Joined September 2025

- Tweets 182

- Following 117

- Followers 442

- Likes 336

83 Photos and videos

16 US banks — JPMorgan, BofA, Citi, Wells Fargo — just announced their own tokenized deposit network.

Not to embrace crypto. To fight it.

Their tokens stay locked inside the banking system. Stablecoins are open to anyone, anywhere.

Which side wins: bank money or open money?

26

⚽ The game is on — watch the ball become $SDA. Featured partner in Coinstore's road to the FIFA World Cup 2026. To take part: open Coinstore, trade SDA, join the World Cup events. Helsinki · MiCA Art. 6 · Solana. coinstore.com/spot/SDAUSDT

2

5

426

🦎 $SDA is now listed on CoinGecko 🎉

Track live price, market cap & supply for Sustainable Digital Assets — the Solana-based renewable-energy RWA token.

📊 coingecko.com/en/coins/sda-t…

Built on #Solana · 100M fixed supply · 0% tax

Not financial advice. DYOR.

3

5

103

Sustainable Digital Assets retweeted

A blockchain platform has just been admitted to Ghana's SEC regulatory sandbox for RWA tokenization. And this one hits differently.

Because this isn't a story about the US, Europe, or Asia.

This is Africa building its own tokenized asset infrastructure, from the inside out.

@africoin_ai has been admitted into the Virtual Asset Regulatory Sandbox under the Securities and Exchange Commission of Ghana - one of only 11 approved virtual asset participants in the entire framework.

Let that number sink in.

Here's what Africoin actually does:

The platform tokenizes real-world assets - commodities, agricultural products, renewable energy projects, and carbon credits... converting physical assets into verified, asset-backed digital tokens.

Every asset goes through independent financial, legal, and technical verification before a single token is issued. Ownership records are transparent, traceable, and immutable on-chain.

Investors get fractional access to asset classes that have historically been locked behind geography and capital requirements. Issuers get direct access to a global investor base without traditional intermediaries. All running 24/7 with near-instant settlement.

What This Means for the RWA Space

1. Africa's regulatory infrastructure is getting serious: Admission into a government-supervised sandbox is a stress test, not a certificate. Africoin now operates under real regulatory scrutiny. AML standards. Investor protection frameworks. This is what institutional-grade looks like at the building stage.

2. The assets being tokenized tell the real story: Mining, agriculture, renewable energy, carbon credits... These are the backbone of Africa's economy. Putting them onchain unlocks capital formation for sectors chronically underfunded by traditional finance.

3. Fractional ownership is the access story Africa has been waiting for: For decades, wealth generated by Africa's resources flowed outward to foreign investors and international intermediaries. Tokenization changes that, opening Africa's most valuable assets to African investors and global investors who previously had no compliant pathway.

4. 11 approved participants, that's the entire field: First movers in a regulated sandbox define the standards everyone who comes after them has to meet. That's not just a milestone. That's a market position.

The Bigger Lesson

Africoin's admission is not just a company milestone. This signals that Africa's regulators are building frameworks sophisticated enough to support the next generation of asset-backed digital infrastructure, in a deliberate and compliant manner.

The continent is not waiting for the global RWA economy to include it; it is building an RWA economy of its own.

At RWA Story House, this is exactly the kind of story we exist to tell. The builders defining Africa's tokenized future deserve to be heard.

