139 Photos and videos

slyvando retweeted

Jun 15

$SPY following my pattern

Got the expected pop over the weekend ❤️

They flipped all those orders sitting at $743 to buyers.

And yes I believe a pullback comes, maybe not as low as shown in this chart.

Happy Monday

Patterns data

26

72

305

26,552

slyvando retweeted

Jun 14

I’ve been a Knicks fan since 2011.

Many of you know this seeing the variation of Knicks hats I wear on stream.

I was born in NJ so our local cable package at the time only came with MSG Sports.

The only basketball games they showed were the Knicks, the New Jersey Nets weren’t really good enough to get their own station, so I ended up deciding I’d be a Knicks fan at the same time that I began playing basketball in Middle School. I grew up with Carmelo, Jeremy Lin, Steve Novak, etc. I quickly realized being a Knicks fan was not going to be fun.

I don’t talk much about sports anymore because over the past 10 years, I shifted my focus from sports to markets when I realized I wasn’t going to ever make the NBA. I just couldn’t dedicate the type of energy to caring about sports when I realized my core focus was going to shift on becoming a better investor. Jerome Powell became more relevant to me than LeBron James.

But last night was special.

I started crying on the couch when seeing Jalen Brunson win (which my sister made fun of me for) but it’s because Brunson is the epitome of never giving up and continuing to fight in the face of everyone doubting you.

“My confidence comes from my work ethic,” was the part that hit me the hardest that he said last night. It is a reminder that anything in life can be achieved if you are willing to do the work that most people cannot fathom doing.

And when you put in that work, the confidence in the big moments is just a reflection of all the time you put in.

Really happy for the City of New York and for a team for inspiring all of us to dream as big as possible.

