Joined February 2009

- Tweets 1,888

- Following 490

- Followers 3,197

- Likes 95

130 Photos and videos

Deal or No Deal?

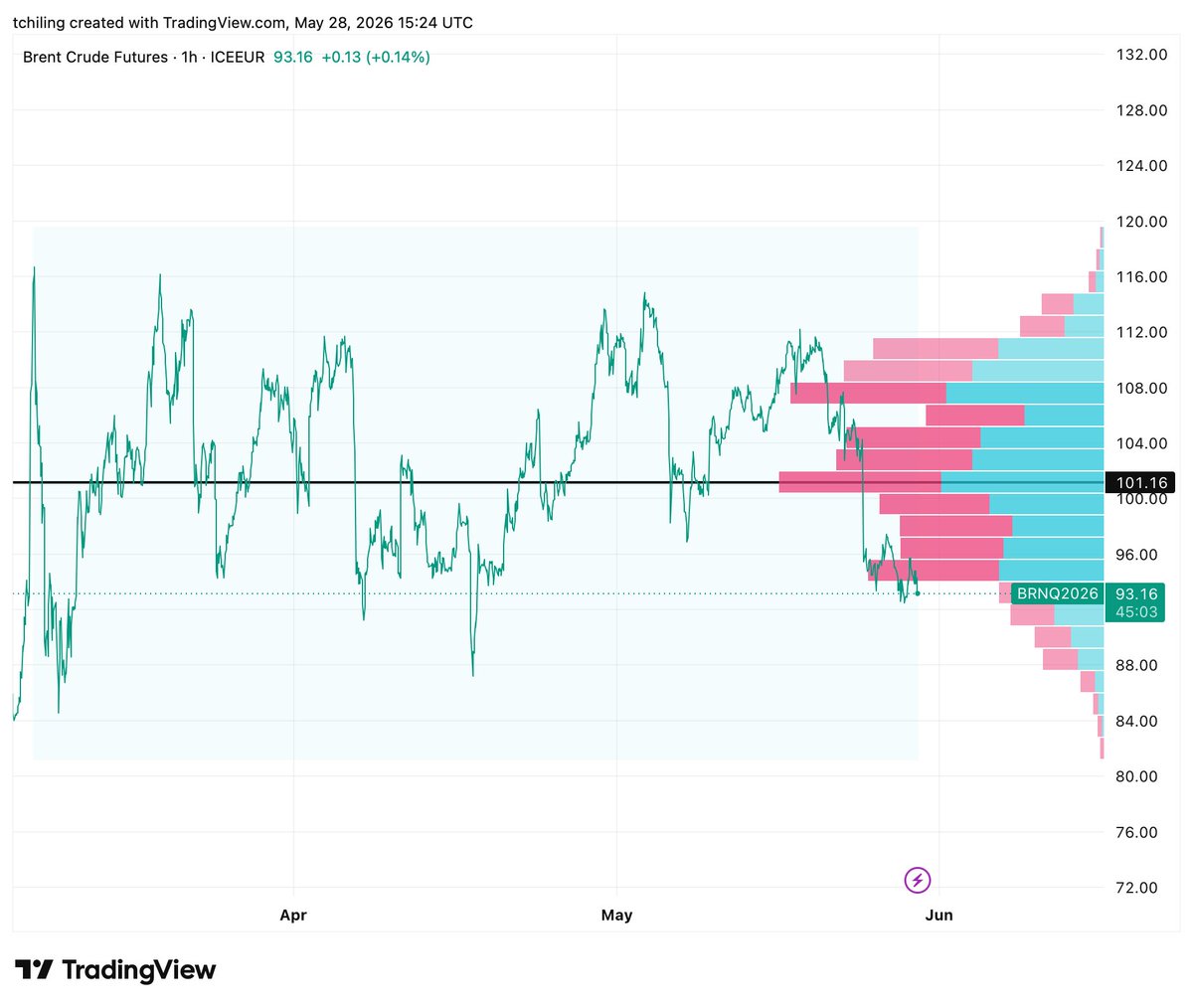

It has been more than two months since President Donald Trump announced a truce and ceasefire with Iran on 8 April. News that the US and Iran are officially signing a memorandum of understanding (MOU) in Geneva this Friday—restoring the free and secure passage of tanker traffic through the Strait of Hormuz and paving the way for negotiations over Iran's nuclear programme—has pushed oil prices lower, with front-month Brent futures trading just above $80/bbl at the time of writing.

Even if an agreement is signed, I suspect most shipowners and insurers will remain reluctant to transit Hormuz for some time. Confidence is not restored by signature alone. It may take days; it may take weeks before commercial shipping is convinced that the agreement is durable.

So, is this really it? In my view, the deal is not done until the ink is dry—particularly as the text of the proposed MOU has yet to be made public. The secrecy may well be deliberate, limiting the scope for last-minute interference and derailment. President Trump has also remained deliberately ambiguous about whether he will attend the signing ceremony himself, suggesting Vice President JD Vance could conclude the agreement in his place.

Last week, CNN tallied the number of times President Trump declared that a deal with Iran was imminent, or that only a handful of issues remained unresolved for a deal to be agreed. Including the period before the ceasefire, the count exceeded three dozen. On each occasion, the President emphasised with gusto and verve both Iran's deep desire to reach an agreement and the severely weakened state of its military and leadership. Whether by persuasion or outright jawboning, Mr Trump's rhetoric appears to have helped prevent oil prices from moving considerably higher.

