Joined March 2025

- Tweets 4,345

- Following 43

- Followers 1,918

- Likes 6,439

34 Photos and videos

Pinned Tweet

21 Oct 2025

Vault reimagines what a crypto wallet should be - simple, secure, and intuitive. It allows you to move and store stablecoins with no need for native tokens. Designed with a banking-like interface and gasless transaction flow, Vault transforms digital assets into a seamless experience for real payments and global transfers.

17

8

69

12,992

Jun 11

Read the review and reflections from @htwtech_ on the newly released whitepaper by @arc

A useful breakdown of what private EVM execution can unlock for on-chain finance, confidential applications, and institutional blockchain infrastructure.

Private EVMs may become one of the most important infrastructure shifts for on-chain finance.

@arc Privacy Sector shows how confidential execution, public finality, and familiar Solidity tooling can work together: opening the door for private payroll, credit markets, asset issuance, and institutional settlement without exposing sensitive data on-chain.

htw.tech/blog/arc-privacy-se…

2

4

12

3,589

Jun 10

She Didn't Care About Crypto — She Just Wanted to Get Paid

Nina, a designer in Tbilisi, had clients in Toronto, Amsterdam, and Dubai. The work was great. The payment process was a recurring nightmare. Crypto wasn't on her mind — getting her money was.

Nina has never read a single article about crypto. She doesn't follow Bitcoin prices. She has no opinion about blockchain, decentralisation, or the future of finance. She is a UX designer, good at her job, with clients in four different countries.

That last part — getting paid — turned out to be the complicated bit.

— The problem —

Nina's client in Toronto wanted to pay via wire transfer:

• Took seven business days.

• Arrived as Georgian lari at a rate set by her bank, unknown until it landed.

Her client in Amsterdam used Wise:

• Worked, but took 2–3 days.

• Had a conversion fee.

Her client in Dubai (her biggest) couldn't use PayPal. He offered to "figure something out," which usually meant delayed payment and an apologetic message.

Nina wasn't losing money to crypto. She was losing money, time, and energy to a system never designed for someone like her — a skilled professional working across borders from a country not on the "easy" list of most payment platforms.

— The payment process, laid out honestly —

Nina invoices a client — what used to happen next:

• She sends the invoice. Waits.

Client confirms receipt. Initiates transfer. Three banks are involved.

• Bank 1 sends to a US correspondent bank. Fee taken.

Day 2. Nina doesn't know this is happening.

• Correspondent bank forwards to Georgian bank. Another fee.

Day 4. Still not there.

• Georgian bank converts to lari at its own rate. She receives less than invoiced.

Day 7. She finds out on Day 7.

• She messages the client to confirm. Awkward, feels like chasing.

The work was delivered. This part shouldn't be hard.

— Two people, one transaction, different problems —

Nina's client in Toronto didn't have a great time either. Wire transfers are slow and expensive for the sender too. He had to call his bank to authorise an international transfer, fill in a form, and pay $35 in wire fees — on top of whatever Nina's bank charged on the receiving end.

Both sides of this transaction were frustrated. Not because either person did anything wrong, but because the tool they were using was the wrong shape for the job.

— The client in Toronto's problems —

• Paid $35 in bank fees just to send payment.

• Filled in forms to authorise the international wire.

• Had no way to track whether it arrived.

• Received a message from Nina asking if it was sent — uncomfortable for both.

— Nina in Tbilisi's problems —

• Waited 7 days after work was delivered.

• Received less than invoiced — exchange rate taken by the bank.

• Had no visibility into where her money was for a week.

• Had to ask her client to confirm — which felt awkward.

— How it actually got solved —

Nina's Dubai client — the one PayPal couldn't serve — mentioned he paid other freelancers in USDT. He was matter-of-fact: "It's just how I pay internationally. Do you have a wallet?"

She didn't. She set one up that afternoon. He sent payment the next day — $1,200 USDT arrived in her VAULT wallet in about 50 seconds.

She stared at the notification, then checked the balance. There it was. Not "pending." Not "processing." Not converted to lari at a rate she didn't agree to. Just $1,200.

— The thought she had —

"I kept waiting for the catch. The fee that would appear. The conversion that would take a percentage. The email saying the transfer was under review. None of it came. I asked him how much it cost him to send. He said: six cents."

She converted a portion of it to lari at a local exchange at a rate better than her bank had ever given her. She left the rest as USDT. The following month, her Toronto client asked if he could switch to USDT too. She said yes before he finished the question.

— What crypto actually is, for people like Nina —

Nina still doesn't care about crypto. She couldn't tell you the difference between proof-of-work and proof-of-stake. She has no interest in Bitcoin cycles or DeFi yields.

She has exactly one use for a crypto wallet: getting paid in full, quickly, without seven banks taking a cut.

And that's fine. That's exactly the right relationship to have with a payment tool. You don't need to care about how your email server works to send an email. You don't need to understand TCP/IP to use the internet. You don't need to understand blockchain to receive USDT in VAULT.

— What VAULT does for both sides of this transaction —

Client:

• Sends once. No wire form, no bank call, no $35 fee. Opens wallet, enters amount and Nina's address, confirms. Total time: two minutes. Cost: six cents.

Nina:

• Receives the full amount. No correspondent bank, no lari conversion at a bad rate, no waiting. The money arrives in under a minute, in a stable dollar value, on her terms.

— The larger point —

Most people who end up using USDT for payments didn't arrive at it through crypto enthusiasm. They arrived at it through frustration. A wire that took too long. A client who couldn't use their preferred platform. A conversion that quietly trimmed their invoice. A payment that simply didn't work.

USDT solved the payment problem. VAULT made it feel like a normal app instead of a technical challenge. Neither of those things required Nina to care about crypto — they just required a tool that worked better than what she had.

