109 Photos and videos

Tarre86 retweeted

May 31

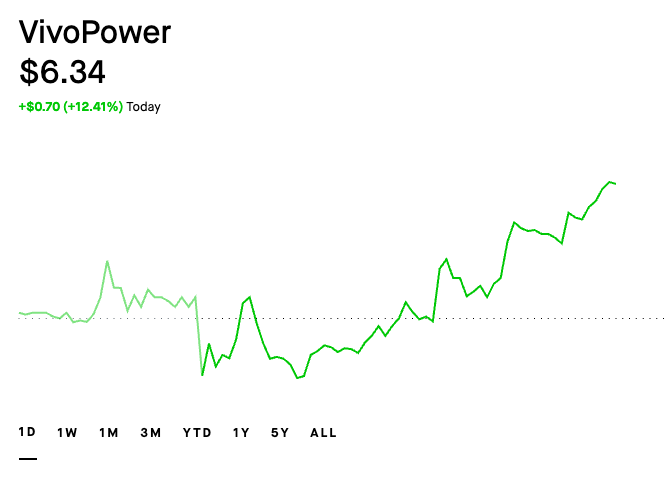

🔌 $VIVO – VivoPower: The unknown AI infrastructure bet you should know about 🧵

1/ Small company. Massive ambitions. VivoPower is building a global platform for AI data centers powered by renewable energy. Here's everything you need to know. 👇

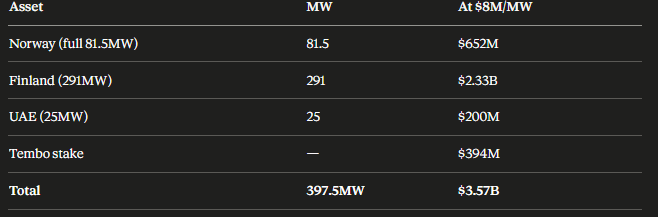

2/ 🏭 The crown jewel: Norway

In April 2026, $VIVO completed the acquisition of a 41.5MW data center in Mo i Rana, Norway. Powered by 100% hydroelectric energy at just $0.035/kWh. For context: US average is ~$0.08/kWh. That's a massive cost advantage for AI workloads.

3/ 💰 The numbers

→ Annualized revenues: ~$31M

→ Pro-forma EBITDA: ~$10M p.a.

→ Expansion potential: 40MW pending approval (>80MW total)

The company expects to reach group-level EBITDA profitability for the first time.

4/ 🤖 AI tenant shortlist underway

VivoPower ran a formal RFP process. Multiple serious AI operators are on the shortlist. There were even acquisition offers at a premium to their purchase price — management said no. They want 10 year lease agreements instead. Long-term thinking.