Since the April ceasefire, I have found myself thinking of Charles M. Schulz's Peanuts comic strip (yes, the one with Snoopy in it). More specifically, the recurring (American) football scene between Charlie Brown and Lucy. Lucy promises not to pull the ball away when Charlie Brown comes to kick it. Charlie Brown hesitates, having been fooled countless times before. Yet each time, persuaded by apologies and assurances, he runs to kick the ball—only for Lucy to snatch it away at the last instant, leaving him flying through the air and landing flat on his back. Will the oil market escape Charlie Brown's fate this time?

Perhaps an MOU will indeed be signed this Friday. Perhaps it will not. But the memorandum may prove to be the easy part. Negotiating a durable agreement over Iran's nuclear programme and enriched uranium in the 60-days after this deal is signed is likely to be considerably more difficult. If so, any relief in the flat price of oil seen recently, or that may follow Friday, may well prove only temporary.

On a side note, Schulz reportedly once remarked that Charlie Brown's greatest strength was not winning at the football game, but continuing to try.

#OOTT #OIL #US #IRAN

176

Jun 11

Dire Straits

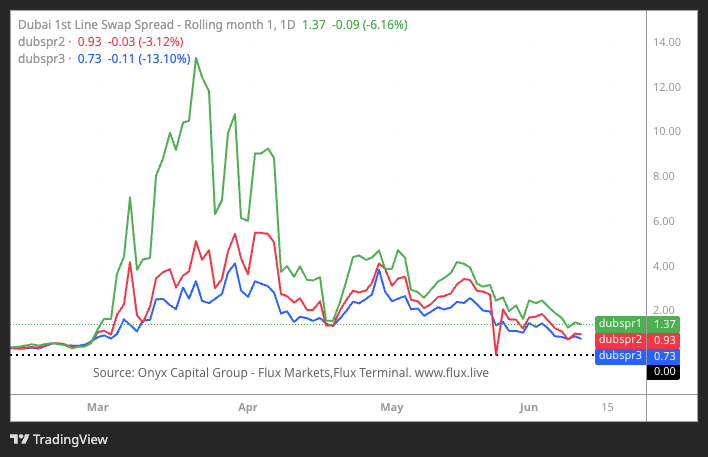

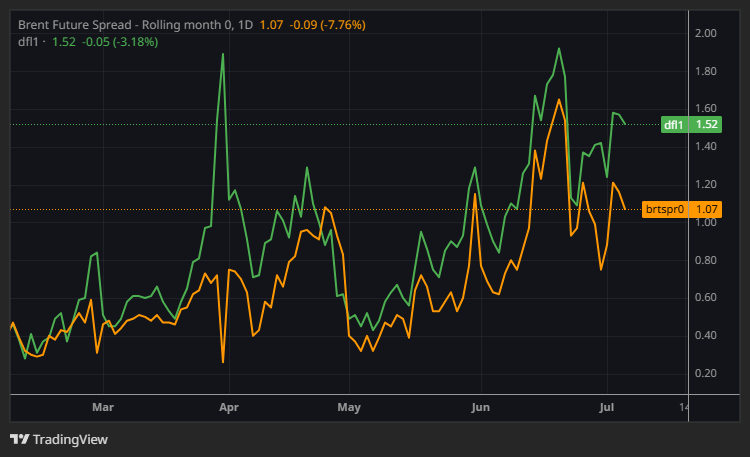

Despite fresh escalation by Iran and the US, Brent futures remain in the low 90s. Yet the flat price does not tell the full story. To borrow the phrase “in vino veritas”, the truth in oil lies not in the flat price but in spreads and the shape of the curve, which better reflect fundamentals. On that measure, the Dubai benchmark’s price structure is not sounding alarm bells as it did in the conflict’s early days.

Dubai swap spreads have weakened while Dubai’s physical premium has languished. In the 1985 song ‘Money for Nothing’, Mark Knopfler sang, “We got to move these refrigerators, we got to move these color TVs”. More than 100 days into the conflict, the pressing need is to move oil out of the Persian Gulf. Saudi and UAE bypass pipelines have helped. While two naval blockades remain, both are porous, and oil is slipping through the Strait of Hormuz, whether covertly, as claimed by President Trump, or through Iranian-approved channels, likely for a fee. Falling crude storage at key Kuwaiti terminals, including Mina Al Ahmadi, and elevated ship-to-ship transfers support the view that oil is getting out. Gulf supply is loosening, weighing on Dubai’s price structure.

Even if more oil is moving through Hormuz, many argue that the decisive factor behind the contained flat price and the relative weakness in Dubai spreads is China, whose crude imports have fallen to their lowest level since October 2017. That fall is widely seen as the key offset to the supply shock created by the US-Iran conflict. The release of IEA strategic stocks and higher US crude exports have also helped, but to a lesser extent.

Oil bulls remain sure that a price spike is near. In their view, the current situation cannot last: storage is drawing fast, operational lows may be close, and US crude exports are likely maxed out. Shell’s chief executive has said the market is short 1.2 billion barrels and is managing the present by borrowing from the future. In that context, oil bulls await the return of Chinese buying, possibly as early as July, and seasonally higher summer demand as the catalyst for the rally they have long been crying wolf about.

If Chinese buying returns, the market could end up in more dire straits. My personal view is that China is content to wait out the conflict for now. It entered this crisis well prepared, having built sizeable inventories last year. Once the conflict began, China moved to restrict oil product exports, lower refinery utilisation rates, and cut crude imports. Beijing may be able to sustain this for several more months. Oil bulls may be underestimating both China’s acumen to weather the storm and its willingness to draw on its strategic stocks.