—

"I don't describe myself as someone who uses crypto. I describe myself as someone who gets paid properly now. Those are different things."

— Nina, UX designer — and the perspective of most VAULT users worldwide

—

What VAULT is for: It's not for people who are excited about crypto. It's for people who are frustrated with the payment system they already have — and want something that works better, costs less, and doesn't require a seven-day wait to find out if their money arrived.

— Key ideas —

• You don't need to care about crypto to use it — you just need to care about getting paid.

• Both sides of an international payment lose: the sender pays fees, the receiver waits and gets less.

• USDT solves the payment problem. VAULT makes it feel like a normal app.

• "I don't use crypto — I just get paid properly now." That's the right relationship with the tool.

— Bottom line —

The best tool is the one you forget you're using. VAULT is designed to be that — the app you open when someone sends you money, and close when it arrives. What happens in between is someone else's problem to understand.

#VAULTwallet #EverydayMoney #Stablecoin #Payments #Freelance #InternationalPayments #USDT

3

11

2,547

Jun 4

This is one of the key reasons we chose @htwtech_ as our infrastructure provider.

Jun 4

Building on Solana? Your dApp performance depends more on RPC architecture than on “theoretical TPS”.

Key best practices from a recent Solana RPC infra guide:

Avoid relying on public RPC for production (rate limits, unstable latency, no SLA).

Separate infra for read vs write, and scale RPC horizontally as load grows.

Optimize requests: batch where possible, cache aggressively, and avoid redundant calls.

Monitor latency, error rates, and slot lag as first‑class product metrics, not just infra metrics.

Treat RPC as core product infrastructure, not a commodity endpoint — that’s where real UX and reliability come from.

You can find the full breakdown on our website in the Blog section.

htw.tech/blog/solana-rpc-inf…

3

17

1,732

May 25

Crossing a Border Shouldn't Break Your Money

Your phone works in every country. Your music works in every country. Your maps work in every country. Your money — somehow — still doesn't.

Warsaw airport — 11 PM

Marta lands after a connecting flight. She needs a taxi. She opens her banking app — it shows her balance in Polish złoty, but this is Berlin and she needs euros. Her card declines at the first ATM. Her bank has flagged the transaction as suspicious activity. She calls the number on the back of the card. It's a Sunday. The helpline is closed until Monday morning.

This is not a rare story. Almost everyone who travels regularly has a version of it.

• The card that worked perfectly at home — declined.

• The ATM that charged €6 for the privilege of giving you your own money.

• The bank that decided your trip to another country was suspicious and froze access without telling you first.

Meanwhile, your iPhone connected to local WiFi in two seconds. Spotify started playing before the seatbelt sign turned off. Google Maps knew exactly where you were. The digital infrastructure of your life crossed the border without noticing. YOUR MONEY DID NOT.

The strange asymmetry

Almost everything digital has become borderless. Streaming services, messaging apps, email, maps, social media — none of them care which country you're in. They work.

Your money has somehow remained stubbornly local, stubbornly slow, and stubbornly expensive to move across any line on a map.

—

Crosses borders without friction:

• Your phone — connects to local networks automatically

• Your music — plays wherever you are

• Your messages — free, instant, to anyone

• Your maps — real-time, in every country

• USDT in VAULT — always $1, works anywhere

Still breaks at borders:

• Your card — foreign transaction fees, potential block

• Your bank wire — 3–5 days, $25 fee

• Your local payment app — only works in one country

• Your currency — changes value the moment you cross

—

The problem isn't that international payments are technically hard. They aren't — money is just information, and information moves across borders instantly.

THE PROBLEM IS that the financial system was designed before the internet, and most of it was never properly rebuilt for a world where people routinely live, work, and travel across multiple countries.

What actually happens at a border

The same card, the same person — different outcomes in different countries:

✕ Foreign transaction fee. Your bank charges 1–3% just for spending in a different currency. You never asked for this. It's buried in the terms. €500 of spending quietly becomes €510–€515.

✕ ATM withdrawal fee. The local ATM charges a fee. Then your bank charges a fee. Then the exchange rate is set against you. A €100 withdrawal can cost €110–€115 in real terms.

✕ Fraud flag. Your bank's algorithm sees spending in an unusual location and freezes access "for your protection." There is often no warning, no notification, and no way to fix it until business hours resume.

✕ Currency conversion at the wrong moment. You have euros, the local currency is different, and the rate you get is determined by whoever is doing the conversion — not by you.

✓ With VAULT. Your balance is USDT. It doesn't change when you land. No foreign transaction fee, no bank fraud flag, no ATM queue. Your money arrived before you did.

—

Your money doesn't know where you are — but your bank does

Here's what's strange about the bank's fraud protection logic: it works against you precisely when you need your money most. You're in an unfamiliar city, it's late, you need cash — and the bank has decided this is the moment to restrict your access.

USDT held in a self-custody wallet has no such logic. There is no bank watching your location and making decisions on your behalf. The money is yours, accessible from any device, in any country, at any hour. Nobody decides that your trip to Thailand looks suspicious.

What VAULT actually changes:

Your VAULT balance is the same in Berlin as it is in Bangkok, Buenos Aires, or Beirut. You don't exchange it, you don't convert it, you don't notify anyone. You open the app. Your money is there. You use it. The border you crossed is completely irrelevant to the transaction.

