Notts County Councillor, Newstead Division. Shadow Cabinet Member for Finance at Notts CC. Newstead Abbey Ward Cllr at GBC. Chair Sherwood Forest Conservatives.

Joined February 2017

- Tweets 8,828

- Following 793

- Followers 315

- Likes 7,108

38 Photos and videos

Cllr Stuart Bestwick retweeted

Jun 9

Britain will over the coming months endure the biggest rise in unemployment of any major advanced economy.

That was the conclusion of the Organisation for Economic Co-operation and Development (OECD) last week, when it warned that UK joblessness will soar from 4.8pc last year to 5.5pc by the end of 2026.

When Labour took office in July 2024, unemployment was just 4.1pc. But the number of payrolled employees has since fallen in fourteen of the twenty-one subsequent months to April – with around 1.81 million now unemployed.

It is unusual, when the population is rising, for the number of payrolled jobs across the economy to fall.

But that pattern has been broken under Labour.

🧵1/8

98

984

2,144

108,631

Cllr Stuart Bestwick retweeted

Jun 7

Labour risks being forced to seek emergency help from the International Monetary Fund (IMF) as Britain lurches toward a debt crisis, leading economists are now warning.

Former IMF chief economist Ken Rogoff says, in a new interview, that there is “more than 50:50 chance” of a major UK debt crisis before the end of this decade.

He is joined by Sir Charlie Bean, a former senior official at both the Bank of England and the Office for Budget Responsibility, who says the need for an IMF bail-out is now a “material risk” for the British economy.

I not only firmly agree with Ken Rogoff and Sir Charlie Bean – but have been repeatedly issuing the very same warnings for a very long time.

Because the grave risk of a major fiscal meltdown has been apparent for at least the last two years – to anyone who combines serious knowledge of UK economics and politics and global debt markets with an open mind.

The UK's public finances were already fragile when Labour took office back in July 2024.

But this government's misguided, ideologically-driven statist policies have made a bad situation much worse, seriously increasing the danger of a deep fiscal crisis - which would cause a disastrous state funding shortfall and a very nasty inflation spike.

That would result in Downing Street being forced to follow the orders of unelected technocrats flown in from Washington and elsewhere.

It would be a very major national humiliation combined with a deep economic slump and an even more intense cost-of-living crisis – in which low-income households, as ever, would suffer the most.

Yet those of us that have shown the brains and courage to point out these inconvenient truths over recent months and years have long been dismissed and derided for our trouble - not only by ignorant politicians and approval-seeking journalists but also the overwhelming majority of "leading economists".

Ahead of the general election in mid-2024, with Labour on course to win, the conventional wisdom among the great sages of broadsheet journalism and the economics establishment was that "the adults would soon be back in charge" ... Labour would "get lucky with the economy" ... and "Britain would now enjoy an extended period of political and fiscal stability".

I thought that was total nonsense – not least as I was well aware Labour's plans irresponsibly to increase borrowing and spending would be met with deep scepticism by the global pensions funds, insurance companies and other institutional investors that lend governments serious money.

My weekly @Telegraph "Economic Agenda" column of 23rd June 2024, a fortnight ahead of the general election, was a total outlier. I recounted the disaster of 1976 – when Britain was forced to go "cap in hand" to the IMF for a bailout – and warned that "The Ghosts of the 1970s" would haunt Labour's (so-called) economic resurrection".

Six months later, after the October 2024 "Hallowen" budget in which Chancellor Rachel Reeves did indeed sharply hike borrowing and spending, I assessed the market reaction then doubled-down – warning more assertively in my column of 12th January 2025 that "The UK risks a return to 1976 unless Reeves changes course".

And then again on 20th July 2025, as Labour's policies raised the costs of doing business, translating into price pressures which pushed up government borrowing costs even more, I again cautioned that "Inflation risks are taking Britain to the debt-crisis cliff edge".

"It’s now screamingly obvious that Labour’s crude Keynesianism – “pump priming” the economy by upping state borrowing and spending – isn’t working," I wrote in that column last July.

"Worse than that, this Government’s actions are pushing Britain towards a budgetary crisis every bit as serious as that in 1976 – when the UK was forced to go “cap in hand” to the IMF for a bail-out".

It's been a lonely task issuing these warnings. I've been hounded in public debates, slagged off by senior civil servants and often dismissed by "leading economists" as "alarmist".

So what do these same "leading economists" now say to Rogoff (Harvard Professor, Former IMF Chief Economist) and Bean (LSE Professor and Former Deputy Governor of the Bank of England)?

