Co-Fund Manager @ithoughtpms

Joined January 2019

- Tweets 263

- Following 355

- Followers 12,697

- Likes 10,936

92 Photos and videos

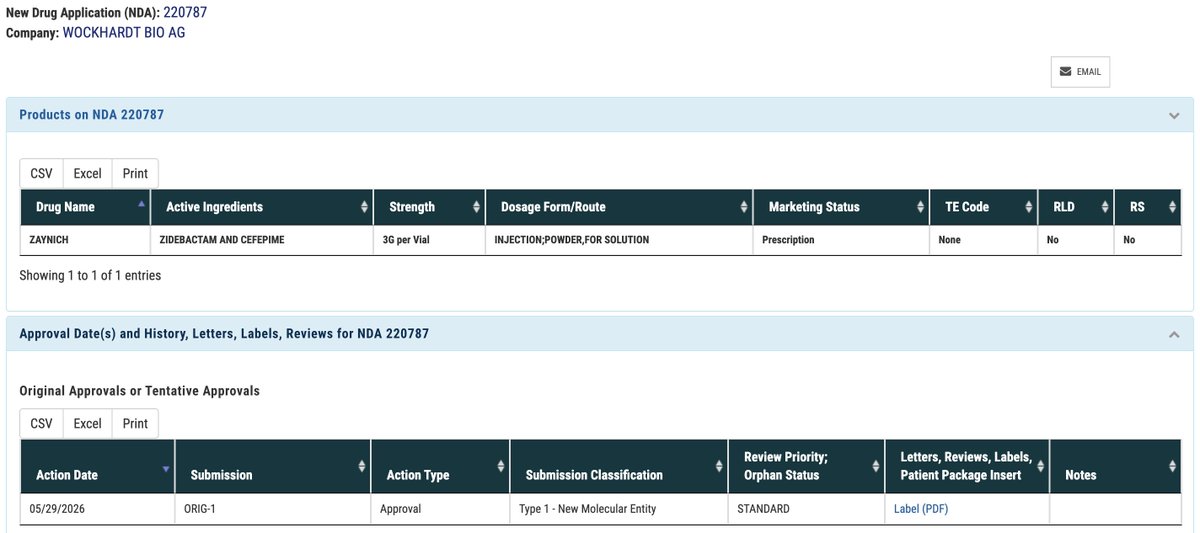

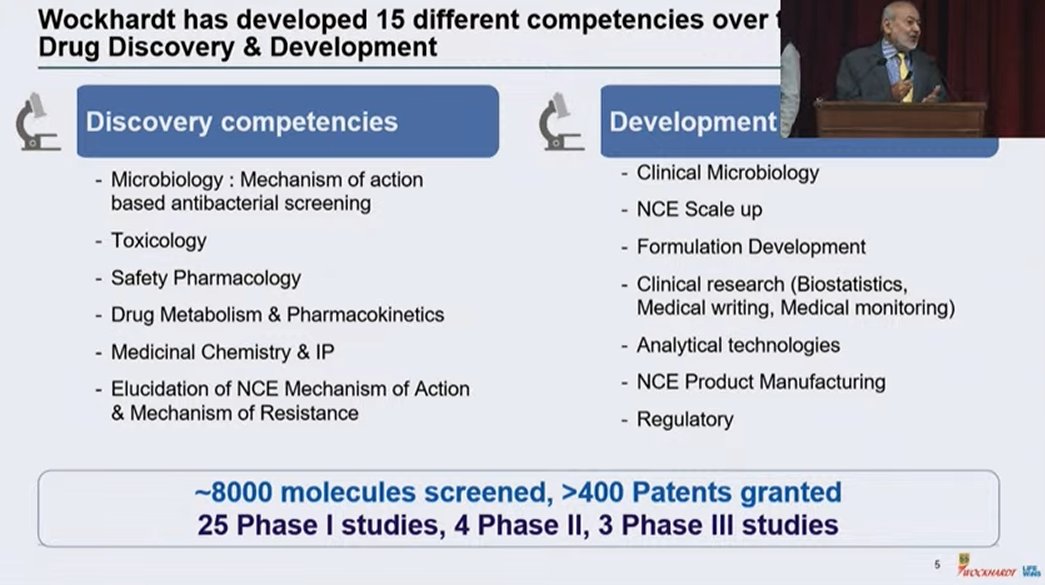

US FDA has approved Wockhardt's Zaynich (WCK 5222)!

