Trading & Investing. Building @RR2Capital with over 220 early stage investments. Join my 39,000 traders community at discord.gg/rand

Joined May 2017

- Tweets 107,083

- Following 1,248

- Followers 349,415

- Likes 587,657

28,918 Photos and videos

Pinned Tweet

13h

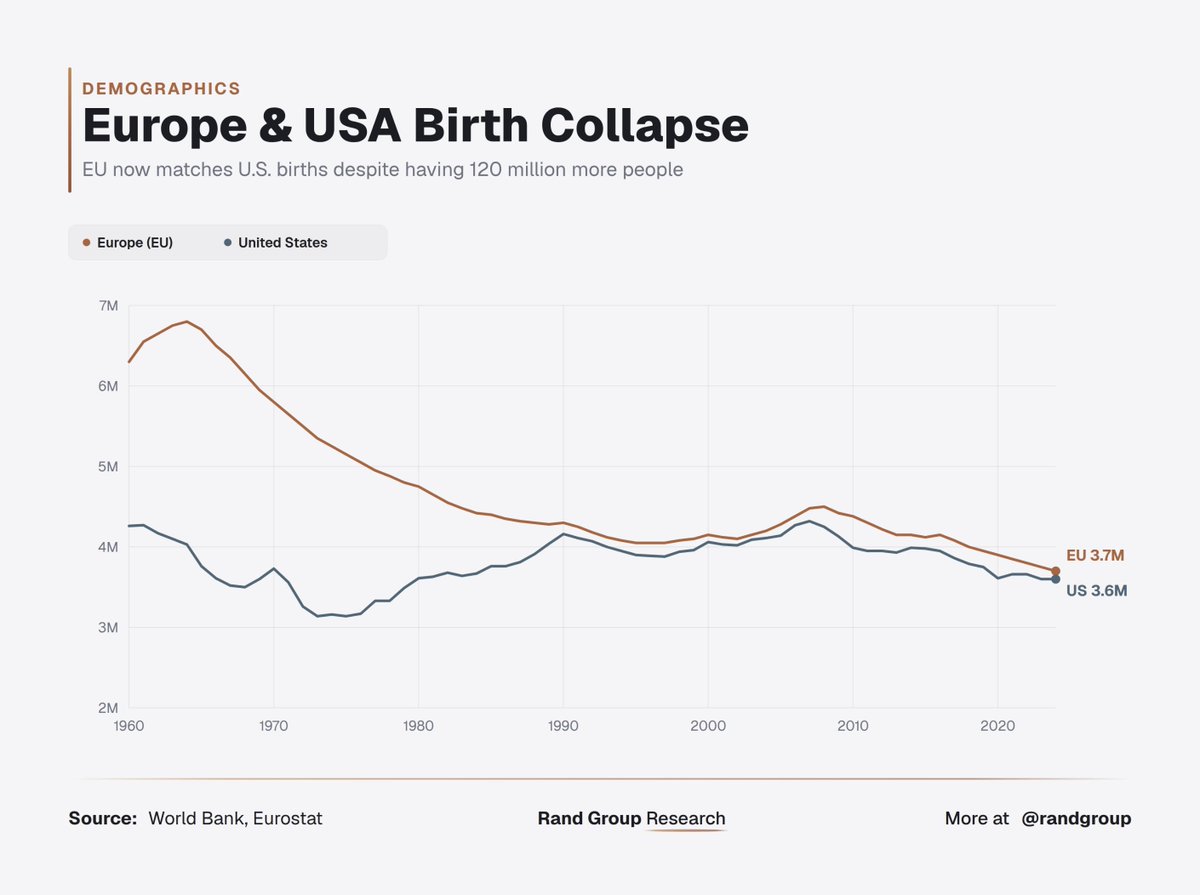

Europe and USA birth collapse:

🇺🇸 USA: 3.6M babies in 2024

🇪🇺 Europe: 3.7M babies in 2024

Who exactly is going to fund those pension systems in 2050?