99

26

1,231

83,608

slyvando retweeted

Jun 9

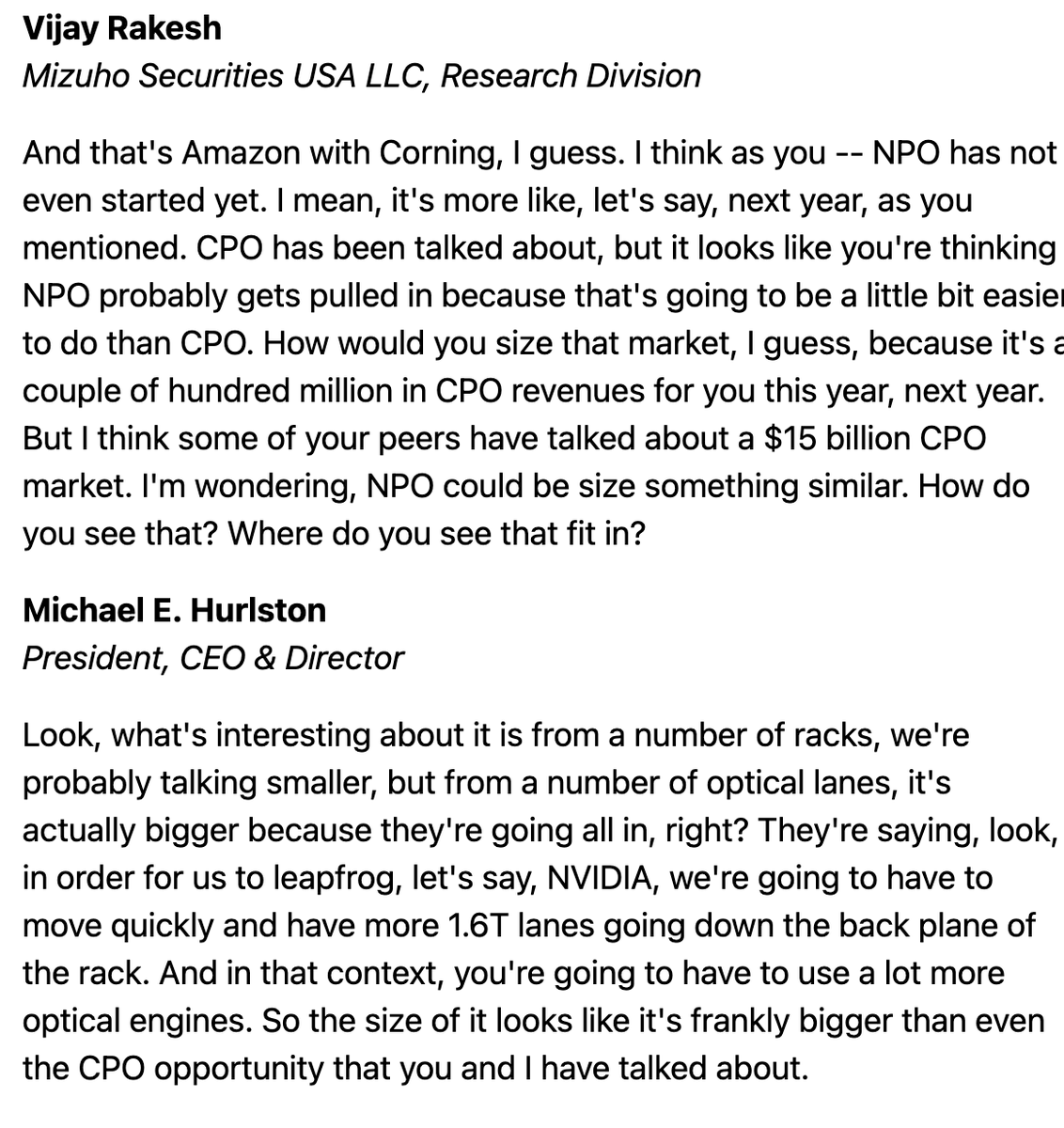

$LITE My own key takeaways from Lumentum’s fireside chat at the Mizuho Technology Conference is that the optical cycle still appears to be early in its architectural expansion.

This connects directly to the central argument in our recent connectivity article: connectivity is not one product category sitting next to compute. It is becoming part of the architecture that determines how efficiently compute can actually scale.

This is no longer just an 800G transceiver story. The opportunity is broadening across 1.6T, scale-up, NPO, CPO and optical circuit switching, while laser and InP capacity remain tight.

What stood out to me is that these architectures are not replacing one another. They are being added on top of an already strong base business. Scale-out keeps growing, scale-up pulls more optics inside and between racks, NPO may arrive before full CPO adoption, and OCS is developing into a separate opportunity around resiliency and traffic management.

That is exactly what we argued in the article (After Memory, I Am Watching Connectivity). As systems become denser, connectivity carries more of the burden. More bandwidth, lower latency, higher reliability and better power efficiency become architectural requirements rather than optional upgrades.

The more concrete bullish read-through for $LITE is that management indicated new NPO opportunities are already absorbing added capacity. At the same time, the recent margin improvement has been driven mainly by pricing and product mix rather than cost cutting.

That matters because it suggests Lumentum is not simply participating in higher volumes. The company is starting to capture better economics as the bottleneck moves deeper into high-performance lasers, optical components and switching.

It also makes the case less dependent on one architecture winning. If NPO develops faster than CPO, Lumentum participates. If scale-up becomes more optical, Lumentum participates. If OCS grows into a much larger market, Lumentum participates there as well.

This is why I still read the cycle as early. Optical content per system is rising, the number of use cases is expanding, and much of the qualified capacity needed to support the transition is still being built.

I read the discussion as strengthening both the $LITE thesis and the broader connectivity thesis. The architecture is becoming more optical, the economics are improving, and Lumentum appears positioned across several of the layers that will matter as the next generation of AI systems is built.

Another bullish nugget from $LITE's CEO: The NPO opportunity "is frankly bigger than even the CPO opportunity".

Key takeaway: NPO or CPO, either way LITE wins.

2

6

24

6,234

slyvando retweeted

Jun 10

Reload in Sept. #gold

Jan 30

That was an epic two year run for gold. But the juice has been squeezed. On to the next.

