Interested in all things Tech. Startups in emerging markets: Africa 🌍 and Middle East.

Joined November 2009

- Tweets 23,299

- Following 4,464

- Followers 2,564

- Likes 2,410

1,670 Photos and videos

Jun 2

Youssef is asking for help to save his mother’s vision as she faces a rare eye disease that’s already caused permanent damage. gofund.me/5b3d9d0b4

3

4

92

Sherif Nessim retweeted

19 Feb 2025

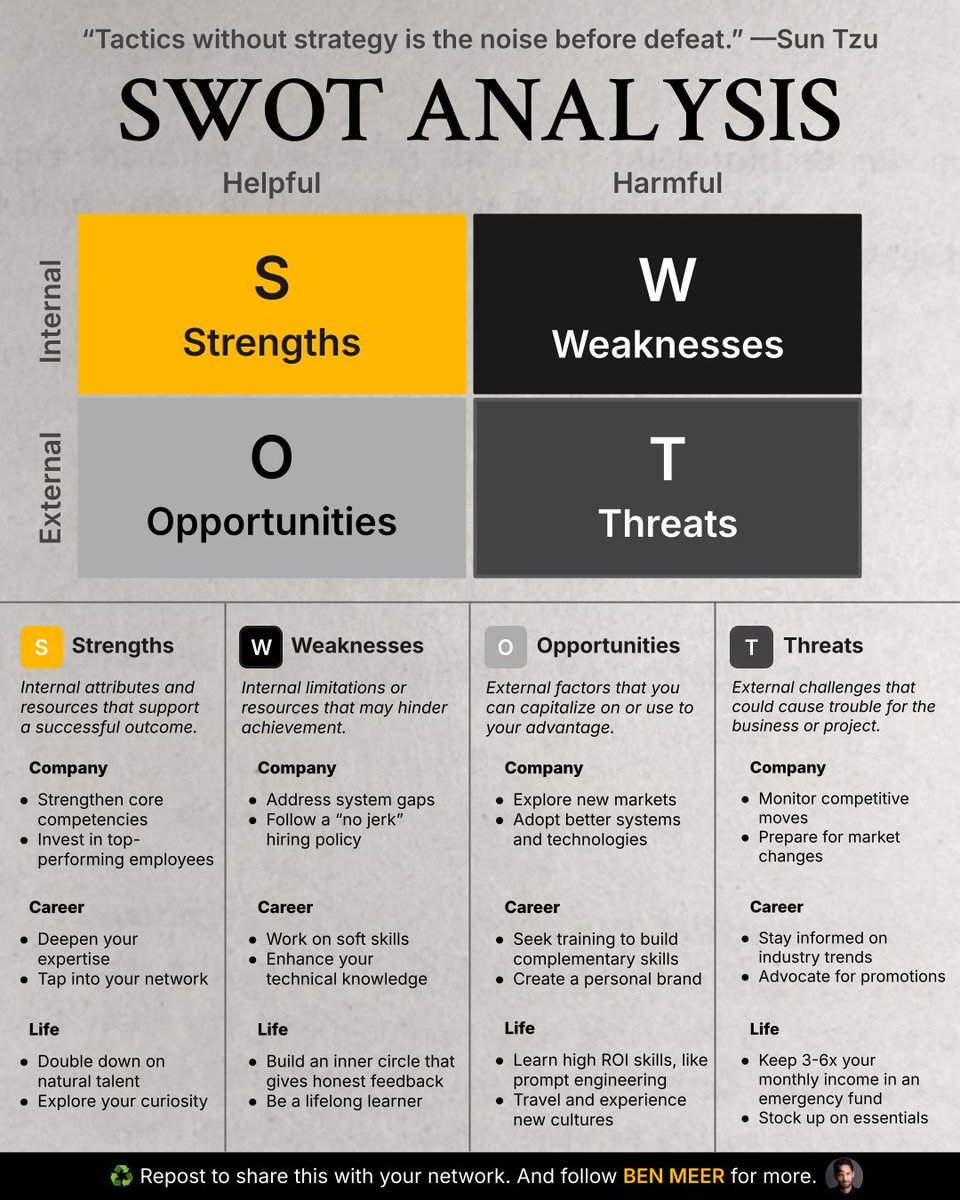

Strategic thinking is a superpower.

Use SWOT analysis to stay ahead:

20

310

1,383

161,492

Sherif Nessim retweeted

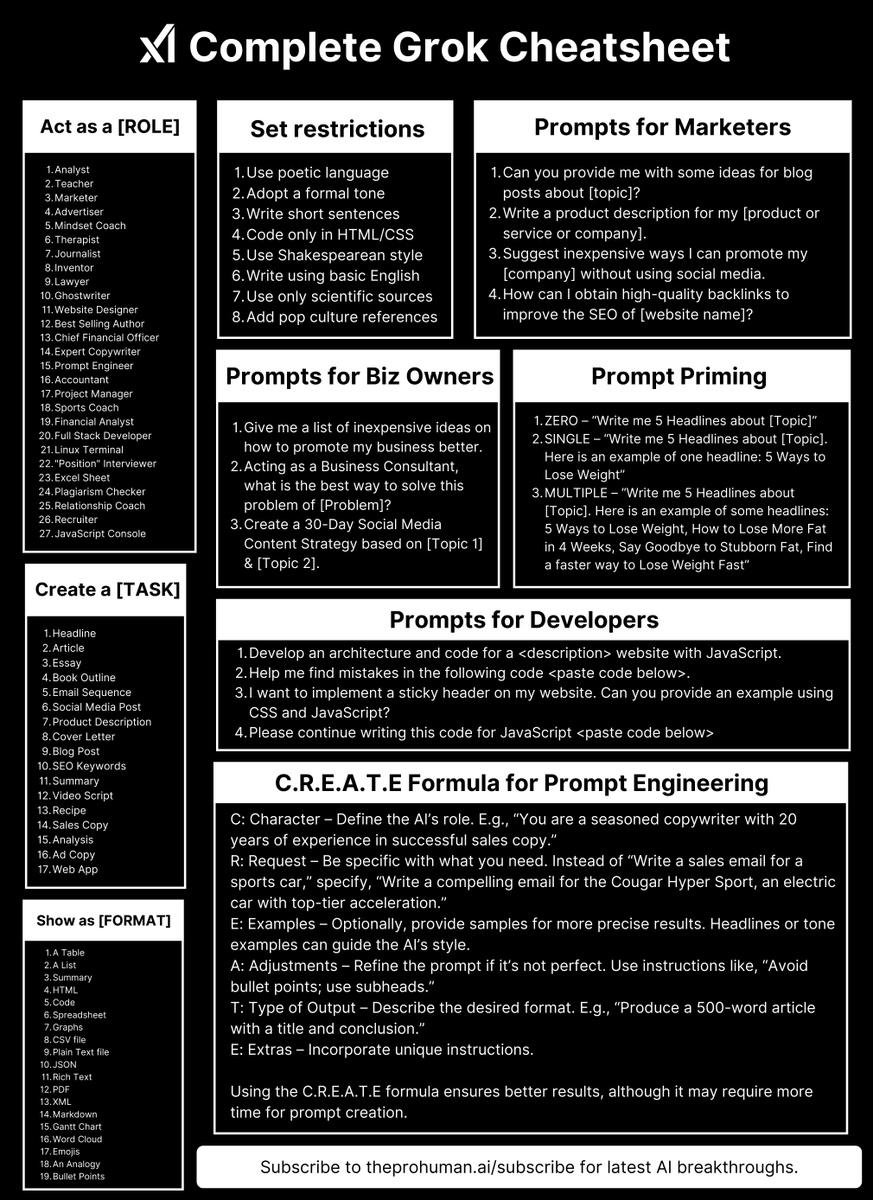

19 Feb 2025

Grok 3 is insanely powerful 🔥

But most people don't know how to use it effectively.

Here's a complete cheatsheet to unlock Grok's full potential and automate your tasks with it:

59

313

1,558

255,929

Sherif Nessim retweeted

10 Feb 2025

Applications for the 2026 #ZayedSustainabilityPrize are now open!

We recognise organisations and high schools with bold, sustainable solutions that transform lives

Every solution counts.

Apply today: entry.zayedsustainabilitypri…

#PowerOfProgress

103

243

5,472

51,727,338

Sherif Nessim retweeted

18 Feb 2025

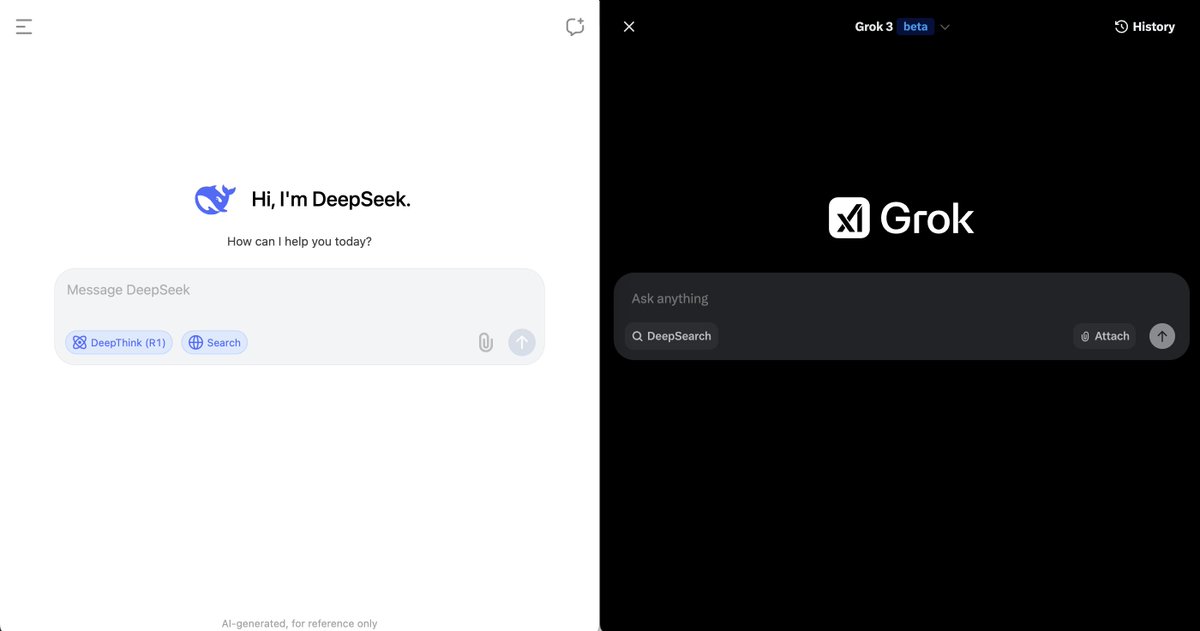

I tested Grok 3 and DeepSeek v3 with same critical prompts.

The results will blow your mind.

