Nomen est omen. Global investor. Looking for wide margin of safety. Accustomed to heavy volatility. Lifelong learner. Not investment advice.

Joined August 2020

- Tweets 825

- Following 120

- Followers 895

- Likes 2,286

73 Photos and videos

Time to close a small position in $FBIOP. Monetization of assets has brought this preferred stock back up from entry point of $5.2. Just shy of 300% return for a 20 month holding period is not too shabby. Thank you @chaka23121 and @LulevTrading for the idea and thesis!

25 Sep 2024

Started scooping up some $FBIOP. When preferred dividend gets reinstated, share price should move back to $17 range. You essentially get a 42% div yield on cost basis for buying and holding this (risky) stock. Looks too cheap to me. Insiders also added recently.

1

1

515

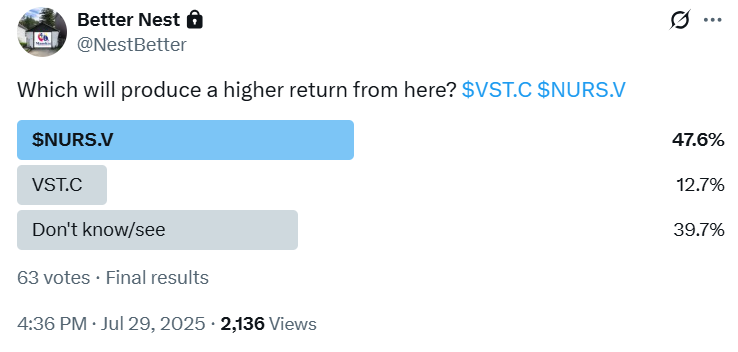

'At least $150M' $NURS revenue guidance could translate into 25, 35, 45 and $55M in revs for the four quarters, for a total of $160M this year. Say 15% net margins in Q4 and annualised would bring this to $33M exit-run rate earnings, i.e. 8x P/E at $5 share price.

1

1

8

936

Unfortunately, and I have to point this out, again no $NURS.v Q&A in the cc...it really seems mgmt is afraid of (my) questions! For a company intending to move to Nasdaq, these are very bad optics!

1

7

615

May 22

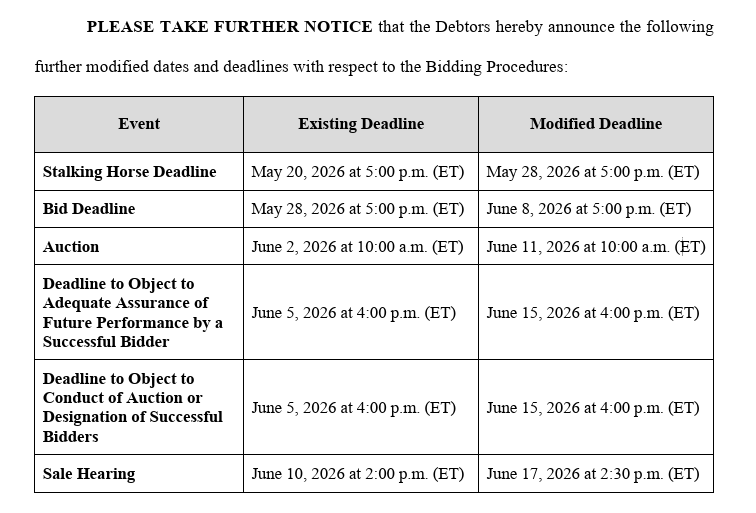

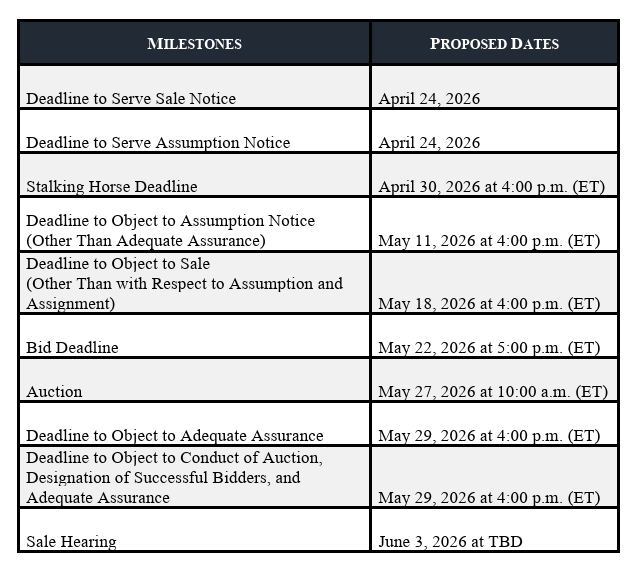

$FNCHQ stalking horse deadline and entire sale process is being delayed once again. Unclear to me if this is because of no interest from prospective buyers for a stalking horse role, or if the OpenBiome hearing is necessitating it. But more time for the judge to issue a decision!