55

107

1,180

140,600

slyvando retweeted

Jun 11

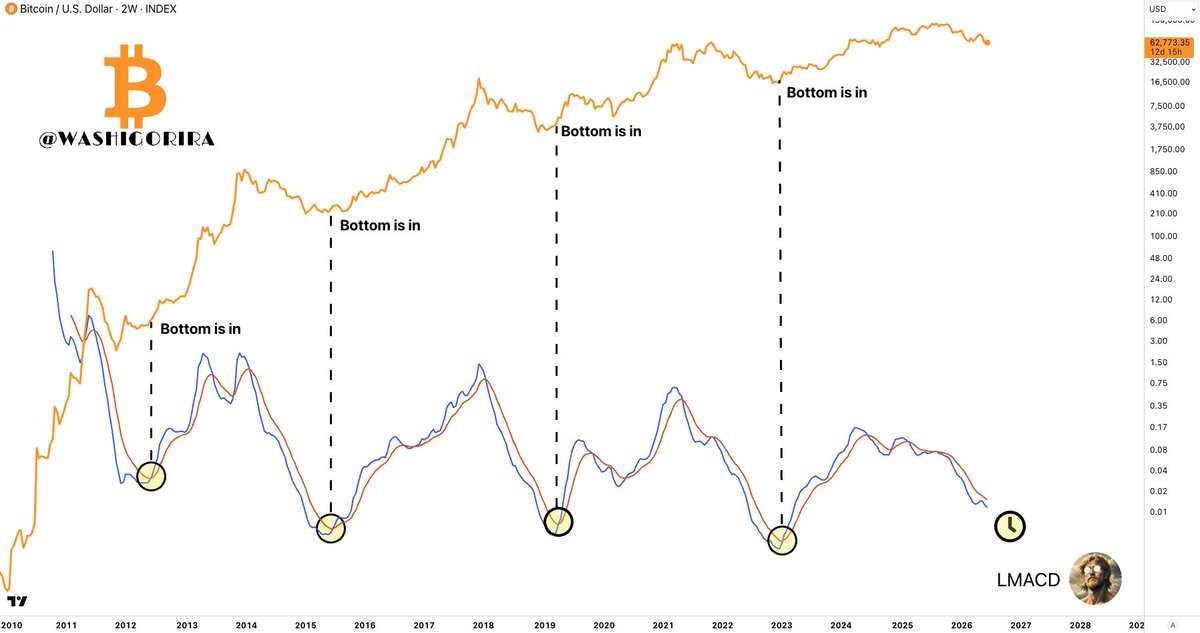

Comparing the current Bitcoin bear market to the last 3 bear markets

162

122

1,767

142,279

slyvando retweeted

Jun 10

78

104

2,450

192,159

slyvando retweeted

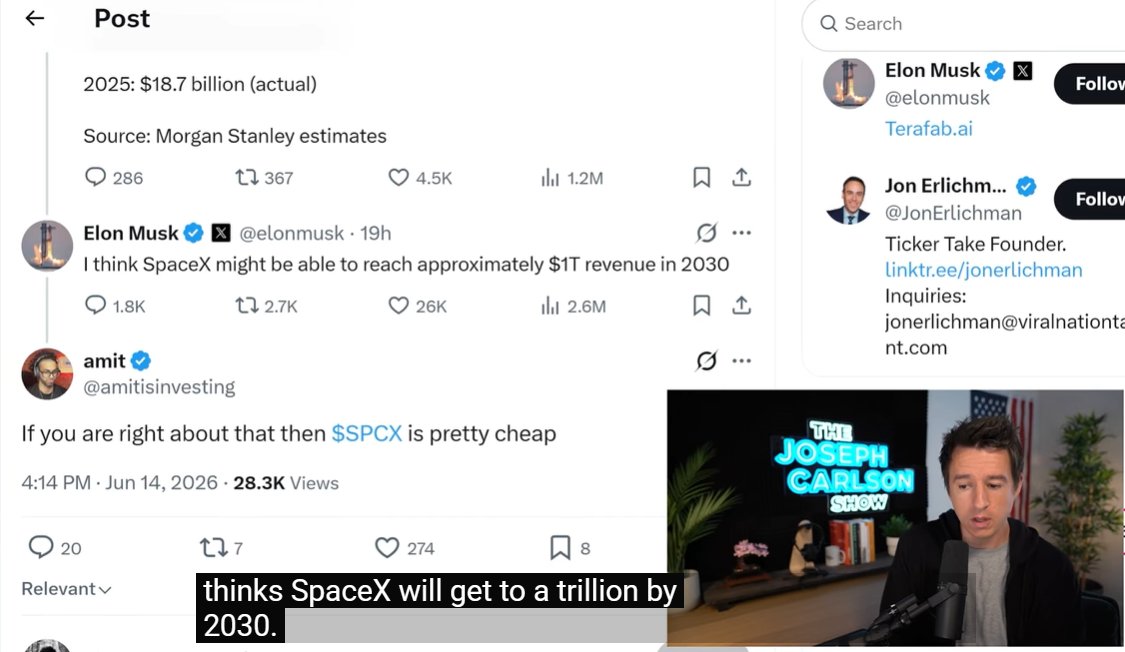

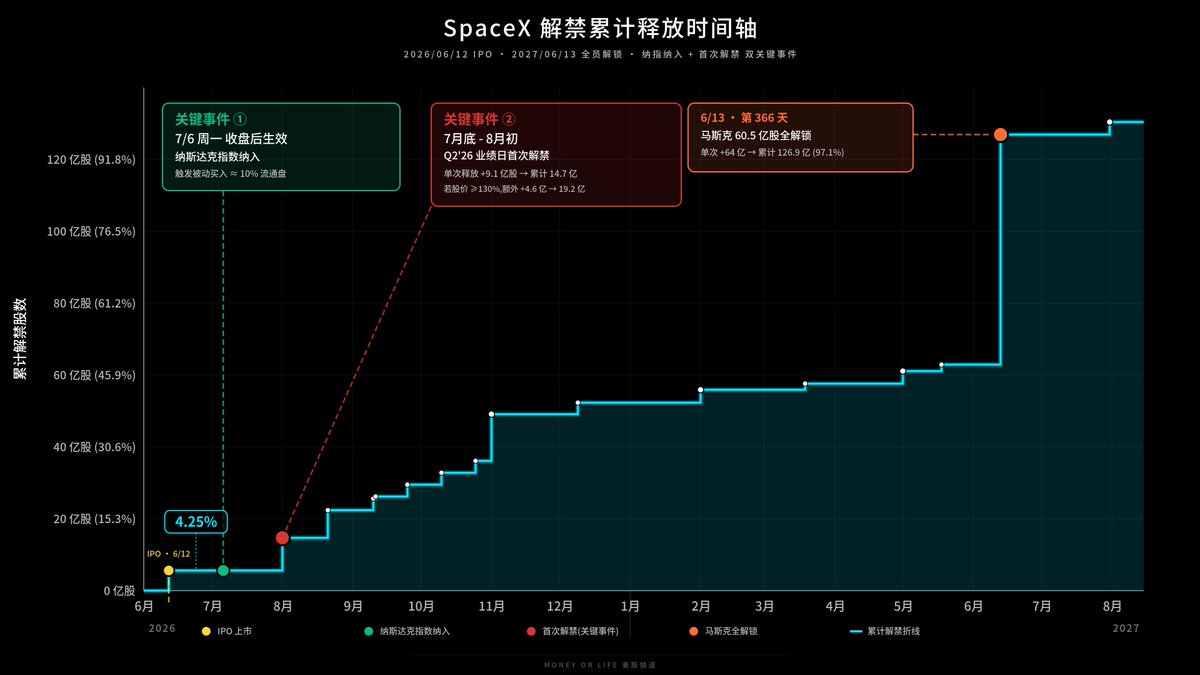

如果要IPO当日投资/投机SpaceX,最重要的一张图。。。

11

13

79

21,475

slyvando retweeted

Jun 9

Most people work for money, validation, or status.

That's the trap.

When your self-worth is tied to your job, every criticism feels like an attack.

Every imperfection feels like failure.

You perform for approval instead of working with purpose.

The shift happens when you find genuine satisfaction in the work itself.

When the mission actually aligns with what you value.

You stop being fragile.

Criticism becomes data, not a verdict.

Perfection stops being the point.

There's a line between commitment and selling yourself — know where it is.