The "economics establishment" – with very few honourable exceptions, the brilliant @jagjit_chadha among them – has been and remains extremely reluctant to point out the deeply unsustainable nature of this government's addiction to ever more borrowing.

The systemic fiscal dangers of evermore "tax and spend" – and the prospect of a serious spike in gilt yields and related fiscal meltdown – are now so real and present as to be completely undeniable.

Yet the UK government is about to shift even further to the left, pushing up borrowing and spending even more under a new leader, in a bid to appease the massed ranks of economic illiterates among Labour's Parliamentary party and activist base – making those dangers even more acute.

Yet, still, the silence among "public intellectual" economists is deafening.

I'm glad the likes of Ken Rogoff and Charlie Bean are now issuing clear warnings. So where is the rest of the "economics establishment" - those who purport to understand fiscal management and financial markets, and often funded by taxpayers' money?

Britain is now clearly in the crosshairs of a very serious danger. The government's creditors are increasingly fickle and based overseas – with no regulatory or cultural obligations to lend money to the UK government.

Those holding UK gilts are increasingly "speculative" rather than "strategic" long-term investors – looking for quick returns, financing their government bond purchases with "leverage" (money borrowed from elsewhere), which will quickly be withdrawn when senitment decisively shifts, causing a plunge in gilt prices and a sharp additional surge in government borrowing costs, setting up a vicious circle.

The UK government is very heavily indebted – and the global investors we rely on to bankroll a huge slice of our state spending are alarmed that of the £132bn the government borrowed last year, no less than £110bn was spent on debt interest – as I wrote in a column on 17th May 2026, "As Labour lurches further left, the markets are calling time".

Global investors are alarmed the UK has consistently had the highest inflation in the G7 (which pushes up borrowing costs) and has easily the highest share of index-linked debt (which magnifies the burden of inflation on the state's balance sheet).

And they are deeply, deeply alarmed that when Labour came to power in mid-2024, the Office for Budget Responsibility was forecasting additional state borrowing of £323bn by 2029, the scheduled end of this Parliament.

But Labour’s runaway spending and growth-crushing tax rises mean that the same five-year borrowing forecast is now £583bn – 80pc higher. And still, the trade unions, MPs and Labour activists who will choose Starmer’s successor now want even more.

It is not too late to pull the UK back from the fiscal brink, to avoid the extremely painful and deep, lingering damage of being forced to go to the IMF and perhaps other multi-lateral creditors for a bailout.

It is not too late to avoid the inflation surge, the currency crash, the shocking blow to consumer and business confidence alongside the sky-high interest rates that will seriously whack our economy – or the perhaps even deeper damage of yet more of the British electorate losing faith in the ability of our establishment to manage the country in a manner that avoids imposing serious hardship on so many hard-working people simply trying to make their way.

But our political and media class needs to start acknowledging the economic and financial truth – that the UK government is borrowing and spending too much, taxation is now so high that it's hammering growth and employment, and that trying to finally get the economy moving by "moving further left", borrowing and spending even more, will result in a fiscal collapse.

Smart, experienced, high-profile economists need to start speaking out – as Rogoff and Bean just have – raising the alarm in a bid to force the broader establishment to face reality. Before it's too late.

If you've read this far, you clearly think this analysis is worthwhile and important. So please like and share.

And for more, read my "Economic Agenda" column in The Sunday Telegraph each week – and subscribe to "When The Facts Change: Economics and Politics in a fast-moving world, with Liam Halligan"

179

967

2,179

92,781

Cllr Stuart Bestwick retweeted

May 30

The Government say that they're “ending the asylum hotels”.

But they're doing it by pushing people into our communities - putting the public, particularly women and girls, at risk.

The only way to solve this problem is to detain and swiftly remove anybody who's here illegally.

215

1,287

5,198

38,370

Cllr Stuart Bestwick retweeted

May 30

The OBR forecast as Conservatives left office was for 2026 2% UK GDP growth, unemployment 4.2% and inflation 1.9% . After Labour’s tax rises they now forecast just 1.1% UK growth, unemployment up at 5.3% and inflation up at 2.3% for 2026.

44

159

475

14,117

Cllr Stuart Bestwick retweeted

May 29

Four pubs a day are closing under Labour.

Now, their 'nice pub tax' singles out rural village pubs for higher business rates simply because they are well-run, well-loved and well-located. It is punishing success.