This honestly feels like a very personal moment for me.

First US FDA approval for an Indian NCE is historic. Wockhardt is a national pride and deserves to be celebrated. Hopefully, this marks the beginning of a pharma innovation cycle in India.

Congratulations to everyone who was part of this journey!

Over and out.

- a rookie analyst from Chennai!

26 Dec 2023

Wockhardt consumed a bit of me and is an example of "Capabilities > Balance Sheet > Income Statement". In fact, the capabilities screwed up the BS and P&L. 😅

I can call myself a (wannabe) "Deep Tech" investor although I am not sure if I will even make money in this.

8

28

150

17,586

A company's opening remarks in Q4 FY26 concall:

“There are certain years in a company's journey where performance improves, and certain years where the foundation for the next decade is built. For us, FY26 has been one such year where we have built our foundation."

7

3

44

10,004

RT @InvestingCanons: Stanley Druckenmiller: “A lot of my style is you [first] build a thesis, hopefully that no one else has built. You sor…

124

6

Sanjay Kumar Elangovan retweeted

Mar 30

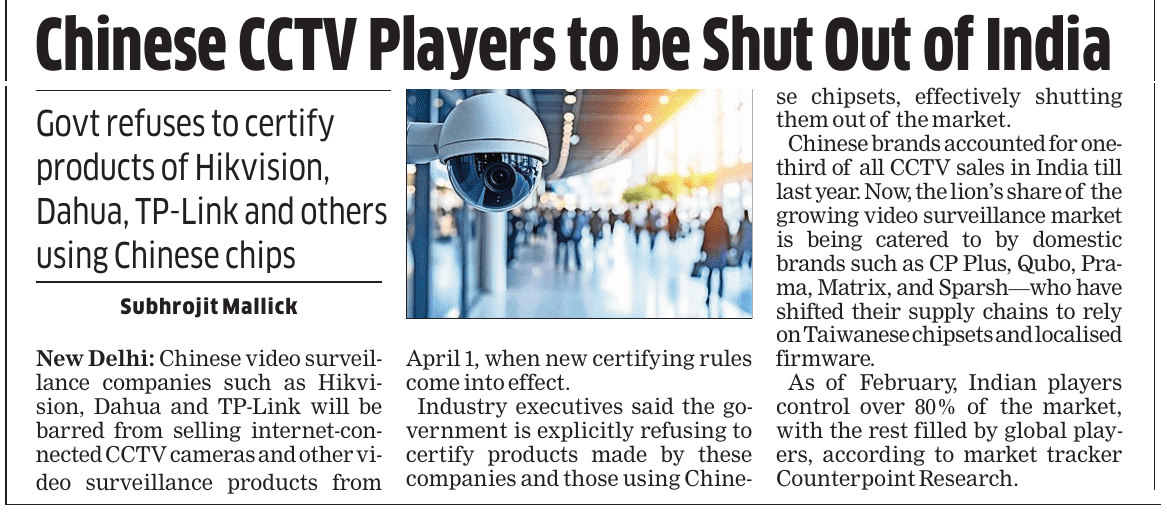

News is focused on which camera brand replaces Hikvision. The more interesting story is who makes the chip inside the camera.

Until 2019, that answer was overwhelmingly HiSilicon, Huawei's semiconductor arm that dominated surveillance SoCs globally. US sanctions killed that supply chain overnight and the entire industry moved to Ambarella, Novatek, and Sigmastar.

India's CCTV ban accelerates the same logic one layer deeper. Not just who assembles the camera, but who designs the silicon.