2

12

691

slyvando retweeted

Jun 8

I love the cadence of this chart

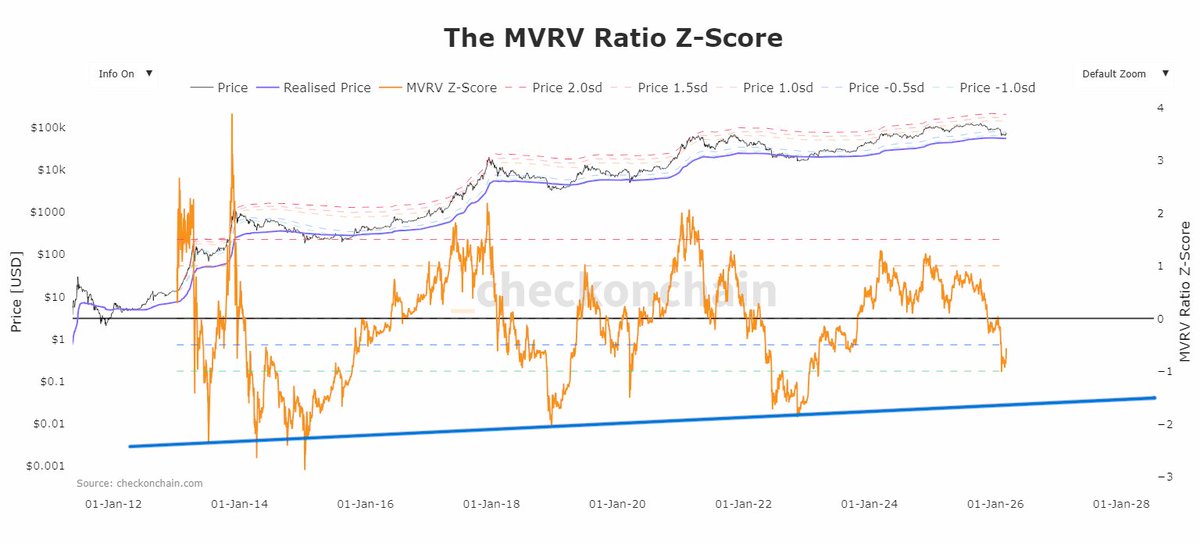

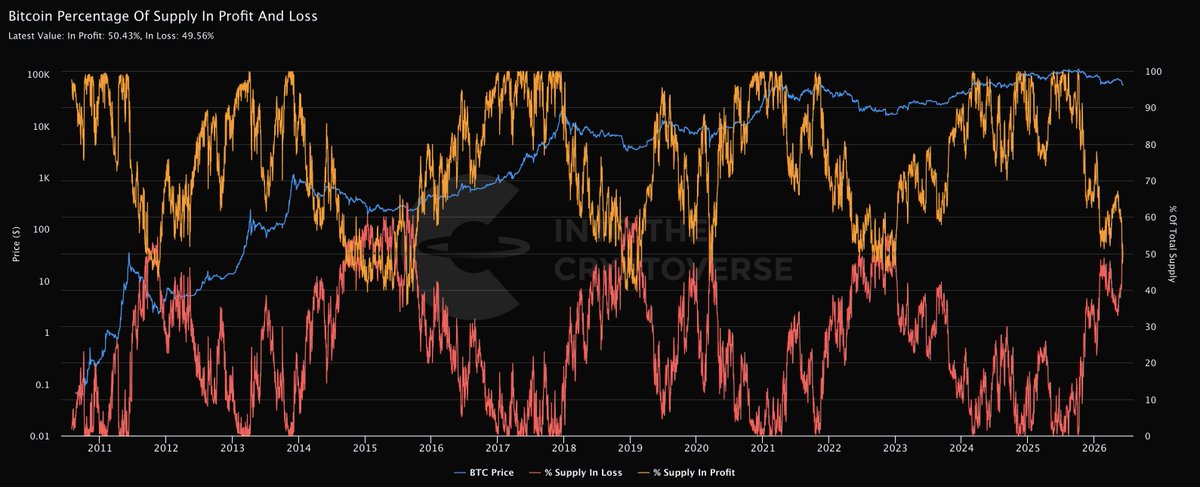

Bitcoin % of Supply in Profit/Loss

As I said previously, you start looking for major market cycle bottoms *after* they cross, not before.

They just crossed.

Such a great chart for keeping people on the right side of the market in midterm years

226

581

5,819

374,258

slyvando retweeted

Jun 8

Genuinely a good time to be a Persona fan.

Just need P1 and P2 remake after all this and its perfect.

59

866

6,445

109,000

slyvando retweeted

Jun 6

I expect the market to be extremely volatile in the lead up to the first Fed meeting by the new chair on 16/17 June.