Our Back Our High Streets Bill would end this.

telegraph.co.uk/news/2026/05…

135

150

470

35,424

Cllr Stuart Bestwick retweeted

May 29

Britain is suffering from a collapse of consequences.

If we’re going to fix it, we need to get tough.

1,390

1,143

7,836

296,727

Cllr Stuart Bestwick retweeted

May 27

It's way too hot out there.

The next Conservative government will reverse the aircon ban created by @RobertJenrick, which blocks new homes from being built with air conditioning.

That's the one he's talking about here ⬇️

300

142

1,078

1,038,575

Cllr Stuart Bestwick retweeted

May 26

Labour's increase to employer National Insurance as part of the 2024 Budget may well have been the worst tax rise it was possible to come up with – leading only to lower wages and reduced employment.

Now Reform UK appear determined to find the worst possible tax cut, with their proposal to exempt overtime from income tax.

The party calls it a 'hard work bonus', says it will cost £5 billion a year, and that welfare cuts will pay for it. It is a clever and bold piece of PR. It is also, on almost any view, terrible.

✍️ Dan Neidle

Article | spectator.com/article/reform…

15

27

76

11,805

Cllr Stuart Bestwick retweeted

Interesting public spat at the top of Reform UK over immigration. Most grown up political parties handle this sort of thing behind closed doors.

May 26

Robert’s answer is not Reform policy.

As the person responsible for our deportation plan I want ensure people know where we stand:

If a foreign national lives in social housing at taxpayer expense, they automatically fail our economic test and will be deported.

126

73

514

45,326

Cllr Stuart Bestwick retweeted

May 26

💥📺🎙️ NEW "When The Facts Change" Interview

Can the Tories rein in the UK's runaway welfare budget?

Welfare spending is set to balloon 19% to £373 billion by the scheduled end of this Parliament in 2029. Within that, working age health and disability benefits will surge 30% – to almost £100 billion. These are colossal sums.

The Tories are challenging the conventional wisdom –that trying to make welfare savings is electoral suicide.

The party is now pledging to make a chunky £47 billion of savings per year, with £23 billion of that to beslashed from the welfare bill.

The welfare savings are being championed by Helen Whately, Shadow Work and Pensions Secretary and, since 2015, MP for Faversham and Mid Kent.

Labour attempts to make welfare savings were last year firmly rejected by the party’s left-wing MPs. So are these Tory plans credible? Could the Conservatives control Britain’s runaway welfare spending.

Hit the link below for a detailed discussion with @Helen_Whately on When The Facts Change: Economics and Politics in a fast-moving world, with Liam Halligan

comment.press/whately

39

52

180

39,903

Cllr Stuart Bestwick retweeted

May 25

"Ten better tax cuts than Reform’s £14bn overtime gimmick" 👍

Another good takedown of Reform's tax break for overtime (hat tip @DanNeidle)...

taxpolicy.org.uk/2026/05/25/…

15

39

143

9,279

Cllr Stuart Bestwick retweeted

Reform’s flagship tax policy just got marked by independent experts. The verdict is brutal.

They costed tax-free overtime at £5bn. The real figure looks closer to £14bn. A £9bn hole in one announcement. 1/

May 25

Reform UK wants to abolish income tax on overtime.

It sounds like a tax cut for hard work. Actually a tax cut for the word “overtime”.

So little GDP impact & huge cost - we reckon £14bn not Reform's £5bn

If you want to spent £5bn on tax cuts, we have ten better ways:

🧵

200

136

471

204,031

Cllr Stuart Bestwick retweeted

May 24

This is the chef's kiss of Reform policy ideas.

The perfect example of public appeal vs retarded policy. Which is really what Reform is all about.

There are so many ways this would will be abused or backfire so I will list them all.

1. I said last night, company directors/owners will suddenly be earning 60 hours weeks every week (but not really).

2. Employee collusion - Business convert salaried roles to lower rate hourly pay, but pays fake "overtime". The employee gets more take home pay but the employer's payroll costs reduce.

3. Diversion - Many jobs don't pay overtime. Teachers for example. If they did, we'd be bankrupt. Why go into teaching on £35k a year when you could earn that on less hours with overtime elsewhere?

Efficiently run company don't have overtime opportunities at all, making them less attractive than those that do.

4. Unfair advantage - Let's say your a small landscaping company employing 5 guys by gaming the system above. You have an unfair advantage over the bigger company playing by the rules. Jobs will be lost as smaller, less scrupulous companies gain advantage over those that play by the rules.

5. It shrinks the job market - Offering overtime becomes a recruitment advantage. In which case employing 5 people to do a job with overtime is better than employing 6 with none.

