Advanced Persistent Defender. All views are my own.

Joined November 2008

- Tweets 272,059

- Following 1,531

- Followers 4,418

- Likes 866,405

4,073 Photos and videos

Pinned Tweet

28 Feb 2022

Himnas vārdos viss iekodēts:

Vēl nav mirusi 🇺🇦 slava un brīve,

Vēl mums, jaunie brāļi, uzsmaidīs veiksme.

Izplēnēs mūsu naidnieki kā rasa saulē,

Saimniekosim arī mēs, brāļi, savā zemē.

2x:

Dvēseli un miesu mēs dosim par mūsu brīvi

Un rādīsim, ka mēs, brāļi, no kazaku cilts esam

28 Feb 2022

A Russian Armor Vehicles in the town of Bucha that was Broadcasting the Propaganda Message, "Citizens, stay calm, everything is under control" was blown up by a Ukrainian Paramilitary Member earlier today with an RPG.

13

118

229

Artis Schlossberg retweeted

Jun 9

SpaceX is absolutely Kardashev-pilled

17

13

158

11,148

Artis Schlossberg retweeted

Europe needs insanely ambitious builders and investors. Right now we have neither at the scale this moment demands.

It's incredibly easy to blame politicians for everything. But Europe has another huge issue: we lack agency. We need a far higher density of ambitious builders — people who start the hard companies instead of waiting for permission.

Every industry that compounds — AI, cloud, chips, robots, space — is being built by the US and China.

AI. No European lab competes with OpenAI, Anthropic or Google. Mistral is the only contender, and an order of magnitude too small. This is the platform layer everything else will run on, and we're not in the room.

Cloud. AWS, Azure, Google — almost 0% European. Our entire digital economy runs on rented American servers. That's not a market we lost. It's leverage we handed away.

Chips. We don't design them (Nvidia, Apple), we don't manufacture them (TSMC). We own exactly one company — ASML — that builds the one machine the whole world needs. It could be Europe's first trillion-dollar company. Miss the rest of the chain and we lose that too.

Batteries & rare earths. Up to 98% come from China. A dirty, low-margin business — but lose the supply chain and the economy stops overnight. Northvolt was our shot. It collapsed into the largest bankruptcy in Swedish history, yet we should try again and again and again.

Autonomy. Waymo and Tesla in the US. Baidu, WeRide, Pony in China. Robotaxis hit European streets in 2026 — running on foreign tech.

Robots. China ships 87% of the world's humanoids. The bright spot: Germany's Neura just raised $1.4B from Nvidia and Amazon. One real bet. We need fifty.

Space. SpaceX launches 80 times a year; we're rebuilding from behind. No reusable rockets, no Starlink alternative, no answer yet as compute moves to orbit.

All of this is fixable. Not by subsidizing the past or regulating the future — by funding people audacious enough to BUILD.

Europe doesn't have a talent problem. It has a courage-and-capital problem.

Build. Build. Build.