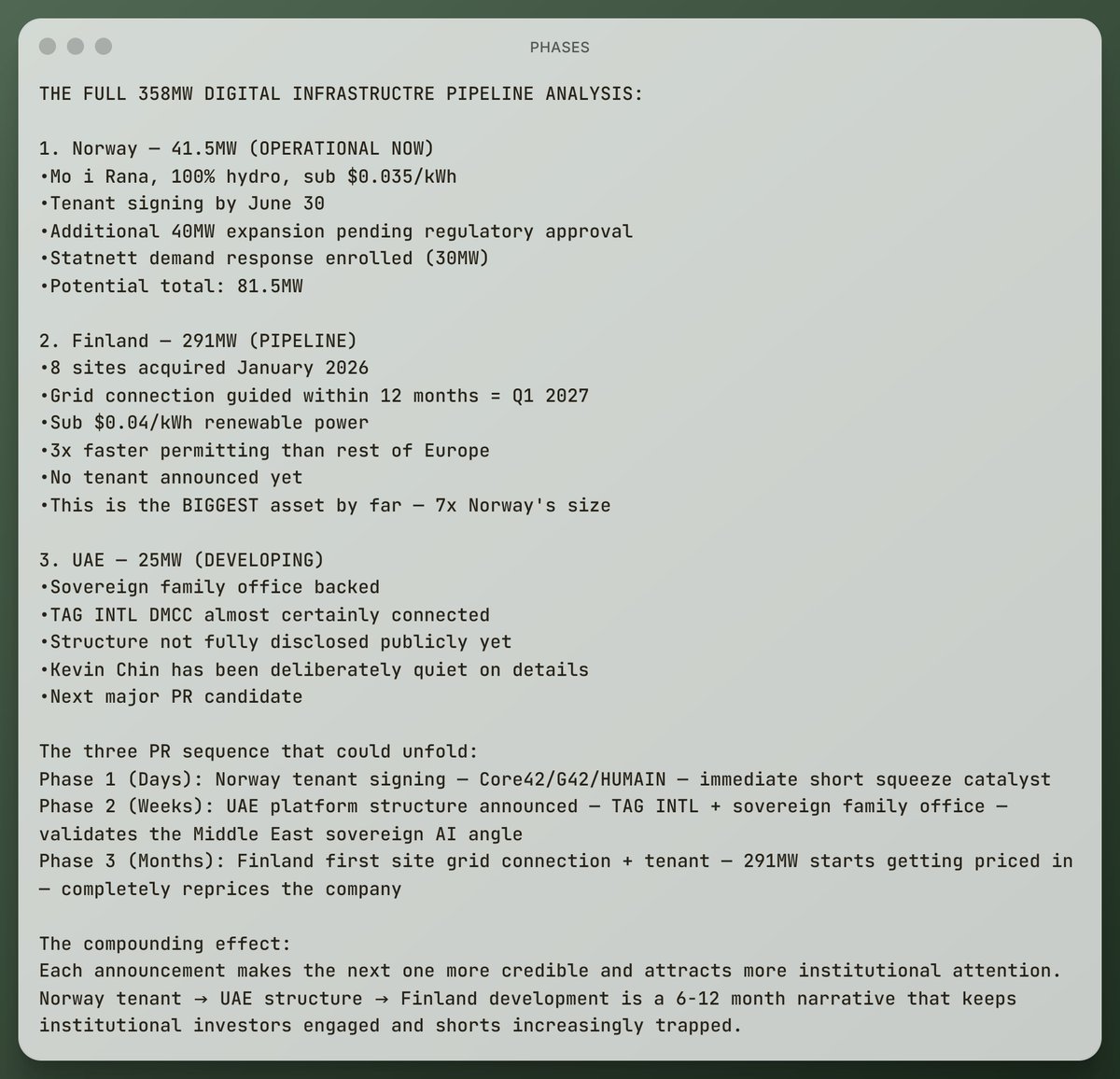

5/ 🌍 More assets in the pipeline

→ 291MW of powered land secured in Finland

→ 25MW data center platform in the UAE in development

→ Focus on "Sovereign AI" – infrastructure for nations seeking AI independence

6/ 💵 Capital structure

February 2026: $VIVO closed a $30M PIPE:

→ Investors: Blue Sky Capital (NYC) Sovereign Family Offices from the GCC

→ Conversion price: $6.80 (current price ~$4.60 → still room)

→ ATM program & F3 shelf both terminated → no further dilution pressure from open markets

7/ 🔄 Clean break from crypto

VivoPower fully exited its digital asset business – with zero realized losses. Ripple Labs shares transferred to Korean partners. In return: 20% stake in KWeather worth ~$4.3M. 100% focus now on AI infrastructure. No distractions.

8/ ⚠️ The risks – honestly

→ Only 41 employees – execution at this scale will be hard

→ Convertible notes dilute at $6.80

→ Net loss last year: $14.4M

→ Market cap: ~$60M – extremely small base

→ 52W range: $1.20 to $8.88 – maximum volatility

9/ 📅 What's coming up

→ Earnings: June 3, 2026

→ Final AI tenant announcement for Norway

→ UAE data center development update

→ Potential spin-outs of Tembo (EVs) & Caret Digital

Each of these is a potential catalyst in both directions.

⚠️ Not financial advice. DYOR.