—

The countries where this matters most:

• Germany: Card works, but €4 ATM fees are common. Cash still widely expected. (Friction)

• Argentina: Official rate vs. real rate — your card gives you less than the market value. (Significant loss)

• Ukraine: Banking disruptions, foreign cards often unreliable. USDT widely used. (USDT preferred)

• Nigeria: International cards frequently blocked or limited. USDT is the practical alternative. (USDT preferred)

• Japan: Still largely cash-based. International cards work in cities, unreliable elsewhere. (Cash friction)

• VAULT wallet: Works in every country on earth. Same balance, same address, no conversion. (Always works)

—

The phone analogy that makes this obvious

You don't carry multiple SIM cards for different countries anymore. Your phone connects to local towers automatically — you don't think about it, it just works. International roaming solved a friction problem that used to be significant.

USDT is the equivalent for money. Not a foreign currency you have to acquire and then reconvert. Not a card you have to call ahead to "activate for travel." Just your balance, working wherever you are, denominated in something that doesn't change when you step off the plane.

—

"I spent three months traveling across six countries last year. My bank card worked in four of them, unreliably. My VAULT balance worked in all six — same balance, same interface, no surprises. I stopped carrying backup cash about halfway through the trip."

— A common experience for people who use VAULT as their travel companion

—

The simple version: Money that respects borders is a legacy problem — a leftover from when finance was physical and local. USDT doesn't respect borders because it was built after borders stopped mattering for information. VAULT puts that money in your pocket, looking exactly like the app you already use for everything else.

—

Key ideas:

• Your phone, music, maps, and messages cross borders without friction. Your money still doesn't — but it doesn't have to.

• Foreign transaction fees, ATM charges, fraud flags, and bad exchange rates are NOT INEVITABLE — they're design choices of legacy systems.

• USDT doesn't know what country you're in. Your balance is the same on landing as it was on departure.

• VAULT is built to be your money wherever you are — not a travel product, just your regular wallet that happens to work everywhere.

—

Bottom line: The fact that crossing a border makes your money complicated is not a law of nature. It's a design flaw in systems built before the internet. VAULT is the fix — money that travels as easily as everything else on your phone.

Stablecoin wallet for your mom

#VAULTwallet #EverydayMoney #Stablecoin #TravelMoney #BorderlessFinance #USDT

3

24

1,876

May 19

Your copy-paste just changed the address

Scam Alert - Don't Do This

There's a scam so simple it's hard to believe. You copy a wallet address. You paste it. But what lands in the field is someone else's address entirely.

When you send money somewhere, you type in an account number. You probably read it back, or at least glance at it. With crypto, most people skip that step - the address is long and ugly, so they just copy, paste, and hit send.

That's exactly what scammers count on.

Real-life analogy: Imagine you write your friend's bank account number on a sticky note. Someone sneaks in, crosses out the last four digits, and writes their own. You don't notice. You send the money. It's gone - and there's no bank to call.

How clipboard hijacking works

One type of malware sits quietly on your phone or computer and watches your clipboard - the invisible place that holds whatever you just copied. The moment it sees something that looks like a wallet address, it swaps it for the attacker's address. You paste, you see a long string of letters, you assume it's fine.

It isn't. That address is not yours to send to.

Crypto transactions are irreversible. Once you send to the wrong address, the money is gone. No undo button. No support ticket. No refund.

What the swap looks like

The fake address looks almost identical. That's the point. Scammers generate addresses that share the first and last few characters with the real one - so a quick glance fools you completely.

Address you copied (your friend's real address):

0x4a9f...c83b12d7ef2c1

First 6 and last 4 characters look like a match

Address that actually got pasted (attacker's address):

0x4a9f...7741cc9a2f2c1

Middle characters are completely different - but who checks those?

The three-second habit that saves you

1. Paste the address

Do this as you normally would.

2. Check the first 6 and last 6 characters

Compare them against the original - in the email, message, or QR code you received. Both ends must match exactly.

3. Only then - send

If anything looks off, don't guess. Ask the person to re-send their address through a different channel.

Habits worth keeping

• Always verify the first and last 6 characters of any address before sending.

• Use QR codes when possible - they don't touch your clipboard at all.

• For large amounts, send a tiny test transaction first. Confirm it arrived, then send the rest.

• Keep your phone and computer updated - clipboard malware often exploits old software.

Three seconds of checking can save everything you were about to send. It's the one habit that costs nothing and pays off every time.

VAULT displays your recipient's address in full before you confirm. And have actual database with scam addresses! Take that moment to look at it. That moment is the whole game.

#CryptoSecurity #ClipboardHijacking #WalletSafety

2

29

1,948

May 15

Why You Double-Check Every Crypto Transaction

You don't triple-check your Venmo. So why does sending USDT make you break into a cold sweat? The answer says everything about what crypto got wrong — and what needs to change.

Think about the last time you sent money through Venmo or PayPal. You typed a name, entered an amount, hit send. Maybe you glanced at the screen for half a second. Then you moved on with your day.

Now think about the last time you sent crypto. Did you check the address once? Twice? Did you send a tiny test amount first — just to make sure — before sending the real thing? Did you feel a small knot in your stomach until the confirmation came through?

That knot is not irrational. It's a rational response to a genuinely stressful system.

—

Why crypto feels so different

When you send money through a bank app or Venmo, there are safety nets built in. If you type the wrong name, the app often catches it. If something goes wrong, there's a customer support team. In many cases, transfers can be reversed.

Crypto has none of those. A wallet address — the thing you paste when sending USDT — is a long string of random letters and numbers. It looks like this:

A typical USDT wallet address:

TQn9Y2khHMQx4agPKjPxjsLn8sR5S4kWzNe

Note: Two characters (h and k) are implicitly highlighted in the original. If either of those were wrong, the money would go to a completely different wallet — or disappear entirely. There is no undo.

If you send to the wrong address, it's gone. No support team to call. No reversal. No "are you sure?" prompt that actually checks anything. The system is designed to be unstoppable — which is great for privacy and censorship resistance, but deeply uncomfortable when you're just trying to pay a friend back for dinner.