And that story is already further along than most people realize. L&T Semiconductor Technologies has signed a deal with CP Plus to supply indigenously designed Vision SoCs for 9 million IP cameras over three years. These aren't concept chips. They support 8MP imaging and this is the first time surveillance cameras will be made using chips from an Indian company.

CP Plus is the largest domestic brand by market share, so this isn't a token pilot.

Beyond L&T Semi, there are at least four more startups building surveillance SoCs under the government's Design Linked Incentive scheme. Mindgrove Technologies has the V2600, a surveillance-grade edge AI chip targeting late 2026 commercial launch. BigEndian Semiconductors raised $3M from Vertex Ventures and partnered with Cadence on Project VASU, a secure-boot SoC with encryption baked into the silicon. 3rdiTech and Netrasemi round out the group. Collectively these four have raised over ₹300 crore and taped out test chips in 2025.

Two years ago none of this existed. Now you have five separate Indian chip efforts targeting the same market, with the largest one already locked into a volume manufacturing agreement.

India did the same thing in telecom: kicked out Huawei, filled the gap with allied vendors, then started building its own stack with Tejas Networks. Surveillance silicon is following the same script, and hopefully moving faster.

Mar 30

India bars Hikvision, Dahua and TP-Link CCTV sales from April 1 under certification rules. Chinese brands had ~33% share till 2025; domestic firms now hold >80% share. Certification denial covers products using Chinese chipsets, shifting supply chains.