11

22

158

18,325

Rand Group retweeted

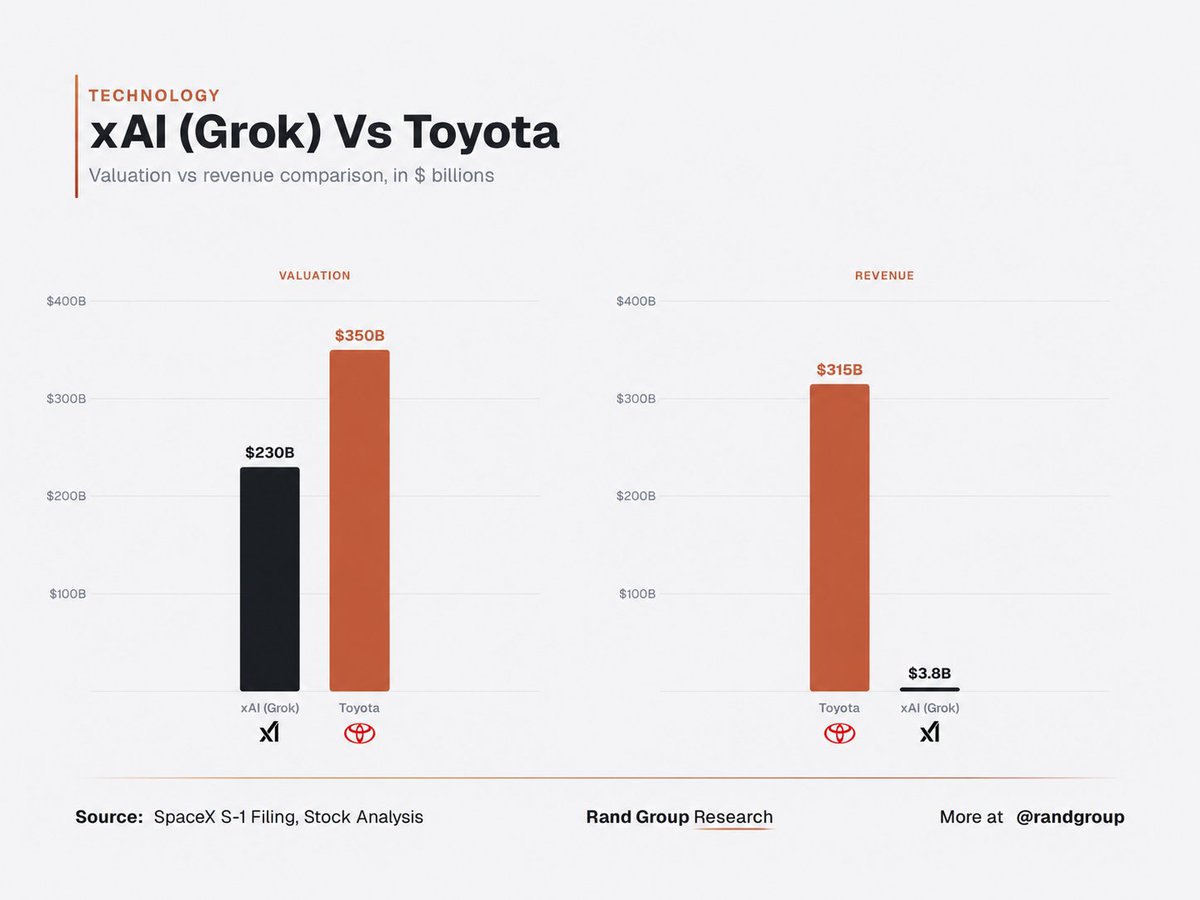

xAI is valued at $230B on $3.8B revenue.

Toyota is valued at $350B on $315B revenue.

If Toyota had xAI's multiple it would be worth a whooping $19 trillion.

6

18

138

16,509

Rand Group retweeted

13h

Europe and USA birth collapse:

🇺🇸 USA: 3.6M babies in 2024

🇪🇺 Europe: 3.7M babies in 2024

Who exactly is going to fund those pension systems in 2050?