#VIVO #VivoPower #AI #AIinfrastructure

4

1

28

2,839

Tarre86 retweeted

May 30

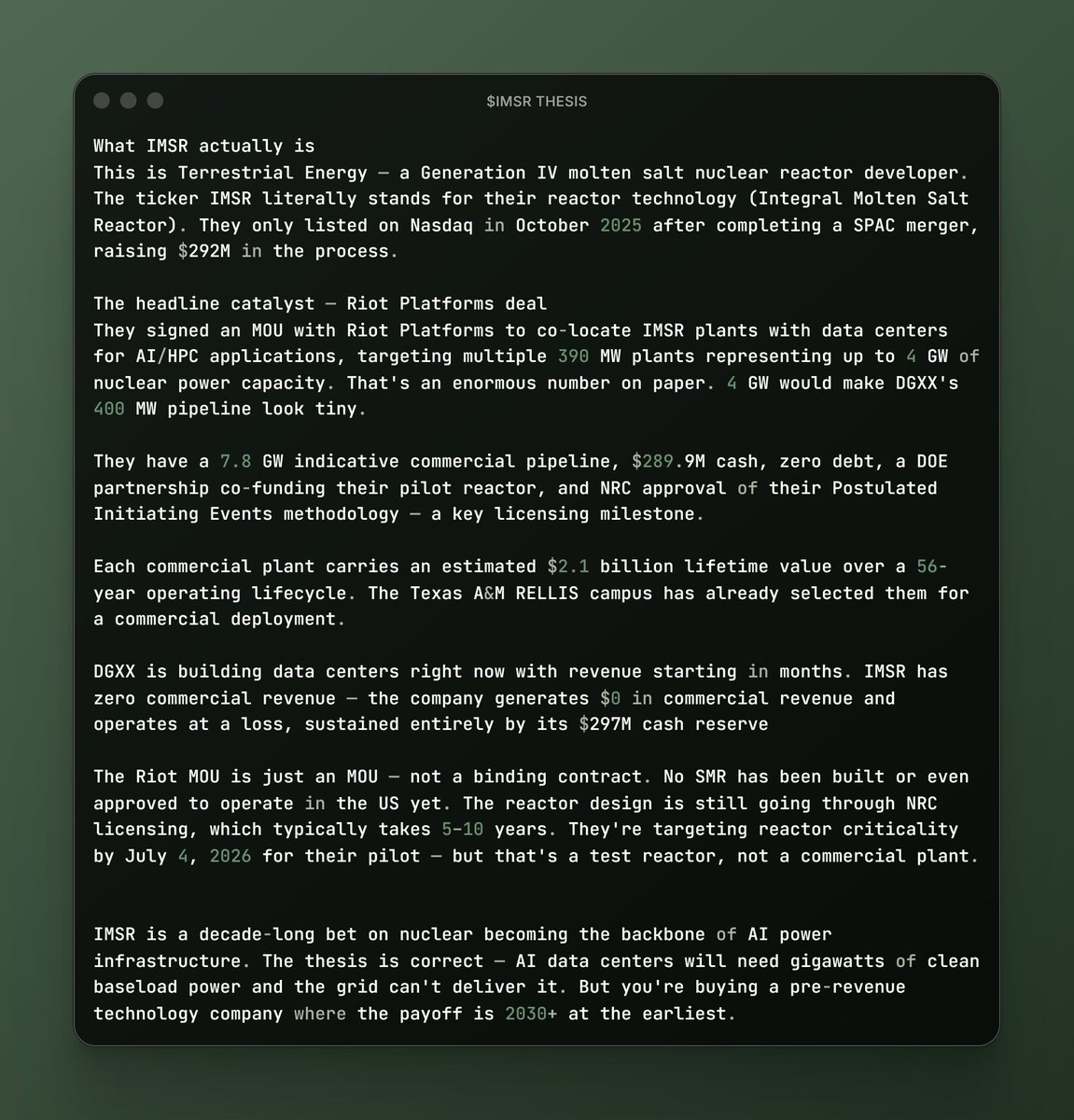

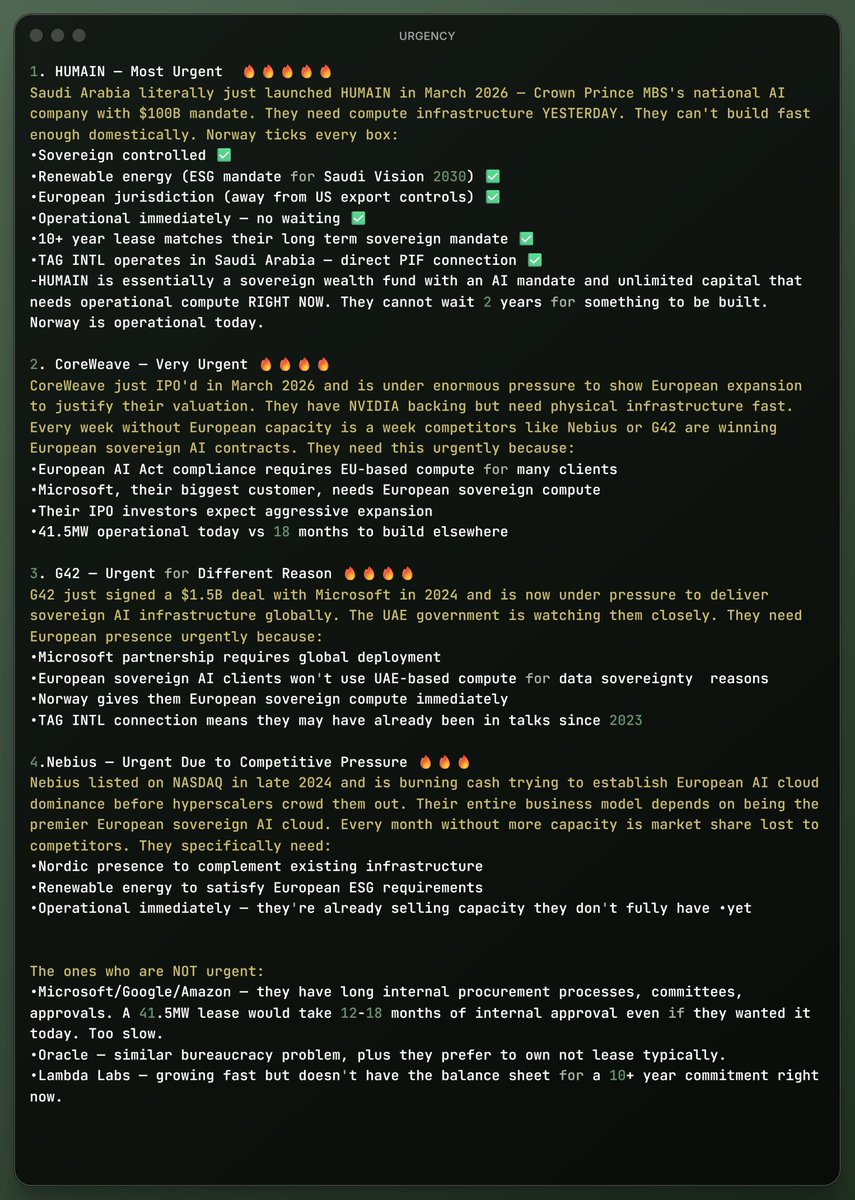

In terms of short term its definetely $VIVO due to short squeeze opportunity. $IMSR is a play betting on nuclear energy. $DGXX $VIVO $KEEL are the plays where you have the MW energy for the hyperscalers in 12-20 months speaking in the present. thesis 👇

$DGXX $IMSR

2

1

11

1,004

Tarre86 retweeted

May 31

$VIVO reminds me of a baby $WYFI.

WhiteFiber had two divisions, colo and HPC cloud. They pivoted to emphasize colo after the unit economics made more sense. They had similar small sites and landed several big clients like Cerebras, Nscale, and Modal Labs. Colo revenue grew 190% YoY last quarter.

VivoPower is running the same playbook, just earlier in the cycle.

They just acquired a 41.5MW operational data center in Mo i Rana, Norway, hydro-powered at under $0.035/kWh. That’s some of the cheapest power for any data center in Europe. There’s another 40MW of expansion capacity on top of that. They’re already doing $31M in revenue and $10M in EBITDA off this one site.

They ran a formal RFP for AI tenants and the response was apparently stronger than expected. Multiple acquisition offers came in too, they turned them all down because they think the long-term lease economics are worth more. Smart. That’s the same bet WhiteFiber made early on.

