Joined June 2025

- Tweets 252

- Following 4

- Followers 351

- Likes 560

23 Photos and videos

Pinned Tweet

May 7

Businesses no longer need a new payment system

to accept stablecoins.

We’ve raised strategic investment from @movement_xyz on this bet

Just add stablecoins. Keep everything else

go: stableyard.fi

53

26

159

19,689

Jun 1

Crypto payments without crypto

5

131

May 21

Live in Vietnam 🇻🇳 & Thailand 🇹🇭

Only app you need

for your everyday spending with crypto.

go: testflight.apple.com/join/GZ…

May 21

Pay to any QR code with crypto 🇻🇳🇹🇭

>self-custody

>fiat settlement

>fully compliant

>works with all local QR codes

>one name for all chain addresses

Test flight access is LIVE in Vietnam and Thailand

(comment "DOPE" for Android access)

testflight.apple.com/join/GZ…

4

13

557

May 18

1200 dopetags have been secured

don’t let other people steal your cool username

Secure it now for all your payment needs

waitlist.dopepay.me/

One username for every chain address

May 13

Fuck 7 cards, 2 currencies & 20 wallets.

Just use DopePay.

→Scan/Tap & pay anywhere with crypto

→Pay with cool names, not wallet addresses

→Expense tracking & auto subs

→Self-custody

→ Global

Secure your dope tag :

waitlist.dopepay.me/

One app for every payment.

2

2

16

565

May 13

Our first product is live.

One app for all your payments.

Go secure your unique @.DopeTag now before they run out.

waitlist.dopepay.me/

May 13

Fuck 7 cards, 2 currencies & 20 wallets.

Just use DopePay.

→Scan/Tap & pay anywhere with crypto

→Pay with cool names, not wallet addresses

→Expense tracking & auto subs

→Self-custody

→ Global

Secure your dope tag :

waitlist.dopepay.me/

One app for every payment.

1

14

393

May 13

Who's calling that shii 👀

8

243

stableyard retweeted

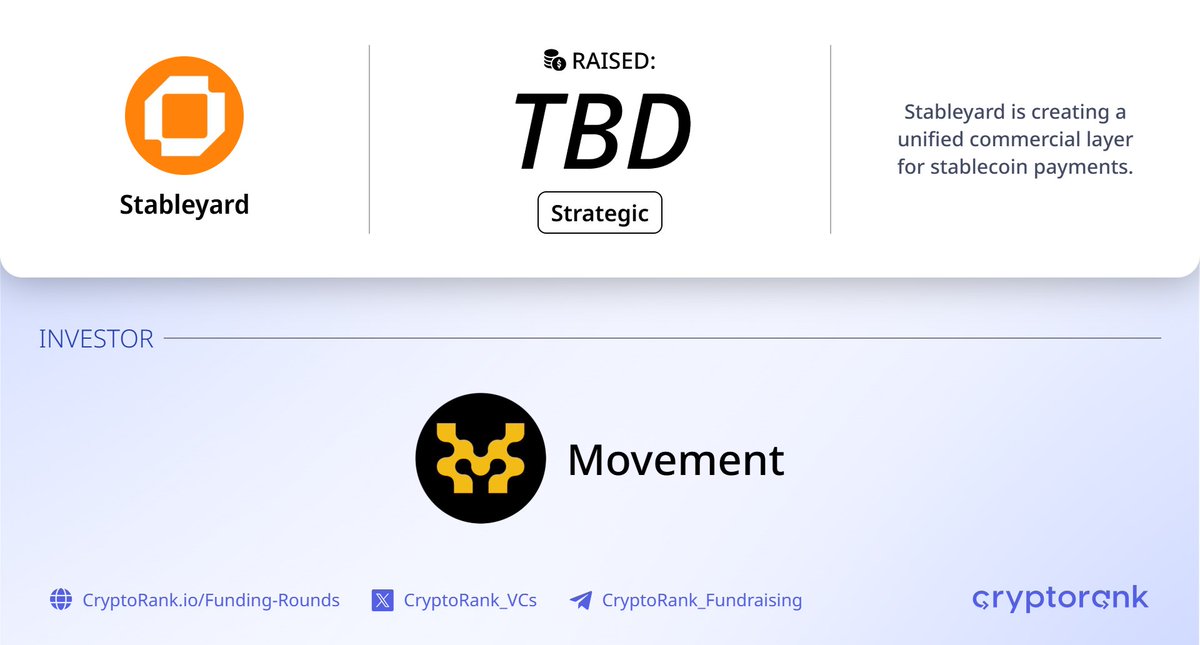

Stableyard Strategic Round⚡️

📑 About:

@stableyardfi is creating a unified commercial layer for stablecoin payments.

