I own only 1 stock at a time and try to dive deep as much as I could on that 1 stock. A risk taker, but also a very cautious one.

Joined February 2021

- Tweets 337

- Following 557

- Followers 2,054

- Likes 542

44 Photos and videos

$SOFI trading up 3.4% amid market red is unusual. Does this prove the sector rotation is coming soon? Read my article 👇

Jun 10

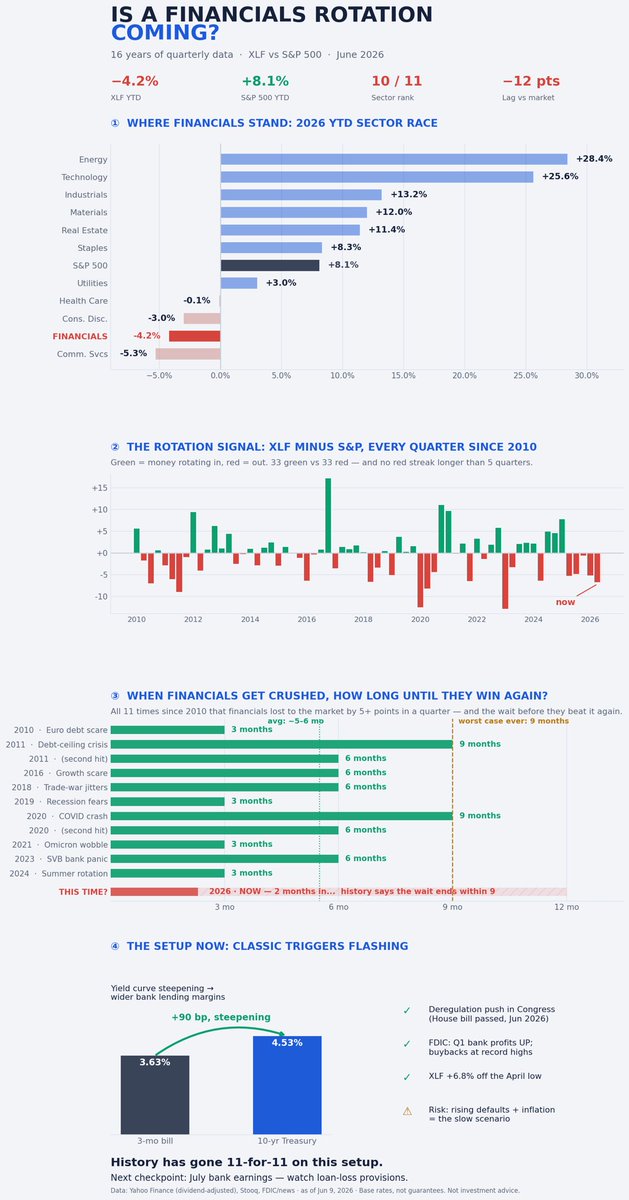

Financials are the 2nd-worst S&P sector YTD: XLF −4.2% vs SPY 8.1%.

But here's the stat nobody talks about -- History says that's exactly when the rotation clock starts ticking:

• Longest XLF losing streak since 2010: 5 quarters

• After every 5 pt lag quarter: outperformance within 1–3 quarters (11/11)

• Yield curve 90bp and steepening — the classic bank tailwind

When the market rotates next, history puts financials at the front of the queue. Here's the full breakdown, plus the 4 signals to watch for confirmation

Check out my article here 👇

$XLF $SOFI $NU

1

363

Seeking Value retweeted

Jun 11

Financial sector ranks 10 of 11 YTD.

Price down fundamentals up catalysts live = the exact setup that preceded all 11 financials snap-backs since 2010.

None took longer than 9 months. We’re 2 months in.

The rotation isn’t a question of if. On 16 years of data, it’s a question of which quarter.

Full data 👇

$XLF $SOFI $NU $HOOD

1

1

417

Seeking Value retweeted

Jun 10

Financials are the 2nd-worst S&P sector YTD: XLF −4.2% vs SPY 8.1%.