21

141

646

57,543

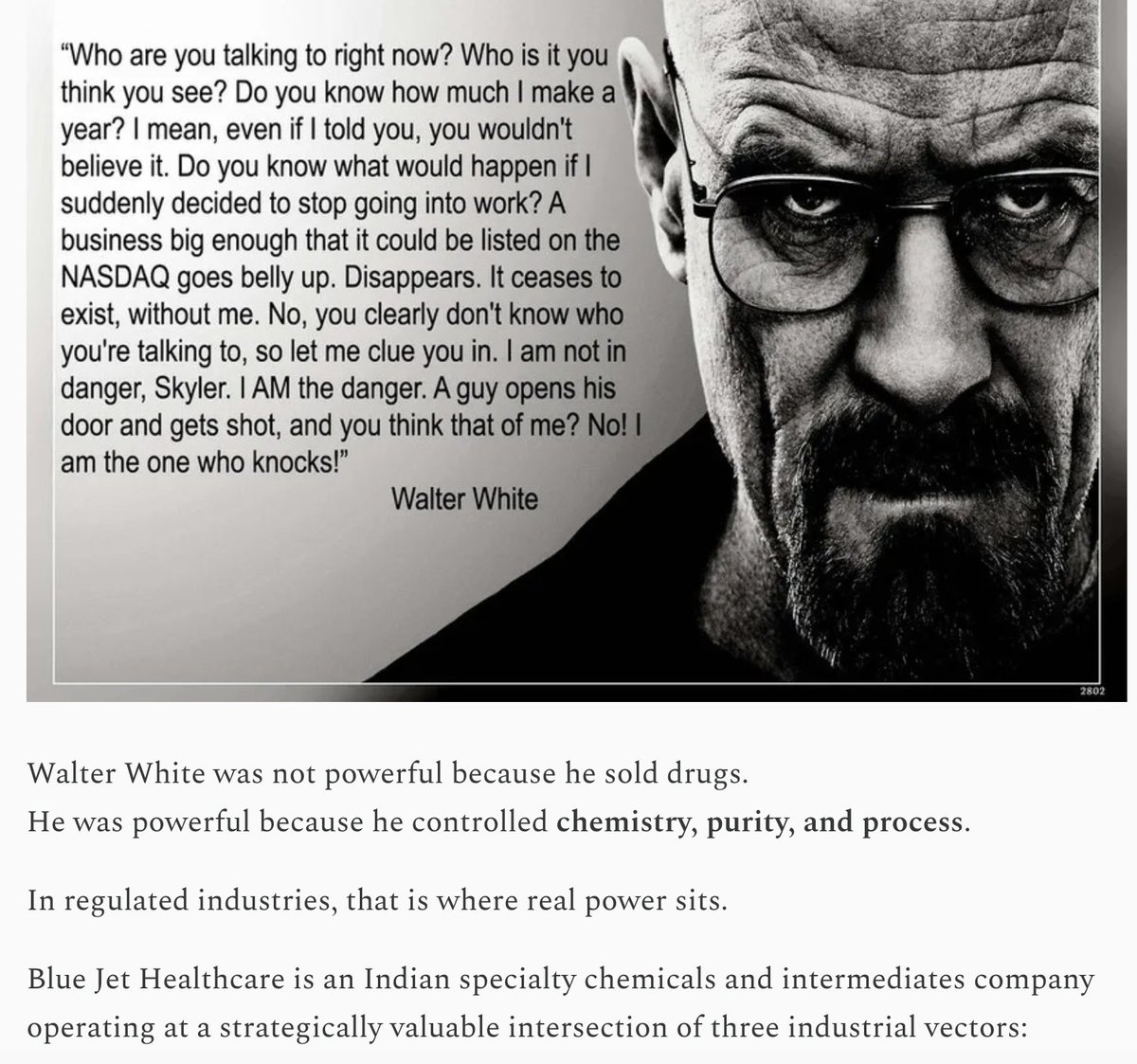

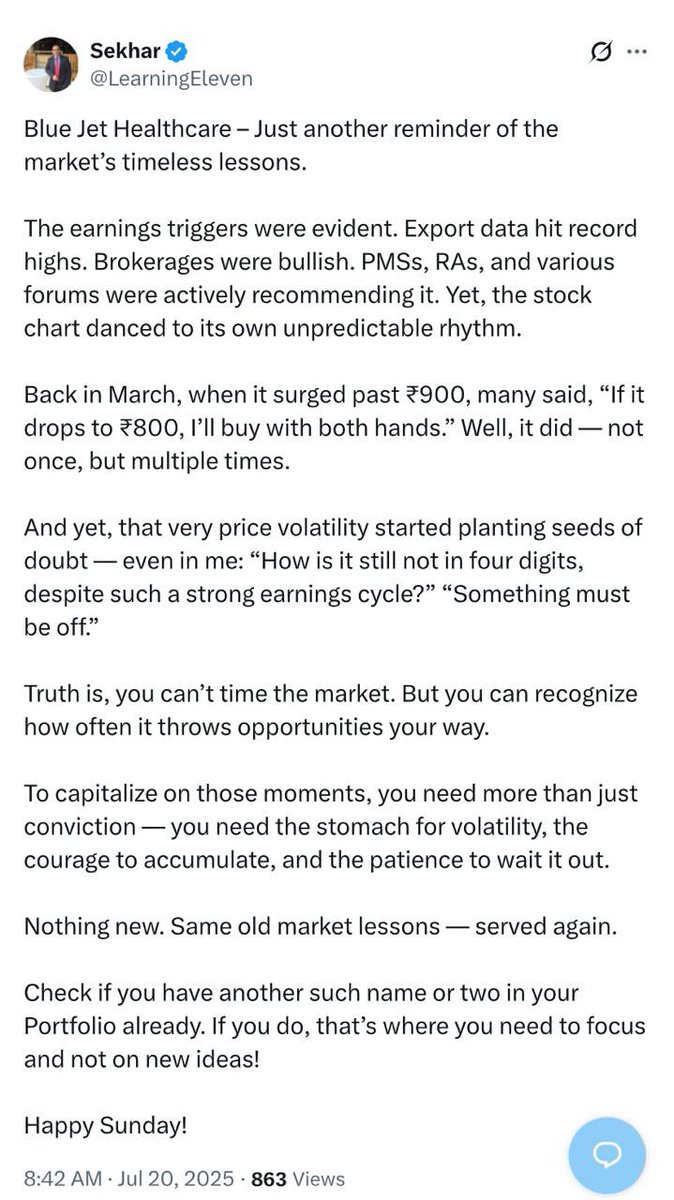

Content and storytelling >>> fundamentals / valuations is peak Substack!