The pipeline is what makes this interesting. They have 8 sites under negotiation in Finland (291MW of powered land) and another site under development in the UAE. The “sovereign AI” angle, partnering with nations that want domestic compute infrastructure, gives them a lane that most small-cap data center names don’t have.

Market cap is around $105M. They raised $30M via PIPE in February at a $6.80 conversion price from Blue Sky Capital and GCC sovereign family offices. For context, $WYFI is at $1.15B doing ~$83M TTM revenue. $VIVO is at a fraction of that valuation with a real asset, real revenue, and a tenant pipeline that’s about to convert.

The risk is execution. They need to finalize these tenant agreements, target is end of June. They need the Finland sites to progress. And they’re still a micro-cap with all the liquidity risk that comes with it.

But if they land quality tenants on long-term contracts the way WhiteFiber did with Nscale and $CBRS, this re-rates.

A deal with $NBIS or Nscale would absolutely send it.

2

5

62

5,491

Tarre86 retweeted

May 16

🚀 FINANCIAL FREEDOM IS MEASURED IN MEGAWATTS! 🚀

Forget the standard retail hype. If you want to make life-changing money in the current AI supercycle, don't stare at overvalued tech giants—look at the infrastructure making it all possible.

Data centers and green energy are the new digital gold. Here are the 3 absolute top picks with astronomical upside. Position yourself here, and you won't need any other stocks in your portfolio to build serious wealth! 💰👇