🤝 Investor:

@movement_xyz

ALT Stableyard Strategic Round

2

1

33

3,090

stableyard retweeted

May 10

Good morning and have a solid weekend everyone!

I am coming in fast with some news today

And this one is actually worth a closer look

Especially because it connects stablecoins

With how the financial world is starting to look at Web3

Stablecoins already proved they can move serious size onchain

But the real shift is not only about volume

It is about making them work inside normal payments

That is why @movement_xyz investing in @stableyardfi feels important

Stableyard is building full-stack infrastructure for stablecoin commerce

Not just another checkout button

Not another isolated payment tool

The project helps payment companies, fintechs, neobanks and merchants accept stablecoins without rebuilding their whole stack

A user can pay from any wallet

Stableyard handles the routing

The merchant receives funds in the currency and flow they need

That is the layer crypto has been missing

Infrastructure that works quietly in the background

While stablecoins start feeling more like normal money

Movement is backing Stableyard with more than capital

They are also helping with merchant introductions, ecosystem connections and checkout integration for Movement-native apps

DopePay makes the idea even easier to understand

Scan a QR

Tap the phone

Pay with stablecoins

No wallet switching

No chain selection

No extra friction

This is how real adoption moves

Not by making people study every chain

But by making crypto simple enough to use without thinking about it

Stablecoins already became infrastructure

Stableyard is working to make them feel like money

May 7

Today we're announcing a significant strategic investment in Stableyard to support the expansion of their full-stack stablecoin payments tooling that makes money move better.

It works for real people and real businesses.

Follow them for updates: @stableyardfi

75

2

113

1,304

stableyard retweeted

May 10

The stablecoin payments race has a new contender worth watching.

And no, this isn’t another “we’re disrupting payments” pitch deck.

It confirmed what the builders already knew.

We all are familiar with the usual payments problem.