Mar 29

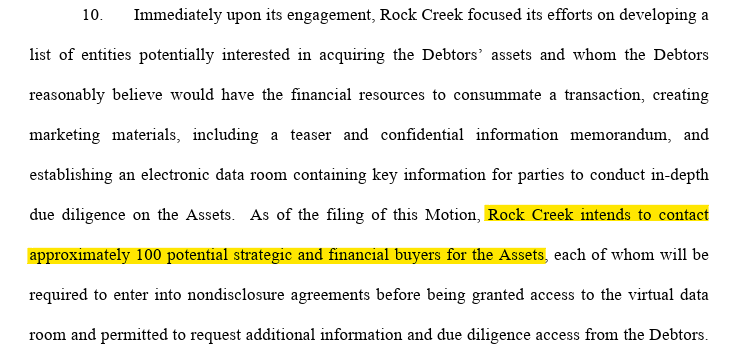

The more I look into $FNCH/ $FNCHQ, the more I like the current set-up. Sale timeline is very clear and short (two months), can be extended/terminated at any time (e.g. in case the post-trial motions verdict finally comes out), 100 possible buyers.

3

5

1,963

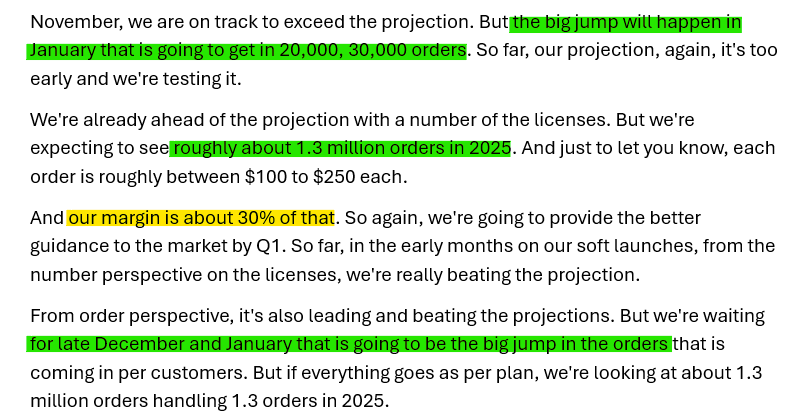

Did $NURS.v restate their licensee recognition methodology to get to 11K? My vibe coded python tool found 3550 licensees for DripBAR Direct alone (71 locations x 50 states). This client probably only accounted for 50 licensees in 2025 (because 'only' 2.5K at YE2025)! 🤨

Jan 15

Four months after an already unnecessary convertible offering ("big opp in next 30-60 days" didn't materialize), $NURS.v is AGAIN diluting, this time 5.56M shares in total, while already cashed up and presumably CF positive with 700K VSDHone orders/month.

2

6

5,259

Honestly not sure what to think about the webinar. A lot of talk about the evolution in the industry and one 'pumpy' slide on the new number of licensees at the end of Q1 2026. $NURS not fielding any questions at the end of the call was not appreciated by investors I'd imagine!

5

750

Mar 29

The more I look into $FNCH/ $FNCHQ, the more I like the current set-up. Sale timeline is very clear and short (two months), can be extended/terminated at any time (e.g. in case the post-trial motions verdict finally comes out), 100 possible buyers.

Mar 23

I wonder if $FNCH can 'leave' Chapter 11 once the lease has been rejected, or if they have to go through with the Bidding Procedure Motion and run the risk of having a low floor price that they can't escape. All in all they are forced to sell here.

2

2

4,635

Mar 23

Oct 2025: Ferring is forcing themselves to sell REBYOTA which must be great news for Finch! Stock 20%

March 2026: Finch is forcing itself to sell itself through court-supervised sale under Chapter 11. Stock -40%

Man what do I love public markets! $FNCH

Mar 23

I wonder if $FNCH can 'leave' Chapter 11 once the lease has been rejected, or if they have to go through with the Bidding Procedure Motion and run the risk of having a low floor price that they can't escape. All in all they are forced to sell here.