— The RWA Story House

2

2

5

554

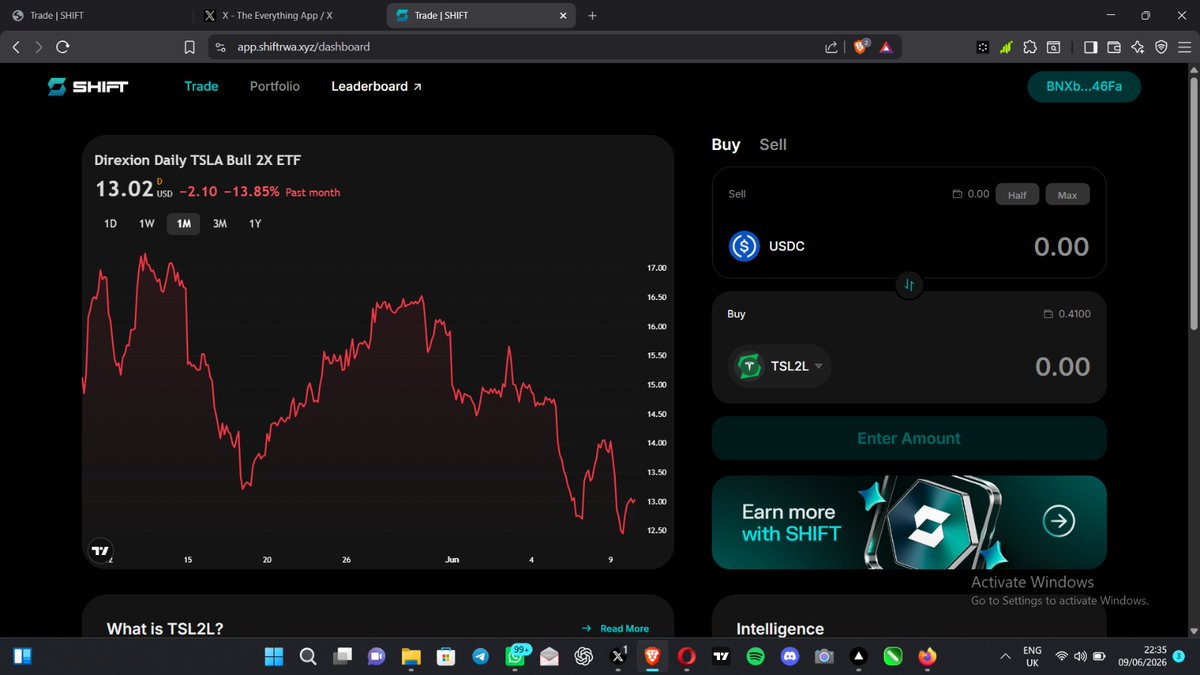

SHIFT STOCK RESEARCH

DIREXION DAILY TSLA BULL 2X ETF ($TSL2L)

My research thesis focuses on the $TSL2L tokenized asset. In the current market environment, choosing the right vehicle requires balancing macro trends with sector-specific catalysts. Leveraged stock tokens allow crypto-native investors to gain amplified exposure to traditional equities 24/7 without leaving the DeFi ecosystem. Right now, tokenized real-world assets (RWAs) stand out as the ultimate "pick-and-shovel" play for bridging the digital asset industry with traditional finance.

Here is the structured investment thesis, catalyst breakdown, and risk analysis for the 2x Long $TSL2L token.

The Thesis: The Ultimate High-Beta Growth Proxy

Investing in the 2x Long $TSL2L token is a thesis built on compounding automotive/energy volume, cutting-edge AI infrastructure, and a cyclical retail market recovery. While trading individual tech stocks carries unique asset exposure, Tesla acts as an informal high-beta index for the health of consumer innovation, renewable transition, and retail trading sentiment.

Revenue Scaling on Global Tech Adoption: Unlike static traditional equities, Tesla generates diverse revenue streams from vehicle production, energy storage business scaling, and automated software licensing. High retail and institutional interest translates directly to massive on-chain trading volumes for this tokenized proxy.

EXPECTED CATALYSTS

RWA Expansion & SHIFT Platform Dominance: Tokenized traditional equities are quietly becoming one of the most active sectors in decentralized finance. By capturing user mindshare and providing permissionless, wallet-native 2x leverage without forced liquidation parameters or centralized lender dependency, $TSL2L offers a seamless gateway for crypto capital to capture Wall Street momentum.

Corporate Earnings, Delivery Volume, & Guidance Beats: Historically, traditional analyst models underestimate the explosive nature of Tesla’s multi-pronged business approach, particularly its energy storage and Full Self-Driving (FSD) ecosystem developments. Upcoming quarterly earnings announcements serve as hard data catalysts where production beats and revised guidance figures can spark massive re-ratings of the underlying equity, providing an amplified 2x tailwind on-chain.