Grok 3 Vs. DeepSeek v3

(Video demos are included)

155

515

4,228

1,109,510

Sherif Nessim retweeted

19 Feb 2025

Beyond beyond. People just not seeing the bigger picture yet — tech is way way beyond what you see and hear out there. AGI in under 100 days. ASI in under 2yrs. Total technical and economic recreation happening in the next 2-5yrs of your life will be way outside your imagination. What to do? Get healthy, learn to add value, communicate well, and lead others. Mastering your mind, emotions and health, and creating great friendships, families, quests and fellowship are the only autonomous games left in the future. It’s about to get wild friends.

21

40

373

85,137

Sherif Nessim retweeted

19 Feb 2025

Read more about our discovery, and why it matters, here: aka.ms/AAu76rr

273

1,918

11,700

1,208,443

Sherif Nessim retweeted

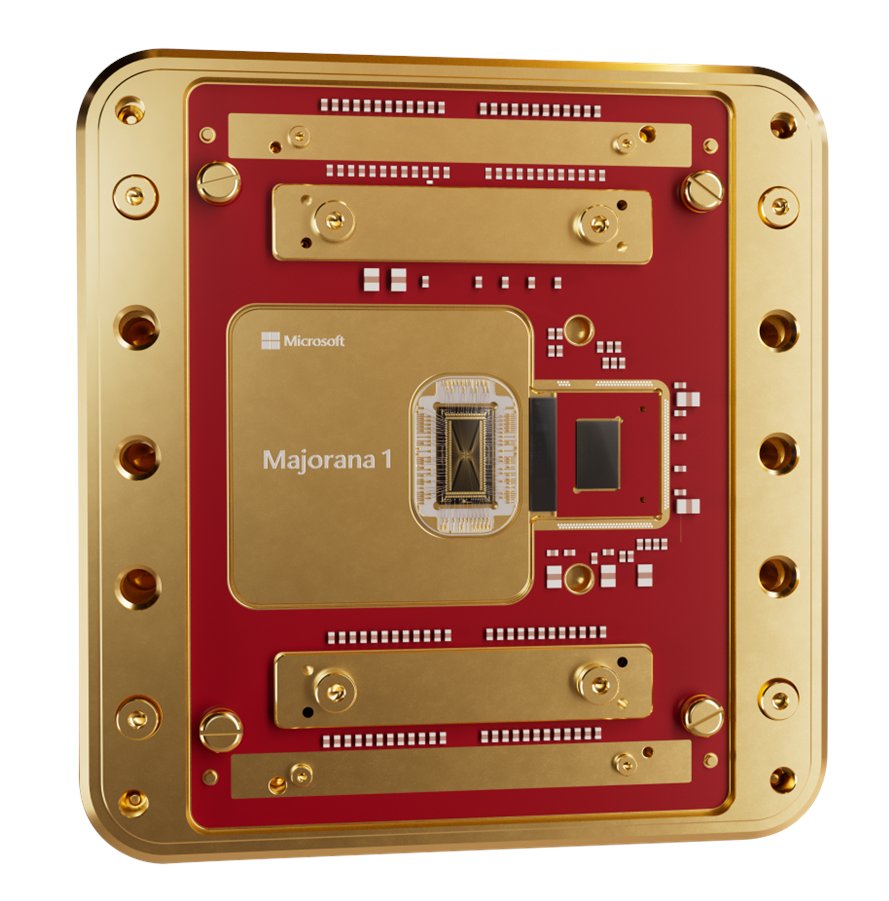

19 Feb 2025

A couple reflections on the quantum computing breakthrough we just announced...

Most of us grew up learning there are three main types of matter that matter: solid, liquid, and gas. Today, that changed.

After a nearly 20 year pursuit, we’ve created an entirely new state of matter, unlocked by a new class of materials, topoconductors, that enable a fundamental leap in computing.

It powers Majorana 1, the first quantum processing unit built on a topological core.

We believe this breakthrough will allow us to create a truly meaningful quantum computer not in decades, as some have predicted, but in years.

The qubits created with topoconductors are faster, more reliable, and smaller.

They are 1/100th of a millimeter, meaning we now have a clear path to a million-qubit processor.

Imagine a chip that can fit in the palm of your hand yet is capable of solving problems that even all the computers on Earth today combined could not!

Sometimes researchers have to work on things for decades to make progress possible.

It takes patience and persistence to have big impact in the world.

And I am glad we get the opportunity to do just that at Microsoft.

This is our focus: When productivity rises, economies grow faster, benefiting every sector and every corner of the globe.

It’s not about hyping tech; it’s about building technology that truly serves the world.

Community note

Microsoft's supporting paper, published in Nature, does not support the claim that they have created a topological qubit. nature.com/articles/s4158…

Peer reviewers of the Nature paper expressed concern that the paper misleadingly implies that a topological qubit was demonstrated or otherwise achieved: static-content.springer.com/esm/art:10.1…

5,119

18,341

104,972

27,154,110

Sherif Nessim retweeted

15 Feb 2025

الصحافي بشبكة العربية وسام كيروز: ترمب سياسي ماهر ومن الخطأ التقليل من الجانب السياسي لديه