3

955

Mar 20

War in Iran seems far from over and the systemic risks from the prolonged closure of the Strait of Hormuz have yet to fully reverberate through the macro financial feedback loop. I have raised cash as this feels like the safest course of action at the present time.

6

355

Feb 15

Claude Code >>> ChatGPT for any vibe coding tools you want to build in Python!

I've finally decided to extensively use Claude for pro stuff

I can confidently say we're going back the world of Mme de Lafayette

The most important skill will be the art of conversation

Except it won't be conversation at court but with your AI. The rest will become irrelevant

1

469

Jan 28

And surprise, surprise, $LODE is diluting again at terms undefined in their press release. Bulls will always tell you the bull case, reality for the equity holders tells you a different story…

Jan 23

The reason Comstock is not up much in the past year is because mgmt diluted SHs by 30% a few months ago, and have a massive ATM in place. Why would you bid this up to then get smashed? I know so many people who would buy big amounts of stock if silver assets were sold! *If*

12

2,133

Jan 19

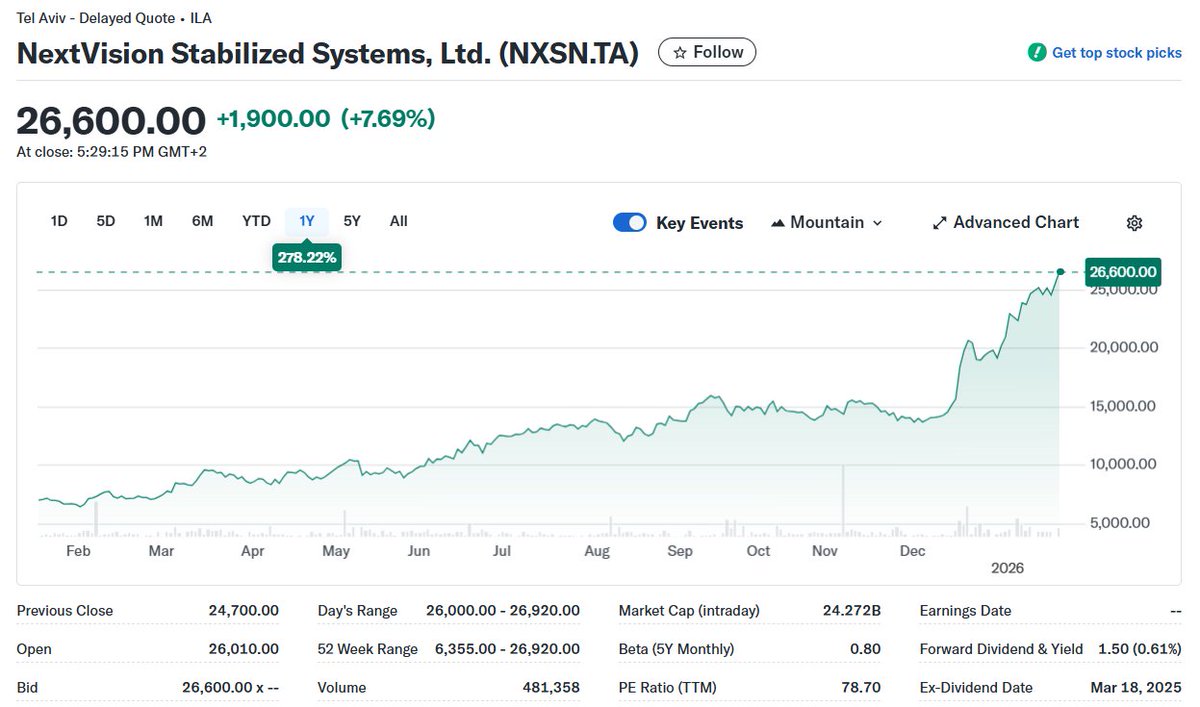

Absolutely phenomenal stock performance of $NXSN.TA over the past year. Getting a bit pricey but what a run it has been. Credits to @rubicon59 for bringing this name to my attention!

5 Mar 2025

$NXSN.TA slowly getting discovered: 35% YTD and still extremely cheap compared to other lower growth, higher capex military businesses in the US and Europe. Still only valued at 14.5x P/E on 2025 exit profits of $125M!