Conclusion

The 2x Long $TSL2L token offers an exceptional risk-to-reward ratio right now because it combines the structural upside of an industry-leading technology disruptor with a built-in 2x leverage profile native to Web3. It bypasses the friction of moving capital back to traditional brokerage systems, focusing instead on capitalizing on high-beta equity volatility straight from your crypto wallet.

1

2

4

89

Sustainable Digital Assets retweeted

May 25

Africa is sitting on the world's greatest renewable energy opportunity.

And almost nobody is financing it properly.

Let's break down why — and how $REQUIZA fixes it.

The problem:

🔸 Africa needs $200B annually to meet its energy infrastructure gap

🔸 Traditional financing locks out small and mid-scale energy developers

🔸 Foreign energy companies extract profits and repatriate them abroad

🔸 Communities that host energy projects rarely benefit from them

🔸 Climate capital from the West rarely reaches African hands directly

The result?

Africa powers the global economy with its resources.

But African communities remain in darkness.

The $REQUIZA solution:

☀️ SOLAR PROJECTS

From rooftop installations to utility-scale solar farms — energy developers can tokenize projects on the Requiza Launchpad and access global green capital instantly.

💨 WIND ENERGY

Coastal and highland wind projects across Africa brought on-chain — turning Africa's natural geography into investable, tokenized infrastructure.

💧 HYDRO PROJECTS

River and micro-hydro developments tokenized and financed through the Requiza ecosystem — powering communities and generating on-chain returns.

⚡ REQUIZA PIONEER ENERGY

We don't just host energy projects. We build our own.

Requiza-owned renewable energy ventures — solar, wind and hydro — generating direct, stable value for every $REQUIZA token holder.

Green energy is the fastest growing investment sector on earth.

Africa has the most untapped green energy potential on earth.

$REQUIZA is the bridge between both.

The question isn't whether this will be big.

The question is whether you'll be inside it when it is.

📜 CA: 5ycEUekKbEWHfK4EE4BWKxomtwUoSFBmRqvHCG6wg5zZ

🌐 requizaempire.io

🐦 x.com/realrequiza

💬 t.me/requizaempiregroup

📢 t.me/requizaempire

🤝 x.com/i/communities/20392362…

8

7

20

169

⚽ From Pizza Day to the World Cup 2026 — powered by $SDA.

Featured partner in @CoinstoreExc's campaign. Live on Coinstore, trade-to-win through Jul 19.

coinstore.com/spot/SDAUSDT

13

16

232

⚽ The stage is set for World Cup 2026.

🇺🇸 🇨🇦 🇲🇽 — who claims it? Make your prediction and join the campaign where $SDA is a featured partner alongside @CoinstoreExc.

Predict RT 👇

Jun 8

The stage is set for the host nations ⚽🌎

Can USA, Canada and Mexico come out to claim their dominant victories?

Share your predictions below 👇

🇺🇸 USA 🇨🇦 Canada 🇲🇽 Mexico

Example:

✅ USA

❌ Canada

✅ Mexico

1️⃣ Follow @CoinstoreExc @sdatoken @SwordsofBlood_

2️⃣ Like & RT

3️⃣ Comment your predictions UID

🎁 10 lucky winners will share 200U worth of sponsor token rewards!

⏰ Ends Jun 10

#Coinstore #SDA #HBOX #FIFAWorldCup #WorldCup2026 #WorldCupPredictions #PredictAndWin