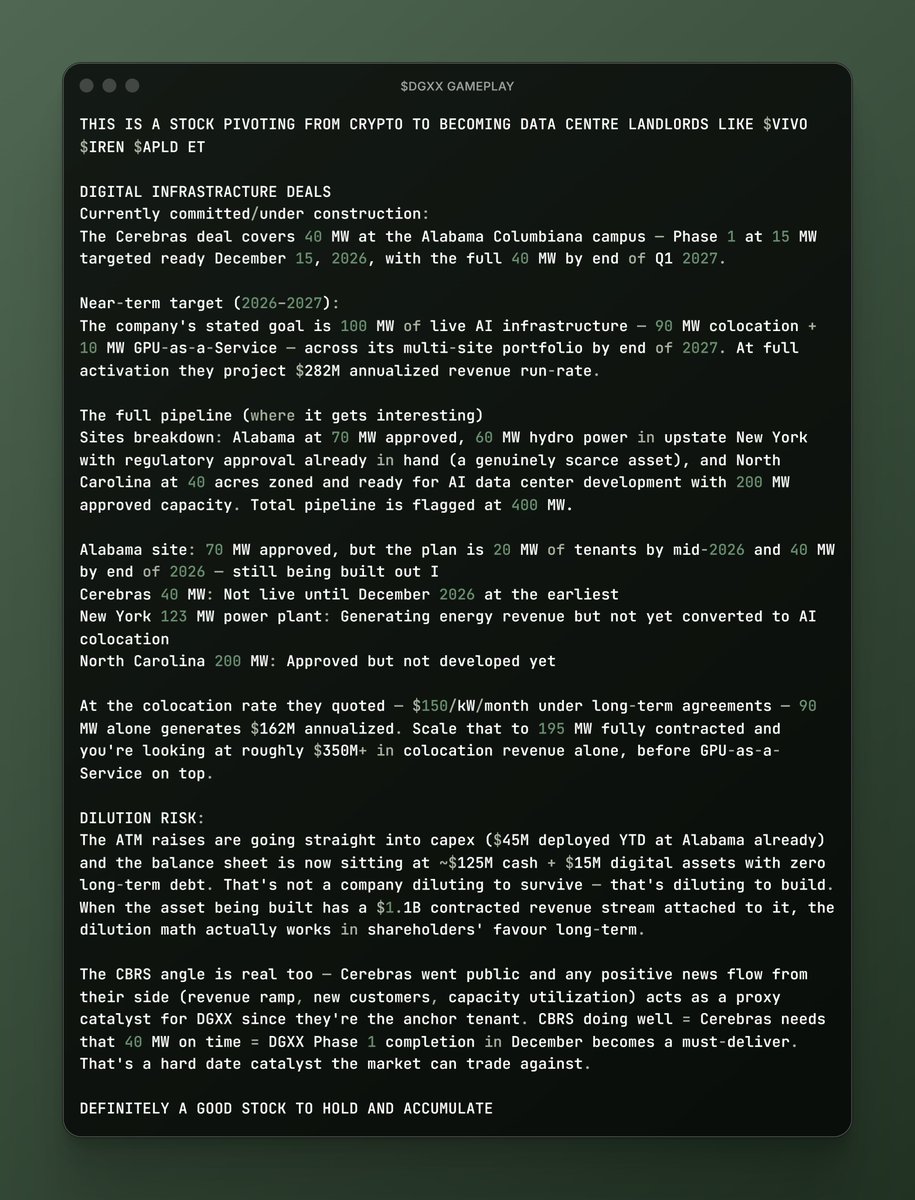

1. ⚡ $DGXX (Digi Power X) – The Foundation for Next-Gen AI

Their pivot from crypto mining to High-Performance AI Computing is a massive catalyst. The transformation is well underway, and the numbers speak for themselves.

• The Gamechanger: They have signed a massive 10-year, $1.1 billion contract for colocation infrastructure.

• The Hardware: Through their GPU cloud business NeoCloudz, initial revenues from brand-new NVIDIA B200 & B300 clusters are already starting to flow as of May 2026.

• Outlook: Management is targeting a $250 million to $300 million revenue run-rate for 2027—all while maintaining a clean balance sheet with zero long-term debt.

2. 🟢 $SLNH (Soluna Holdings) – Green Energy Meets Brute-Force Compute

AI models eat electricity for breakfast. Whoever solves this power crisis wins the entire game. Soluna targets the most critical bottleneck: the energy source.

• The Concept: They develop modular data centers located directly at renewable energy sites. They utilize excess, low-cost power for AI hosting and Bitcoin mining.

• The Leverage: With mega-projects (Dorothy and Kati) and their proprietary MaestroOS for grid optimization, they scale exactly when the tech world is desperately starving for clean energy. A pure high-leverage rocket.

3. 🌐 $VIVO (VivoPower) – The King of "Sovereign AI"

Governments and major corporations no longer want to store sensitive AI models and data on foreign soil. They demand data sovereignty. VivoPower delivers the perfect infrastructure for it.

• The Asset: They build Sovereign AI Data Centers powered 100% by local hydropower and renewable energy.

• Global Expansion: Their blueprint project in Mo i Rana, Norway, is already live. Mega-projects in the UAE and Finland are next in line. This is an incredibly rare, infrastructure-backed moat!

🔥 Bottom Line:

While the masses are still chasing overpriced legacy tech stocks, smart investors are securing the strategic bottlenecks of tomorrow: compute, space, and power. Betting on the trio of $DGXX, $SLNH, and $VIVO perfectly covers the entire sector. Strap in—the upside is absolutely massive!

