Joined June 2017

- Tweets 1,623

- Following 488

- Followers 137

- Likes 490

167 Photos and videos

Jun 11

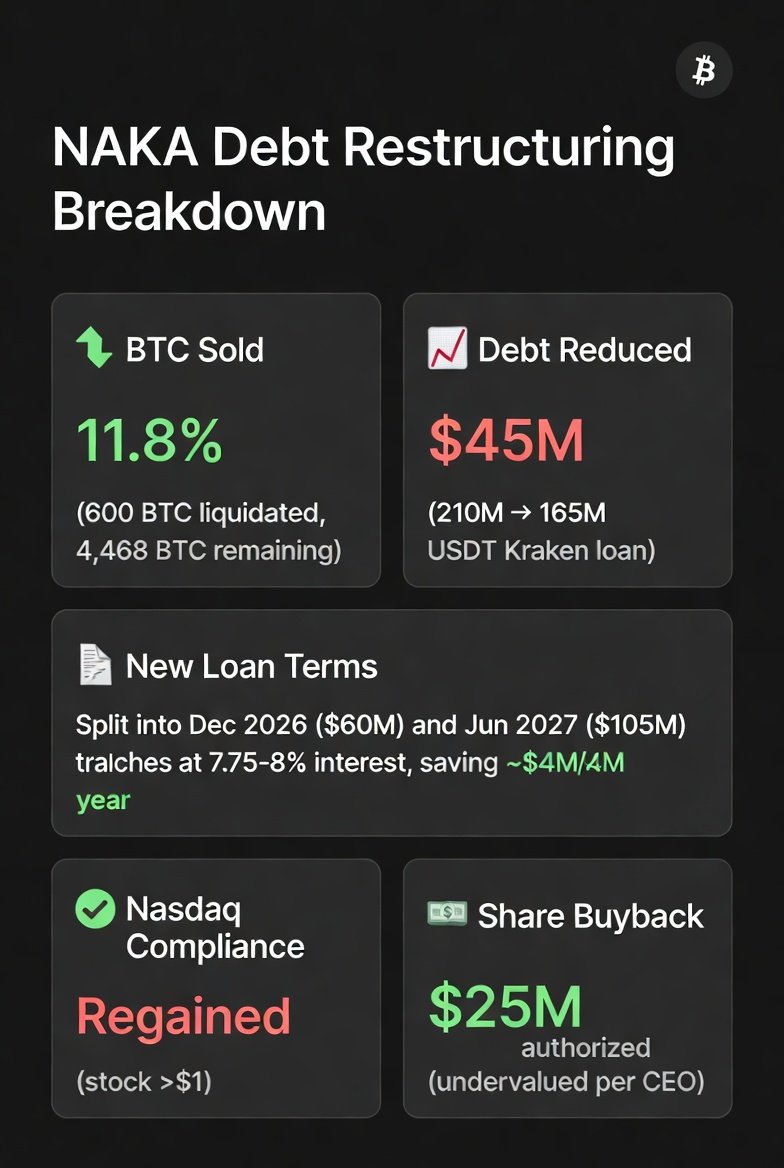

Why did @nakamoto sell ~600 BTC?

To restructure its Kraken loan on better terms, lower its interest rate, regain Nasdaq compliance, and authorize a $25M share buyback.

34

Jun 10

XUSD is coming for you @XMoney

Jun 2

Introducing MGUSD.

MoneyGram's native U.S. dollar stablecoin.

Natively issued on @StellarOrg.

Built with @Stablecoin, @M0 and @FireblocksHQ.

Live in the U.S. today.

2

77

Jun 9

Inside the CLARITY Act: 10 Reasons Banks Are Terrified

1. Stablecoin Yield & Deposit Flight

The Provision: The bill allows stablecoin issuers to offer "activity-based rewards" to retail users holding digital dollars.

The Threat: Instead of keeping cash in a traditional checking account earning 0.01%, users can hold compliant stablecoins and earn a 3.5% retail baseline yield. This could trigger a massive flight of retail deposits away from commercial banks, stripping them of the cheap capital they use to fund high-interest loans.