—

The same task, two very different experiences

Sending $50 on Venmo:

• Search friend's name

• Enter $50

• Tap Pay

Sending $50 in USDT (Typical crypto wallet):

• Ask friend for address

• Which network? TRC-20? ERC-20?

• Paste 42-character address

• Check it. Check again.

• Send $1 test first

• Wait. Refresh. Confirm.

• Send the real amount

• Check again. Breathe.

The double-check isn't a personality quirk. It's the only rational response when mistakes are permanent and there's no way to recover from them.

—

This isn't how it has to be

The anxiety isn't built into the idea of digital money — it's built into the current design of crypto wallets. And design can change.

When you send money to a name or a phone number instead of a 42-character address, the chance of a catastrophic error drops dramatically. When the app confirms who's receiving the money — not just that the address format is correct — you can breathe. When the network is handled automatically so you can't accidentally send on the wrong one, a whole category of mistakes disappears.

—

The goal isn't to make crypto less powerful. It's to make the scary parts invisible — the same way your bank app hides routing numbers and SWIFT codes behind a simple "send to contact" button.

— The design philosophy behind VAULT wallet

—

Until then, here's the honest advice:

Always double-check the first and last four characters of an address before sending. Send a small test amount first when trying a new address. And if the app asks you which network to use and you're not sure — find out before you send, not after.

—

The short version:

You double-check every crypto transaction because the system punishes mistakes permanently. That's not your fault — it's a design flaw. The best wallets are working to make this anxiety unnecessary. Until they do, caution is the right instinct.

—

Key ideas:

• Crypto transactions are irreversible — a wrong address means the money is gone, permanently.

• The anxiety you feel is a rational response to a poorly designed system, not an overreaction.

• Good wallet design removes the need for that anxiety by replacing addresses with names, and handling the technical details automatically.

• Until then: always verify the first and last four characters, and send a test amount when in doubt.

#VAULTwallet #EverydayMoney #CryptoSafety #WalletDesign #USDT

3

29

3,740

May 13

Why people use USDT instead of their bank

For hundreds of millions of people, the bank simply isn't good enough. Here's what they use instead — and why.

—

If you live in a country with a stable currency and a reliable bank, it's easy to assume that everyone does. But most of the world doesn't.

Banks are slow, expensive, and sometimes simply unavailable. Or the local currency loses value so fast that keeping money in it feels like watching it melt.

USDT — the most widely used stablecoin — has quietly become the dollar account for people who can't get a real one. Here's why.

—

A global perspective:

• 1.4 billion adults globally without a bank account

• $25–50 typical fee to wire money internationally

• <$0.10 typical cost to send USDT anywhere

—

Four reasons people choose USDT over a bank:

1. Their local currency is losing value

In countries like Argentina, Turkey, or Nigeria, the national currency can lose 30–50% of its value in a single year. Keeping savings in USDT — which is always $1 — means your money holds its value. It's like having a dollar savings account, without needing a US bank to open one.

2. They need to send money across borders

Banks charge big fees for international transfers and take 1–5 business days. USDT arrives in under a minute, costs almost nothing, and works on weekends. For migrant workers sending money home to their families, this alone saves hundreds of dollars a year.

3. They don't have access to a bank at all

Opening a bank account in many countries requires documents, a minimum deposit, or a physical branch nearby. USDT only requires a phone and an internet connection. No paperwork, no queues, no approval process.

4. They don't fully trust their bank

In some countries, banks have frozen accounts, blocked withdrawals, or collapsed entirely. With USDT in a personal wallet, your money is controlled by you — not by a bank that can lock you out at any moment.

—

A real-world picture

Everyday example: Maria works in Spain and sends money home to her family in Colombia every month.

Before, she used Western Union: $8 fee, 2-day wait, and her family walked to a pickup location.

Now she sends USDT from her phone — it arrives in 20 seconds, costs 10 cents, and her daughter receives it directly in her own wallet.

This is a story familiar to millions of migrant workers around the world.

—

So it's not really about crypto

Most people using USDT don't think of themselves as "crypto users." They don't care about blockchain or technology. They care about one thing: keeping their money safe and moving it cheaply.

USDT just happens to be the tool that does it better than anything else available to them. It's a practical solution to a practical problem — the same way people use WhatsApp instead of paying for international phone calls.

Simple version: USDT is a dollar that lives on your phone. No bank required. No borders. No business days. For a huge part of the world, that's not a luxury — it's just the smarter option.

—

What this means for you

Even if your bank works fine, the advantages are real: you can send money abroad instantly, hold dollars without a US account, and keep a backup outside the traditional banking system. More and more people — not just in developing countries — are discovering this.

Key ideas:

• USDT holds its value even when local currencies don't.

• Sending it costs cents, not dollars — and takes seconds, not days.

• All you need is a phone. No bank account, no documents.

• Your money stays in your control — nobody can freeze it.

Bottom line: Banks were built for a world that doesn't exist for everyone. USDT fills the gap — simply, cheaply, and reliably.

#VAULTwallet #EasyStablecoins #StablecoinWallet

1

18

2,851

May 10

Why is a stablecoin always ~$1?

It doesn't happen by accident.

There's a simple system behind it — and it's been working for years.

If you've never touched crypto before, you might wonder: how can something called a "coin" always be worth exactly one dollar? Doesn't the price of everything go up and down?

Yes — but stablecoins are built differently. There's a system behind them that keeps the price from moving. Let's look at how, using things you already know.

Think of a coat check at a restaurant.

You walk in, hand over your coat, and get a little ticket. That ticket is worth exactly one coat. Not two coats, not half a coat. One. When you leave, you hand the ticket back and get your coat.