If China stays at bay, I see little merit in going long Dubai structure. With supply improving, it may be wiser to stay short front-end spreads while bidding a longer-dated time spread to protect the position against renewed Chinese buying.

#OOTT #OIL #OILPRICE #HORMUZ #DUBAI #US #IRAN #CHINA

3

675

May 28

Oil: rinse and repeat.

The oil market remains fixated on US–Iran talks. A comprehensive “deal” still appears a distant prospect given entrenched positions, notably on nuclear issues. Yet the market hopes both sides can move towards some form of memorandum of understanding (MOU) — a first step towards reopening the Strait of Hormuz.

Even if a diplomatic framework were agreed and Hormuz securely reopened, the normalisation of physical oil flows would take months. In other words, the market should not expect a sudden wave of supply, even if the ink were dry on a signed — and potentially fragile — agreement.

Still, sentiment continues to dominate outright price direction. Traders remain glued to every twist and turn in rhetoric from Washington and Tehran, and the prospect of an MOU could send prices sharply lower. Since the start of the conflict, the constant back-and-forth in rhetoric has dictated the up and down swings in Brent futures.

The moves have been amplified by a Brent futures market that has shrunk materially in open interest, while tighter capital-at-risk constraints have contributed to increasingly nervous positioning, particularly among macro-oriented funds managing risk exposure across several asset classes simultaneously.

The market knows it will be a long and winding road. Hopes of a breakthrough have repeatedly been dashed almost as quickly as they emerged, creating what now feels like a recurring — and dare I say predictable — pattern. Rinse and repeat.

Oil prices, which appeared to soften earlier in the week on renewed diplomatic optimism, can easily firm up again. This week is not the first — nor likely the last — time that both sides have hinted a deal may be very near, only for optimism to unravel following denials, rebuttals or renewed, albeit limited, kinetic action. Recent US strikes near Bandar Abbas and Iranian retaliation towards Kuwait have revived the possibility of renewed US military action. Yet President Trump has shown as much exuberance in escalating brinkmanship as in projecting confidence that a negotiated solution is within reach.

Since the onset of the war, the front Brent futures contract has traded closer to $100/bbl on average than the $150–200/bbl levels suggested by some bullish commentators at the outset of the conflict.

So, how does one trade this oil market? Through options, perhaps — a volatility bet and arguably the only game left in town. But being long at-the-money straddles does not come cheap, while even the less onerous out-of-the-money strangle structure requires counterparties willing to underwrite and dynamically hedge gamma in an environment where every tweet or Truth Social post can send prices sharply in either direction. If one believes this rinse-and-repeat environment will persist for the next few months, then short near-dated strangles — for those not faint of heart — may yet prove an interesting avenue to explore.

#OOTT #Oil #HORMUZ #BRENT #OILPRICE #US #IRAN

2

363

May 28

The (@OxfordEnergy) Oxford Institute for Energy Studies has just released its latest forum issue, titled “Unpacking the Hormuz Crisis: Implications for Energy Markets and the Transition”.

👉 oxfordenergy.org/wpcms/wp-co…

The publication brings together a series of 25 articles examining the current crisis in the Middle East and the implications of the closure of the Strait of Hormuz for oil and gas markets — from fundamentals and physical disruptions to the ripple effects across financial pricing and trading.

I am humbled to contribute to this forum alongside such respected voices in the oil market. My contribution examines the dynamics between physical and financial crude oil pricing, focusing in particular on the widely discussed perceived disconnect in these prices during the early stages of the conflict. I am very appreciative of the feedback provided on initial drafts of this piece, although any remaining errors or opinions are entirely my own.

Many thanks to Bassam Fattouh for the invitation to contribute my thoughts. I hope the piece proves useful in helping readers better understand oil pricing during what has become an unprecedented crisis for the market.

#OOTT #Hormuz #oil #Brent #Dubai #oilmarkets #energy #OIES

1

4

28

3,707

May 19

Very appreciative of the Oxford Institute for Energy Studies (@OxfordEnergy)for the invitation to discuss oil markets with Bassam Fattouh and Paul Horsnell, two of the most knowledgeable oil market analysts I know. See the link to the podcast below.

👉 Podcast: oxfordenergy.org/wpcms/wp-co…

The podcast examined the fallout in oil markets from the conflict between the US and Iran and the resulting closure of tanker traffic through the Strait of Hormuz. Among the topics discussed are the scale of the disruption to oil flows and its implications, why futures prices appeared disconnected from physical prices in the early stages of the conflict, the drivers behind the collapse in futures open interest, the outlook for long-dated oil prices, and how shifting refinery demand and trade flows — particularly towards US barrels — have influenced the relative pricing of the Brent and Dubai benchmarks. The discussion concludes with the outlook for the global oil balance and its key components in 2027.

#OOTT #SOH #Hormuz #Brent #oil #oilprice #oilpricing #oilbalance #oilcurve #positioning #openinterest #volatility #Dubai

1

4

445

Harry Tchilinguirian 🛢 retweeted

May 11

US President Donald Trump will sign an executive order to, in effect, lower tariffs on foreign beef imports as the White House struggles to reduce meat prices.

Apr 14

I know we're all looking at oil.

But live cattle just rose above $2.5 per lb for the first time (to an all-time high). The BBQ season in America is going to be rather expensive for flipping burgers.

19

40

198

58,381

Apr 28

#UAE DECIDES TO EXIT #OPEC AND OPEC

#OOTT Just my two cents on the headline

The timing of this decision, in the context of the ongoing US/Iran conflict will no doubt leave many perplexed, but the outcome has likely long been in the making.