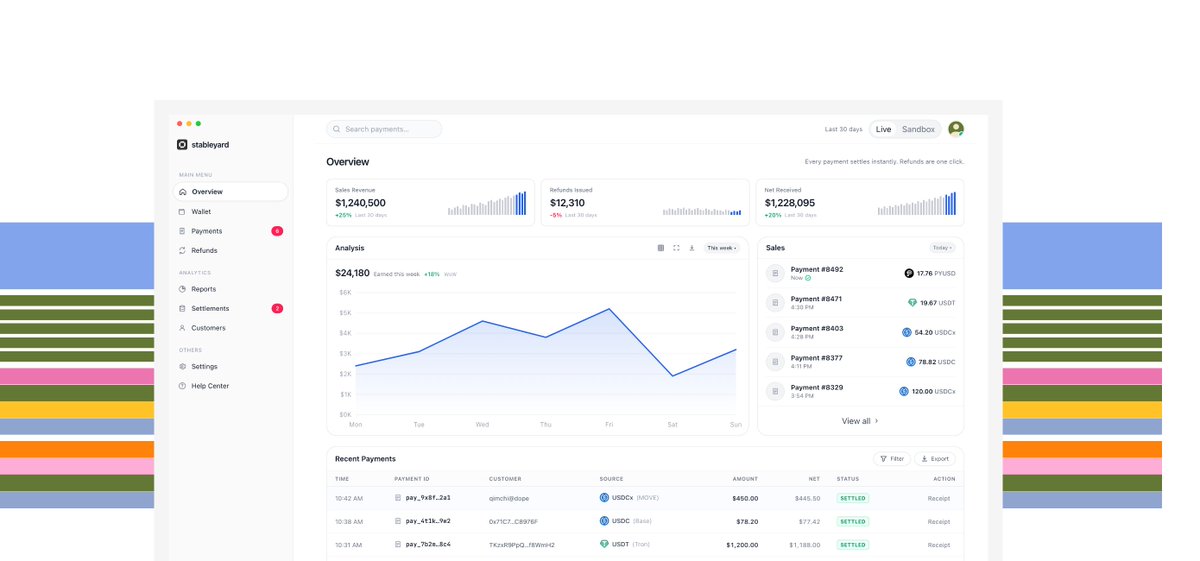

The Card rails bleed merchants 2.5 to 3.5% per transaction, then Settlement takes days, and Chargebacks are a nightmare to behold. Cross border? They are damn Expensive and slow by design.

Stableyard made a significant shift in the ecosystem

This guys are never replacing your checkout, neither Keep your POS, your website or your app.

They did added one integration.

Customers pay in USDC, USDT, PYUSD across 60 currencies and 8 chains from wallets they already use.

Then Merchants get instant on chain settlement, flat 1% fee, acclaimed one click refunds, and full self custody.

Stableyard never touches your keys. That’s the moat.

Programmable rules for limits, splits, approvals, yields. Non-custodial vaults. POS apps, QR codes, NFC cards, SDK widgets. And agentic payments via x402plus for the builders paying attention.

Let me break you a context first.

BVNK built enterprise grade stablecoin infra starting 2021.

In which Cross border payments, treasury tools, compliance baked in.

By 2025 to 2026 they were moving tens of billions across 130 countries. March 2026, Mastercard acquired them for up to $1.8 billion.

Not hype. Validation.

Stablecoins moved $33T on-chain recently. Boston Consulting Group broke down $26T in stablecoin volume. 92% was crypto-native. Only 8% was actual payments and B2B use.

That gap gives the entire opportunity for a full fledged evolvement

Most of CT is sleeping on it because there’s no direct token to ape. But the infrastructure being built right now is exactly what captures that shift when it flips.

Movement’s strategic investment announced May 7, 2026 gives Stableyard capital, merchant intros, network routing, and deep integration on a high-performance L1 built for this exact use case. Same rocket fuel that separated BVNK from the rest early on.

The difference between Stableyard and what BVNK built? BVNK went full enterprise orchestration, perfect for big PSPs and treasuries. Stableyard is the accessible layer.

Seamless indeed, Self custody, plug and play, no heavy KYC upfront. Built for the long tail. Shops, SaaS, creators, hospitality, Web3 projects.

The ones bleeding margin to Stripe and Visa right now.

Early traction in Southeast Asia. Savings calculator showing merchants keeping ~2% more vs cards. Volume metrics trending up over the last 30 days.

BVNK went from startup to $1.8B exit in roughly 5 years by nailing infrastructure and compliance. Stableyard is running the same thesis. Non custodial moat, real merchant pain, serious backing.

If you’re a merchant head to stableyard dot fi, run the numbers on what you’re losing to card fees right now.

If you’re a builder or investor watching the payments layer get rebuilt in real time, the picks and shovels play is right in front of you.

Because The 8% becomes 30%. Then 50%. The infrastructure capturing that shift is being built today.

@stableyardfi is actually one of them.

x.com/octop3s/status/2053512…

and the revolution has already begun.

this week alone, here are some chain/neobank-related launches and funding rounds:

• movement backed @stableyardfi with a strategic investment building new ways for businesses to accept stablecoin payments.

• megaeth announced its upcoming wallet, m(os)s, which i presume will have built-in neobank features to bootstrap their usdm stablecoin.

• solana and its founder participated in another raise for @multisig to build neobank infrastructure for individuals and businesses.

• sui’s largest wallet, @slushwallet, announced its crypto card in collaboration with @redotpay.

slowly but surely, everything is coming together.

1

2

9

1,128

May 8

-POS

-QR codes

-Payment SDKs

-Self-checkouts

-Online checkouts

-In-person payments

-Deposits & treasury management

-Agentic payments with x402plus and MPPx

-Single unified payment identity & vaults

All from just one integration, without any crypto complexity or new systems.

May 7

Businesses no longer need a new payment system

to accept stablecoins.