2. Access to the Federal Reserve

The Provision: The bill allows state-chartered trust companies the entities that manage stablecoins and crypto custody to apply for and access the Federal Reserve’s payment and operational infrastructure.

The Threat: Crypto companies will no longer have to rely on giant commercial banks like JPMorgan Chase or Citigroup to settle large transactions or clear funds. It ends the traditional banking cartel's exclusive monopoly over central bank liquidity.

3. Alternative Trading Systems (ATS)

The Provision: The bill formally legalizes and regulates Alternative Trading Systems (ATS) to clear and settle spot trades for digital commodities.

The Threat: Wall Street banks make enormous profits serving as intermediaries and clearing houses for major asset markets. This provision allows digital native platforms to handle execution and settlement internally, cutting traditional prime brokers completely out of the fee structure.

4. Independent Payment Rails

The Provision: The bill legally recognizes "payment stablecoins" as valid instruments for daily commercial transactions.

The Threat: If retail merchants can accept stablecoins directly via fast public blockchains with sub-cent transaction costs, they can bypass credit and debit card processors entirely. This threatens the tens of billions of dollars banks collect annually from 2% to 3% merchant swipe fees (interchange).

5. The Decentralized Governance Safe Harbor

The Provision: The bill establishes that non-custodial, decentralized software developers and open-source protocols are not financial intermediaries and cannot be regulated as traditional money transmitters.

The Threat: Traditional banks face steep regulatory barriers that keep startups from competing with them. By protecting decentralized finance (DeFi) protocols from these heavy compliance overheads, the bill allows software-based lending and borrowing systems to legally exist and directly undercut legacy bank loan desks.

6. Mandatory Asset Segregation

The Provision: The legislation mandates strict, 1:1 asset segregation for digital commodity brokers, legally defining user crypto as "customer property" that must be kept separate from corporate funds.

The Threat: Commercial banks routinely pool customer deposits together and lend them out to generate corporate profit (rehypothecation). This provision completely outlaws fractional-reserve practices for digital commodities, turning custody into a strict storage service rather than a capital-churning lending engine.

7. The Shift to CFTC Jurisdiction

The Provision: The bill places the oversight of digital commodity spot markets exclusively under the Commodity Futures Trading Commission (CFTC) rather than the SEC.

The Threat: Wall Street giants have spent decades and billions of dollars building legal teams perfectly optimized for complex SEC securities frameworks. Shifting the jurisdiction to the CFTC creates an environment where crypto-native firms hold a massive structural advantage, leaving legacy banks behind while they retool their compliance systems.

8. Capital Requirement Parity

The Provision: The bill sets up a customized, risk-appropriate capital framework specifically designed for digital commodity dealers operating under the CFTC.

The Threat: Under global Basel III banking rules, traditional banks face a punitive 1,250% risk weight on crypto assets, meaning they must hold dollar-for-dollar cash reserves against any crypto on their balance sheets. The bill enables digital-native competitors to manage digital assets with far greater capital efficiency than legacy institutions can legally achieve.

9. Restrictions on Proprietary Bank Ledgers

The Provision: While the bill permits national banks to engage in digital asset activities, it places strict portfolio margining and regulatory boundaries on their operations.

The Threat: Major banks want to capture the market by launching proprietary, closed-loop "tokenized deposit" networks. The bill's restrictions prevent banks from using their scale to monopolize digital ledgers, giving open, public blockchains room to dominate.

10. Protection of Self-Custody Rights

The Provision: The text explicitly prohibits any federal agency from outlawing or restricting an individual’s right to use a self-hosted wallet to maintain absolute control of their own private keys.

The Threat: Banks rely on keeping your wealth locked inside their institutional walls so they can monetize it via asset management fees. Legally protecting self-custody guarantees users a permanent structural exit hatch, allowing them to instantly withdraw capital from the traditional financial system if bank fees or terms become unfavorable.