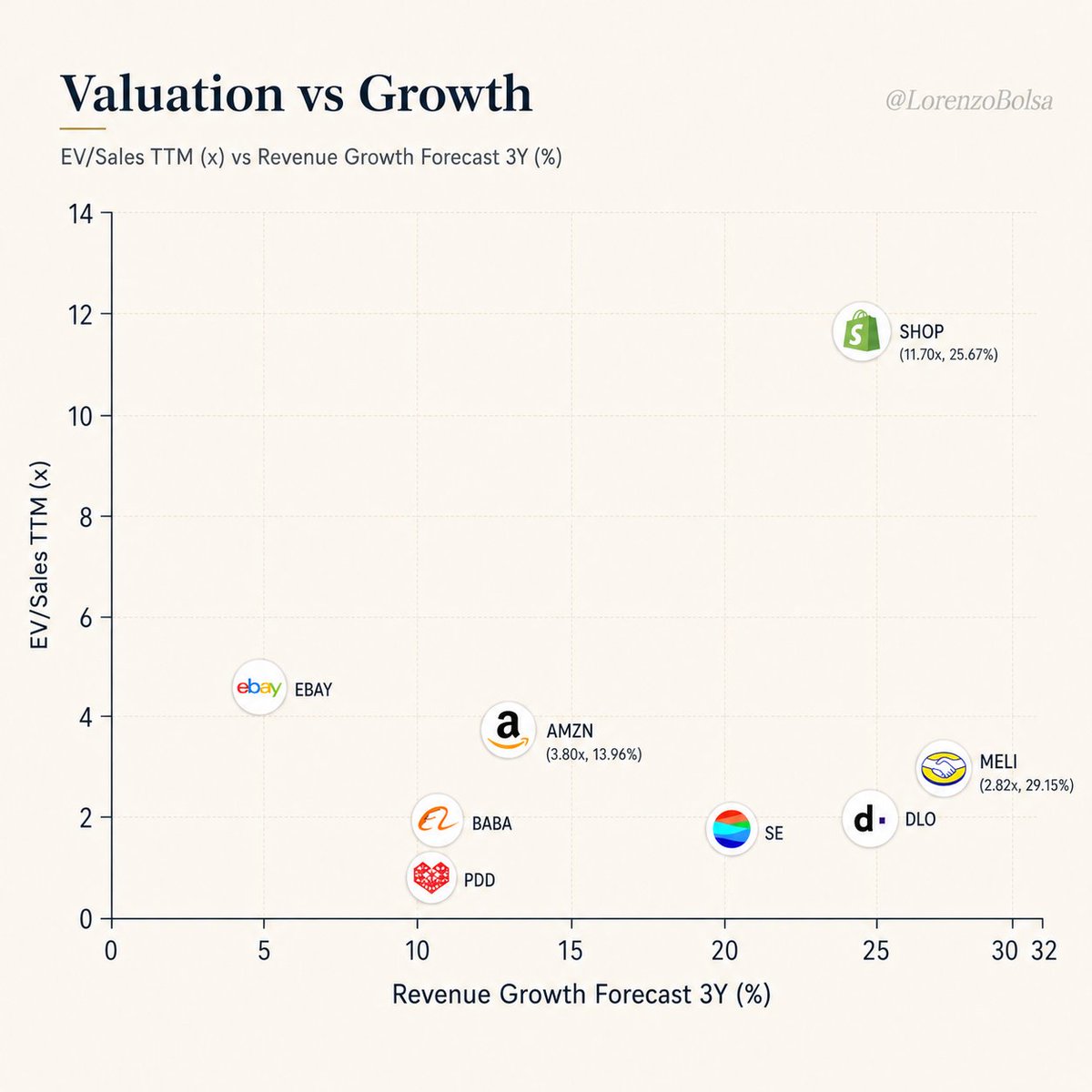

These are the stocks i’m watching and prices I would be glad to add at:

$SE: $77

$GRAB: $3

$GLXY: $20

$NBIS: $173

$HOOD: $69

$FICO: $950

$DLO: $10.70

$RBRK: $64

Jun 6

Shared some musings with subscribers on Thursday that I thought I would share here (summarised version).

I hypothesised that we would see some volatility in the lead up to the Fed meeting on 16/17 June, as the market awaits the rate decision that will come at the conclusion of the meeting.

The key reason being, the Catch-22 that Kevin Warsh faces:

(1) Trump, who put him in the seat, needs rates to come down to stimulate economic growth, boost housing and to offset the financial strain on consumers. This is especially crucial in the lead up to the mid-terms, where Trump would hope to continue holding legislative power and enacting his policies with little opposition.

(2) The economic reality is that geopolitical tensions wrt SoH has pushed headline inflation (PCE) up to 4%. Lowering interest rates now would inject more money into the economy, worsening the inflation crisis and violating the Fed's primary mandate of price stability.