In previous OPEC meetings, agreed upward changes with Saudi Arabia to the UAE’s production reference level and quota, were a short-term fix to a larger, long-term issue: the UAE’s expanding production capacity to provide the necessary liquidity for the physically deliverable IFAD Murban futures contract and achieve economic goals.

In the end, the UAE needed to unshackle its output from a quota system—not only for the good of its flagship Murban futures contract, but also for its longer-term economic development: shifting Dubai towards a service-oriented economy, focused on business and tourism, using oil revenues to finance the transition.

Below the Bloomberg headlines

BN 04/28 12:20 *UAE DECIDES TO EXIT OPEC AND OPEC

BN 04/28 12:21 *UAE SAYS TO EXIT OPEC

BN 04/28 12:22 *UAE STATE-RUN WAM NEWS AGENCY REPORTS ON OPEC DECISION

BN 04/28 12:23 *UAE TO BOOST OIL PRODUCTION GRADUALLY: WAM

BN 04/28 12:24 *UAE'S OPEC EXIT WILL HELP COUNTRY MEET CHANGING DEMAND

BN 04/28 12:25 *UAE'S OPEC EXIT ALIGNS WITH INCREASE IN LOCAL ENERGY INVESTMENT

*UAE DECIDES TO EXIT OPEC, OPEC STARTING MAY 1: WAM

2026-04-28 12:22:10 GMT

1

2

4

1,748

Harry Tchilinguirian 🛢 retweeted

Apr 24

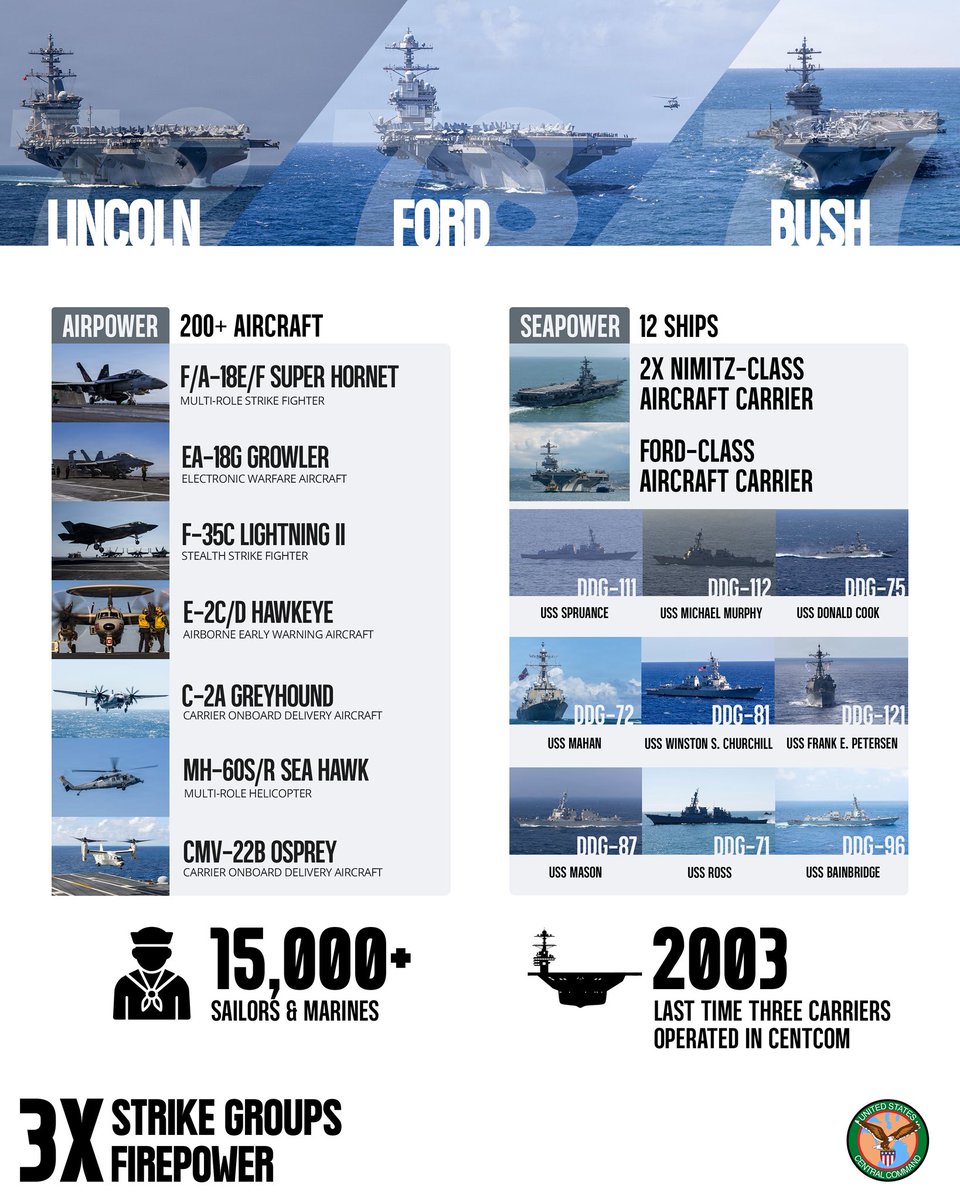

For the first time in decades, three aircraft carriers are operating in the Middle East at the same time. Accompanied by their carrier air wings, the USS Abraham Lincoln (CVN 72), USS Gerald R. Ford (CVN 78) and USS George H.W. Bush (CVN 77) include over 200 aircraft and 15,000 Sailors and Marines.