6. It can shrink productivity - It's now in your interest to stretch your workload over more hours or game the system. Which means more hours worked for the same production.

7. If you think the answer is that there will be increased compliance enforcement and auditing from an already overwhelmed HMRC when Reform want to cut the civil service I'm afraid you're mistaken.

May 23

🚨Important policy announcement:

Britain was built on the hard graft of people who go the extra mile.

A Reform government will ABOLISH income tax on hours worked beyond 40 hours a week, for incomes below £75,000 a year.

It’s time to REWARD hard work, not punish it! 🇬🇧

114

273

1,189

174,563

Cllr Stuart Bestwick retweeted

May 24

While it makes for a good headline, this is a terrible policy for several reasons.

1. It would create a 'cliff edge' at £75,000, which means many people going from earning £75k to £76k would get hit by a tax bill that's bigger than their raise. This will hugely deter people from earning more.

2. It would be exceptionally easy to game to facilitate tax avoidance. Nothing would stop unscrupulous employers and and employees agreeing that the regular pay is very low, but an hour of overtime is paid (say) 100x ordinary wages. All of a sudden, the whole wage is tax-free.

3. It would be unfair between professions where hours are contracted and those it's not. The professional services sector, for example, rarely pays overtime. This would incentivise those professions to move to clock-punching: forcing professions to change their culture to suit government.

4. By targeting hours, it gives a tax break to work that takes longer. But we should be incentivising higher wages through higher productivity, not lower wages on longer hours.

5. Self-employed people and people who work multiple jobs wouldn't benefit from this. For absolutely no reason whatsoever.

Just cut taxes generally. Don't dream up schemes that make our tax system even more complicated and even more distortionary just to get a quick headline.

May 23

Nigel Farage has pledged to axe income tax on overtime as he vows to “make work pay”.

If Reform UK wins the next general election, people who earn less than £75,000 and work overtime above a 40-hour week will pay no income tax on the extra hours.

🔗: telegraph.co.uk/politics/202…

117

163

782

186,627

Cllr Stuart Bestwick retweeted

May 22

In 1980, we had one regulator for every 11,000 people working in financial services.

Today, it's closer to one regulator for every *75* people.

Bureaucrats always create more rules and always work to expand their powers. The idea that we can "regulate for growth" is ludicrous.