We’ve raised strategic investment from @movement_xyz on this bet

Just add stablecoins. Keep everything else

go: stableyard.fi

4

4

22

1,088

May 8

for real people and real businesses🤝

move is for real and better money

May 7

Today we're announcing a significant strategic investment in Stableyard to support the expansion of their full-stack stablecoin payments tooling that makes money move better.

It works for real people and real businesses.

Follow them for updates: @stableyardfi

1

2

19

445

stableyard retweeted

May 7

Businesses no longer need a new payment system

to accept stablecoins.

We’ve raised strategic investment from @movement_xyz on this bet

Just add stablecoins. Keep everything else

go: stableyard.fi

53

26

159

19,689

May 7

Businesses no longer need a new payment system

to accept stablecoins.

We’ve raised strategic investment from @movement_xyz on this bet

Just add stablecoins. Keep everything else

go: stableyard.fi

53

26

159

19,689

May 7

@stableyardfi is bridging that gap.

A Unified commerce layer for stablecoin payments from checkout to settlement, designed to make stablecoins work like money:

→ checkout → settlement (end-to-end)

→ payment identity (like a bank account, but native)

→ agentic commerce (payments that execute themselves)

→ experience layer (feels like web2, not crypto)

→ cross-chain routing (user doesn’t think, it just works)

2

13

586

May 7

Stablecoins have won as a better infrastructure

Now, we make them better money.

Welcome to the better commerce, @stableyardfi 🤝

Don’t change. Upgrade what already works:

stableyard.fi

More on the strategic investment here:

movementnetwork.xyz/article/…

For more info on Stableyard check- stableyard.fi/blog/movement-…

1

12

536

Apr 9

IT JUST WORKS!

DOPE!

Apr 9

Crypto Payments in 2025:

>Multiple wallets and cards

>Bridging across chains

>Offramping to fiat

>Wallet addresses

>Begging merchants to accept crypto

>Still can't buy coffee

Crypto Payments with DopePay:

>Scan. Tap. Pay.

IT JUST WORKS

6

204

stableyard retweeted

Apr 8

> be @dopepayme

>super payments app

> fix broken payments

> scan/tap. pay. done.

> Global P2P payments

> Works on any QR or POS

> Simple to use, like Apple Pay

> Give users one unified payment ID

> Send money to names like claudelover@dope instead of wallet addresses

hit me up for early 200 exclusive testing access in Vietnam

7

7

24

1,321

stableyard retweeted

Mar 31

this is exactly the kind of thing that’s been bothering me

we’ve known this problem for years

yet a new user still can’t do a basic transaction without hitting “you need ETH for gas”

no one outside crypto cares about:

ETH

gas

which chain they’re on

they just want to use their money

this is what’s actually holding stablecoins back for real users

not infra, not narratives, just basic usability

i care deeply about this, and we’ve taken this seriously while building @stableyardfi and @dopepayme

the goal is simple:

users should never have to second guess what to do next

doesn’t matter if someone comes from mars, uranus, or anywhere

if they have money, they should be able to use it

no extra steps

no hidden requirements

no “figure it out yourself”

that’s the bar

and that’s what we’re building towards

Tried helping a friend w/ a first trade with @coinbase @base app. They set up Coinbase with usdc —> to their new base wallet. Learn they need eth to do a swap, even the swap to buy eth couldn’t use the usdc in their account! Crypto is still plagued with the worst user experience

1

5

321

Mar 28

Agents need infrastructure that works the way they do

programmable, autonomous, always on.

that's what we're building.

>treasury accounts for agents

>yield on idle funds

>money that moves on logic

the agentic economy starts with agentic money.

Mar 28

honestly the funding step is great but it still doesn’t make agents fully “Autonomous”.

imagine hiring 50 employees and personally handing each one cash every time they needed to buy something.

that’s what manual agent funding is.

it works at 1. it breaks at 10. it’s impossible at 100.

thats why

we’re building this at @stableyardfi combining OWS stableyard accounts:

— agents get native treasuries.

—idle funds earn yield automatically.

—agents send and receive between each other and humans.

—fully programmable money flows. no links. no clicks. no you.

we’re giving them a bank account.

agents need their own economy to be fully autonomous and we are giving them that.

5

181