1,019

3,865

15,272

1,445,919

Apr 23

🛢️ Brent/Dubai: the empire strikes back 🛢️

I thought it would be interesting to follow up on my previous post, “Oil: Tea for Two”. US–Iran talks have not progressed; if anything, things have only worsened. While President Trump may have declared an indefinite truce, talks between the US and Iran in Islamabad, Pakistan, are going nowhere fast, with Vice President Vance being pulled out at the last minute.

The Brent/Dubai differential in the oil swaps market (chart from Flux Terminal, available on flux.live) saw Brent gain against Dubai rather than the other way around at the front of the curve. The gain in the prompt tenor is indeed impressive, but we need to look at how the situation in the Middle East has evolved.

In my simple view, the marginal medium sour barrel in the region is facing even stronger challenges in escaping the Persian Gulf, with Iran taking aim at ships while the US blockade effectively extends beyond the passageway of Hormuz, with the US intercepting vessels in the Indian Ocean, far from the Strait.

While the odd barrels still make it out (oil always finds a way, as they say) by navigating Iran-approved routes, it is getting more difficult, and I am guessing that Dubai’s strength relative to Brent will come back.

#OOTT #OIL #Brent #Dubai #US #Iran #Hormuz

3

319

Apr 16

🛢️ Oil: Tea for Two 🛢️

“Tea for Two” is a classic American song from the 1920s, first featured in a Broadway musical — a light-hearted duet that became a jazz standard, inviting improvisation.

In oil markets, the Brent/Dubai price duet is perhaps not romantic, but no less prone to improvisation in my view recently. Policy shifts continue to shape the relative pricing of these crudes, with implications for how oil flows globally.

Since the escalation of the US/Israel conflict with Iran, Dubai initially moved to a sharp premium over Brent in mid-March. That premium later eased as oil continued to flow — albeit at very reduced rates — through the Strait of Hormuz towards Asia, with Iranian permission. Iran benefited from a US waiver on oil already on the water, as did Russia, easing pressure on importers such as India and China. The International Energy Agency also coordinated a strategic stock release, helping to lessen supply concerns among Middle East-dependent buyers, notably Korea and Japan.

The Brent/Dubai spread has had a material impact on flows between the Atlantic Basin and Asia. Tanker tracking data shows a sharp rise in Atlantic Basin loadings to East of Suez from mid-March, with elevated arrivals in Asia expected between May and June. At the same time, empty VLCCs have been heading to the US Gulf coast to load up on crude for a journey east, a trend likely to extend into early summer.

With Washington and Tehran now mutually imposing a blockade on the Strait of Hormuz, and US waivers to likely expire, a full disruption to transit through Hormuz would increase Asia's reliance on Atlantic basin crude supply, putting upward pressure on Dubai relative to Brent. Higher freight rates, if vessel availability tightens, would reinforce this price dynamic for arbitrage economics to be workable.

Recent price action, however, tells a more nuanced story. In the swaps markets (chart below from Onyx's Flux Terminal on flux.live), Dubai’s premium for the balance of April remains above $3 a barrel, but falls below $1 for May to July, with the front of the curve relatively range-bound recently. Under current conditions, wider summer spreads might have been expected.

The market may still be pricing in a swift reopening of Hormuz or positive prospects in US-Iran talks intermediated by Pakistan. My more pessimistic view still points to renewed strength in Dubai vs Brent. This leaves our last duet, China and the US, to possibly be a source of the current restrained Dubai pricing. Washington may allow China-bound cargoes to transit Hormuz, given, in President Trump's words, that President Xi Jinping will give him a "big, fat hug" when they meet in a couple of weeks and that they "are working together smartly, and very well".

🎶 Tea for two, and two for tea, just me for you, and you for me alone.

#OOTT #OIL #BRENT #DUBAI #US #IRAN

2

3

536

Apr 13

🛢️ On oil prices: structure over flat price 🛢️

Since the conflict between the US, Israel and Iran escalated, the flat price of Brent futures has shown two notable features.

➡️ First, a disconnect from physical crude prices. Dubai partials, for instance, were pushing towards $150 a barrel in mid-March, while front-month Brent futures struggled to move sustainably above $100/bbl.

➡️ Second, pronounced volatility. Prices have swung sharply up and down, sometimes within a single session, with spikes repeatedly sold into, leading Brent futures to revert towards the $100/bbl level.

Has the market grown numb to bullish headlines? Is it waiting for demand destruction as higher prices begin to bite? Or is it underestimating the scale of supply disruption, with significant volumes of Gulf production shut in at the wellhead? There may also be excessive confidence that US exports — with an armada of VLCCs heading to the Gulf Coast — can help attenuate shortfalls for Asian refiners. The US move to impose its own blockade of the Strait of Hormuz (that is now in effect) adds further uncertainty over the return of stranded barrels. And even if the US initiative proves successful, logistical and scheduling hurdles mean that several weeks may pass by before stranded Persian Gulf oil is again fully available to the international market. And, of course, the US blockade initiative will invite, in my view, some form of tit-for-tat response from Iran.

It is tempting to simply take a bullish view on Brent futures’ outright price, given tight fundamentals and rising geopolitical risk, particularly with a hope-filled two-week ceasefire now looking to be dead on arrival. But that risks overlooking the potential for sharp reversals, as witnessed before, in a market overcrowded in one direction: long. As noted before, price spreads are a better reflection of the underlying fundamental reality.