4

9,446

Jan 15

Four months after an already unnecessary convertible offering ("big opp in next 30-60 days" didn't materialize), $NURS.v is AGAIN diluting, this time 5.56M shares in total, while already cashed up and presumably CF positive with 700K VSDHone orders/month.

20 Aug 2025

$NURS.v Raising C$11.5M at a valuation of C$190M implies a HUGE cost of capital with guidance of 400K orders/day (and thus $700M mcap). Selling shares at C$3.82 when fair value is closer to C$13 is incredibly short-sighed move by mgmt: for value creation the ROI has to be huge.

2

1

11

4,657

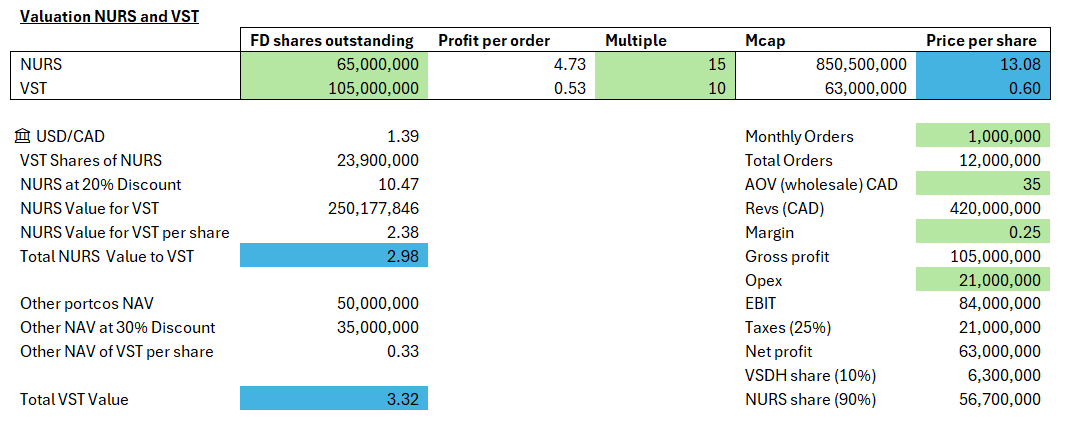

Jan 15

It is sad to say, but this raise again underlines the superiority of $VST.cn as a play for this investment thesis: the 10% VSDHone profit share is not diluted by this raise. Although VST will also tank tomorrow. Maybe a good time to initiate the buyback!

1

3

639

Jan 15

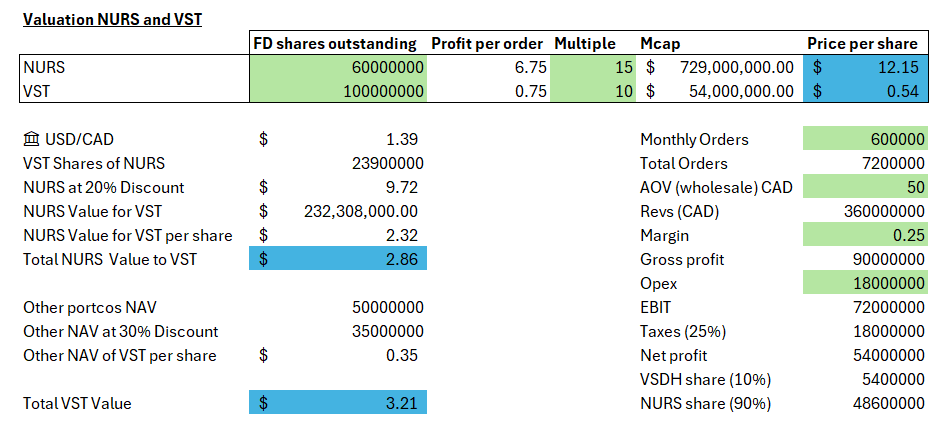

In conclusion, while I deplore this action by mgmt, the prospects for VSDHone are (as far as I know) unchanged and the share price should reflect that in the medium term. Let's revisit $VST.cn in 12 months. Still attractive as shown in my updated valuation sheet.

1

9

916

29 Dec 2025

Have no opinion on $SHMD's core biz, but the €10M convertible was shark financing: 15% interest rate, conversion at $2.15 (55% discount vs market price!), 2% 'arrangement' fee plus 1.25m 'incentive' call options (5Y @ $4.20) --> 6.3M shares dilution for €9.8M i.e. ~$1.55/share!

1

13

1,818