#ترمب

#أميركا

#الأسبوع_وما_بعد

#قناة_العربية

1

1

9

10,707

Sherif Nessim retweeted

8 Feb 2025

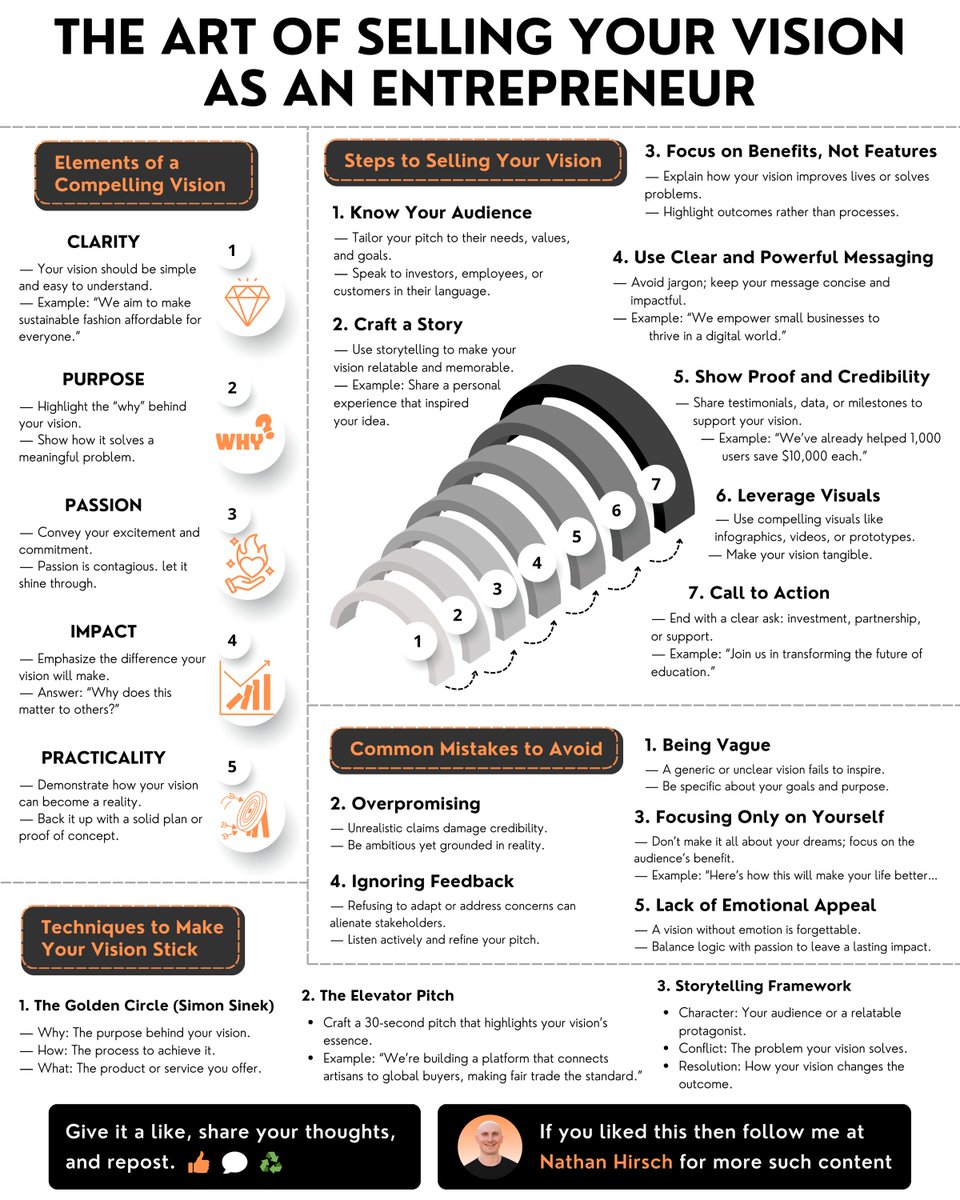

You fail as an entrepreneur if you can't sell your vision

Jeff Bezos didn't start Amazon to sell books, he sold the vision of an online world

Richard Branson sold the vision of a customer-centric airline, not just flights

Here’s how to sell your vision with clarity and impact:

15

167

914

111,649

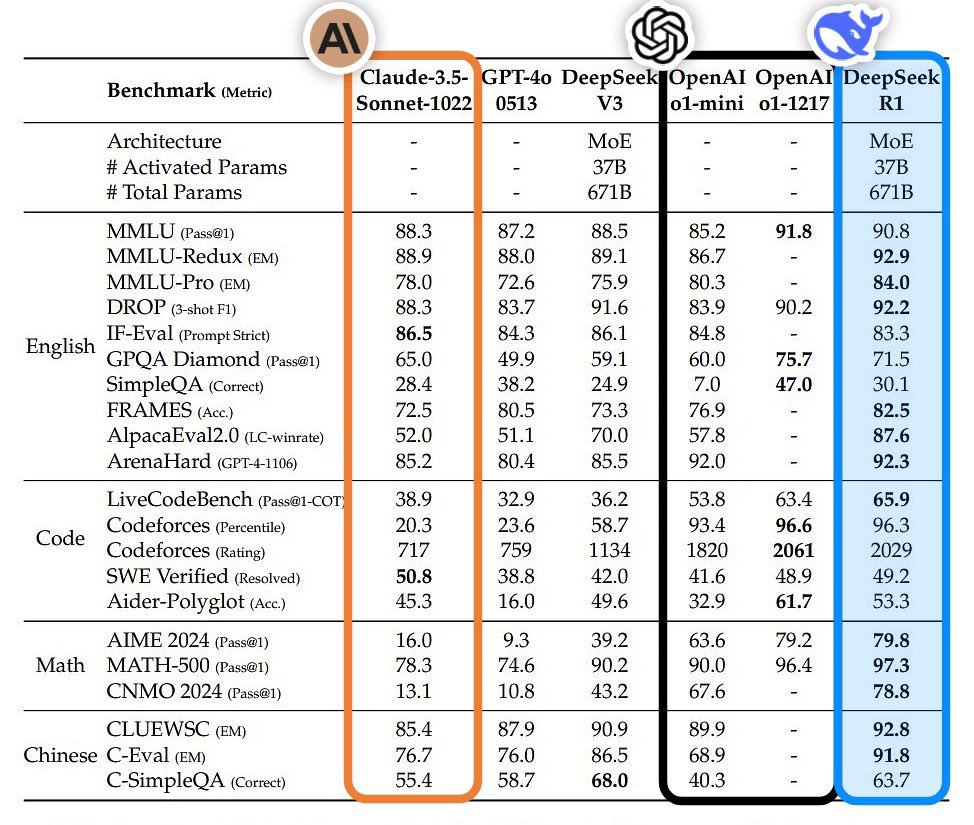

DeepSeek-R1 just released.