Front-month Brent futures, after gapping higher this morning during the Asian trading session (following news of the US blockade), have retreated slightly at the time of writing, while in the swaps market, BFOE spreads, used here for illustrative purposes (chart from Onyx's Flux Terminal on flux.live), moved up with the flat price and then have slightly ebbed. As traders, analysts, consultants and other pundits try to draw inferences for flat prices, in my opinion, the safer way to express a trading view in this environment still remains structure over flat price

#OOTT #OIL #BRENT #US #IRAN #HORMUZ #BLOCKADE

2

5

2,671

Apr 12

Hormuz musical chairs

Until now, it was Iran that sought to restrict shipping through the Strait of Hormuz — in principle a free international waterway — threatening to target vessels lacking its permission, while advocating a new passage route closer to its shores and the introduction of a tolling mechanism.

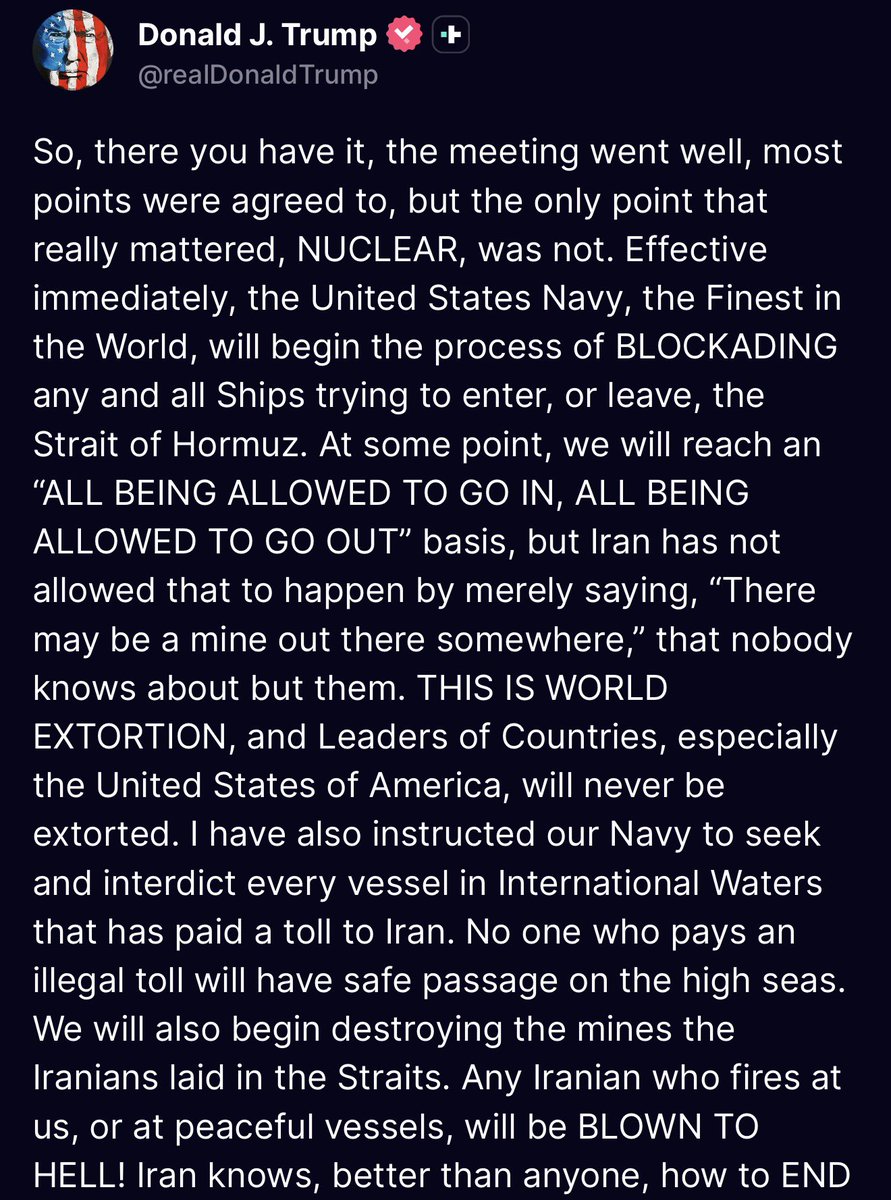

Today, President Donald Trump said on his Truth Social platform that he had instructed the US Navy to blockade the Strait, denying passage to all vessels in and out, while also seeking to clear the sea of mines.

This new development raises questions as to why the US is effectively pursuing its own blockade? Basically, is this just to wrest back control of the waterway from Iran? Such a move would halt Iranian oil flows, squeezing revenues without resorting to direct kinetic strikes on Kharg Island or occupation with ground troops. It could also prompt a reaction from countries whose flags have been flown by Iran-authorised vessels. Some of these countries, like China, a prominent importer of oil ex Hormuz, has been rather publicly silent since the US-Israel conflict with Iran escalated.

How outright prices will react on Monday remains uncertain. Will there be the now-familiar spike during Asian trading hours, followed by a pullback in the European and US sessions? Perhaps. Many have already been whipsawed by the often incongruous ups and down moves in flat prices.