1

5

183

Ripplobar retweeted

Jun 3

The actual doom loop you should be worried about with MSTR is not them selling BTC to fund the preferreds. That's a rounding error. The true doom loop is one they've talked about in their calls - selling bitcoin to fund equity repurchases in an accretive manner.

6

5

74

15,023

May 28

The Truth About Wall Street's $114 Trillion Blockchain Migration to Stellar

Ever wonder how the DTCC tokenizing $114 TRILLION in assets actually changes the game for Wall Street giants like Citadel or Jane Street?

It’s not about hype it’s a massive upgrade to the pipes of global finance. Here is what's really happening behind the scenes:

1. When you buy a stock today, you don't actually own it. A private entity named Cede & Company (part of the DTCC) holds the master title. You just own a claim.

2. Tokenizing assets on public blockchain does not change your existing claim. You still own a legal claim to your shares just like before, but it has simply been digitized. The tech is new, but the control is the same.

3. Right now, Market Makers leave billions of dollars sitting idle just to guarantee trades clear. With instant on-chain settlement, that money is freed up. They can deploy capital exactly when a trade happens, unlocking massive efficiency.

4. Moving real-world assets to digital ledgers creates price mismatches between old and new systems. High-frequency trading algorithms will instantly exploit these tiny gaps, creating a brand-new gold rush for automated arbitrage.

2

52

May 27

It was neither Ethereum nor Solana. Stellar was the chosen tokenization platform for stocks, ETFs, and bonds.

$xlm

2

79

May 27

The biggest winner of tokenization is Stellar.

May 27

Today, @The_DTCC's tokenization service announced plans to connect with @StellarOrg starting H1 2027.

This integration will allow market participants to leverage traditional assets in a digital ecosystem for faster settlement, greater asset mobility, extended trading hours, cost efficiency, and lowered risk.

The network was built for this moment.

Watch ↓

1

29

Ripplobar retweeted

May 16

13 days until the CME gap phenomenon is no longer possible. May 29th, CME starts 24/7/365 Bitcoin Futures trading.

Enjoy one last weekend manipulation CME gap.

1

4

34

1,745

May 14

The Clarity Act passes in 15-9 vote and the bill now goes to the Senate. The bill will become a law this year.

May 14

🚨JUST IN: The Clarity Act ADVANCES out of the Senate Banking Committee in a 15-9 bipartisan vote, with two Democrats voting in favor: @SenRubenGallego and @Sen_Alsobrooks.

Next stop: the full Senate.

90

May 1

The CLARITY Act is officially moving to a Senate Banking markup on May 13th.

Senator Tillis confirmed today that bank concerns are addressed and the yield compromise is finalized. The 10-week runway for US crypto rules just got a massive green light. 🇺🇸🏛️

1

91

Mar 20

This is the sign the crypto community has been waiting for. It looks like the senators might have reached a deal with the White House to resolve the stablecoin yield dispute with banks.

