113 Photos and videos

Tengo una empresa que la tasación de 1 solo activo (De los 9 que tiene) supera en un 36% su market cap 🤯.

Como el mercado no cree el valor de los activos, he tenido que visitarlos a pie de calle, a ver que #### pasa¡

Mañana deep value del DURU para el clap de @MomentumFinanc3

5

1

27

4,545

80% de mi tiempo en burocracia , 20% generando PIB, y se pondra peor. Pasaporte para los productos 🤣

camarabilbao.com/empresa/int…

Luego os preguntáis porque los productos son mas caros en la UE, si en China valen mucho menos. Imposible competir así.

4

2

10

547

SPCone retweeted

Jun 10

The $295 billion stimulus package is a massive boost for cloud companies $BABA and $BIDU—it cuts their costs and directly boosts their profits... but have some fund managers really not figured this out? 🤦♂️

5

2

29

3,925

Primero Kazajistan, ahora Uzbekistan.... Central Asia the place to be @Benceno88

Hong Kong SAR Chief Executive John Lee led a joint Hong Kong-Mainland business delegation and concluded the visit to Uzbekistan on June 5 by learning about the latest developments in the digital economy and cultural preservation of the country. He visited IT Park Uzbekistan, an innovation technology park and met with the First Deputy Minister of Digital Technologies of Uzbekistan, Ayubkhon Sultonov, on strengthening co-operation between the two places in I&T and the digital economy. He also witnessed the exchange of memorandum of understanding or the confirmation of intention to co-operate between IT Park Uzbekistan and Hong Kong’s three major I&T parks — Cyberport, the Hong Kong Science & Technology Parks Corporation and the Hong Kong-Shenzhen Innovation & Technology Park — to enhance co-operation in areas such as startup incubation, talent exchange and joint research and development.

The Central Asia visit has yielded fruitful results, advancing a hub-to-hub cooperation model and creating broader prospects for future partnerships between Hong Kong and the Central Asian region.

info.gov.hk/gia/general/2026…

2

7

197

5

150

Más madera

Jun 4

Mainland investors are lining up in Hong Kong to open bank and brokerage accounts after regulators moved to phase out unauthorized cross-border trading platforms. The shift is benefiting local brokers but raising fresh legal and capital-control risks caixinglobal.com/2026-06-05/…

2

118

SPCone retweeted

Kuaishou's Q1 2026 results highlighted an increasingly important reality: much of the AI value in the company may now sit inside Kling.

While Kuaishou reported record quarterly revenue of RMB 33.72 billion ($4.65 billion), adjusted net profit fell 26% year-over-year to RMB 3.37 billion ($465 million). Meanwhile, Kling generated more than RMB 650 million ($90 million) in quarterly revenue, with ARR approaching $500 million, up roughly 5x from a year ago. The business is reportedly seeking outside funding at a $20 billion valuation.

What's notable is that Kling's growth appears largely independent of Kuaishou's core short-video business. Around 70% of revenue reportedly comes from overseas markets, driven by professional users in advertising, film, gaming, and short dramas rather than Kuaishou's domestic consumer traffic. That makes a spin-off easier to justify: Kling gains access to capital and talent incentives without sacrificing a major distribution advantage.

The timing also reflects how competitive AI video has become. Management says inference costs for Kling 2.5 Turbo have fallen nearly 30% and margins are approaching breakeven, but this remains a scale business. ByteDance is reportedly planning up to $70 billion of AI infrastructure spending this year, while Kuaishou's 2026 capex target is around RMB 26 billion ($3.6 billion).

One thing we have argued before is that defensibility in AI increasingly comes from distribution and integration rather than model performance alone. Kling's foothold among overseas professional creators may be one such advantage. The question is whether it can maintain that position as competition intensifies and some of the engineers who helped build it are now working elsewhere.