But here's the stat nobody talks about -- History says that's exactly when the rotation clock starts ticking:

• Longest XLF losing streak since 2010: 5 quarters

• After every 5 pt lag quarter: outperformance within 1–3 quarters (11/11)

• Yield curve 90bp and steepening — the classic bank tailwind

When the market rotates next, history puts financials at the front of the queue. Here's the full breakdown, plus the 4 signals to watch for confirmation

Check out my article here 👇

$XLF $SOFI $NU

1

5

996

Seeking Value retweeted

May 22

Great conversation. Appreciate how much time you spend on @Sofi . Thank you @stevenfiorillo and @amitisinvesting for having me on @basispointpod!

May 22

It was a pleasure to sit down with the CEO of $SOFI @anthonynoto to discuss the future of SOFI on @basispointpod. Thank you Anthony for taking the time!

84

110

1,416

288,947

Seeking Value retweeted

May 22

$SOFI

"Does it bother me the stock is down as much as it is year to date? Yeah, it f****** bothers me a ton. At the end of the day, we're being held to a high standard. I've accepted that responsibility and I'll work my butt off to make sure we deliver on it."

108

165

2,008

1,446,040

Mar 25

$SOFI Bullish 🚀🚀

Mar 24

BIG NEWS FOR $SOFI

If the Clarity Act closes the yield loophole on stablecoins, the market might be missing who actually wins from that and it’s not the obvious names.

Right now, $CRCL makes most of its money from USDC reserves sitting in short-term Treasuries.

If the bill limits the ability to pass yield to users, that model becomes less attractive, and the competitive edge shifts to banks that already have direct access to the Fed.

That’s where $SOFI Technologies gets interesting.

Because SoFi is a nationally chartered bank, it can hold reserves directly at the Federal Reserve instead of relying on Treasury portfolios.

That means it earns Interest on Reserve Balances (IORB), which is structurally different from stablecoin yield.

Here’s the key part most people miss:

• The bill targets passive yield paid on stablecoins

• It does NOT fully block usage-based rewards, fee reductions, or banking incentives

• Banks with Fed access can repackage yield as benefits instead of calling it yield

$SOFI could do things $CRCL cannot:

•Lower transaction fees

•Offer cashback-style rewards

•Give better savings / checking incentives

•Bundle stablecoin with banking products

•Capture spread from IORB without violating the law

That turns regulation into a moat. If this version of the bill survives, the stablecoin market may shift from

crypto issuers to regulated banks

And in that scenario, SoFi is competing with the entire banking system, with a tech stack built for it.

4

486

Seeking Value retweeted

Mar 23

Holy sh*t

The MW CEO was just destroyed by CNBC on his $SoFi short report

39

22

420

145,941

Mar 17

Good for $SOFI home loan business 🚀

Mar 17

THE AMERICAN DREAM.

President Donald J. Trump signs two executive orders to help American citizens achieve the dream of homeownership. 🇺🇸

1

417

Mar 3

FRAME THIS $SOFI 🚀

Mar 3

.You are guessing. You don't know because you haven't asked. No need to guess you can ask me. There is only one reason I buy SoFi it's because I think it's a great risk reward DESPITE the concentration. I am a blue color kid from Poughkeepsie and no matter how much money I have $1 million is a ton of money and I have a thousand other ways to spend it or use it that would be meaningful and impactful to people and organizations that are near and dear to me and my family. BTW a prepaid forward is not a sale it's a way to finance liquidity. I can roll it forward each time before expiration if i want (many times) and keep participating in the upside and not resulting in a sale and tax event. Look at the price point of the ceiling and that might make you more informed about how I think about value in a given time period. No need to guess it's all researchable and when you can't find the answers just ask me. And Going forward I will correct your mistakes. This time I will give you the benefit of the doubt. WDW

2

549

Mar 3

Thank you sir! @anthonynoto 🫡

- $SOFI shareholders -

Mar 2

I can picture @anthonynoto buying $SOFI like crazy right now loll. We're so back! 🚀🚀

1

748