Fully open source & transparent with MIT license.

Developed with reinforcement learning directly on the base model.

20-30x cheaper API at comparable performance to OAI’s o1.

(USD)

0.14 / million input tokens (cache hit).

0.55 / million input tokens (cache miss).

2.19 / million output tokens.

To simplify, R1 is like R1-Zero but with multi-stage training:

Its pipeline:

• Fine-tune base with CoT data points

• RL stage similar to R1-Zero

• SFT using ~600k data points from rejection sampling and supervised datasets (e.g., writing, self-cognition).

• RL stage to optimise objectives: helpfulness, harm reduction, etc.

Emergent properties like longer responses, reflection, and alternative exploration emerge as natural products during training without explicit programming.

RL rewards focus:

• Accuracy (e.g., unit test-based scoring for code).

• Format (e.g., tags for reasoning separation and language consistency).

No outcome/process RMs used (simpler).

22

455

2,236

543,777

The team at @nayaplatform and @SherifKozman have verified several reasons behind the shortfall at @getevolved1925. Evolve, if there’s nothing to hide, open source the data—let the public and independent experts like Naya validate or disprove the claims.

9 Dec 2024

🚨 𝗧𝗟;𝗗𝗥 𝗦𝘂𝗽𝗽𝗼𝗿𝘁𝗶𝗻𝗴 𝗧𝗿𝗮𝗻𝘀𝗽𝗮𝗿𝗲𝗻𝗰𝘆: 𝗡𝗔𝗬𝗔'𝘀 𝗘𝗳𝗳𝗼𝗿𝘁 𝗶𝗻 𝘁𝗵𝗲 𝗦𝘆𝗻𝗮𝗽𝘀𝗲-𝗘𝘃𝗼𝗹𝘃𝗲 𝗖𝗮𝘀𝗲

At @nayaplatform , we believe that transparency is the foundation of trust in the financial services industry. That’s why we stepped forward to offer our assistance in reconciling the data between Synapse and their banking partners, including Evolve, Lineage, and AMG.

Without access to Synapse's internal ledger, achieving accurate reconciliation is challenging. However, based on the data provided by Synapse CEO @sankaet , in the form of bank statements from Evolve, we were able to extract and calculate charges and fees imposed by Evolve on Synapse.

Here’s what we uncovered from the provided data:

- 𝗗𝗙𝗲𝗲𝘀: $13.8M

- 𝗔𝗰𝗰𝗼𝘂𝗻𝘁 𝗔𝗻𝗮𝗹𝘆𝘀𝗶𝘀 𝗖𝗵𝗮𝗿𝗴𝗲𝘀: $12.4M

- 𝗢𝘃𝗲𝗿𝗱𝗿𝗮𝗳𝘁 𝗖𝗵𝗮𝗿𝗴𝗲𝘀: $757K

- 𝗖𝗵𝗲𝗰𝗸 𝗔𝗺𝗼𝘂𝗻𝘁𝘀: $6.59M

- 𝗥𝗗𝗖 𝗔𝗱𝗷𝘂𝘀𝘁𝗺𝗲𝗻𝘁𝘀 𝗮𝗻𝗱 𝗙𝗲𝗲𝘀: $38M , including Fed Adjustments and Encoding Errors.

We hope these insights contribute to shedding some light on the situation and fostering productive discussions. At NAYA, we remain committed to supporting the resolution of this matter, as it’s crucial for the industry’s transparency and impacts everyone—from fintech companies to consumers.

We remain committed to transparency and the work necessary with all parties to validate or disprove the remaining allegations with regards to reconciliation.

To proceed, we request further data from the Synapse estate and Evolve Bank to complete the reconciliation.

Let’s work together to build a more transparent financial ecosystem.

𝗗𝗶𝘀𝗰𝗹𝗮𝗶𝗺𝗲𝗿: NAYA's analysis is based solely on the provided data and does not verify its authenticity. Our goal is to remain an independent, neutral party supporting industry-wide governance.

#Fintech #Reconciliation #Transparency #FinancialGovernance

1

3

18

3,672

Sherif Nessim retweeted

9 Dec 2024

🚨 𝗧𝗟;𝗗𝗥 𝗦𝘂𝗽𝗽𝗼𝗿𝘁𝗶𝗻𝗴 𝗧𝗿𝗮𝗻𝘀𝗽𝗮𝗿𝗲𝗻𝗰𝘆: 𝗡𝗔𝗬𝗔'𝘀 𝗘𝗳𝗳𝗼𝗿𝘁 𝗶𝗻 𝘁𝗵𝗲 𝗦𝘆𝗻𝗮𝗽𝘀𝗲-𝗘𝘃𝗼𝗹𝘃𝗲 𝗖𝗮𝘀𝗲

At @nayaplatform , we believe that transparency is the foundation of trust in the financial services industry. That’s why we stepped forward to offer our assistance in reconciling the data between Synapse and their banking partners, including Evolve, Lineage, and AMG.

Without access to Synapse's internal ledger, achieving accurate reconciliation is challenging. However, based on the data provided by Synapse CEO @sankaet , in the form of bank statements from Evolve, we were able to extract and calculate charges and fees imposed by Evolve on Synapse.