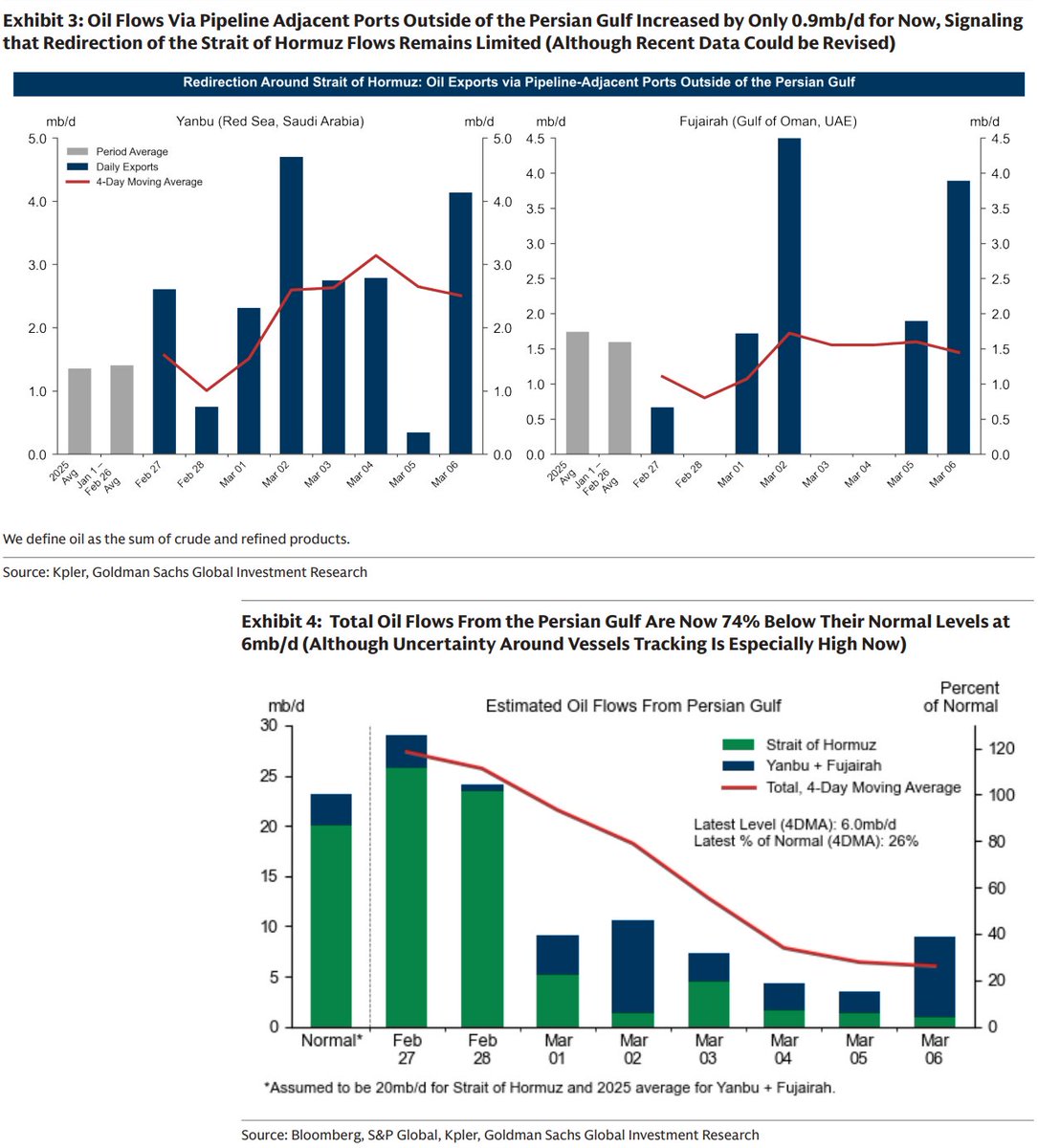

Notwithstanding incremental flows to Yanbu and Fujairah, roughly 10mn b/d of crude production is shut in at the wellhead across the region, leaving a sizeable supply gap in the global balance. At the same time, flows through Hormuz are likely to become even more constrained in the coming weeks. Given the above, being long Brent spreads or flys is still the best way to navigate (no pun intended) the current oil market conditions.

#OOTT #OIL #IRAN #US #HORMUZ #Brent

151

Mar 20

Through the oil looking glass

pemedianetwork.com/petroleum…

Persian poet and mathematician Omar Khayyám wrote: “The Moving Finger writes and, having writ, moves on.” The initiation of military operations by the US and Israel against Iran on 3 March was a transformational moment not only for the Gulf region but also for global oil markets — one from which there is no return. No matter how this war ends, or what objectives are ultimately achieved, there will be no reverting to the previous status quo.

At the invitation of @PetroleumEcon, I wrote an opinion piece on the current dynamics of the oil market. With new events unfolding by the hour, it was hard to come up with a thematic that would have a shelf life of more than a half a day. So I took on the idea of how the market achieves equilibrium in these trouble times.

With little scope in volumetric adjustments in current state of supply and demand fundamentals, it is all down to price changes to bring about a equilibrium, albeit even fleetingly. For the lost volumes through Hormuz, quantity-wise, there is no immediate replacement solution to allow the oil price to deflate with speculators selling the fact, having bought the rumour.

The price adjustment in the coming weeks will inevitably be messy as the market tries to separate signal from noise. Brent futures may well ultimately converge towards the physical Dubai benchmark, with a potential move towards $150/bbl. However, in the near term, it is more likely, if no de-escalation takes place, for Brent futures to converge first towards UAE’s Murban crude valuation, which recently crossed above $125/bbl, before it takes aim at catching up with Dubai. This, in my opinion is likely to come even as Treasury Secretary Scott Bessent dismisses rumours of intervention in financial oil markets and raises the possibility of easing sanctions on Iranian crude already on water and conducting unilateral US SPR releases.

#OOTT #OIL #BRENT #US #IRAN

2

2

9

4,415

#OOTT #Oil #US #Iran — how markets rebalance

Basic economics suggests that market equilibria are reached either through mostly volumetric adjustments — the Keynesian view, reflecting the assumption of sticky prices — or through price alone, if you adhere strictly to the neoclassical school of thought. In practice, the balancing mechanism is usually some combination of both, with the possibility that price can over- or undershoot its theoretical equilibrium level during periods of instability or stress.