#DGXX #AI #DataCenter #Crypto #GrowthInvesting #SLNG #VIVO

May 5

A major milestone for $DGXX . $DGX.NE

Digi Power X announced a Master Services Agreement with Cerebras Systems for a purpose-built 40MW AI data center campus in Columbiana, Alabama.

Initial 10-year term: ~$1.1B

Total potential contract value: up to $2.5B

This is real validation of Digi Power X’s power-first AI infrastructure strategy.

Read More - digipowerx.com/press-release…

For Digi Power X, this is more than a contract. It is validation of the company’s power-first AI infrastructure strategy at a time when demand for high-density compute continues to accelerate.

$DGXX $DGX #digipowerx #aiinfrastructure #datacenters #aicompute #colocation #hpc #nasdaq #cerebras

4

4

31

5,453

Tarre86 retweeted

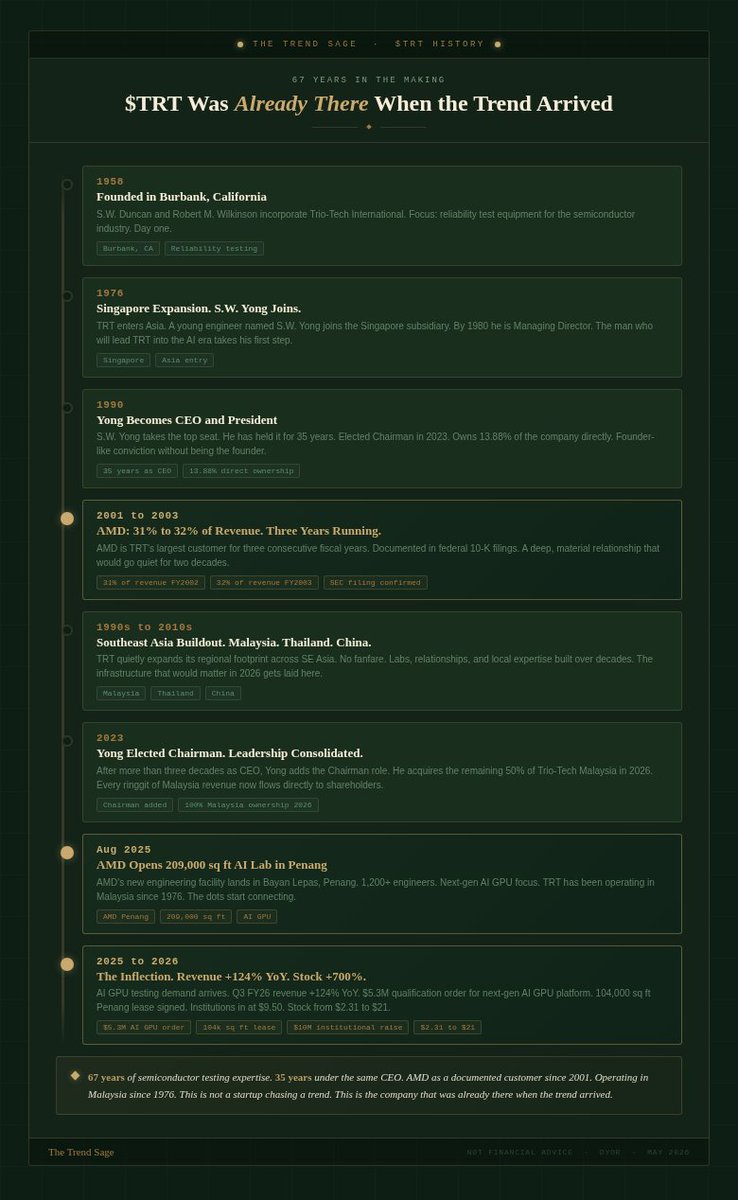

May 26

I think $TRT has room to go a lot higher this year - and maybe see $100

Here is why.

Revenue is not plateauing. It is steepening.

Q1 FY26: 58%.

Q2: 82%.

Q3: 124%.

Order book just got $10.3M in new orders in a single quarter.

- AI GPU qualification.

- Follow-on.

- Automotive IDM.

Three separate programmes.

104,000 sq ft of industrial space signed in Penang on April 28.

That is not optimism.

That is a production commitment.

Balance sheet is clean.

$29M cash.

CEO owns 13.88% directly.

No debt pressure.

No desperation.

Valuation at 3x sales with 124% revenue growth.

$AEHR does a similar job at 37x sales.

The one real bear case is gross margin at 16%.

The Penang lease adds fixed costs before the volume arrives.

H1 FY27 will be the test.

But if the ramp fills and board manufacturing scales, the operating leverage from here is significant.

The fundamentals say this has room to run.

3

27

3,894

Tarre86 retweeted

May 22

Most people think $TRT is a new story.

It is not.