Here’s what we uncovered from the provided data:

- 𝗗𝗙𝗲𝗲𝘀: $13.8M

- 𝗔𝗰𝗰𝗼𝘂𝗻𝘁 𝗔𝗻𝗮𝗹𝘆𝘀𝗶𝘀 𝗖𝗵𝗮𝗿𝗴𝗲𝘀: $12.4M

- 𝗢𝘃𝗲𝗿𝗱𝗿𝗮𝗳𝘁 𝗖𝗵𝗮𝗿𝗴𝗲𝘀: $757K

- 𝗖𝗵𝗲𝗰𝗸 𝗔𝗺𝗼𝘂𝗻𝘁𝘀: $6.59M

- 𝗥𝗗𝗖 𝗔𝗱𝗷𝘂𝘀𝘁𝗺𝗲𝗻𝘁𝘀 𝗮𝗻𝗱 𝗙𝗲𝗲𝘀: $38M , including Fed Adjustments and Encoding Errors.

We hope these insights contribute to shedding some light on the situation and fostering productive discussions. At NAYA, we remain committed to supporting the resolution of this matter, as it’s crucial for the industry’s transparency and impacts everyone—from fintech companies to consumers.

We remain committed to transparency and the work necessary with all parties to validate or disprove the remaining allegations with regards to reconciliation.

To proceed, we request further data from the Synapse estate and Evolve Bank to complete the reconciliation.

Let’s work together to build a more transparent financial ecosystem.

𝗗𝗶𝘀𝗰𝗹𝗮𝗶𝗺𝗲𝗿: NAYA's analysis is based solely on the provided data and does not verify its authenticity. Our goal is to remain an independent, neutral party supporting industry-wide governance.

#Fintech #Reconciliation #Transparency #FinancialGovernance

2

4

12

5,309

Sherif Nessim retweeted

15 Jun 2024

ChatGPT Cheat Sheet:

The Ultimate ChatGPT Guide to Get More Done in Less Time

42

1,980

13,439

3,104,454

Sherif Nessim retweeted

12 Jun 2024

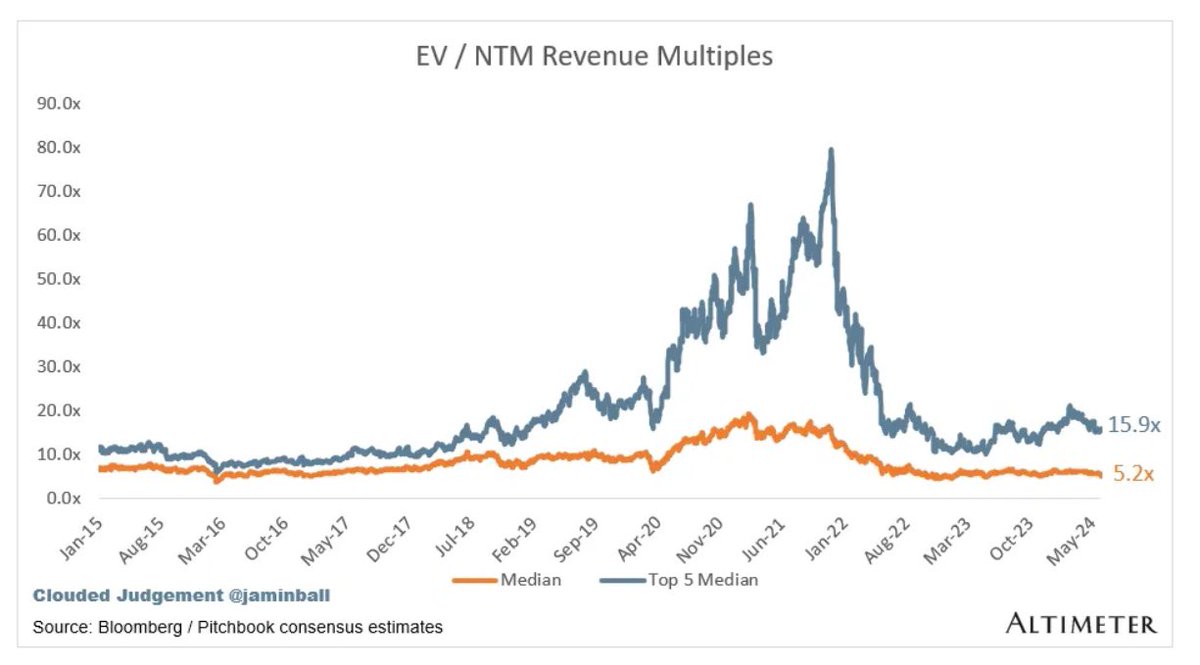

Was at a VC dinner last night where the main topic was the max divergence of public multiples (now 5.2x fwd EV in software and 15.9x for top cos) vs private VC multiples. In AI land we’re back at 2021-era 100x multiples, this time without the elevated public comps. Growth funds are modeling time to “breakeven” from multiple compression at over 2 years with even the most optimistic company forecasts. While there will likely be some number of new generational companies built this cycle, many funds will likely lose $ in the hype, as they had in the 2021 cycle. What will happen from here?