If your investment thesis needs a Breaking Bad analogy, you’re not analysing the business, you’re writing fiction.

The "TSMC of Niche Pharma" is down 60% from the post and 33% since quoting Walter White.

22 Jul 2025

Timeless lessons lasted 2 days! 😂

"Nothing new. Same old market lessons - served again."

5

25

5,047

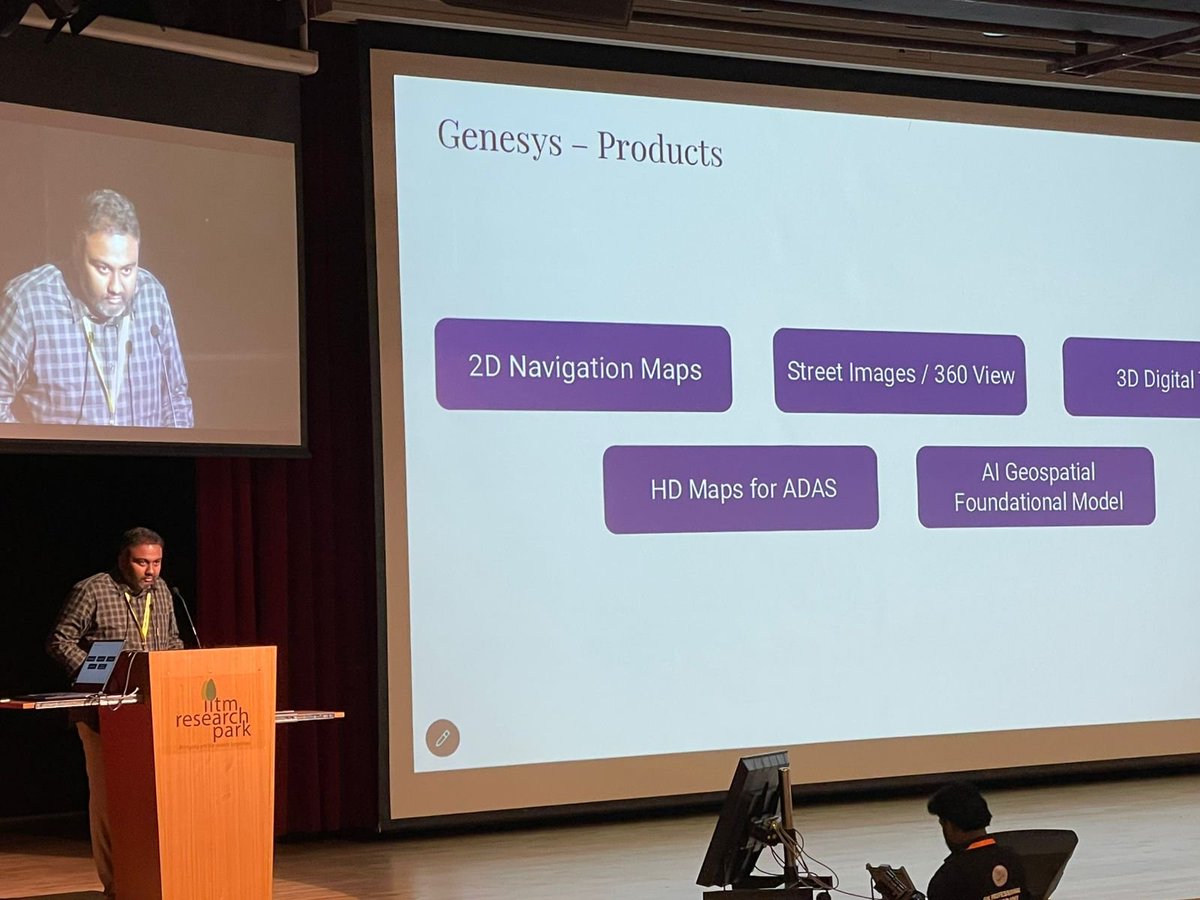

It was a pleasure to speak at the TIA 20-20 Ideas Summit 2026 at IIT Madras Research Park.