11

22

158

18,325

Rand Group retweeted

11h

Things that didn't exist yet when the US last fully audited Fort Knox:

🔸 The internet

🔸 The space program

🔸 Color television

🔸 iPhones

The year was 1953. $662 billion in Gold. Trust us bro 👍

8

25

160

17,575

Rand Group retweeted

21h

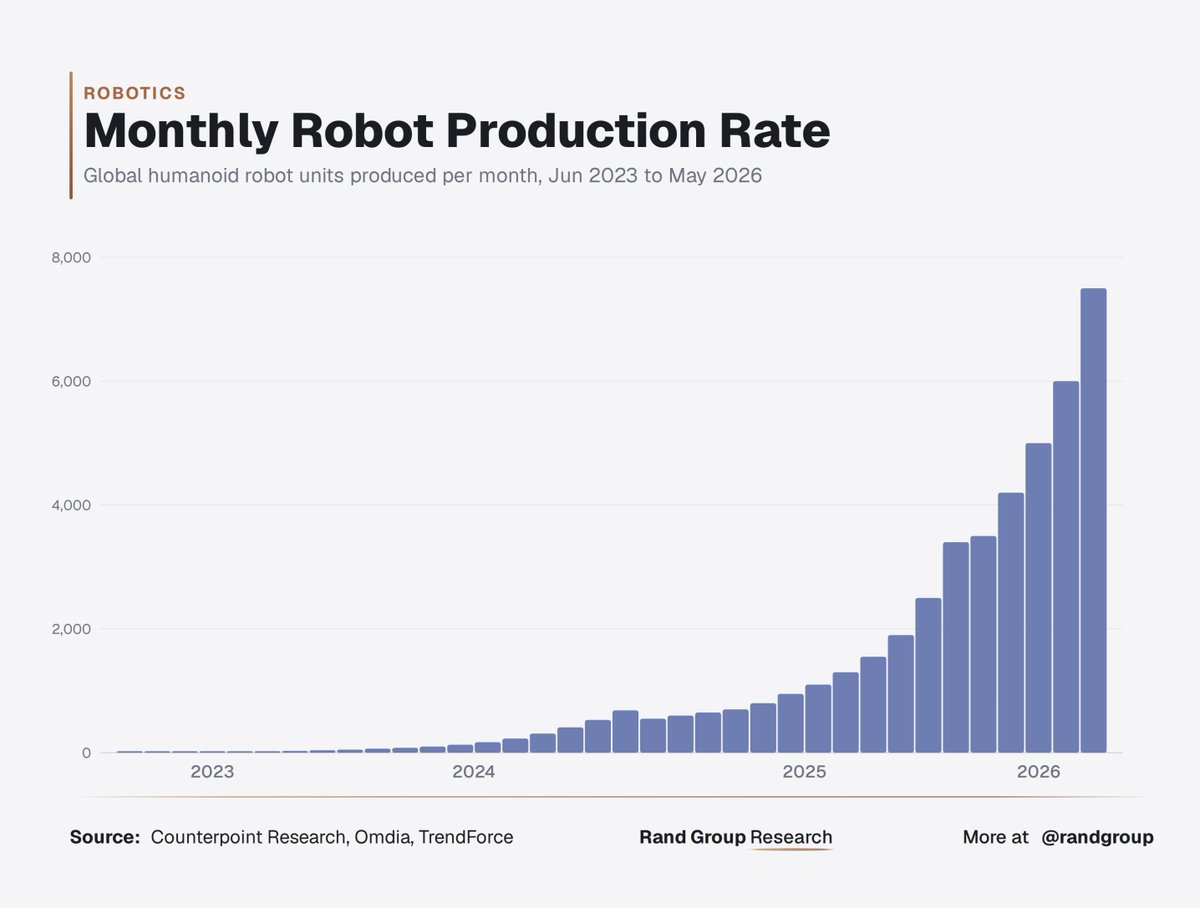

Just FYI, 🇨🇳 China shipped 90% of the world's humanoid robots last year.