2

77

Mar 17

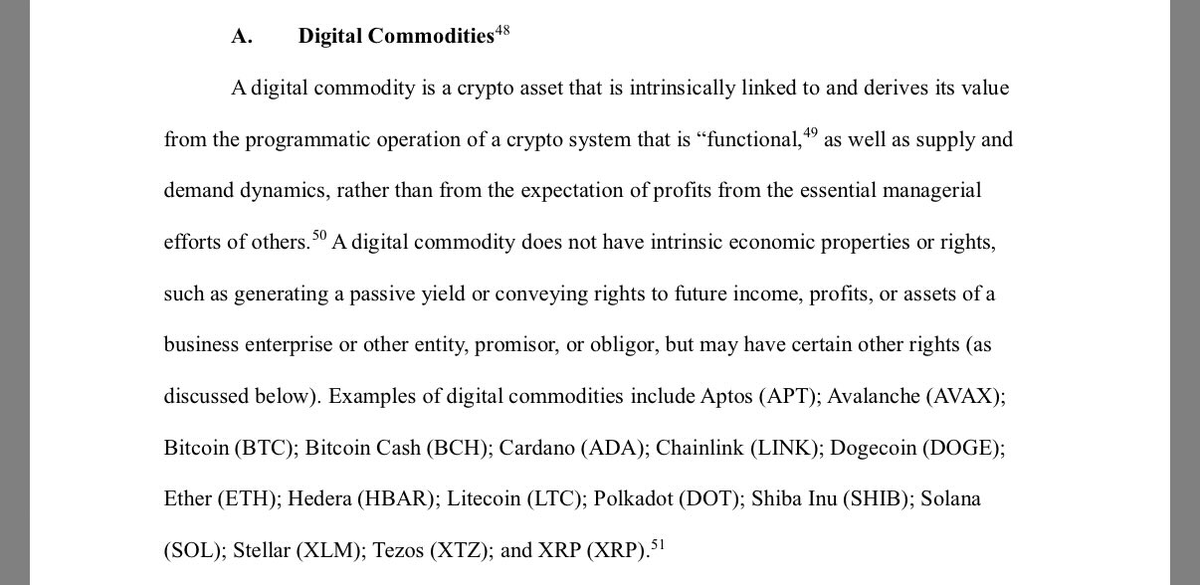

🚨 Crypto Is Now a "Commodity"🚨

The SEC just reclassified major digital assets as Digital Commodities. This unlocks the 60/40 Tax Rule, which drops your tax bill by nearly a third.

The 60/40 Rule Breakdown It doesn't matter if you held the asset for an hour or a year. Your profit is now split:

60% of profit is taxed at 20% Long-Term rate.

40% of profit is taxed at 37% Short-Term rate.

Your total tax rate is now 26.8% instead of 37%.

On a $100,000 profit:

OLD TAX: $37,000

NEW TAX: $26,000

You SAVE $10,200

The commodity label makes the U.S. the most profitable place to trade.

1

42

Mar 17

The SEC has classified the following crypto assets as commodities: $BTC, $BCH, $ADA, $LINK, $DOGE, $ETH, $HBAR, $LTC, $DOT, $SOL, $XLM, $XRP, $AVAX, and $APT. Exchange tokens will be classified as securities. 🚨

In addition to providing greater clarity regarding the Commission’s treatment of crypto assets, today's interpretation complements Congressional efforts to codify a comprehensive crypto market structure framework into statute.

More details below. 👇

2

202

Mar 14

And the silver medal in the "Still Waiting for My Lambo" Olympics goes to... XRP!

Mar 14

BREAKING: Ethereum is now projected to lose its spot as the second largest cryptocurrency.

57% chance Ethereum is flipped this year.

polymarket.com/event/eth-fli…

1

80

Mar 8

Why Banks Are Really Fighting Clarity Act

The big banks are trying to kill the Clarity Act. They say they are worried about people moving their money to apps like Coinbase to get 4% interest. They claim this will cause "bank runs" and hurt the economy.

But this doesn't make sense. Even without the new law, Coinbase can still pay you rewards. So why are the banks fighting so hard right now? It’s because the interest rate is just a smoke screen. The real war is about the payment rails.

The "Fee-Gate" Monopoly 🚧

Right now, every time you send money, it has to go through a bank. Banks make billions of dollars every year in "settlement fees" just for moving your dollars from Point A to Point B. They own the only payment rails.

The "Internal Settlement Rule" Threat ⚙️

The Clarity Act has a secret "Internal Settlement" rule. This rule would let companies like X, Circle, and Ripple move money on their own digital pipes (SOL, XRP, and XLM) without ever touching a traditional bank.

If this law passes:

• Money moves from person to person instantly.

• The bank doesn't get a fee.

• The bank doesn't even see the transaction data.

The banks aren't fighting to save your deposits. They are fighting to save their fees. They want to keep the "fee-gate" closed so they can keep charging you every time you move your own money.

If Clarity Act passes as currently written, it doesn't just "regulate" crypto—it ends the 100-year monopoly that banks have had over how dollars move.