Presented my stock pitch on Genesys - a niche business & potential proxy to India's digital infrastructure build-out!

Feedback welcome.

Thank you @TIA_Investors for the opportunity.

23 Dec 2025

My investing journey started in 2018 at @TIA_Investors' Bullet Proof Investing event. Almost 8 years later, I’m honoured and excited to be presenting at their 20-20 Ideas Summit!

7

5

91

11,133

Many are writing off Indian IT by assuming Palantir or AI agents will own these risks:

• Governance

• Compliance & audit

• SLAs, performance, delivery

And Enterprises still need someone for orchestration and integration.

Indian IT must evolve but it’s far from obsolete.

Feb 6

I recently spoke at Umagine2026 where I said that we are in a Shackleton moment. We have to let go of our ego and accept the fact that software services as we know it is no longer relevant. AI commoditises code. The head count and arbitrage model will be broken. Software engineering, architecture, domain ownership and AI-governed delivery stays relevant. This is a great time where coding is democratised. Build on your ideas, productise them. The Anthropic announcement on building the C compiler with agents in 2 weeks should tell us something.

4

7

2,928

Sanjay Kumar Elangovan retweeted

Our cofounder Sagar Arya dives into the tremendous shift underway in the aerospace industry in this riveting conversation with @ishmohit1 @soicfinance

With Western supply chains struggling and a global backlog of 17,000 aircraft, India is emerging as the next manufacturing hub.

In this video, @soicfinance deep dives into the value chain, astutely focusing on key players including @DynamaticTech.

youtube.com/watch?v=YsMadW-b…

5

10

61

20,485

Sanjay Kumar Elangovan retweeted

26 Dec 2025

When you find a company with

elite management, structural tailwinds, strong products, fast growth, and ruthless ambition, and you have the ability to track it closely:

you don’t nibble. You size up.

A 5–10% allocation feels safe today,

but becomes a regret in hindsight.

These setups don’t come every year.

They show up once in a few years.

And no, valuations won’t look cheap.

When quality is obvious, the edge lies in growth, not multiples.

18

16

232

25,724

23 Dec 2025

My investing journey started in 2018 at @TIA_Investors' Bullet Proof Investing event. Almost 8 years later, I’m honoured and excited to be presenting at their 20-20 Ideas Summit!

22 Dec 2025

Sanjay Kumar Elangovan, Co-Fund Manager, ithought PMS, will be speaking at TIA 20-20 Ideas Summit 2026 !

@sanjaylangval @ithoughtpms

Link to Register :

docs.google.com/forms/d/e/1F…

2

32

14,508

24 Oct 2025

Kenneth on Metals:

“Audacious statement - By 2030, Tata Steel’s balance sheet will be better than India’s largest FMCG firm”

youtube.com/live/qkvzEkbmqnA…

7 Mar 2025

China aiming at crackdown of “neijuan” and West wants to industrialise

A couple of good years of cashflows and corporate India might have a debt free Steel company (after having virtually all sectors deleveraged)

5

18

225

62,215

22 Jul 2025

Timeless lessons lasted 2 days! 😂

"Nothing new. Same old market lessons - served again."