19

39

203

23,966

Rand Group retweeted

May 8

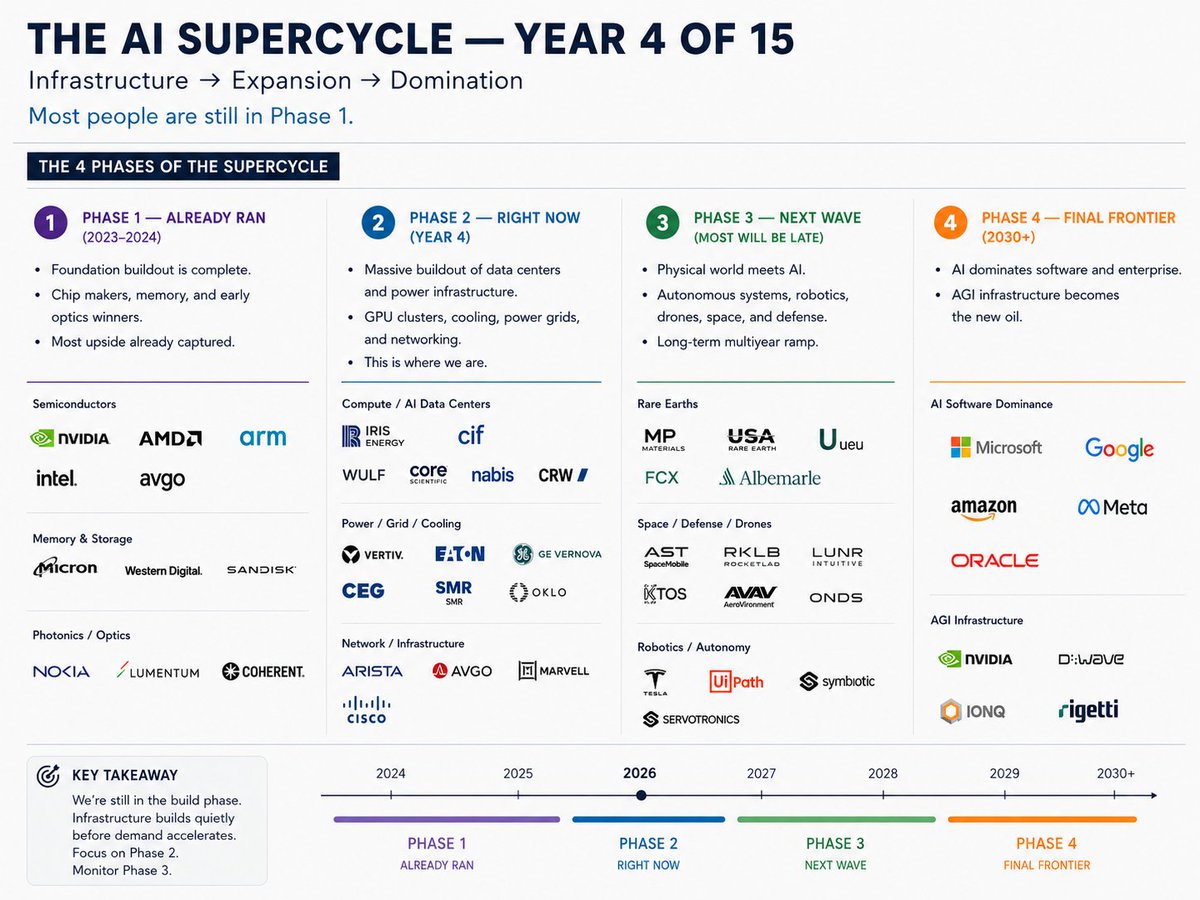

The AI supercycle will last 15 years. We're in year 3.

Most investors are still buying Phase 1 names while the real money is already rotating into Phase 3.

I mapped the entire cycle into 4 phases with the tickers that matter at each stage:

The AI supercycle is the biggest investment theme of our generation. Bigger than mobile. Bigger than cloud. A 15 year structural shift that will reshape every sector of the global economy. Hyperscalers just committed $725 billion in capex for 2026, nearly doubling last year. Microsoft, Google, Amazon, and Meta each spending over $100 billion individually.

