Bitcoin Maxi. Deep Value Contrarian Investor. Don’t invest blindly. $GME

Joined June 2024

- Tweets 8,636

- Following 69

- Followers 1,443

- Likes 13,778

2,840 Photos and videos

Pinned Tweet

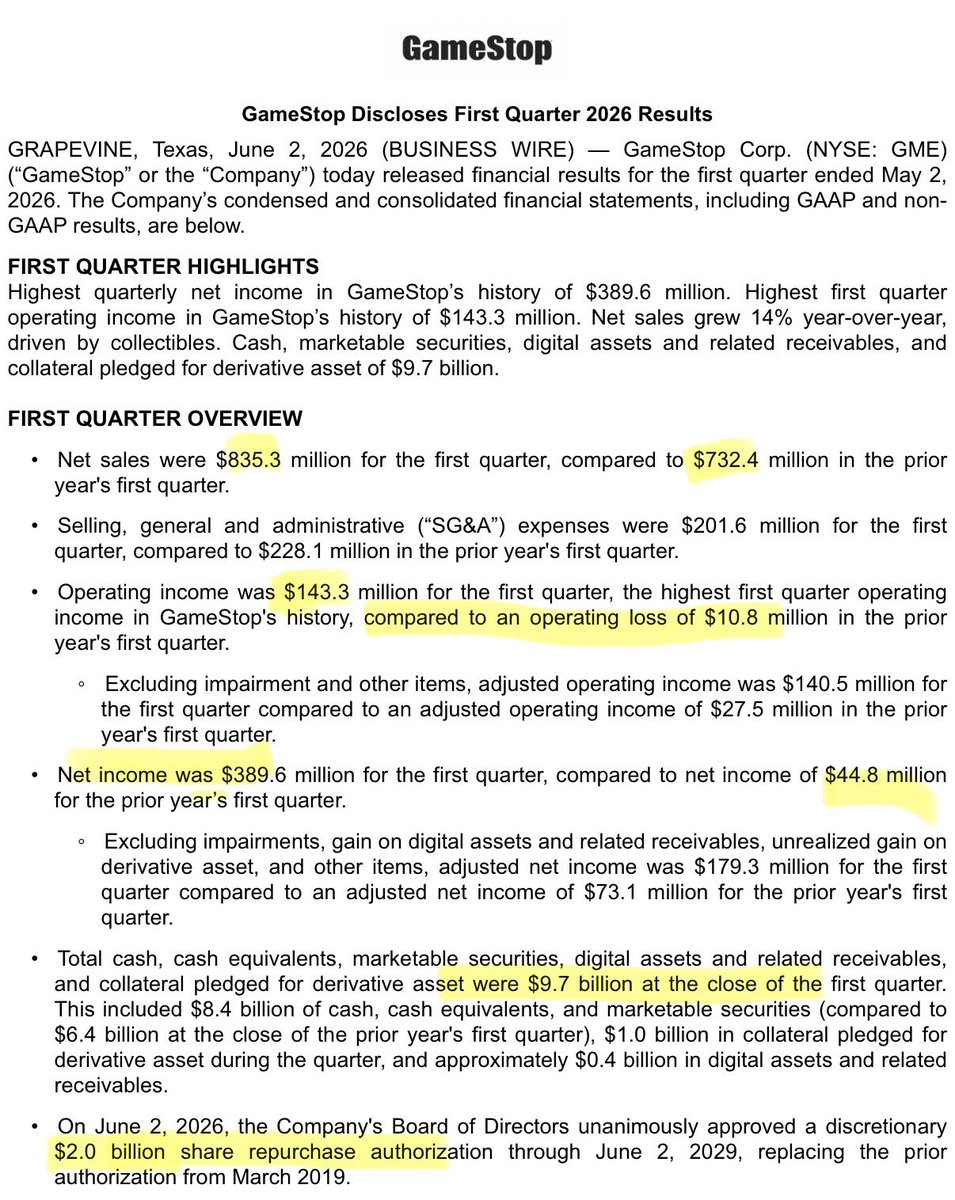

2026 $GME operating income prediction:

Q1: $143m ✅

Q2: $150m

Q3: $150m

Q4: $200m

Total ~$643m

A 177% YoY gain

I am being conservative. Q1 has always been their weakest quarter. Based on that retailer trend, Q2-Q4 could be respectably higher than stated above.

This does not include interest income or $EBAY derivatives gain.

Just my opinion based on fundamental data released by the company in quarterly earnings.

4

2

46

2,398

Stay Predictable retweeted

Yes it reads:

“Delaware allows this but I’m a little bitch and don’t like it so I want to complain.”

I’m surprised you can’t read little bitch, little bitch.

2

1

4

100

Stay Predictable retweeted

2 Nov 2025

Wait for the fat pitch.

135

169

1,294

178,069

This company is trading at $9.5B market cap with these fundamentals. And this is typically their worst quarter of the year.

There is no denying the overt suppression.

$GME

12

26

268

5,927

This is what you see when a lot of rich people who were in pre-IPO have their shares locked and are trying to keep the price propped up since only $85b of the $2.5T is able to sell right now.

Keep the good vibes going until they can sell their shares over the next 6 months.

Good company. Bogus valuation (today).

Many elite are in this pre-ipo. Any big purchases they show you in open market could be small in comparison to their pre-ipo position. They need it to stay up.