4

1

47

14,923

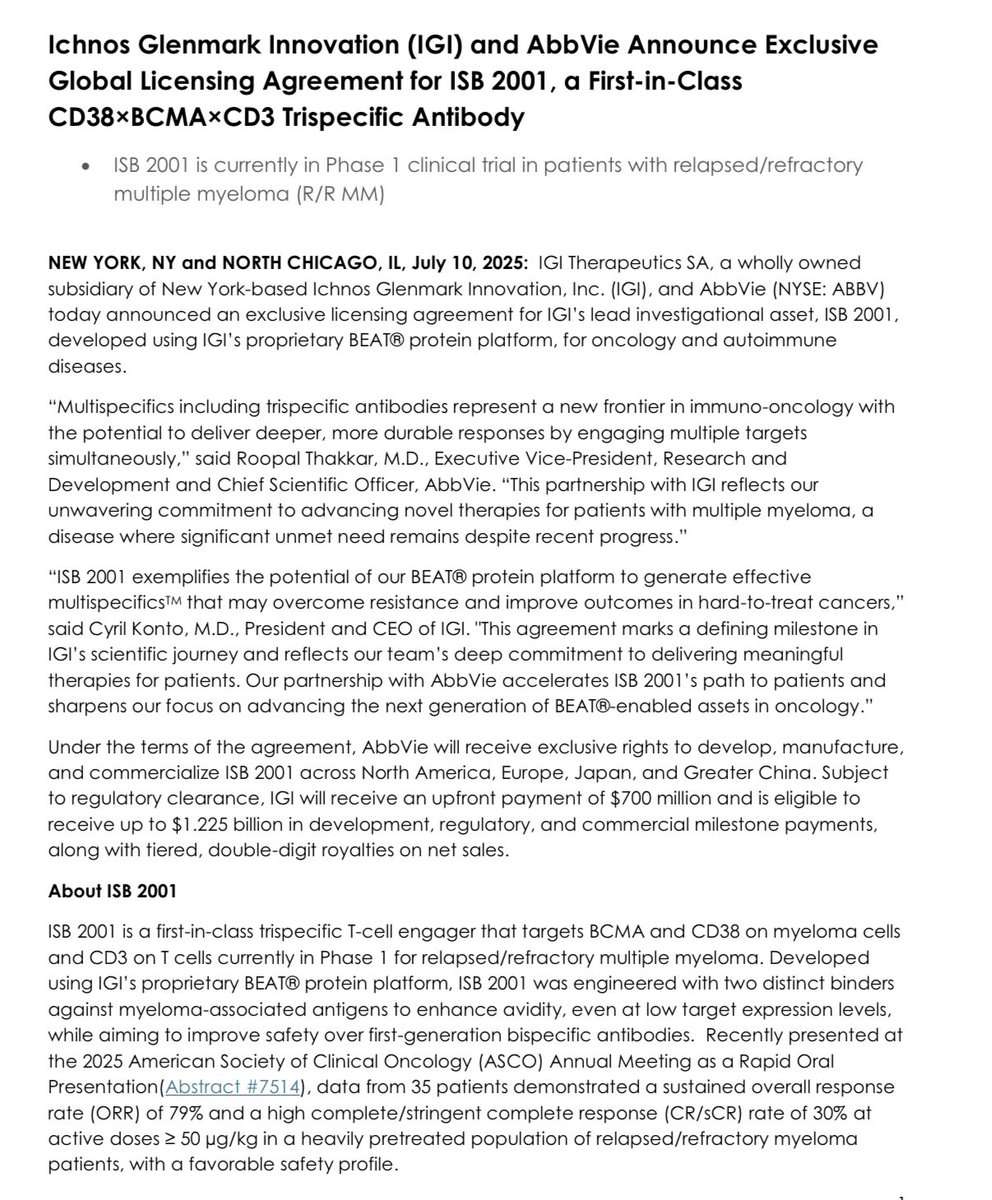

10 Jul 2025

$700 Mn upfront payment for an Indian drug in Phase 1

5 Mar 2025

If CDMO companies working on innovator molecules are getting such multiples, wonder what Indian innovators will get when their drugs start.

4

4

63

8,764

Sanjay Kumar Elangovan retweeted

21 Jun 2025

We are excited to launch the ithought Equity Research Fellowship, a full-time, nine-month program based in Chennai designed for aspiring equity analysts.

Please refer to our LinkedIn post for complete details of the program and application instructions:

linkedin.com/posts/ithoughtp…

1

10

59

30,967

4 May 2025

WB:

"You learn more from balance sheets than most people give them credit for.