A stablecoin works the same way:

You hand over $1 to the company that issues the stablecoin.

They hold that dollar in a real bank account.

In return, you get one digital token — worth exactly $1.

Want your dollar back? Return the token, get the dollar.

The rule: For every stablecoin that exists, there is one real dollar sitting in reserve. The token and the dollar are always 1-to-1.

—

What keeps it from drifting?

Here's the clever part.

If somehow the price of a stablecoin went up to $1.02 on an exchange:

Traders would immediately buy millions of new ones at $1 from the issuer.

They would sell them for $1.02 — pocketing the difference.

That flood of supply pushes the price back down to $1.

If the price slipped to $0.98:

People would rush to buy stablecoins cheaply.

They would redeem them for a full $1.

That demand pulls the price right back up.

You don't need to understand the mechanics — the point is: the system self-corrects automatically. Like a thermostat that keeps the room at exactly 20°C.

Typical price swings over 1 year:

• Bitcoin: ±40–80%

• Stablecoin: ±0.1–0.5%

—

Two simple examples:

Real-world comparisons

• You put $200 in a stablecoin wallet on Monday.

→ On Friday, you still have exactly $200.

• You put $200 in Bitcoin on Monday.

→ On Friday, you might have $160 — or $240.

That unpredictability is why most people don't use regular crypto for everyday money. Stablecoins remove that problem entirely.

—

The "~" part — why not exactly $1?

You might notice we write ~$1, not exactly $1.

In practice, stablecoins trade at $0.999 or $1.001 on any given day. That tiny wobble is completely normal — like how a perfectly calibrated scale still reads 99.8g sometimes. For any real-world use, it makes zero difference.

Bottom line: A stablecoin stays at $1 because every token is backed by a real dollar, and the system automatically fixes any small drift. It's not magic — it's just good design.

—

Why this matters to you:

• You know exactly what your money is worth at any moment.

• You can save, send, or spend without watching charts.

• It behaves like cash — but works on the internet.

#VAULTwallet #EasyStablecoins #Stablecoin

1

2

22

4,671

VAULT wallet retweeted

May 9

Representing @stable_VAULT and joining the conversation about stablecoins at @consensus2026 was truly exciting and inspiring.

Huge thanks to everyone for the great discussions, insights, and energy 🚀

Stay tuned — the VAULT team will be landing in your region very soon 🌍

1

1

20

1,753

May 9

What do you actually own in crypto?

And is it safe to store money this way?

The honest, jargon-free answer.

—

When you put $500 into a savings account, you know what you own: $500 at a bank, insured by the government, available whenever you want it. Simple.

But when you put $500 into stablecoins, what exactly do you have? This question makes a lot of people nervous — and that's fair. Let's answer it clearly.

You own a key, not a coin

There are no actual coins. No file on your phone. Nothing physical. What you own is something called a private key — a secret password that proves to the blockchain that those funds belong to you.

Think of it like a locker at a train station: Your money sits in the locker. The locker is public — anyone can see it exists and how much is inside. But only you have the key that opens it. Without the key, nobody — not a hacker, not even VAULT — can touch what's inside.

This is fundamentally different from a bank. At a bank, the bank holds your money and gives you permission to access it. In crypto, you hold the key directly. No permission needed.

Bank account:

• Bank holds your money

• Bank can freeze access

• Government insures it

• Bank can go bankrupt

—

Your stablecoin wallet:

• You hold the key

• Nobody can block access

• You are your own bank

• No middleman to fail

So is it safe?

Yes — with one important condition. The safety of your funds depends entirely on one thing: keeping your key (or recovery phrase) private and secure.

Your recovery phrase is a list of 12 words you get when you create a wallet. It's the master key. Whoever has those 12 words controls the wallet. That's it — that's the whole security model.

The one rule: Never share your 12-word recovery phrase with anyone. Not support staff, not family, not a website form. Anyone who has it owns your funds. Store it written on paper, offline, somewhere safe.

What are the real risks?

Risk: You lose your recovery phrase

How likely?: Medium

How to avoid it: Write it down, store offline

Risk: Someone tricks you into sharing it

How likely?: Medium

How to avoid it: Never share it with anyone

Risk: Your phone is hacked remotely

How likely?: Low

How to avoid it: Use a trusted wallet app

Risk: Stablecoin loses its $1 value

How likely?: Very low

How to avoid it: Use major coins: USDT, USDC

Risk: Someone steals your phone

How likely?: Low

How to avoid it: Wallet requires PIN or face ID

Notice what's not on that list: the blockchain going down, the stablecoin company disappearing overnight, or a government freezing your wallet. These are theoretical concerns, but in practice they're extremely rare for major stablecoins like USDT and USDC.

How does this compare to a bank?

Banks are insured by governments — in the US up to $250,000 per account. That's a real safety net that crypto doesn't have. So for very large amounts, a bank offers protection that no wallet can match.

But banks can freeze your account, go bankrupt, or simply be unavailable. A self-custody wallet has none of those weaknesses — as long as you guard your recovery phrase, nobody can touch your funds.

Simple version: A stablecoin wallet is like a personal safe. The bank is like a safe deposit box at a bank branch. Both can hold your money securely — but only you have the key to your personal safe.

What this means day to day

• You own your money directly — no bank holds it for you.

• Your 12-word phrase is your only master key — protect it like cash.

• No one can freeze, block, or take your funds without that phrase.

• For everyday amounts, a well-kept wallet is genuinely safe.

Bottom line: Storing money in stablecoins is safe — if you take care of your recovery phrase. That one responsibility is the trade-off for being your own bank. Most people find it simpler than they expected.

#VAULTwallet #EasyStablecoins #StablecoinWalletForYourMom

1

16

3,100

May 7

What happens when you click "Send" on a stablecoin transfer?