2

5

169

Sustainable Digital Assets retweeted

Jun 8

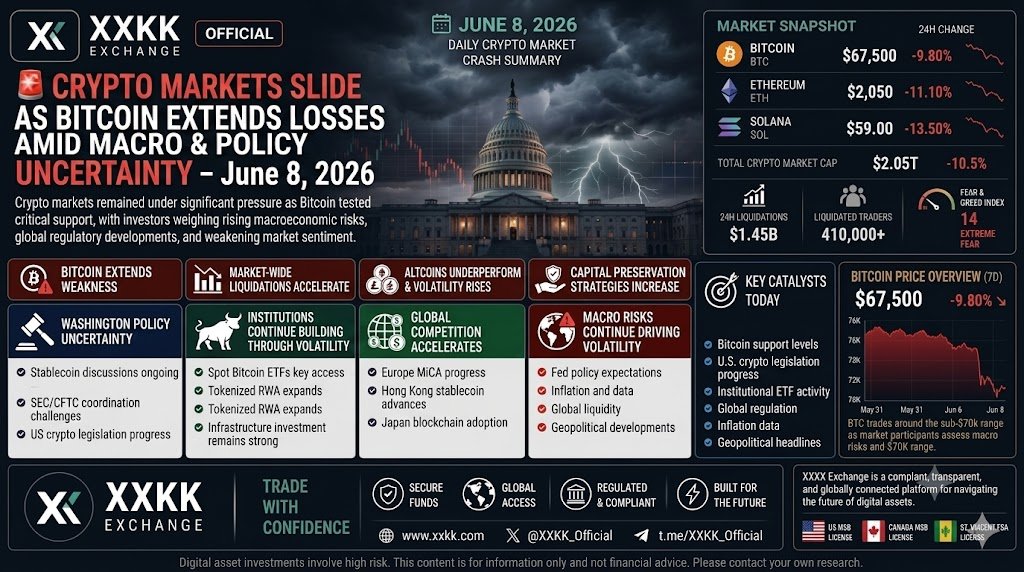

🚨 Crypto Markets Slide as Bitcoin Extends Losses Amid Macro & Policy Uncertainty – June 8, 2026

Crypto markets remained under significant pressure this weekend as Bitcoin continued its downward trend, testing critical support levels while investors weighed rising macroeconomic risks, global regulatory developments, and weakening market sentiment.

The broader crypto market followed Bitcoin lower, with Ethereum and major altcoins experiencing additional selling pressure as traders reduced exposure ahead of a busy week for both economic data and policy developments.

📉 Bitcoin Weakness Dominates Market Sentiment

After several failed attempts to regain momentum, Bitcoin remains under pressure as risk appetite across global markets continues to deteriorate.

Today's key market developments:

🔻 Bitcoin trades near recent lows

🔻 Market-wide liquidations continue increasing

🔻 Altcoins underperform as volatility rises

🔻 Fear sentiment returns across digital assets

🔻 Traders move toward capital preservation strategies

Market participants are closely monitoring whether institutional buyers step in at current levels.

🏛️ Washington Crypto Policy Remains a Key Catalyst

While market sentiment remains weak, regulatory developments continue progressing.

Investors are watching:

• Stablecoin legislation discussions

• SEC & CFTC regulatory coordination

• Digital asset market structure proposals

• Institutional custody frameworks

• Blockchain innovation and tokenization initiatives

Industry leaders continue emphasizing that regulatory clarity remains one of the most important long-term drivers for digital asset adoption in the United States.

🏦 Institutions Continue Building Through Volatility

Despite the sell-off, institutional activity remains active:

• U.S. Spot Bitcoin ETFs continue serving as a primary access point for institutional capital

• Major asset managers maintain long-term crypto exposure

• Tokenized Real-World Assets (RWA) continue expanding

• Blockchain infrastructure investment remains strong

Many institutions view current market weakness as part of a broader cycle rather than a fundamental shift in the long-term digital asset thesis.

🌍 Global Competition for Digital Finance Accelerates

International crypto development continues despite market weakness:

🇪🇺 Europe moves closer to full MiCA implementation

🇭🇰 Hong Kong advances regulated stablecoin initiatives

🇯🇵 Japan expands institutional blockchain adoption

🏦 Global banks continue testing tokenized settlement and payment infrastructure

Competition among major financial centers to lead the future of digital finance remains intense.

⚔️ Macro Risks Continue Driving Volatility

Markets remain focused on:

• Federal Reserve policy expectations

• Inflation and employment data

• Global liquidity conditions

• Oil market volatility

• Geopolitical developments

As uncertainty remains elevated, crypto markets continue trading as a macro-sensitive asset class.

📈 What Markets Are Watching This Week

⚠️ Bitcoin support levels

🏛️ U.S. crypto legislation progress

🏦 Institutional ETF activity

🌍 Stablecoin regulation developments

📊 Inflation and macroeconomic data

⚔️ Geopolitical risk headlines

XXKK Official keeps users ahead of every major market catalyst — from market volatility and institutional flows to global regulation and macroeconomic developments.