25

12

101

4,872

Artis Schlossberg retweeted

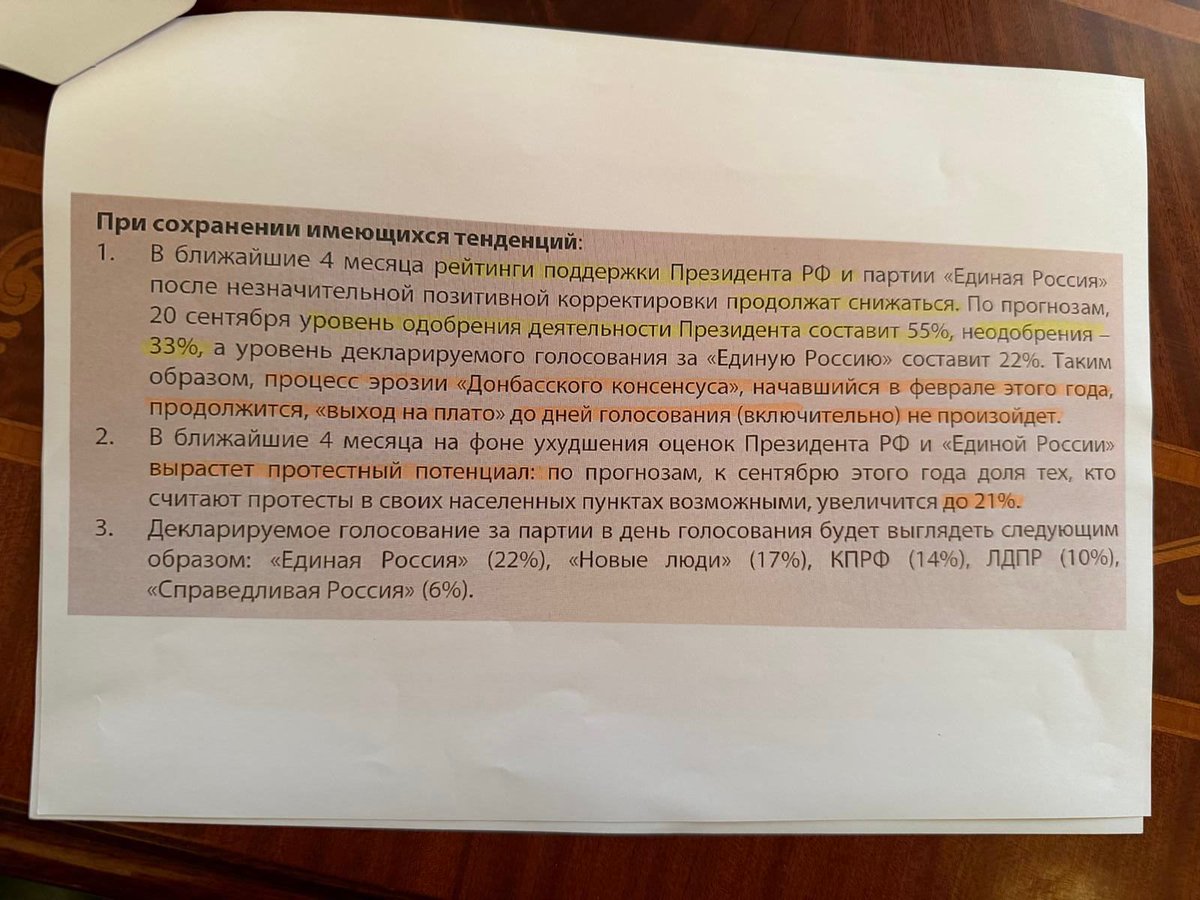

I thank all friends of Ukraine and everyone who helps us obtain important information and supports Ukrainian intelligence operations. Our intelligence agencies reported on the results of their work to assess the internal situation in Russia and obtain documents that end up on the Russian leader’s desk. We understand that Putin rarely receives information that is entirely truthful and unvarnished. But even what he sees in the documents that reach him still allows conclusions to be drawn.

In particular, the so-called “projected indicators” of Russians’ dissatisfaction with Putin will continue to rise steadily, and he is already being conditioned to accept the idea that this growing dissatisfaction cannot be stopped and that this indicator “will not plateau” by September, when parliamentary elections are scheduled in Russia.

As for the level of support for Russia’s ruling party, a steady downward trend is being recorded, which means significantly greater electoral fraud will be needed. They are also reporting a substantial rise in protest sentiment in Russian regions. We believe these reports also do not yet take into account the potential events of June, July, and August, which are bound to further affect the situation in Russia.

The entirely justified pressure on Russia over this war will continue and intensify – and it won’t be just our pressure. So by September, Putin will be facing significantly worse indicators. Unfortunately, to all the public and non-public peace proposals we have made, the only response has been words about continuing his war.

The internal situation in Russia should convince him of the opposite: that peace is needed. Ukraine is proposing to negotiate a dignified peace. Obviously, the trends will not change, and over time this may mean that an agreement will have to be reached with someone else from Russia – someone who will not shut themselves off from reality. Glory to Ukraine!