$SPCX

22h

🚨 BREAKING:

BILLIONAIRE RON BARON SAID LIVE ON CNBC:

"SPACEX IS GOING TO BE WORTH $10T, $20T, AND $30T, AND I COULD BE VERY LOW."

THIS MAN BOUGHT THE 2008 CRASH AND CONTROLS OVER $53 BILLION IN ASSETS

HE DEFINITELY KNOWS SOMETHING!!

1

3

18

1,462

Stay Predictable retweeted

Jun 15

Two and a Half Men S1E2 (2003)

32

705

11,976

309,289

Stay Predictable retweeted

Time to get that volcano lair I’ve always wanted.

I think it’s in the “Beyond” section of BB&B.

6

28

277

21,316

Stay Predictable retweeted

Jun 15

If a company retires its convertible debt, the delta-neutral hedge is shattered and the math changes instantly.

Conversion Ratio: 0

Delta: 0

Required Short Position: 0

To return to 0, funds are forced into the open market to cover every share they shorted against that debt. When a company retires billions in convertibles, it triggers a mandatory, mathematically enforced de-hedging event.

When that forced buying hits the market, the price has nowhere to go but up.

20

11

194

7,969

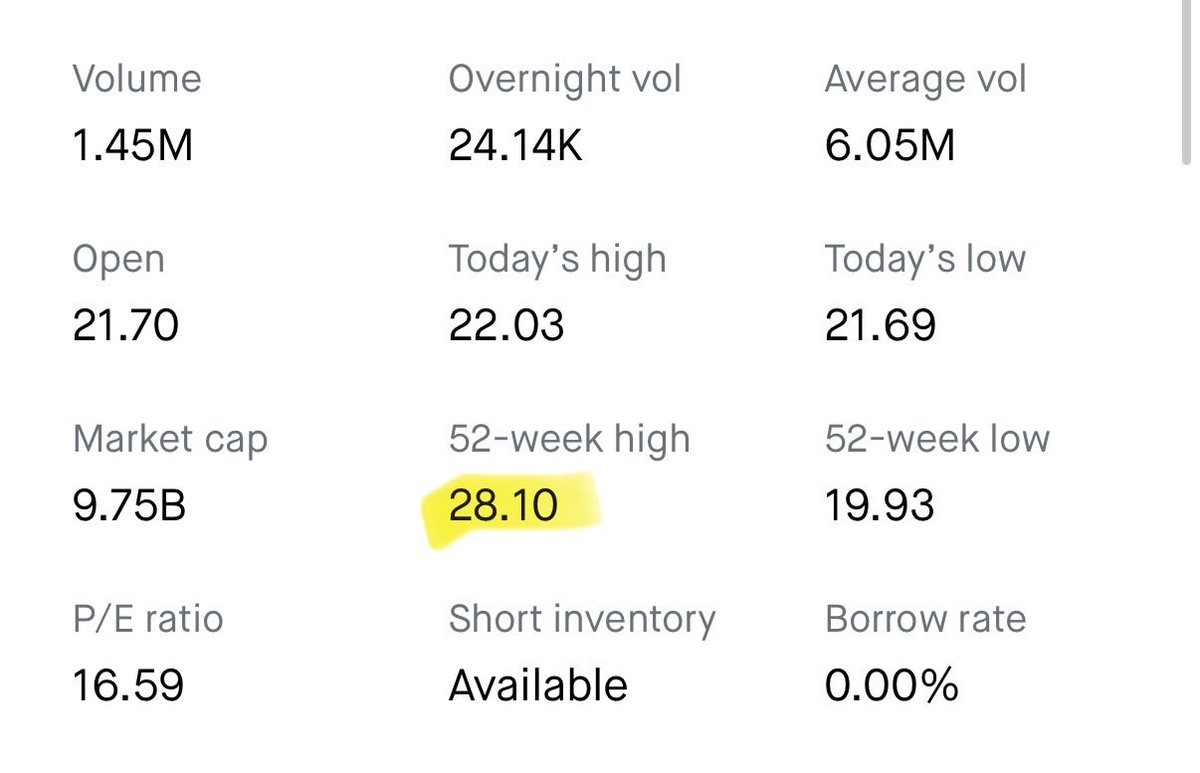

Jun 15

The $GME prices above $30 before the convertible notes in 2025 have officially dropped off the 52 week data.

52 week high is officially $28.10.

We have now reached the 1 year mark for both sets of convertible notes, although I am not sure of the exact date the restrictions are lifted off the second set of notes.

4

3

73

6,803

Jun 15

Time to get that volcano lair I’ve always wanted.

I think it’s in the “Beyond” section of BB&B.

11

518

Jun 15

RT @sierrastrades: $GME ROARING KITTY TURNED OFF HIS VPN!

THIS IS THE SIGNAL!

BUCKLE UP!

🌊🌊🌊

85

Jun 14

2

2

61

4,994

Jun 14

Hey @ryancohen, your Teddy.com website has been down for 2 weeks now.

I really want to buy some books. It’s not like you to let your products be inaccessible to customers.

You must be doing something important behind the scenes while the site is down?

$GME $EBAY

7

10

138

6,089

Stay Predictable retweeted

20 Mar 2025

Arabian dress look interesting

255

314

2,704

153,706

Stay Predictable retweeted

27 Mar 2025

What is the Next big move?!

279

260

2,987

131,239