With US MSB, Canada MSB, and St. Vincent FSA licenses, XXKK Exchange delivers a compliant, transparent, and globally connected platform for navigating the future of digital assets.

#Bitcoin #Crypto #BTC #Ethereum #CryptoMarket #CryptoNews #ETF #Blockchain #Web3 #DigitalAssets #XXKKExchange #MarketUpdate #Stablecoins #Regulation

1

3

363

Sustainable Digital Assets retweeted

Jun 6

CHAPTER 5: DREX Mineral –

The Financial Engineering of Subsurface RWA Tokenization

The traditional commodity model is a liquidity trap. Under the legacy paradigm, Brazil exports raw, unrefined critical minerals (Lithium, Niobium) while absorbing high banking spreads and currency volatility in USD debt markets. DREX Mineral disrupts this by merging orbital intelligence with Web3 programmable finance, bypassing traditional banking intermediaries to capture direct global liquidity

1. The Tokenization Architecture:

From LiDAR to LedgerThe financial engineering of DREX Mineral operates in three automated layers:

The Physical Validation (Oráculos de Ativo):

Advanced satellite imagery and orbital LiDAR map the exact volume, density, and purity of subterranean critical minerals. This data is audited by national agencies (ANM) and fed into the blockchain via decentralized oracles as immutable geological proofs.

The Fractional Tokenization:

These proven, in situ (soterradas) reserves are legally structured into special purpose vehicles (SPVs) and fractionalized into digital Real World Asset (RWA) tokens directly on the Central Bank’s DREX platform.

Programmable Smart Contracts:

Each token represents a fractional claim on future mining yields or raw asset value, embedded with automated compliance, royalty distribution, and tax deductions executed instantly on-chain without clearing houses.

2. De-dollarized Liquidity & Infrastructure Financing

DREX Mineral serves as an alternative sovereign credit mechanism that transforms underground wealth into immediate working capital:

Collateralized Liquidity Pools:

Brazil can place these RWA tokens into global decentralized finance (DeFi) pools or sell them directly to institutional funds (e.g., BlackRock). Global capital deploys hard currency directly into the DREX network, purchasing green-backed assets completely insulated from Western inflation or Chinese credit traps.

Funding the Sanctuary:

The capital raised does not sit in treasury bonds; it is programmatically locked via smart contracts to fund domestic high-value infrastructure: building the USP PocketFab micro-foundries and deploying the green data centers powered by our $30–$35/MWh energy matrix.

By financializing the subsoil prior to extraction, Brazil stops trading its future for "digital mirrors." We decouple from the Wall Street banking monopoly, utilizing sovereign programmable money to fund the physical assets of our computing sanctuary.

1

2

112

Sustainable Digital Assets retweeted

Jun 3

🚨 Crypto Sell-Off Deepens as Bitcoin Slides Below Key Support – June 3, 2026

Crypto markets faced heavy selling pressure today as Bitcoin fell sharply toward the $68K–$70K range, triggering renewed concerns across digital assets. Ethereum, Solana, and other major cryptocurrencies also declined as traders reacted to a combination of macro uncertainty, profit-taking, and risk-off sentiment across global markets.

The decline comes after weeks of regulatory optimism and strong institutional inflows, highlighting that short-term volatility remains a defining feature of the crypto market.

📉 Bitcoin Breakdown Sparks Market-Wide Liquidations

Bitcoin's decline below recent support levels triggered a wave of liquidations across leveraged positions, increasing volatility throughout the market.

Key market developments:

• Bitcoin falls to multi-week lows

• Altcoins underperform as risk appetite weakens

• Liquidations accelerate across futures markets

• Traders rotate toward cash and defensive assets

Market sentiment has shifted noticeably as investors reassess near-term risk exposure.

🏛️ Regulatory Progress Continues Despite Market Weakness

While prices declined, regulatory developments remained constructive.

Washington continues working toward a clearer framework for digital assets, with discussions focusing on:

• Stablecoin regulation

• Digital asset classification standards

• SEC & CFTC coordination

• Institutional custody requirements

• Tokenized asset frameworks

Industry leaders continue emphasizing that regulatory clarity remains one of the most important long-term catalysts for crypto adoption.