521

1,229

7,333

338,638

Artis Schlossberg retweeted

Jerry & the gang not giving you this

Jun 12

Curb Your Enthusiasm was always far superior to Seinfeld

24

727

12,419

703,609

Artis Schlossberg retweeted

Jun 12

Curb Your Enthusiasm was always far superior to Seinfeld

9

98

3,025

112,294

Artis Schlossberg retweeted

Carney: The post Cold-war world rules-based order is breaking down

The only way for medium-sized powers to avoid becoming vassals of either the United States or China is through commercial and strategic integration, as exemplified by the European Union.

The EU's internal market already exceeds €4 trillion in annual trade, and in more than 88% of EU countries, the EU itself is their largest trading partner.

Europe should continue expanding by welcoming new members while also building stronger partnerships—or even deeper forms of integration—with the United Kingdom, Canada, Latin America, the Indo-Pacific region, and Africa.

Only by creating a broad network of aligned economies and strategic interests can Europe maintain its autonomy and influence in an increasingly multipolar world

2

19

51

1,360

Artis Schlossberg retweeted

Economists valuing business over culture

As usual

Switzerland is rich partly because it is a hub for international business. It will struggle to remain so if it is closed to foreign brains econ.st/4eny8kL

Photo: Getty Images

30

51

330

18,052

Artis Schlossberg retweeted

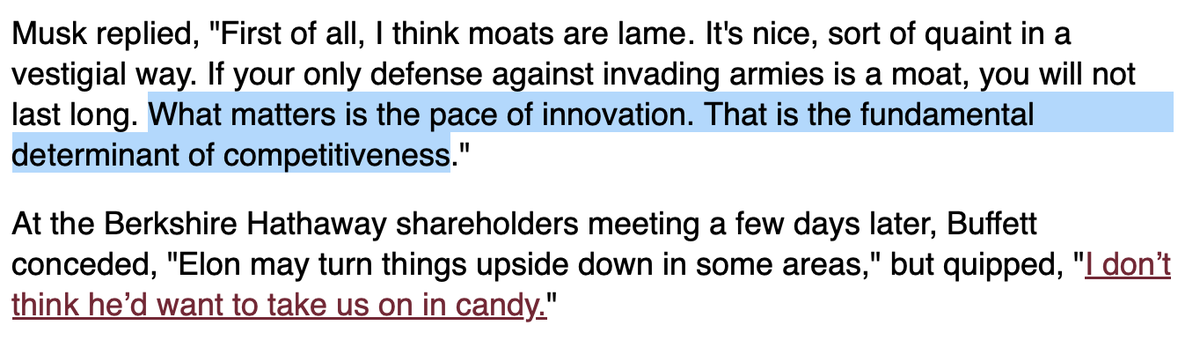

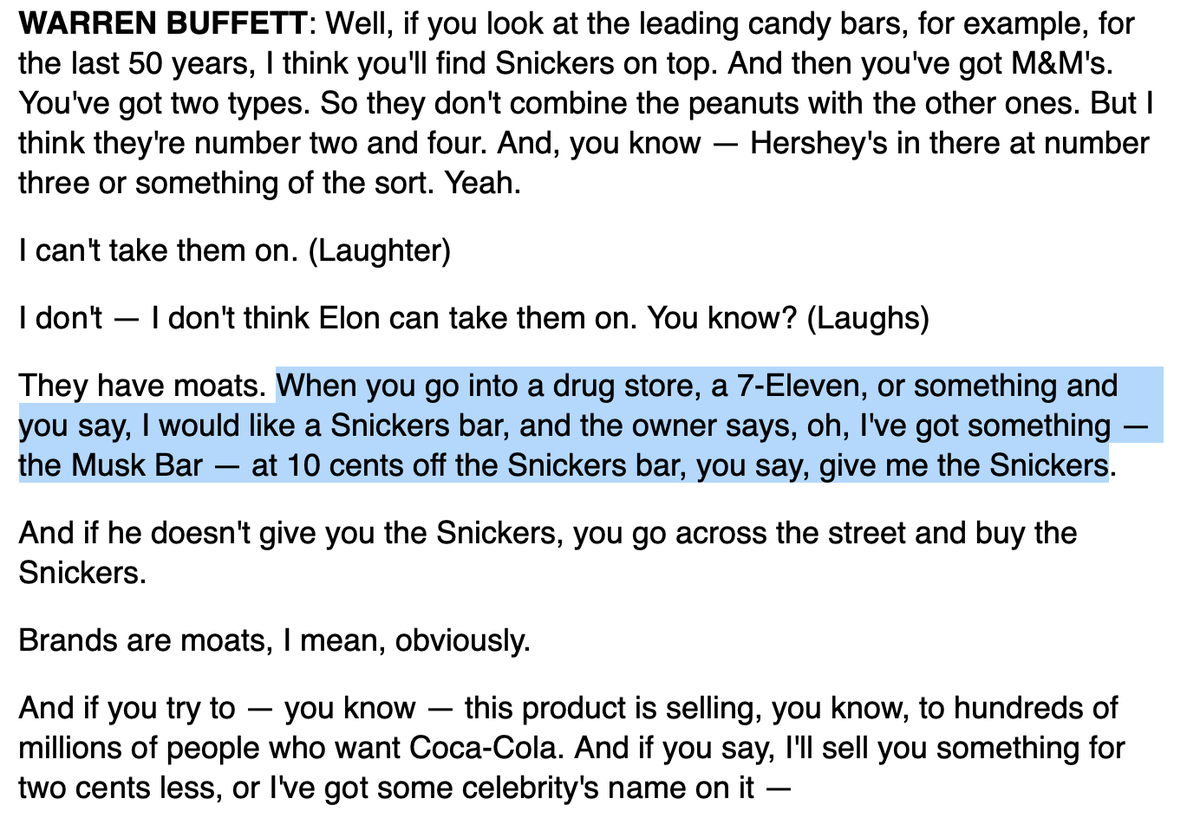

Buffett seeks to win by finding moats, which usually arise out of competitive mkt failures. Great for Buffett, who gets to extract higher rents, but not for the rest of society, which has to pay them.