1

4

362

Mar 3

X Money Is Changing Everything

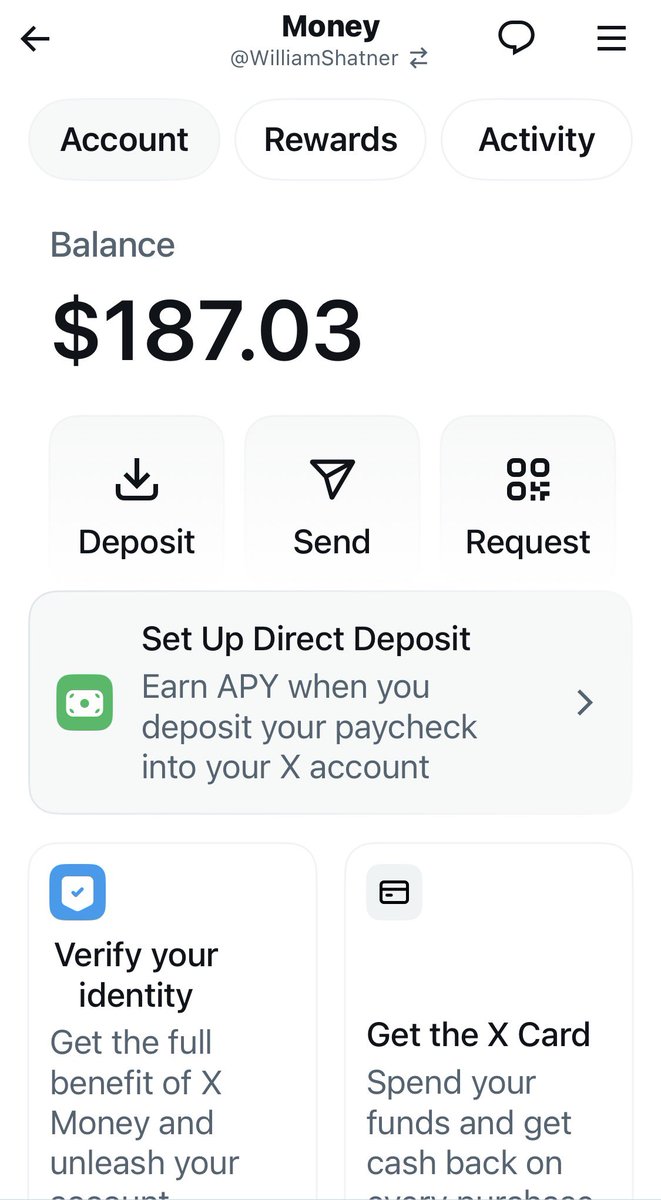

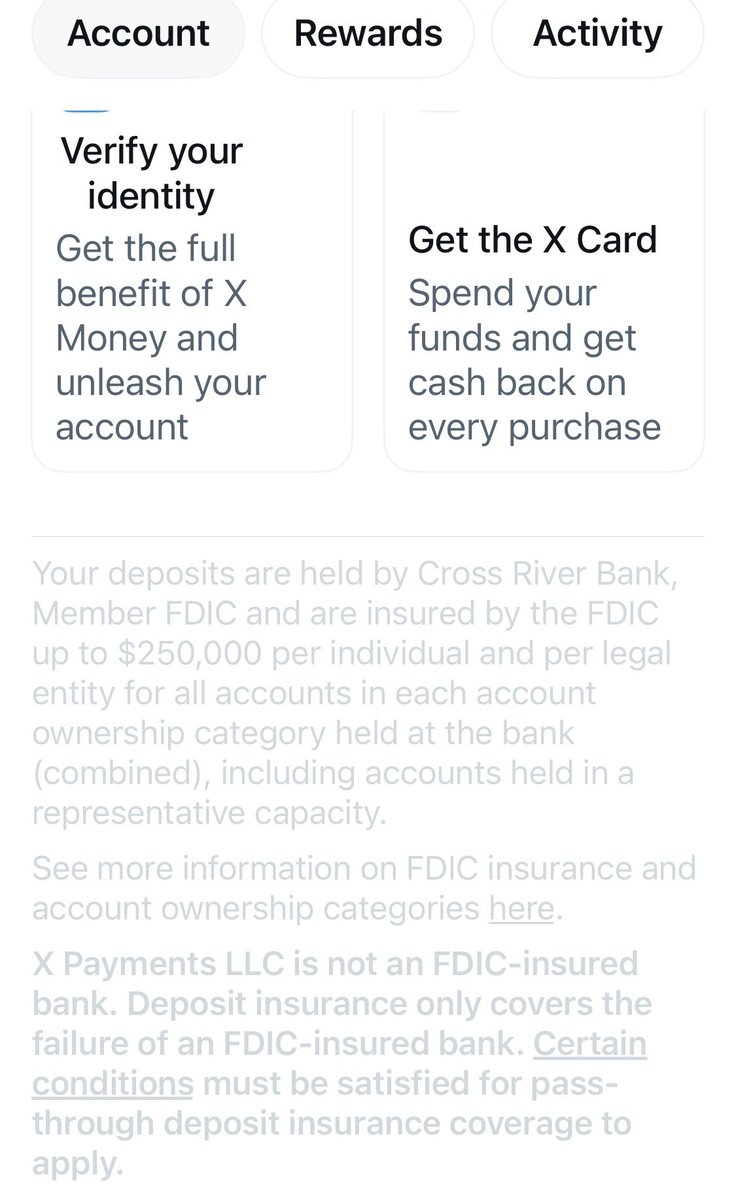

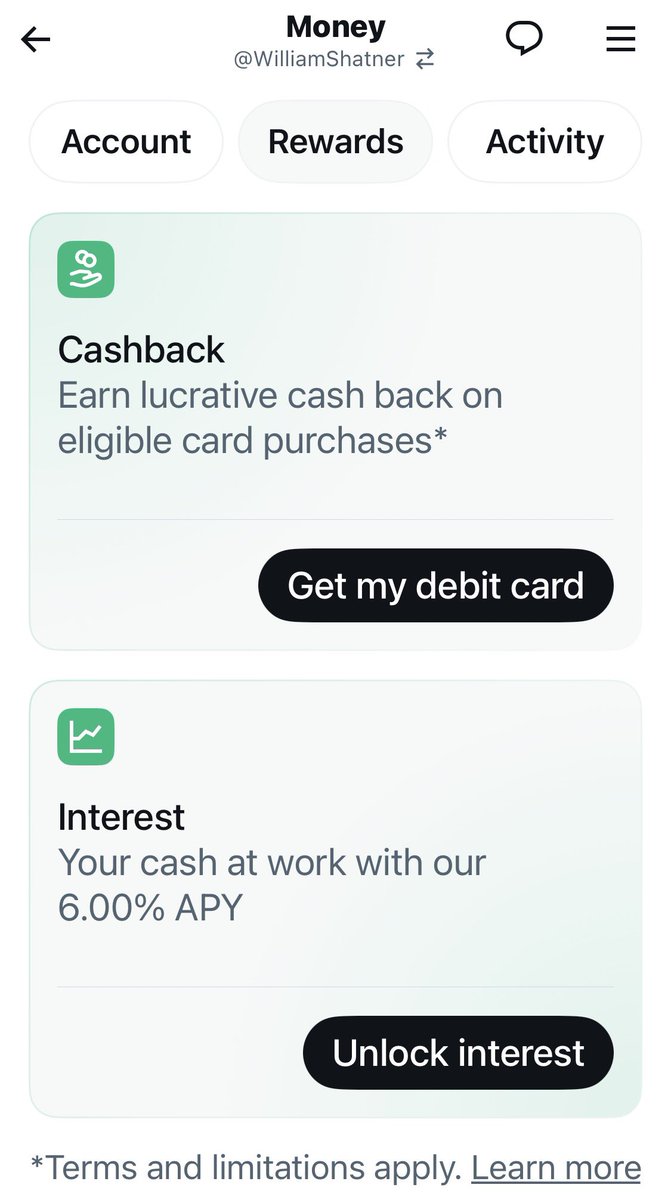

@elonmusk is turning X into a giant digital bank by partnering with Cross River Bank, a real, regulated institution. This means money on X can have FDIC insurance up to $250,000.