188

1,029

4,665

107,514

Cllr Stuart Bestwick retweeted

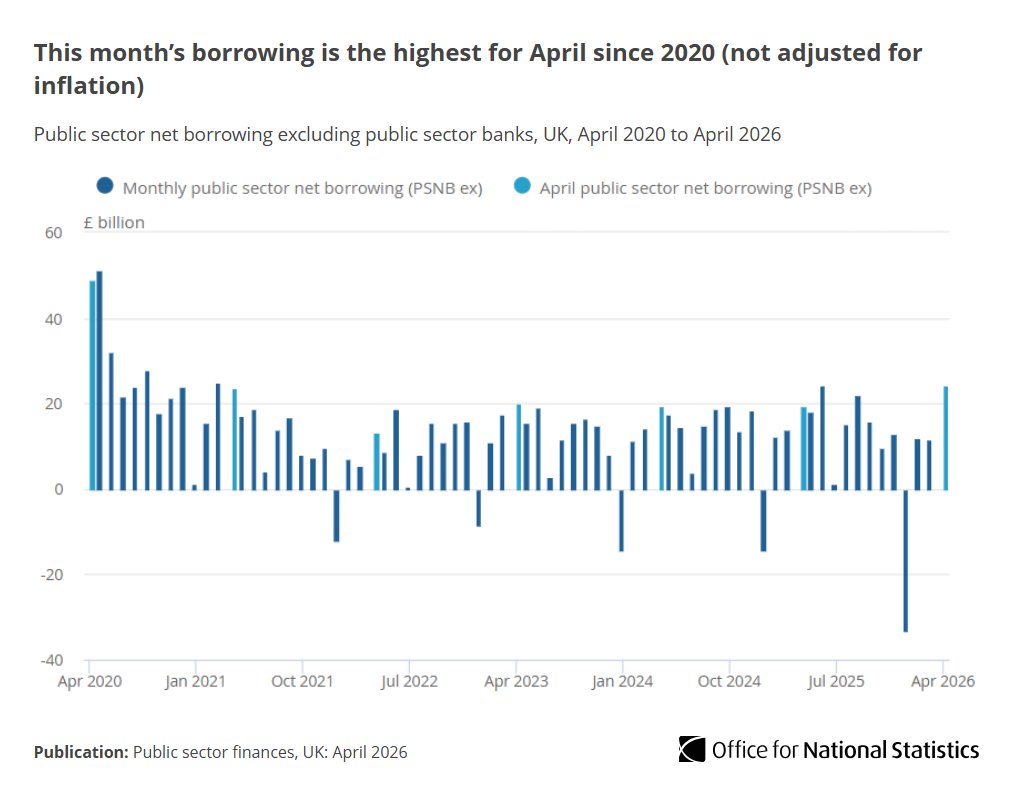

May 22

Labour borrowed £24.3 billion last month - well above the OBR forecast and 25% higher than last April. Our debt interest spending was the highest of any April on record.

The recent spike in borrowing costs shows markets are increasingly worried about Keir Starmer’s replacement, leaving families to pick up the bill for a £300 Burnham Penalty.

Only the Conservatives have a leader with the backbone and strong team needed to restore confidence in the public finances by cutting debt through our Golden Economic Rule.

Borrowing – the difference between total public sector spending and income – was £24.3 billion in April 2026, 25% more than in April 2025.

Read more➡️ ons.gov.uk/economy/governmen…

ALT Chart showing this month’s borrowing is the highest for April since 2020 (not adjusted for inflation).

64

119

270

28,712

Cllr Stuart Bestwick retweeted

May 22

The UK borrowed another £24.3 billion in April, above the £20.9 billion forecast by the Office for Budget Responsibility.

The ONS said the debt interest bill rose to £10.3 billion last month – the highest on record for April, which marks the start of the new financial year. The government is paying more than £100 billion a year to service its debts. Yet a cacophony of Labour and Green pols think we should borrow even more.

346

1,888

5,877

202,732

Cllr Stuart Bestwick retweeted

May 15

86 years ago today, Winston Churchill, Prime Minister for exactly 5 days, was woken by his phone ringing at 7:30 a.m.

It was Paul Reynaud, the French Premier. His voice was hollow.

"We have been defeated. We are beaten; we have lost the battle."

Churchill, half-asleep, couldn't process it:

"Surely it can't have happened so soon?"

Reynaud: "The front is broken near Sedan. They are pouring through in great numbers with tanks and armoured cars."

The German invasion was 5 days old. The "impassable" Ardennes forest had just funneled seven Panzer divisions through France's weakest hinge.

The next day, Churchill flew to Paris. He asked General Gamelin a single question:

"Where is the strategic reserve?"

Gamelin shrugged. "Aucune."

None. France had no reserve. There was nothing behind the line that had just broken.

Churchill later wrote that this was one of the greatest shocks of his life. The country he'd grown up believing had the finest army in Europe had already lost the war. They just didn't know it yet.

Six weeks later, Paris fell.

128

974

12,486

1,541,459

Cllr Stuart Bestwick retweeted

May 15

This is the price of Labour’s leadership chaos.

30 Year Gilt yields and borrowing costs at their highest level in decades. Billions worth of extra costs.

All of us will pay dearly for Labour’s game of musical chairs.

12

67

170

6,908

Cllr Stuart Bestwick retweeted

May 12

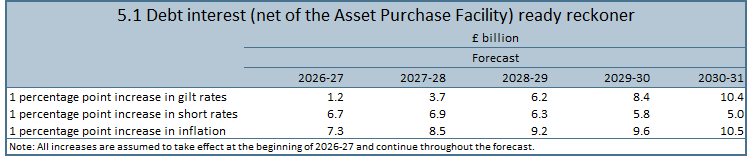

FYI, here is the OBR's debt interest ready reckoner, and an explainer 👇

1⃣ The annual cost of a 1%-point (100bp) increase in gilt yields will rise over time as new borrowing is financed at the higher rate. In year one it is just over £1bn, rising to more than £10bn in year five.

2⃣ The impact of an increase in short rates (the official interest rate set by the Bank of England) comes through more quickly (the Bank financed its purchases of gilts under "QE" by creating deposits on which it pays interest at the Bank rate).

3⃣ An increase in inflation also has a direct impact on debt interest payable, because of the UK's relatively large stock of inflation index-linked debt.

4⃣ Altogether, a sustained 1%-point (100bp) increase in gilt yields, short rates and inflation would add around £15bn to the annual debt interest payable in year one and around £26bn in year five.

(cc @IanMurrayMP 😉)

obr.uk/efo/economic-and-fisc…

4

30

81

9,826