This company has been operating for 67 years.

Let me give you the full history.

1958. Burbank, California.

→ S.W. Duncan and Robert M. Wilkinson incorporate Trio-Tech International.

→ Focus: reliability test equipment and services for the semiconductor industry.

→ The company that would one day burn-in AI chips starts in a California garage era.

1976. Singapore.

→ Trio-Tech expands into Asia.

→ A young engineer named S.W. Yong joins Trio-Tech International Pte Ltd in Singapore.

→ By 1980 he is appointed Managing Director.

→ By 1990 he is CEO and President of the whole company.

He has been running it ever since. 35 years.

1990s. Malaysia and beyond.

→ TRT builds out its Southeast Asia presence.

→ Malaysia. Thailand. China.

→ The company quietly becomes one of the most established semiconductor testing networks in the region.

No fanfare. Just execution.

2001 to 2003.

→ $AMD accounts for 31% to 32% of TRT's revenue for three consecutive fiscal years.

→ Documented in federal SEC filings.

The relationship is real, material, and significant.

2015.

→ Crede Capital Group acquires TRT, taking it private.

→ The company restructures.

→ Focus tightens on semiconductor back-end solutions.

2023.

→ Yong is elected Chairman of the Board in addition to his CEO role.

→ After more than three decades at the helm, he consolidates leadership.

→ He owns 13.88% of the company directly.

→ He is not going anywhere.

2025 to 2026.

→ AI GPU testing demand arrives.

→ Revenue accelerates from $36.5M to $62M annualised in under 12 months.

→ Q3 FY26: 124% YoY.

→ $5.3M AI GPU qualification order lands.

→ 104,000 sq ft Penang lease signed.

→ Institutions write a $10M cheque.

→ Stock runs from $2.31 to $21.

67 years of semiconductor testing expertise.

35 years under the same CEO.

AMD as a documented customer since 2001.

Now sitting at the intersection of AI GPU burn-in demand in Penang.

This is not a startup chasing a trend.

This is the company that was already there when the trend arrived.