Let's break it down step by step and answer the question nobody wants to ask: can you get it back?

—

Sending money via a bank feels safe. You type a number, hit confirm, and know that if something goes wrong, the bank can help. Stablecoins are different — faster, cheaper, simpler — but there's a key difference that surprises new users.

—

From your wallet to theirs — in seconds:

When you tap "Send" in VAULT, here's what happens behind the scenes:

• Step 1: You confirm the transfer. Enter the amount and recipient's address, then tap Send. Your wallet signs the transaction — like a digital signature on a check.

• Step 2: The network picks it up. Your transaction is broadcast to the blockchain — a public record maintained by thousands of computers worldwide. (Takes a few seconds)

• Step 3: It gets confirmed. The network verifies you have the funds and the transaction is valid. Once confirmed, it's added to the permanent record. (Usually under 30 seconds)

• Step 4: The money arrives. The recipient's wallet balance updates. No clearing house, no business days, no middleman. (Done.)

Key analogy: It's closer to handing someone cash in person than sending a bank wire. The moment it leaves your hand, it's theirs.

—

Can you reverse it?

The honest answer: No.

Once a stablecoin transaction is confirmed, it cannot be reversed, cancelled, or recalled — by you, by VAULT, or by anyone. There's no "undo" button, no support line to freeze it mid-flight.

This might sound alarming, but consider the flip side: when someone sends you money, it arrives immediately and permanently. Nobody can take it back without your permission. That's a feature — it makes stablecoins trustworthy for receiving payments.

—

Comparing bank transfers and stablecoin sends:

• Speed: Bank takes 1-3 business days (slow); Stablecoin takes under 30 seconds (instant).

• Fees: Bank charges $10-$50 for international; Stablecoin costs a few cents.

• Reversibility: Bank can freeze, reverse, or delay (reversible); Stablecoin is permanent once confirmed (irreversible).

• Availability: Bank is closed weekends and holidays; Stablecoin works 24 hours, 7 days a week.

—

The one thing to always double-check:

Since there's no reversal, the address matters — a lot. An address is a long string of letters and numbers identifying a wallet. Copy it correctly, and the money arrives instantly. Mistype even one character, and the money goes nowhere useful — and won't come back.

Good habit: Always copy-paste the address — never type it by hand. Before sending a large amount to someone new, send $1 first as a test. Wait for it to arrive, then send the rest.

—

Why this is actually fine:

Once you know the rules, using stablecoins feels natural. Check the address, confirm, send. It works every time, in seconds, for almost no cost. Most daily users say they'd never go back to waiting three days for a wire.

Key takeaways:

• Sending is instant — no waiting, no business days.

• There are no middlemen who can block or delay your transfer.

• Transactions can't be reversed — so double-check the address first.

• When in doubt, send a small test amount before the full sum.

Clicking "Send" is like handing over cash — it's fast, final, and goes directly to the person you chose. Check once, send with confidence.

#Stablecoins #CryptoWallet #VAULTwallet #Blockchain #DigitalPayments

1

12

4,201

May 5

What Can Go Wrong with Stablecoins — And How to Avoid It

Using stablecoins is genuinely simple, but small mistakes can have big consequences. The good news? Every error is predictable and avoidable. Here's a quick guide to the five key mistakes new users make — and how to steer clear of them. Read once, never forget.

—

The Five Mistakes — And How to Fix Them

• Mistake 1: Sending to the Wrong Address (High Risk)

A wallet address is a long string of letters and numbers. One wrong character, and your money goes to a stranger — or vanishes. No undo. No support can help.

Fix: Always copy-paste the address. Never type manually. For large amounts, send $1 as a test first, confirm it arrived, then send the rest.

• Mistake 2: Losing Your Recovery Phrase (High Risk)

Your 12-word recovery phrase is the only key to your wallet. If your phone is lost or stolen, those words are your only way back in. Lose them — lose your funds. Forever.

Fix: Write the phrase on paper, not in a notes app or email. Store it safely — a drawer or fireproof envelope, like any vital document.

• Mistake 3: Sharing Your Recovery Phrase (High Risk)

Scammers pose as support staff, asking for your 12 words to "verify" or "fix" issues. Share them, and your wallet is emptied instantly. Real support never asks for this.

Fix: Treat it like a PIN. No app, agent, or website should request it. If they do, it's a scam. Close the window and walk away.

• Mistake 4: Sending on the Wrong Network (Medium Risk)

USDT travels on different "roads" like Tron, Ethereum, or Solana. Send on one, but if the recipient's wallet uses another, the money doesn't arrive.

Fix: Confirm the network with the recipient before sending. Ask: "Which network should I use?" VAULT shows the network clearly on every send screen.

• Mistake 5: Falling for Fake Wallet Apps or Websites (Medium Risk)

Scammers create fake apps or lookalike sites to steal funds or phrases. They can look identical to the real thing.

Fix: Download only from official app stores or websites. Bookmark the real URL. Ignore links from messages or ads — go straight to the source.

—

Your Quick Safety Checklist

Tick these off once, and you're set up safely:

• I wrote my 12-word recovery phrase on paper and stored it safely.

• I never entered my phrase anywhere online or in any app.

• I always copy-paste addresses and double-check the first and last 4 characters.

• I confirm the network with the recipient before every new transfer.

• I downloaded VAULT only from the official source — not a link or ad.

—

The Reassuring Part

Look at this list again. Every mistake is under your control — not the tech. The blockchain doesn't break. USDT doesn't lose value randomly. Risks aren't hidden; they're specific and avoidable. Most regular users say after a few transactions, it becomes routine: Check the address. Send. Done.