This is not speculation. I've mapped the entire supercycle into four phases so you know exactly where we are and where the asymmetric opportunities sit.

🔴 Phase 1: Already Ran (2023 to 2025)

The foundation layer is complete. $AMD ran 78% in 2025, $NVDA 39%, and $INTC just posted a blowout Q1 that sent the Philadelphia Semiconductor Index above 10,000 for the first time. Chips still power every phase but the generational entries are gone and risk/reward has compressed.

- $NVDA, $AMD, $ARM, $INTC, $AVGO, $MU, $GLW

- Semiconductors, Memory & Storage,Photonics/Optics

- Foundation complete. Still growing but priced for it.

🟠 Phase 2: Peak Buildout (2025 to 2027)

The phase most investors just woke up to. $CEG acquired Calpine to become the largest U.S. private power producer at 55 GW. $GEV up over 200% in a year. $VRT co engineering cooling for NVIDIA's Rubin architecture. $GLW up 74% YTD on optical fiber demand. Nuclear SMRs are the breakout with $OKLO, $SMR, and $BWXT positioning to power data centers directly. Still upside but the obvious names have moved.

- $CEG, $GEV, $VRT, $VST, $TLN, $ANET, $GLW, $MOD, $EQIX $OKLO, $SMR, $BWXT, $NNE

- Power/Grid, Cooling, Networking, Nuclear/SMR Peak buildout.

- Nuclear SMRs are the sleeper.

🟡 Phase 3: The Positioning Window (2026 to 2028)

Where AI escapes the data center and enters the physical world. Most will be late. Tesla converting Fremont to Optimus production, $25B capex, mass production targeted H2 2026. Rocket Lab posted record $602M revenue with $1.85B backlog. $LUNR up 47% YTD with $943M in contracts. $KTOS Valkyrie drone selected for the Marine Corps. The window to position is open right now.

- $TSLA, $RKLB, $LUNR, $KTOS, $AVAV, $PATH, $ISRG $MP, $FCX, $ALB, $ASTS

- Robotics/Autonomy, Space/Defense/Drones, Rare Earths

- This is where the asymmetric risk/reward lives.

🟢 Phase 4: Final Frontier (2028 )

The endgame. Microsoft capex $190B. Alphabet $190B. Amazon $200B. Meta $145B. Google Cloud backlog past $460B. They're building the rails for AI software dominance and AGI. Quantum still early but $IONQ and D Wave are laying groundwork. The platforms that control the software layer win the entire supercycle.

- $MSFT, $GOOGL, $AMZN, $META, $ORCL, $IONQ

- AI Software Dominance, AGI Infrastructure Decade long thesis.

- Accumulate on weakness.

💊 Key Takeaway

- Phase 2 is confirmed ($725B hyperscaler capex)

- Phase 3 is where the smart money positions nowRobotics, space, defense, nuclear

- SMR are the 2026 to 2028 trades

- Most will rotate into these names 12 months too late

15 year supercycle. Not a trade. Phase 1 ran. Phase 2 is priced. Phase 3 is where you want to be.