1

17

4,705

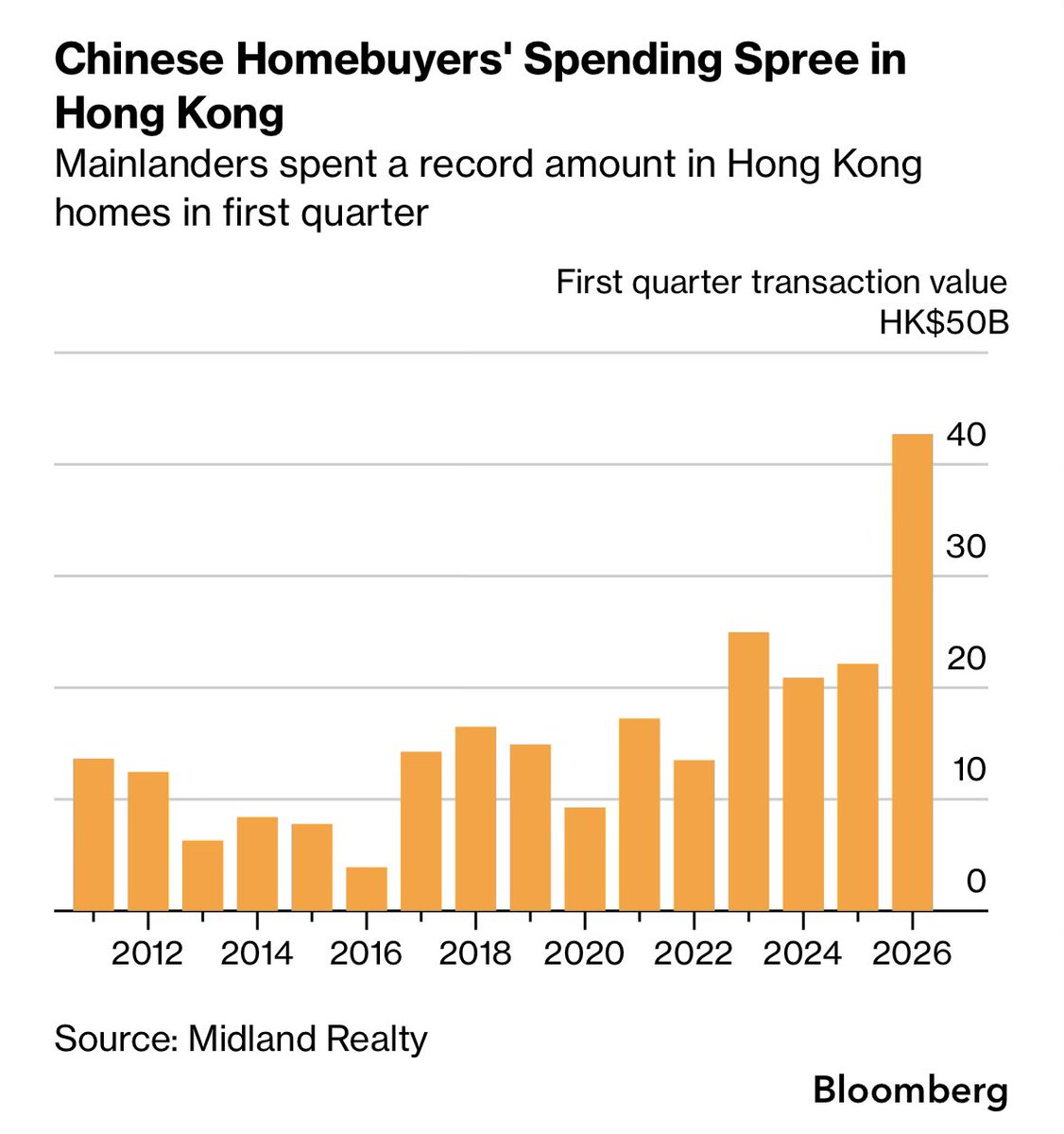

El método clásico ha sido y es comprar real estate en HK.

Tal y como explicamos en

youtu.be/C6iMy-5-LeY?is=SwmZ…

In China, individuals are generally limited to transferring just $50,000 overseas each year. Yet demand for foreign assets remains strong, and people have found ways to circumvent some of the world's toughest capital controls. Here's how. bloomberg.com/news/articles/…

2

206

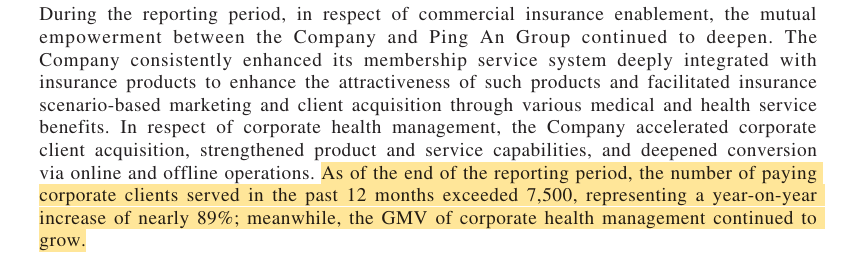

1833 PA Good Doctor

El negocio progresa adecuadamente, en la parte donde está la pasta que es en el servicio a empresas.

La cotización por el momento, NO

Hay que seguir monitorizando el crecimiento del Corporate

open.substack.com/pub/moment…

2

5

558

El mayor DISPARO EN EL PIE de la historia. By @AdrianDiazMarro

youtu.be/Ftf3h7y7B6I?is=eFSO…

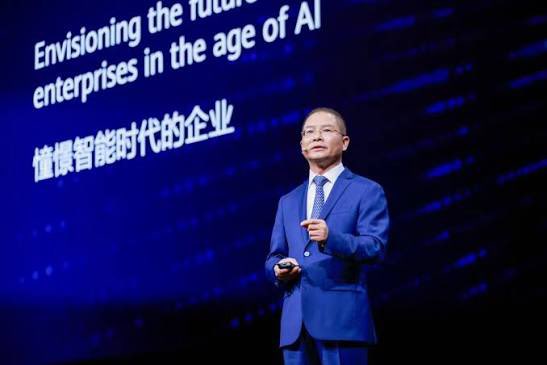

#Huawei: U.S. sanctions accelerated China’s semiconductor rise.