🏦 Institutions Remain Focused on Long-Term Adoption

Despite today's sell-off, institutional participation remains a major structural driver:

• U.S. Spot Bitcoin ETFs continue attracting long-term attention

• Major asset managers remain active in digital assets

• Tokenized Real-World Assets (RWA) continue expanding

• Traditional financial institutions keep investing in blockchain infrastructure

Many analysts view the current volatility as a short-term market adjustment rather than a fundamental change in institutional adoption trends.

🌍 Global Digital Asset Competition Accelerates

Outside the U.S., governments continue advancing digital asset initiatives:

🇪🇺 Europe moves closer to full MiCA implementation

🇭🇰 Hong Kong advances stablecoin licensing

🇯🇵 Japan expands institutional Web3 adoption

🏦 Global banks continue exploring blockchain settlement systems

Competition to become a leading digital asset hub remains intense across major financial centers.

⚔️ Macro Risks Return to the Spotlight

Markets remain focused on:

• Federal Reserve policy expectations

• Inflation concerns

• Global liquidity conditions

• Energy market volatility

• Geopolitical developments

Risk assets broadly weakened as investors adopted a more defensive posture ahead of key economic events.

📈 Key Themes Today

🔻 Bitcoin breaks below recent support

🏛️ U.S. crypto legislation remains in focus

🏦 Institutional adoption continues

🌍 Global stablecoin competition accelerates

⚔️ Macro uncertainty drives volatility

📊 Traders monitor key support levels

XXKK Official keeps users ahead of every major market catalyst — from market volatility and institutional flows to global regulation and macroeconomic developments.

With US MSB, Canada MSB, and St. Vincent FSA licenses, XXKK Exchange delivers a compliant, transparent, and globally connected platform for navigating the future of digital assets.

#Bitcoin #Crypto #BTC #Ethereum #CryptoCrash #CryptoNews #DigitalAssets #ETF #Regulation #XXKKExchange #CryptoMarket #Blockchain #Web3

2

1

4

450

Sustainable Digital Assets retweeted

🚀 Crypto Pulse | June 4, 2026 🚀

Stablecoins, mining infrastructure, tokenized finance, Cardano weakness, and prediction market disputes shaped today’s crypto cycle.

Revolut moved deeper into the U.S. financial market with plans for a new bank that will include stablecoins, crypto trading, multi-currency deposits, and FDIC-insured banking products.

The signal is clear.

Stablecoins are no longer being treated as a crypto side feature.

They are becoming part of the future banking stack.

Revolut already serves tens of millions of users globally, and its U.S. banking push shows how fintech firms are trying to merge traditional accounts, global payments, crypto access, and stablecoin rails into one consumer product.

This matters because the next phase of stablecoin adoption may not come only from crypto exchanges.

It may come from fintech apps, digital banks, remittance platforms, and cross-border payment tools.

Bitdeer also pushed forward with physical infrastructure, breaking ground on a 100 MW energy and computing facility in Alberta.

That headline matters because mining is becoming less about simply plugging machines into cheap power.

The industry is moving toward vertically integrated energy, data centers, high-performance computing, and AI-linked infrastructure.

Bitcoin miners are trying to prove they are not just mining companies.

They want to become energy and compute companies.

That shift could define the next cycle for public mining firms.

Cardano faced another difficult market moment as ADA reportedly slipped below 20 cents while Charles Hoskinson warned about deeper ecosystem failures and said he was taking a break.

The pressure around Cardano reflects a wider problem across older Layer-1 ecosystems.

Strong communities alone are not enough.

Networks now need active developers, working products, sustainable funding, liquidity, and real user demand.

When those weaken, price follows sentiment.

Goldman Sachs also appeared in today’s institutional tokenization cycle through reports of a tokenized real estate fund effort involving Apex and Archax.

The bigger point is not just one fund.

It is that tokenization is spreading beyond U.S. Treasurys and stablecoins into real estate, private markets, and structured investment products.

Traditional finance is not ignoring blockchain.