- VC consolidation will continue but slowly. As 2021 era investments eventually become marked to mkt, LP allocations to VC will continue to adjust to pre-2021 era. A couple “index” funds may continue to accumulate capital but otherwise selection and discipline (and ability to invest in the long-term winners) will separate returns

- AI multiples will remain high. In many cases AI companies are raising large rounds because they are demonstrating remarkably fast revenue and user growth. However, retention remains a leading indicator of which products may reach true PMF (eg it is actually helping people do something 10x faster / cheaper / better) vs which are enjoying AI novelty. As soon as a company’s growth declines from 2-3x to <50% many will struggle to raise a next round at such a high watermark. Understandably many are stockpiling funds while they can now

- As we’ve seen from WWDC, in many use cases, incumbents are the largest threat and most likely long-term winner. The M&A market unlocking (post elections) would be a big positive for VC DPIs

24

41

401

193,018

Sherif Nessim retweeted

6 Jun 2024

Master time management:

111

8,975

44,443

9,553,583

Sherif Nessim retweeted

3 Jun 2024

Landing The Plane: A Necessary Choice For Many Startups

How many Founders does it take to land a plane? None, they'll just pivot to a helicopter ride-sharing service.

Joking aside, there’s nothing more fun than being part of an incredibly successful Startup. The relentless ambition of passionate teams doing everything they can to ship code and scale is energizing.

And for most Startups, their goal is to join the ranks of “real” companies by growing large enough to eventually execute a well-received Initial Public Offering. Having their own ticker symbol etched in the annals of Wall Street drives many Founders, and as importantly, IPOs are a critical source of investment returns for the VCs that fuel the startup ecosystem. Without IPOs, VC math doesn’t math!

However, reality is sobering. Only a few percent of all Startups backed by Tier 1 VCs achieve the scale required for a successful public offering, and the numbers are much, much worse for the broader Startup ecosystem. So, what happens when it’s obvious that a Startup isn’t on a trajectory to capture hundreds of millions of dollars of high margin revenue which would allow them to go public?

The unfortunate truth is that once it’s clear that a Startup is going to struggle to achieve escape velocity, they need to work with their Investors to “Land The Plane.” This is typically very tricky because navigating a safe and controlled descent towards a positive outcome isn’t straightforward nor guaranteed. It often involves finding a strategic buyer that recognizes the value in the Startup's financial performance, technology, customer base, or talent pool. It often devolves into very heated debates about how to distribute a pool of money or stock that’s less than everyone is happy with. And it often requires a Founder to internalize what they’ve built and what their options are with crystal clarity rather than through their normal “eternally optimistic” lens.

And given the “Grand Reset” that’s happening within the Startup ecosystem (which I wrote about here: x.com/fintechjunkie/status/1… ), everyone is embracing the reality that the ZIRP environment funded too many Startups that will never achieve escape velocity. The implication is that there are a lot of planes in the air right now that need to be guided to safe landings or they’ll most likely run out of fuel and crash.

STEP 1: AGREE TO LAND THE PLANE

While not the original destination, a strategic acquisition can be a win for a Founder and for a VC, even if the financial windfall isn't astronomical. Internalizing this is important for all parties because it takes alignment and coordination to pull off a safe landing. Benefits include:

Payment For Value Creation: In many cases, a strategic sale translates to some form of renumeration, whether it be in terms of cash or stock. Even if the financial returns aren’t great, any cash returned to Investors means they can return it to their LPs which is a major driver in raising additional money from them in the future. And if the payment is in stock, hopefully there will be some return in the future that offsets the time and money poured into the Startup.

The Mission Can Continue: Acquisition by a larger company often injects valuable resources, expertise, and market access that can accelerate a Startup’s mission. The startup's technology, service or product could gain instant exposure to a wider audience, potentially amplifying its original mission far beyond what it could have achieved independently. Founders witnessing their creation flourishing within a larger ecosystem can be incredibly rewarding, even if they're no longer “at the top of the food chain”.

Employee Success: A strategic buyer is likely interested in retaining the Startup's talent because these are the people who built what the acquirer is coveting. Many times, the Founders and Employees end up with great jobs at the acquirer and no longer feel the pressure of having to outrun the cash burn of an underfunded Startup. Employees are typically offered opportunities for growth that also come with great pay packages and real stability. Founders who prioritize their team's happiness can find solace in knowing they've secured great jobs for the people who believed in their vision. And it’s common for Founders to use the integration period to breathe, learn from past experiences, and potentially prepare themselves to build something even bigger.

Building a Strong Reputation: A successful acquisition, even at a moderate valuation, can solidify a Founder's reputation in the VC ecosystem. It demonstrates their ability to build something of value, attract interest from Investors, and navigate the complexities of a sale. This positive track record positions them for future success when seeking funding for their next venture. Investors are more likely to back Founders who can navigate “Landing The Plane” instead of “Fighting To Remain Independent” when the writing is on the wall that it’s time to sell.

STEP 2: PREPARE FOR A SALE

Preparing to sell a company isn’t as easy as it sounds. It’s not as simple as hiring a Banker and putting together a data room. Building awareness about what a Startup does within the prospective buyer community and cleaning up how it operates are critically important and time consuming steps in most successful M&A processes. This means that the time to sell a company is 6-12 months before it would run out of cash. Cutting it too close will almost always lead to a fire sale, an acqui-hire (with no value exchanged for the Startup’s assets) or a no-bid.

Building Awareness Within The Buyer Community: Most successful M&A transactions occur between known parties. If your first outreach to a potential strategic buyer is a Banker led M&A process then the odds of completing a transaction with that buyer is extremely low and diligence will be extremely long. Many times the buyer is a company that already interacts with the Startup in some form or fashion or has already expressed interest in the past. If the Investors and Founders of a Startup determine it’s time to sell, then the first step is to take stock of who already knows the company and whether or not they’re likely buyers. The second step is to determine who knows other potential buyers and put a plan in place for introductions in advance of launching a formal process. This can take many months or even many quarters depending on how the potential universe of buyers makes decisions. So starting early is critically important.