8

3

60

3,951

Tarre86 retweeted

May 15

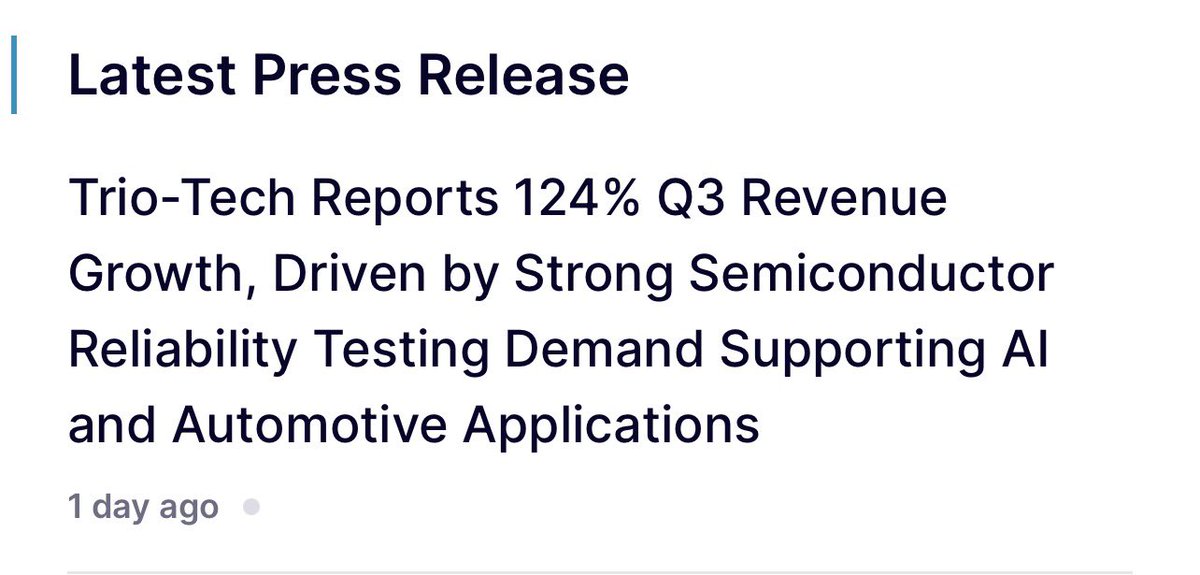

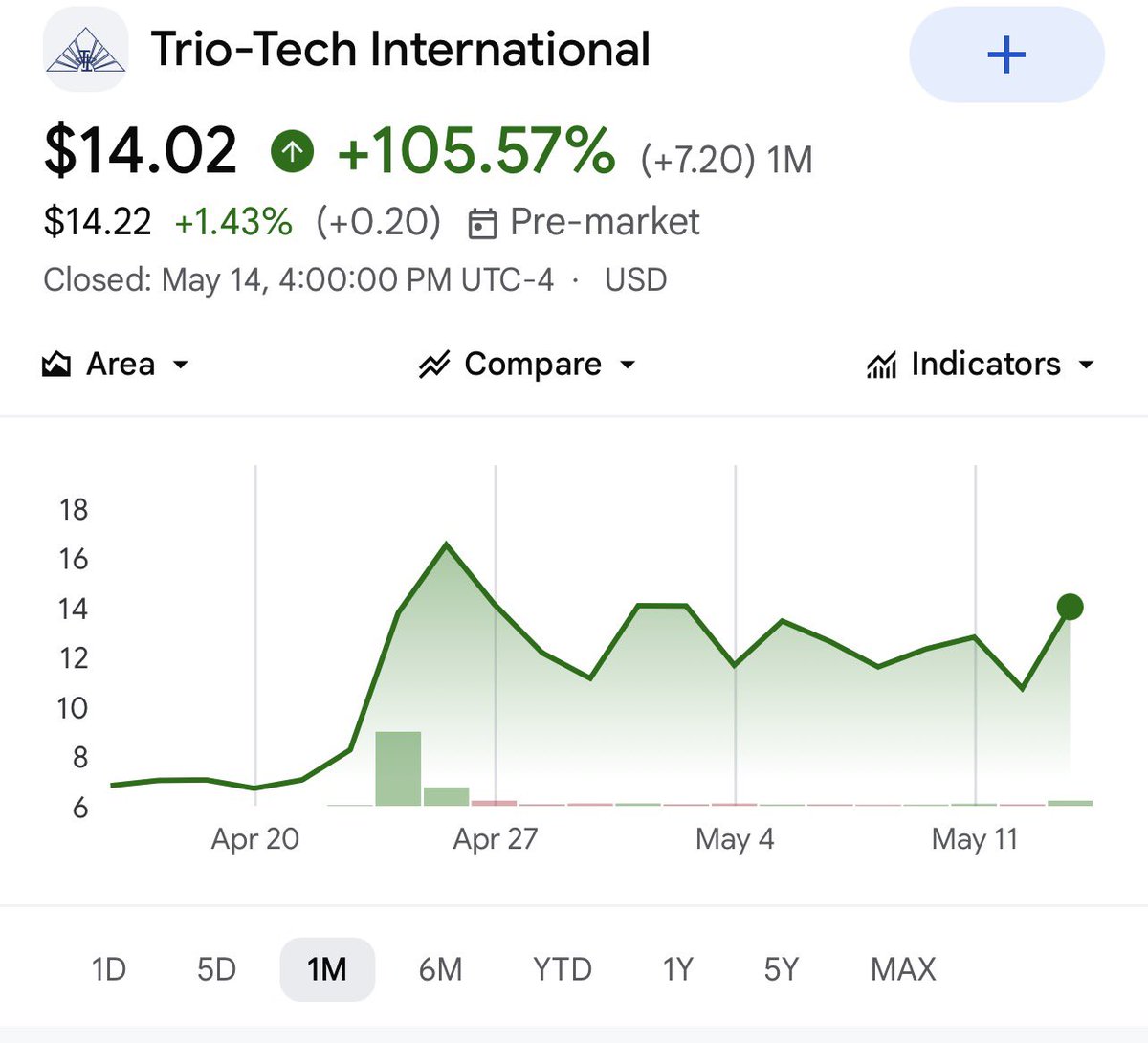

$TRT ER just dropped May 14 and it’s insane how fast this company is moving.

The revenue is not only growing it’s accelerating: Q1: 58%. Q2: 82%. Q3: 124%.

AI GPUs and EV chips can’t ship without reliability testing. $TRT runs the burn-in. $7.8M in orders already confirmed. New 104K sqft facility coming online in Malaysia.

This is $AEHR in the making. Picks and shovels for the AI and EV silicon buildout. The market is just starting to realize it.

Revenue run rate approaching $65M annualized. Balance sheet clean. Debt-to-equity 0.11.

This is still early but it’s going fast.

Complementary TA from @mkfilko, looks like a break out is bound to happen.

I’m long $TRT

NFA

10

13

92

53,177

Tarre86 retweeted

Apr 5

Every flat Earth retard should be strapped onto a rocket ship and blasted into outer space.

271

80

1,240

36,608

Tarre86 retweeted

Mar 19

Fuck Trump and fuck you

Hegseth: The world, the Middle East, our ungrateful allies in Europe, even segments of our own press should be saying one thing to President Trump: Thank you.

147

348

3,227

43,206

Tarre86 retweeted

Feb 28

I fully support regime change in Israel.

68

736

6,015

52,204