Stock markets also tend to have a "test" for a new Fed Chair, and typically see a drawdown in the first three months after a new Fed Chair is appointed. (Avg drawdown of 12.0% in the 3 months after appointment)

To be clear, my stance is only bearish in the IMMEDIATE term. Markets hate uncertainty and that is what we are currently facing. I believe Warsh will hold rates steady, and markets will breathe a sigh of relief.

These few weeks will be a brilliant opportunity to add to several great companies, of which I will detail in the next post.

5

1

52

8,850

slyvando retweeted

Jun 5

9

13

153

17,487

slyvando retweeted

Jun 5

#Bitcoin Yearly low has been swept ✔️

A price reaction at this level is possible.

If not, the next liquidity pools lie at:

▪️58,900

▪️52,600

▪️49,000

28

63

316

16,037

slyvando retweeted

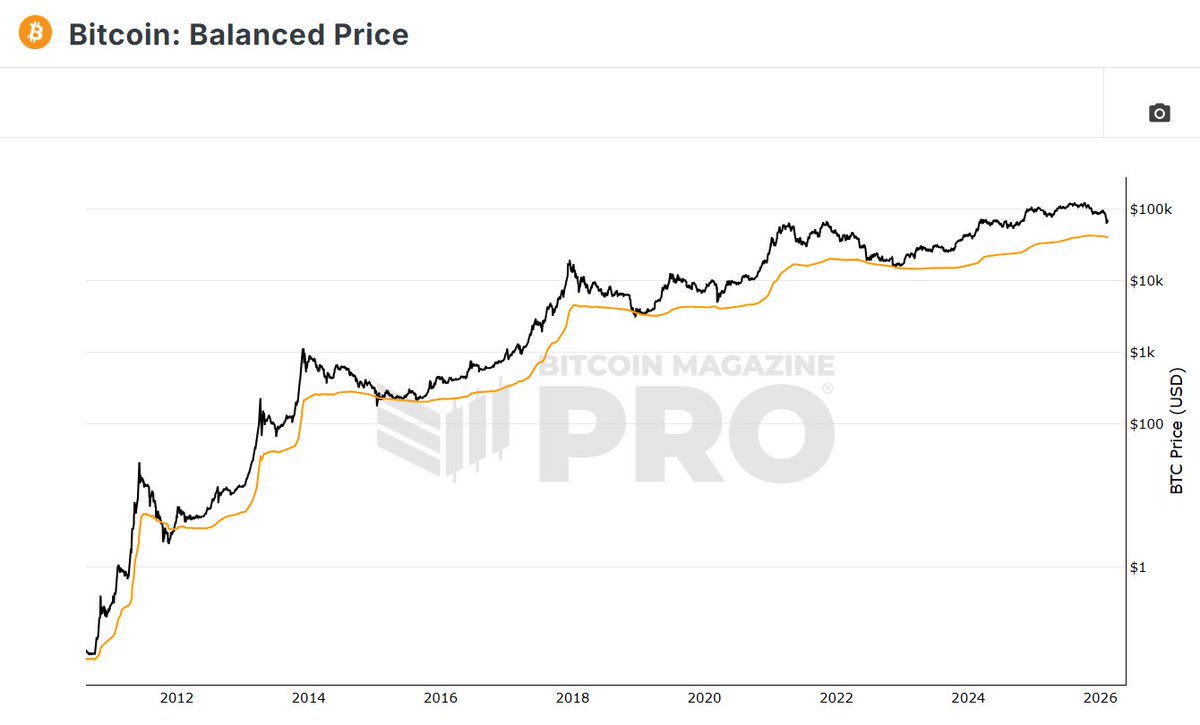

More than half of all $BTC in circulation is now held at an unrealized loss.

10.5M BTC are underwater. Only 9.8M are in profit.

This crossover has coincided with every major bear market bottom in history.

BTC also just touched its 200-week moving average at $61,300, a level reached in every previous bear market cycle, though it broke below it for 9 months in 2022.

If $60k breaks, the next support is $54,000, the average cost basis of every coin in circulation.

History says we're near a bottom. History also says "near" can take a while.

95

136

1,294

58,122

slyvando retweeted

Jun 2

Plausible path:

Bitcoin forms a low in June (like it did in June 2018 and June 2022).

BTC rallies in July

SPX correction later in year which allows Bitcoin to finally bottom (most likely October)

Four year cycle wins again

281

603

6,939

346,152