Eric Xu, Vice chairman of Huawei, says the external pressure forced the buildout of a fully domestic chip supply chain—now gaining broad industry support.

6

15

2,570

Se ha declarado en bancarrota como en Julio de 2024? Para hablar de actualidad financiera vais un poco tarde diría yo.

Venga, esforzaros un poco mas que a mi me interesan saber las malas noticias de China tb

Jun 1

El Banco de China Jiangxi se ha declarado en bancarrota, un acontecimiento que está generando interés entre analistas económicos y observadores de los mercados internacionales.

Aunque se trata de una entidad específica y no necesariamente de una señal representativa de todo el sistema bancario del país, la noticia abre interrogantes sobre la evolución de la economía china.

Te leemos en los comentarios

Visita: WWW.TRADINGPRO.APP

#China #Economia #Mercados #Inversion #Geopolitica

4

132

Crisis así me gustaría tener a mí. En fin, almenos ya sabemos donde informarnos de verdad.

Jun 1

Shanghai’s resale home market had its strongest May in six years last month, with 28,023 transactions, up about 31% from a year ago, according to online data from the Shanghai Real Estate Trading Center. Activity has stayed elevated through 2026, with monthly sales topping 28,000 units for three straight months.

1

5

210

SPCone retweeted

May 31

🪙No habrá Paz para los Indexados Vol.2

👉Nuevo artículo para la Newsletter de Momentum centrado en la enorme empapelada que se avecina a costa de los desprevenidos inversores pasivos. Invertir tomando el sol en la playa, tenía un precio 😅.

✅Link en mi perfil.

3

17

1,519

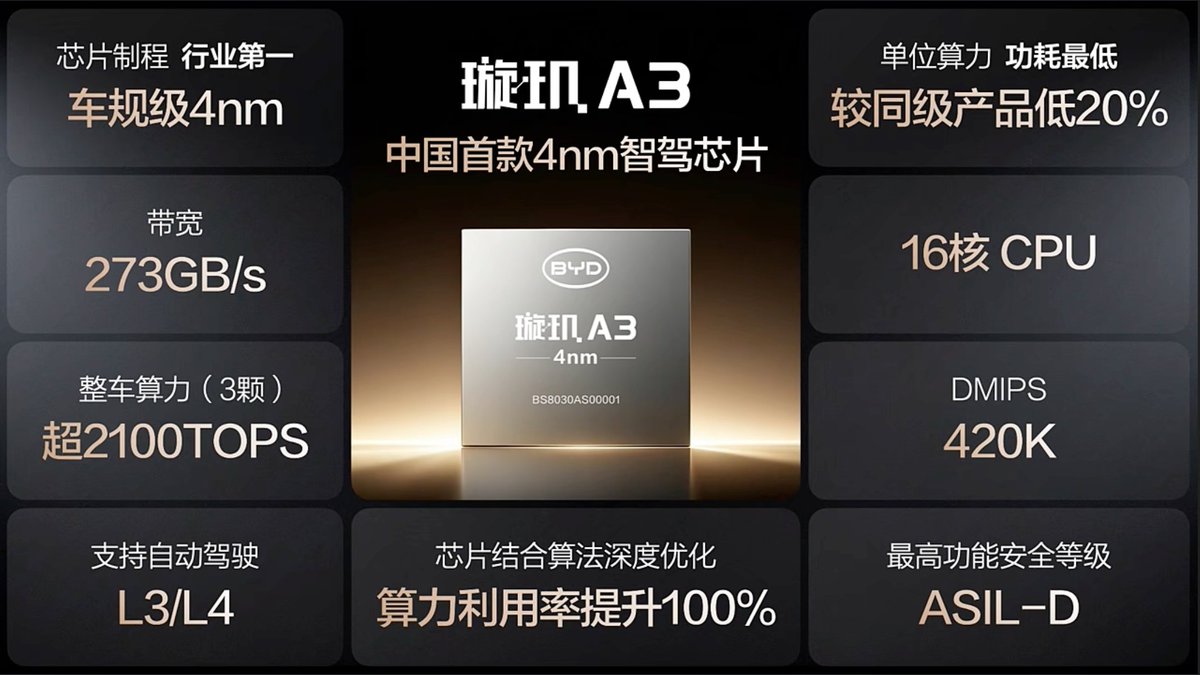

9660 Horizon Robotics se la pega por esta noticia.

May 28

BYD has officially launched its first in-house developed smart driving chip, the Xuanji A3, which supports L3 and L4 autonomous driving.

Key specs of the chip:

1. Built on a 4nm process with 273GB/s bandwidth.

2. Features a 16-core CPU with a single-core computing power of around 700 TOPS.

3. Delivers 420K DMIPS and meets ASIL-D safety standards.

$BYDDY #ChinaEV

4

122