Cleaning Up How A Startup Operates: The truth that nobody in the Startup ecosystem wants to internalize is that most Startups are actually liabilities, not assets. If a Startup is burning money, then the cash-burn of the entity is a liability it wants a buyer to assume. If a Startup has a tech stack that doesn’t seamlessly integrate with a buyer’s tech stack, the integration and cut-over costs are liabilities that the Startup wants the buyer to assume. If employees would “die before they’d work for a big company”, then the acquirer is being asked to absorb the disruption of near guaranteed attrition.

Not all these issues can be solved before kicking off an M&A process, but the ones that can be addressed should. Reducing the burn of the entity is CRITICALLY important so making cuts to G&A and other “optional” areas should be done before pulling together a forecast of future performance. And talking to the leadership team about “who’s in and who’s out” can help negotiations down the road, especially if a Founder can get commitments from their team about the value of putting in “two years and one day” for the sake of everyone involved.

STEP 3: RUN AN ORGANIZED M&A PROCESS

Books could be written about the nuances how to set up an M&A process for maximum odds of success, but the high level generic advice consists of running a very organized process with a clean data room and financials, being prepared to tell a compelling story about the value of what’s been built, being realistic about what the real value is to each potential acquirer, and doing everything possible to get more than one buyer interested to generate leverage.

Conclusion:

“Landing The Plane” may not be the glamorous IPO envisioned by Founders and Investors, but by no means should it be considered a complete failure. It signifies the ability to internalize reality, adapt to market conditions, and secure some outcome for all stakeholders. Ultimately, a successful landing paves the way for another journey in the future. And a successful landing could return cash to and free up time for Investors to seek out the next potential rocket ship.

31 May 2024

The Grand Reset: VCs and LPs Are Starting To Internalize Reality

The past few years in the VC space have been brutal. Darwin has returned from vacation and the frothy gold rush of the 2018-2021 startup ecosystem has vanished. The ZIRP environment caused valuations to soar and VCs threw money at any startup with a pulse. The money was put to work by Founders quickly, many of whom chased shiny objects and undisciplined growth because their bank accounts were flush with cash.

But a harsh reality set in once we entered a new and higher interest rate economic cycle at the beginning of 2022: The vast majority of the high-flying ZIRP era startups are unlikely to deliver great financial outcomes for their investors and employees.

Early in the correction cycle there was a lot of denial by Founders, VCs and LPs, but this denial has for the most part gone away. For many startups it’s clear that it will be challenging if not impossible to earn their way into their last valuation. For many investors it’s clear that they’re playing to recoup their money (i.e. – playing for pref) rather than playing for “fund returning outcomes”. And for many LPs, they realize that this is an industry wide phenomenon because every active fund manager played the game that was on the field.

This has birthed a phenomenon that can be thought of as "The Grand Reset" where everyone in the ecosystem is seeking the cleanest path to a “do over”.

Venture capitalists know that they have one or two funds that are going to underperform but are excited about their front book opportunities. So the “new deal” they’re making with LPs is that they’ll try to quickly recoup what they can and make the most of the back book in return for being more disciplined going forward.

LPs understand that more investments than normal will fail and they know that absorbing those losses will lead to lower fund performance. LPs realize that the VC asset class is cyclical and great vintages can be created by great managers once the ecosystem flushes out the mistakes produced in an abundant and free flowing capital environment. The “new deal” they’re making with VCs is that they’ll forgive a bad vintage if the VCs will be honest with them about what the back book is “worth”, be more disciplined going forward and they’ll do everything they can to return some cash “soon”.

And many Founders have realized that the ZIRP funding environment hurt their startups in multiple ways. First, their common equity is likely buried under a massive preference stack. Second, too much money caused them to hire too many people and invest in too many projects and undoing this has been challenging. Third, raising capital when a company has been in “shedding mode” rather than “growth mode” is difficult which puts re-booting growth at risk. And finally, the opportunity cost of trying to fix a broken business vs. starting a new one from scratch makes sticking around “expensive”.

The net result of this “Grand Reset” is that there’s no longer incentive for anyone to maintain the illusion they can shepherd mediocre companies towards billion-dollar IPOs that aren’t going to happen. Instead, the focus has shifted towards "landing the plane" for the 90% of companies that aren’t ever going to achieve escape velocity. This generally means navigating an acquihire for struggling companies and helping “good but not great” portfolio companies find exits through acquisitions or mergers even if it means selling for a fraction of their inflated peak valuations.

This shift can be brutal for Founders who envisioned a triumphant IPO. But for many, it's a wake-up call. The pressure to "grow at all costs" has receded, replaced by a need to focus on building sustainable businesses with real revenue models and clear paths to profitability.

And "The Grand Reset" isn't just about selling off inflated companies. It's about resetting expectations on all fronts. VCs are re-evaluating their investment theses, focusing on strong unit economics and caring about capital efficiency. Founders are being forced to build businesses that can turn over cards in a disciplined way and survive without the crutch of endless VC funding. And LPs are seeking to re-up with Funds that have great pre-2018 track records and have a true competitive edge in today’s new normal environment.

This new landscape has its downsides. The flow of easy money has dried up which makes it harder for promising early-stage startups to secure funding. But there are upsides as well. The emphasis on fundamentals could lead to the creation of a new generation of startups built on a foundation of sustainable growth, not just hype.

The Grand Reset represents a significant course correction for the startup ecosystem. It's a painful process, but it could ultimately lead to a healthier and more sustainable future for both VCs and startups alike. As the dust settles, one thing is clear: The era of easy money is over. The startups that emerge from this reset will be the ones that can demonstrate real value and build strong businesses for the long term.

(More on "landing the plane" in a thread next week).

21

23

173

125,264