Bottom Line: Mistakes are real, but they're human errors, not system failures. Know these five, follow the checklist once, and you'll avoid 99% of what can go wrong.

#Stablecoins #CryptoSafety #VAULTwallet #CryptoTips #BeginnerCrypto

2

1

23

4,075

May 4

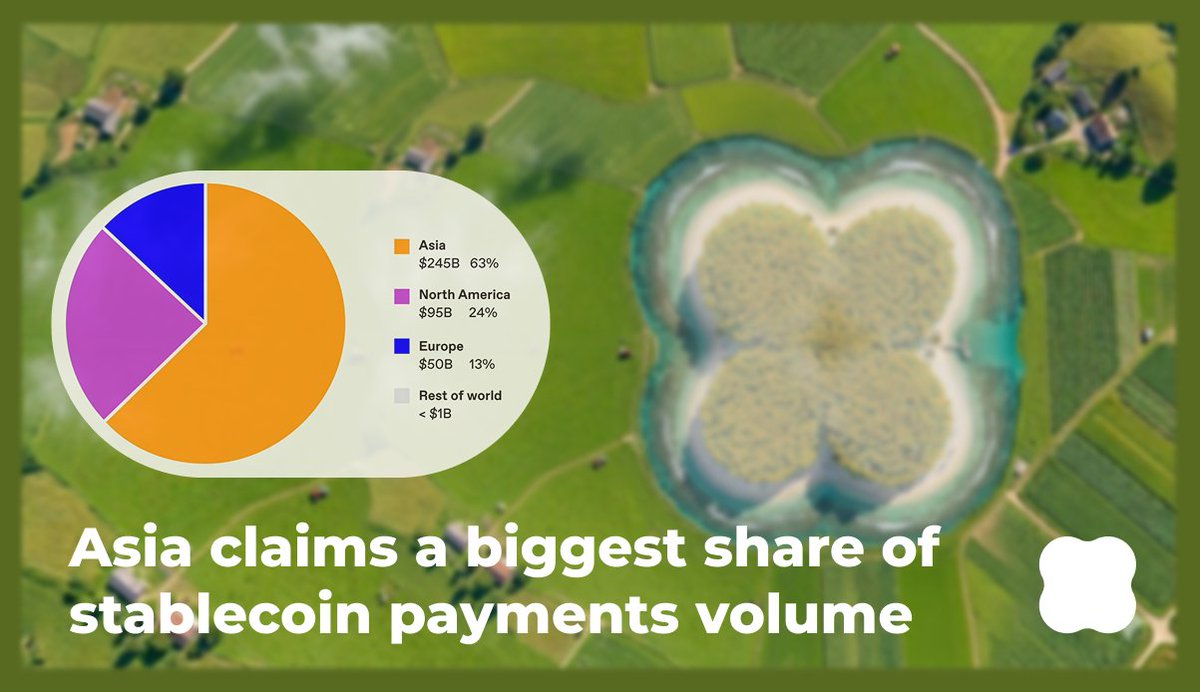

Stablecoins are no longer a niche experiment, they’ve already surpassed traditional giants like

@Visa

and

@Mastercard

in total payment volume.

And what’s even more telling is where this activity is happening.

It’s not evenly distributed.

In fact, the growth is being driven far beyond the “native” regions of traditional finance.

Nearly two-thirds of all stablecoin transaction volume comes from Asia — with key hubs like Singapore, Hong Kong, and Japan leading the charge.

This isn’t accident. It reflects real demand: – faster cross-border settlement – access to dollar-denominated liquidity – reduced dependency on legacy banking infrastructure

The implication is simple: Stablecoins aren’t just competing with traditional payment rails — in many parts of the world, they’ve already replaced them. Shot out to @a16zcrypto for highlighting

2

3

24

3,400

May 3

Sending money is just sending a message.

And the fee?

It's a stamp — not a bank charge. Here's why it exists, and why it's almost nothing.

—

When you send $200 to a friend via a bank wire, you pay a fee. Sometimes $15. Sometimes $40. It feels like the bank taking a cut.

With stablecoins, there's also a small fee. But it works completely differently — and once you understand it, you'll see why it's almost nothing compared to what banks charge.

— Sending money is literally sending a message —

When you tap "Send" in VAULT, your wallet sends a message to the blockchain that says — "Move 200 USDT from my address to this address."

That's it. A message.

Think of it like a postcard — except instead of going to a post office, it goes to a global network of computers that reads it, confirms it's real, and updates the record.

How your transfer travels:

Your wallet → The network → Their wallet

Message sent → Verified → Delivered. Usually under 30 seconds.

No banks. No clearing houses. No human processing. Just computers, confirming your message and delivering it — around the clock, every day of the year.

— So why is there a fee at all? —

Those computers don't run for free. The people who run them — and keep the network secure — are paid a tiny fee for every transaction they process. That fee goes directly to them, not to any company.

Think of it like a postage stamp. You're not paying the post office for profit — you're paying for the delivery service itself. The stamp covers the cost of moving your letter from A to B.

The key difference: A bank fee goes to the bank. A crypto network fee goes to the network itself — the infrastructure that makes the transfer happen. No middleman takes a cut.

— How much does it actually cost? —

Let's compare a bank wire vs. stablecoin for sending $500:

• Bank wire fee: $25.00 (5.0% of transfer)

• Stablecoin fee: ~$0.05 (0.01% of transfer)

— Does the fee change? —

Yes — slightly, depending on which "road" you use to send. USDT can travel on different networks, each with its own fee level.