It is selectively adopting the parts that improve issuance, settlement, access, and recordkeeping.

Polymarket also remained in focus after a dispute around Strategy’s recent bitcoin sale.

The issue centered on timing: whether a Strategy sale should count for May or June based on the sale date versus the disclosure date.

This shows one of the hardest problems in prediction markets.

It is not only about betting on events.

It is about how rules define truth.

If resolution rules are unclear, even accurate market participants can end up fighting over interpretation.

Today’s market signal:

Revolut’s U.S. banking plan shows stablecoins are moving closer to mainstream fintech products.

Bitdeer’s Alberta facility highlights the mining industry’s shift toward energy-backed compute infrastructure.

Cardano’s weakness shows how older ecosystems can lose momentum when projects, funding, and confidence weaken.

Goldman Sachs-linked tokenized real estate activity strengthens the real-world asset narrative.

Polymarket’s Strategy dispute shows why prediction markets need precise, enforceable resolution rules.

Takeaway:

Crypto is splitting into two markets.

One side is becoming more institutional, regulated, and infrastructure-driven.

That side includes stablecoins, tokenized assets, public mining companies, banking products, and settlement rails.

The other side is still struggling with ecosystem confidence, weak token demand, governance disputes, and unclear market structure.

The lesson is simple.

Check first. Then decide.

1

1

173

Backpack just announced Solana's first regulated IPO tokenization.

Real shares, not synthetics. Superstate's SEC-registered transfer agent. Actual IPO allocations, on-chain.

Not a bridge. Not a synthetic. The real thing, natively on Solana.

SDA: MiCA Solana. Built for this.

4

104

Sustainable Digital Assets retweeted

🌍🚀 Green Carbon Exchange Projects (GCXP) is where blockchain meets one of the world’s biggest real-world markets, Carbon Credits.

A multi-trillion-dollar global industry is moving toward digital infrastructure… and GCXP is positioned at that intersection.

✅ First environmental blockchain-focused vision

✅ Built around carbon credit marketplace utility

✅ Real-world asset (RWA) exposure

✅ Global environmental demand blockchain speed

✅ Utility beyond speculation

Carbon credits are becoming a major global conversation, and GCXP gives investors access to that momentum through blockchain.

While many crypto projects chase hype… GCXP is focused on real utility tied to a growing environmental market.

🌱 Blockchain Carbon Credits Real Utility = GCXP

Website: greenrycoin.com

Buy: tinyurl.com/usdcGCXP

CA: 0x13b4e3deb676E3ceca7b78C4c87d8DB071673712

#GCXP #CarbonCredits #RWA #Crypto #ERC20 #Blockchain #GreenCrypto

26

11

42

3,660

📰 $SDA in the headlines.

Our Coinstore Pizza Day × FIFA 2026 campaign was picked up by Benzinga, GlobeNewswire & Finbold — plus a dedicated Coinstore feature on SDA.

Trade-to-win runs through Jul 19.

Read → coinstore.medium.com/sda-tur…

49

🍕⚽ $SDA on Coinstore — Pizza Day × FIFA 2026 trade-to-win is live.

May 20 → Jul 19. Rewards every round: BTC predictions, photo & social drops.

Open Coinstore → Trade → Play → Earn.

coinstore.com/spot/SDAUSDT

142

🍕⚽ $SDA on Coinstore — Pizza Day × FIFA 2026 trade-to-win is live.

May 20 → Jul 19. Rewards every round: BTC predictions, photo & social drops.

Open Coinstore → Trade → Play → Earn.

coinstore.com/spot/SDAUSDT

1

1

99

Sustainable Digital Assets retweeted

May 26

Chilling with a pizza and watching the charts! Celebrating Bitcoin Pizza Day with CoinStore. 🍕📈

UID: 36310276300907604

#Coinstore #BitcoinPizzaDay #SDA #HBOX

1

1

65

Sustainable Digital Assets retweeted

May 26

Bitcoin once turned pizza into history. Today my Pizza Day moment is simple: charts open, coffee ready, pizza beside me, and waiting for the market to write its next story 🍕⚡️

UID: 36310276299536520

1

1

60