within 12–18 months . Growth equity portfolios will be forced to mark down failing investments (60–90% losses in the worst cases). As one industry veteran wryly noted, “Funds with 40% of their book in AI might experience a 80% write-down in that slice – it’ll be historic.”

Timeline: From Bubble to Shakeout

2021–2023 – Build-Up: Breakthroughs in generative AI (GPT-3, DALL-E, etc.) trigger a flood of startup creation and funding. Valuations skyrocket on hype. Investors cite “AI is the new electricity,” and fear of missing out leads to overfunding of very early-stage projects . Many companies launch with little more than a demo or a fine-tuned model wrapper.

2024 – Peak Froth: Funding reaches record levels (as noted, $56B VC dollars into genAI in 2024 ). By late 2024 and early 2025, AI headlines dominate tech. But underneath, cracks appear: infrastructure bottlenecks (GPUs), first reports of AI startups with negligible traction, and Big Tech (OpenAI, Microsoft, Google) racing ahead of the pack. The largest AI firms themselves remain unprofitable despite fast-growing revenue – e.g. OpenAI doubled its ARR from $6B to $12B in the first half of 2025 (annualized run-rate), yet it continues to burn cash ($14B loss expected in 2025). This suggests even market leaders haven’t found efficient economics yet.

2025 – Early Signs of Saturation: By mid-2025, the number of AI products on the market has exploded. Every sub-sector (coding assistants, AI content generators, chatbots for support, etc.) is crowded. Customer adoption, while real, cannot keep up with the supply of solutions. Anecdotally, sales cycles for B2B AI software start to lengthen as CIOs get fatigued by thousands of similar pitches. Customer acquisition cost (CAC) rises – more effort needed to convince users who have already tried 5 different AI copywriters or coding copilots. Big Tech enters aggressively, bundling AI features into their platforms (often free or at low cost), undercutting standalone startups. Investors grow more selective, favoring startups with real differentiation or proprietary tech.

Late 2025 to 2026 – The Crunch: This is when the “gravity” of finite capital hits. Many startups that raised in the 2021–22 boom face end of runway by late 2025 . Unfortunately, the funding environment now is much tougher – interest rates are higher, and LPs (the investors in VC/Growth funds) are nervous about overexposure to AI. We can expect a sharp pullback in new funding for all but the top 5% of AI companies. The rest must either find an acquirer or drastically cut costs to survive. In mid-2026, we’ll likely see a wave of down-rounds (companies raising capital at much lower valuations) and outright failures. Investor sentiment flips from FOMO to caution: as one VC noted, “there’s far more scrutiny on unit economics and revenue traction” now . The mere mention of “AI” no longer secures a premium – in fact, hype-y startups are viewed with skepticism unless they have solid metrics.

2027 – Mass Extinction Phase: By 2027, the global liquidity squeeze is in full effect. Earlier-stage VC funds may have the dry powder to prop up a few of their best bets, but growth equity and crossover investors (who fueled the largest rounds) largely retreat, nursing losses. Without new funding, thousands of AI startups will fold in a short period – the “bursting of the AI bubble.” This is analogous to the dot-com crash circa 2000–2001, when countless internet startups went under. The survivors likely fall into two camps: (a)Infrastructure-level players (the big foundation model providers or cloud platforms – many of whom are incumbent tech giants or heavily funded leaders like OpenAI), and (b)a handful of startups with truly defensible, domain-specific AI solutions (e.g. a company with a unique dataset or enterprise integration that gives it an edge in a niche). These survivors might consolidate the market – mergers and acquisitions spike as the stronger firms acquire IP/talent from failed ones for pennies.