• Network: Tron (TRC-20)

Typical fee: ~$0.01 – $0.10

Speed: Under 1 minute

• Network: Solana

Typical fee: ~$0.001

Speed: Under 5 seconds

• Network: Ethereum (ERC-20)

Typical fee: $1 – $10

Speed: 1 – 5 minutes

For everyday transfers, most people choose Tron or Solana — both are fast, reliable, and cost almost nothing. VAULT shows you the fee clearly before you confirm.

— The fee never scales with the amount —

Banks quietly never tell you this: Sending $50,000 via stablecoin costs the same fee as sending $50. The network only charges for the computing work of processing the message.

A bank charges a percentage, or a flat fee that assumes you're paying for their infrastructure, staff, and profit. A network fee is purely operational — and tiny.

Bottom line: The fee exists to pay the computers that deliver your money. It's a stamp, not a bank charge — usually just a few cents, fixed regardless of how much you send.

What is it:

• Your transfer is a message; the fee pays for delivery.

• No bank takes a cut — the fee goes to the network itself.

• Typical cost: a few cents, not $25.

• The fee stays flat whether you send $5 or $50,000.

#VAULTwallet #Stablecoins #CryptoFees #MoneyTransfer

11

1

24

3,046

Apr 30

What is a stablecoin, really?

Crypto that actually stays at $1 — and why that changes everything.

—

You've probably heard the word "crypto" and thought: too risky, too confusing, too volatile. And honestly? You'd be right — for most crypto. Bitcoin can drop 30% in a week. That's not money, that's a rollercoaster.

But there's a different kind of crypto that most people don't know about. One that was designed to not go up and down. It's called a stablecoin.

Think of it like digital dollars

A stablecoin is a type of cryptocurrency that is always worth exactly $1. Not approximately. Not usually. Always — by design.

If you have 50 stablecoins today, you have $50. Tomorrow, you still have $50. Next month — still $50.

Simple version: A stablecoin is like a dollar bill, except it lives on the internet and you can send it to anyone, anywhere, instantly — without a bank.

—

Why doesn't the price move?

The companies that create stablecoins keep real dollars in a bank account to back them up. For every stablecoin in circulation, there is one actual dollar sitting somewhere as a reserve.

So when you hold a stablecoin, you're essentially holding a digital receipt that says: "This is worth $1, and there's a real dollar that proves it."

—

Two real-life examples

Example 1 — Sending money abroad

Your daughter lives in another country. You want to send her $200. With a bank wire, it takes 3 days and costs $25 in fees. With a stablecoin, you send 200 digital dollars in about 30 seconds, and the fee is a few cents.

Example 2 — Saving without a bank

You keep $500 in stablecoins in a digital wallet. No bank account needed, no paperwork. The value stays exactly at $500 — it doesn't shrink, it doesn't spike. Just sits there, like cash in an envelope.

—

Why does this matter to you?

• It's as stable as cash — but works anywhere in the world, 24/7.

• You don't need a bank, a credit card, or a wire transfer.

• You stay in control of your own money.

• No volatility. No surprises. No rollercoaster.

Stablecoins are how crypto finally becomes useful for everyday people — not just for traders and tech enthusiasts. They're the "boring" part of crypto, and boring is exactly what you want when it's your money.

A stablecoin is digital cash. Same value as a dollar. Easier to send than a wire. No bank required. That's it.

#VAULTwallet #EasyStablecoins #StablecoinWalletForYourMom

1

1

24

3,384

Apr 28

New network coming to VAULT soon 👀👀👀

Cooking…

Even your parents might stop asking “did it go through?” every 5 minutes.

2

24

1,217

Apr 27

Private USDT on Bitcoin: How Utexo Built This?

@utexocom is building a stack where USDT moves on Bitcoin, but nothing is visible from the outside. Here is how they use RGB and Lightning to achieve it.

Private USDT on Bitcoin: How Utexo Built This

If you've ever moved stables on a public chain, you know the feeling. Any chainalysis bot, any competitor, any bored analyst opens the explorer and sees your entire flow. Payroll, vendor settlements, inter-exchange transfers - all on display. Privacy here isn't about paranoia, it's basic operational hygiene.

Utexo is building a stack where USDT moves on Bitcoin, but nothing is visible from the outside.

The transaction never hits the chain

With an EVM token you send, the whole network writes it down. Everyone running a node stores your transfer. The explorer just makes it readable. RGB Protocol is built differently. Transaction details, who's sending, to whom, how much, live only between sender and receiver. What goes to Bitcoin is just a cryptographic proof that something happened, without content.

Like signing a private contract instead of running a public auction, and only logging the contract number in the registry. What's inside stays private.

RGB calls this Client-Side Validation. The network stops being a witness to your transactions.

The sender doesn't know where it actually went

CSV covers the content, but not everything: the sender can still see the output UTXO. Utexo closes that gap with Blinded UTXOs.

The receiver generates a blinded reference to their address with a cryptographic secret inside. The sender pushes the transfer to that reference without knowing the real destination address.

In multi-hop setups, PSPs, exchange settlements, iGaming payouts, each participant in the chain sees only the next hop.

Lightning hides the fact that money moved at all

Lightning Network adds the final layer. In the Bitcoin chain, only two events are visible: channel open and channel close. Everything that happens between them stays inside.

A thousand USDT payments can move between those two points and not one of them shows up on-chain.

Where it actually gets slippery

RGB drags along an uncomfortable mechanic. With a normal token, the blockchain stores your history for you. With Client-Side Validation, you store it yourself. Lose your validation data and you lose access to your assets. There's no global state to back you up.

Utexo handles this through Tether WDK: RGB keys are derived from a standard BIP-39 seed phrase, validation data is encrypted and backed up locally.

RGB took a long time getting to production. Corporates who need to trust infrastructure with real payroll or vendor settlements aren't rushing. The stack looks solid, but that conversation happens after the first real tracks show up.

2

2

22

2,306