I actually spend more time looking at balance sheets than income statements. Wall Street often focuses on IS, but I like to study BS ideally over an 8 to 10-year period before I even glance at IS."

7 Jul 2023

Capabilities > Balance Sheet > Income Statement

It has taken me 4 years to understand what Kenneth meant when he said "I am a Balance Sheet investor"

Add valuation to it, you wont go wrong.

If you are entering based on a good P&L, you are late to the party. Most of FinTwit is.

1

1

26

3,569

4 May 2025

"You can’t hide as much on the balance sheet. It's harder to manipulate than earnings figures."

1

8

1,651

26 Apr 2025

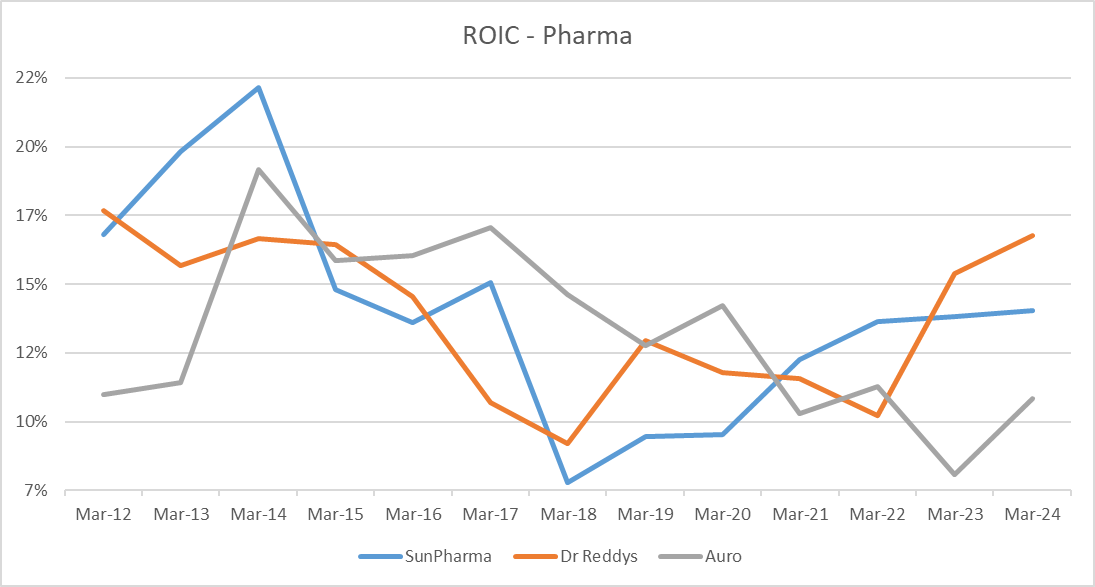

I had done a basic analysis of pharma companies based on Kenneth's framework.

ROIC = NOPAT Margin (P&L item) * Asset Turn (Balance Sheet item)

One could have bought Sun in FY18/FY19 and Auro in FY23/FY24 and beaten Nifty 50 comfortably.

25 Apr 2025

Hi Sanjay,

Couldn't DM you due to X rules on msg'g. you made a breakdown of tweets on Kenneth Andrade's style of investing during COVID unfortunately you had to take them down due to obligations on the work front. Is there a way I can have a glimpse of that?

@sanjaylangval

4

2

29

5,492

26 Apr 2025

I had also applied this capital cycle framework to broader index of BSE 500 companies in this webinar:

youtube.com/watch?v=Up08Pnuj…

1

1

19

3,053

26 Apr 2025

One tweet summary of what I learnt from Kenneth:

x.com/sanjaylangval/status/1…

7 Jul 2023

Capabilities > Balance Sheet > Income Statement

It has taken me 4 years to understand what Kenneth meant when he said "I am a Balance Sheet investor"

Add valuation to it, you wont go wrong.

If you are entering based on a good P&L, you are late to the party. Most of FinTwit is.

1

4

1,950