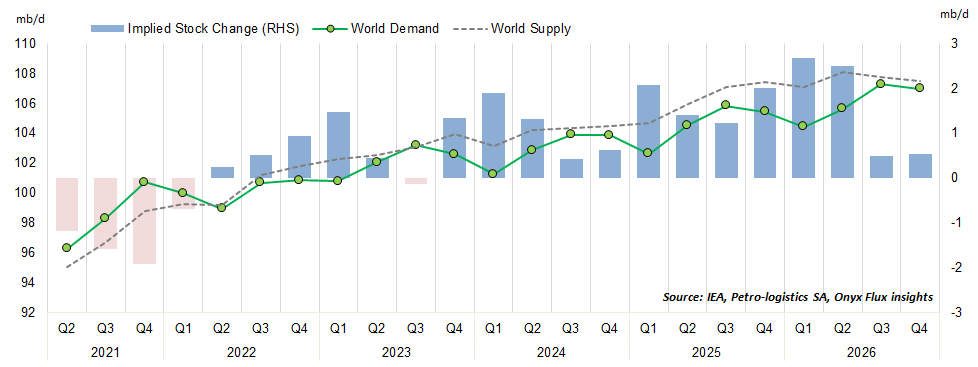

In the current oil market, a volumetric adjustment — what in trading analytics jargon is referred to as the “solver” — has yet to emerge. This adjustment volume can take the form of a short-term solution such as a release of strategic stocks or the resumption of safe transit for oil tankers through the Strait of Hormuz, understanding there is an the inevitable ramp-up period in normalising logistics and scheduling before flow is fully restored. Alternatively, we can have combination of both where a stock release is a bridge measure before Hormuz traffic returns to normal.

#Brent futures surged to nearly $120/bbl at the Asian open this morning, before settling back down at the time of writting around $105/bbl. This is what a market attempting to rebalance looks like in the face of a potentially durable supply disruption. Price is doing the heavy lifting in achieving a new equilibrium.

Later today, #G7 governments are expected to hold an emergency meeting to discuss conditions in the oil market and the potential need for a coordinated release of strategic reserves by the International Energy Agency (IEA). The Financial Times reported that energy ministers will hold a call with the IEA’s executive director, Fatih Birol, at 8.30 am New York time.

In the interim, while waiting for that call and any decision it might bring, we cannot discount that the flat price of Brent can test higher again.

1

6

616

#OOTT What constitutes a supply disruption and the march higher in #oil prices

The market’s initial response to the outbreak of conflict between the #US and #Iran was proportionate, with Brent futures climbing from the low $70s into the low $80s a barrel. Last week, Brent rose decisively above $90/bbl as traders began pricing in the supply shock associated with the potential for a prolonged disruption to flows through the Strait of #Hormuz. Physical prices for Middle Eastern crude grades have in turn moved above $100/bbl.

Speculation has grown that Gulf producers may be forced to shut in production as limited storage capacity becomes saturated. Iraq has reportedly cut back output, with the UAE and Saudi Arabia thought likely to follow, even as they divert some supply respectively to the Red Sea at Yanbu and to Fujairah on the Gulf of Oman.

The Executive Director of the International Energy Agency (IEA), Fatih Birol, indicated last week that global oil supply remained abundant for the time being and that the market faces a logistical, not a production, problem. A release of strategic stocks is not being contemplated at the time of writing. Since its creation, the #IEA has coordinated five emergency stock releases, including during the Gulf War in 1991, hurricanes in the Gulf of America in 2005, the Libyan civil war in 2011, and more recently the conflict in Ukraine. In the event of an actual or potentially severe supply disruption, the agency first assesses the market impact before determining the need for a coordinated response.

In the current circumstances, the distinction between a disruption that removes sufficient production to trigger IEA action and the inability of oil to move in and out of the Strait of Hormuz is likely lost on the market. The global oil supply chain is under severe strain as crude cannot reach its end users, most notably in Asia. Barrels that have been unable to leave the Gulf since hostilities began are effectively lost, forcing refiners either to source supplies elsewhere or draw on inventories. For India and China, sanctioned oil held in floating storage offers one option, but only a short-term solution.

From the market’s perspective — and arguably in reality — if oil cannot move through Hormuz, the outcome is effectively the same as halting production: a supply gap that pushes prices higher until flows are restored or demand destruction occurs. When producers eventually curtail output at the wellhead is, in my view, less pressing than the need for the market to balance. Whether that occurs through a volumetric solution — such as an IEA stock release or the safe passage of oil through Hormuz — or through a higher flat price, I lean towards the latter. As such, backwardation in the prompt spreads of the curve, already at stratospheric levels could widen further.

3

599

Harry Tchilinguirian 🛢 retweeted

Mar 8

Saudi and the UAE are trying to reroute some of the flow through Yanbu and Fujairah, but it’s nowhere near enough to offset the massive liquid losses from the Hormuz shutdown.

On top of that, physical diffs for crude loading outside the Persian Gulf and tanker rates are through the roof—some grades have already blown past $100/bbl.

If traffic doesn't get moving again fast, even Saudi and the UAE are looking at production shut-ins.

#oott #com

6

36

220

21,511

Harry Tchilinguirian 🛢 retweeted

Mar 3

TRUMP ON IRAN AND OIL PRICES:

"...People felt that something had to be done [on Iran]. So, if we have a little high oil prices for a little while, but as soon as this ends, those prices are going to drop, I believe lower than even before..."

28

40

326

110,284