X uses this bank partner to navigate new regulations. While big banks try to stop crypto companies from paying interest, X Money calls its 6% interest a “bank reward,” allowing it to bypass rules that other crypto platforms face.

$USDC, the regulated “digital dollar” backed 1:1 by US Treasuries, is the primary asset moved between X users.

X relies on three blockchains to move money:

@solana ** $SOL - Cross River Bank is one of the first U.S. banks to use Solana, which settles payments for the X Card (Visa).

@Ripple ** $XRP - Cross River was an early Ripple partner. It uses Ripple’s technology for international transfers and serves as the bridge connecting the XRP network to traditional banking for many crypto companies.

@StellarOrg ** $XLM - Cross River acts as the money bridge, converting regular cash to digital dollars via the Stellar network. Stellar is the only payment-focused blockchain with a global physical cash network integrated with MoneyGram’s 500,000 locations across 180 countries, enabling anyone including the unbanked to convert USDC to local currency cash and back for a fraction of a cent.

Here’s a few more screenshots. There’s a debit card with cash back too! 😳😱

1

127

Feb 27

Revenge of the Utility Assets

🏆The Biggest Winner: Ripple and RLUSD

The Bank (RLUSD) - By securing the OCC National Trust Bank charter in December 2025, Ripple stepped inside the traditional banking perimeter. While the OCC is currently carpet-bombing unregulated shadow banks and tech companies with yield bans, Ripple is safely operating as a federally recognized institution. They are the compliant vendor that Wall Street is legally allowed to use.

At the same time, the advancing DCIA classifies XRP as a Digital Commodity. Since stablecoins are now legally barred from offering yield or speculative upside, institutional and retail capital seeking velocity and rewards must rotate into commodities.

Ripple can offer banks perfectly compliant 1:1 stablecoin (RLUSD) for safe holding, while offering the high-velocity, high-liquidity commodity (XRP) for actual cross-border bridging. They win on both sides of the new regulatory divide.

💀The Biggest Loser: Coinbase and The Legacy Crypto Exchange Model

The very regulations designed to protect community banks and the new tech features designed by Elon Musk are perfectly calibrated to destroy Coinbase's primary revenue engines.

Coinbase relies massively on its revenue-sharing agreement with Circle for USDC yield. In a high-interest-rate environment, that was a multi-billion-dollar golden goose. The OCC’s move to ban stablecoin rewards across "affiliated exchanges" directly targets and decapitates this revenue stream. Coinbase withdrew support for the Clarity Act precisely because they saw this coming—and the OCC did it anyway.

The government and legacy banks have successfully walled off the "Store of Value" (stablecoins/deposits). This forces all the market's energy into the "Velocity of Money" (trading and utility).

❌Stablecoins Yield in USA - OCC stablecoin rules

❌DeFi in USA - The Clarity Act's DeFi restrictions

❌ETH - Ethereum's entire value proposition over the last few years has been acting as the global settlement layer for DeFi and yield generation

❌SOL - Solana built the fastest, cheapest rail for USDC and PYUSD but the OCC just heavily restricted

The "Web3" Era (ETH, SOL, DeFi): Built on permissionless yield, unregulated smart contracts, and tech-branded stablecoins was pushed into the corner by the OCC and Congress

The "Global Ledger" Era (Ripple, XRP, XLM, X Money): Built on bank-chartered custody, KYC - compliant velocity, and legally defined Digital Commodities was green-lit by the government and adopted by Big Tech

Feb 26

🇺🇸 JUST IN: The US OCC proposed rules to restrict branded stablecoins and ban yield rewards.

116