171

812

3,944

770,486

15h

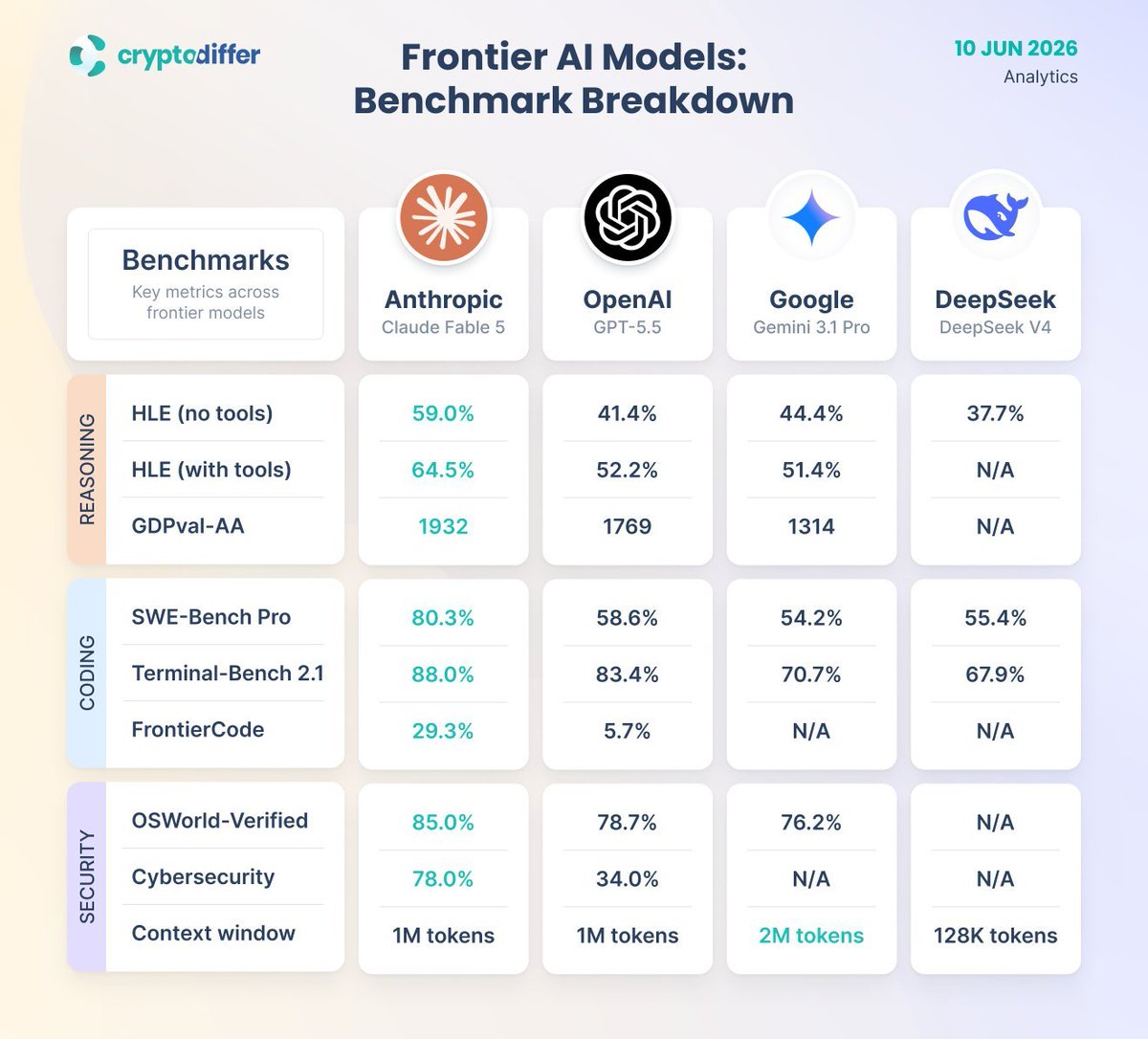

DeepSeek V4 left five out of nine benchmarks blank and still has the fastest-growing API user base on earth. Are we sure benchmarks are what wins this race?

10

18

158

15,960

17h

32.6% of all $ETH is staked. In 2021 it was under 5%. The price fell 60% and the staking ratio accelerated... reasons?

20

17

153

18,340

19h

BEFORE AI

Idea: 🙋♂️🙋♂️🙋♂️

Execute: 👨💻👨💻👨💻👨💻👨💻👨💻👨💻👨💻

AFTER AI

Idea: 🙋♂️🙋♂️🙋♂️🙋♂️🙋♂️🙋♂️🙋♂️🙋♂️🙋♂️

Execute: 👨💻👨💻👨💻

6

12

134

16,750

Rand Group retweeted

Jun 12

$SPCX is now worth more than:

🇨🇦 Canada

🇧🇷 Brazil

🇰🇷 South Korea

19

49

280

41,773

Jun 13

England fans went from zero beers allowed in Qatar to $18 beers in Florida.

6

11

134

16,492