Musk seeks to win by innovating faster & better than his competition. Great for everyone. In his efforts, he has created several orders of magnitude more value for the world than Buffett. There really is no comparison.

Interesting clips from CNBC's weekly Buffett email on when Buffett and Musk traded barbs on moats. I think Elon makes a great point in his quote here, and I'd love to hear what WB thinks about what he said a decade ago, specifically the idea that Snickers or M&M's brand have more pricing power than a hypothetical "Musk bar". The upstart brands (see the protein bar isle), health food focus, store brands (Kirkland, etc) and the downfall of all kinds of once powerful food brands like GIS, KHC, etc... I wonder if WB has a different view today

10

11

96

12,819

Artis Schlossberg retweeted

Russia threw the kitchen sink at Hungary’s election: bots, deepfakes, “Maidan” paranoia, anti-Ukraine hysteria, and the full Kremlin-friendly propaganda machine. GRU, SVR, the Social Design Agency - all tried to interfere. Pro-Fidesz propaganda amplified anti-Ukraine hysteria.

And still failed.

The lesson is: Russia is dangerous - but not omnipotent. The myth of an all-powerful Kremlin is itself Russian disinformation.

My comments to @Telexhu @stuthnagyniki

#authoritarianinflation

telex.hu/english/2026/06/12/…

9

54

124

3,760

Artis Schlossberg retweeted

Apsēdos pie datora un pārlasīju Riga Pride 2026 gājiena noteikumus. Vai Palestīnas karogs kā simbols no Palestīnas atbalsta bloka grupas gājiena tiešām iestājas par LGBT kopienas pamattiesībām? Kā tas simbolizē LGBT kopienas tiesības? Kādā veidā? Cik neprātīga ir šī loģika!

1

4

19

518

Artis Schlossberg retweeted

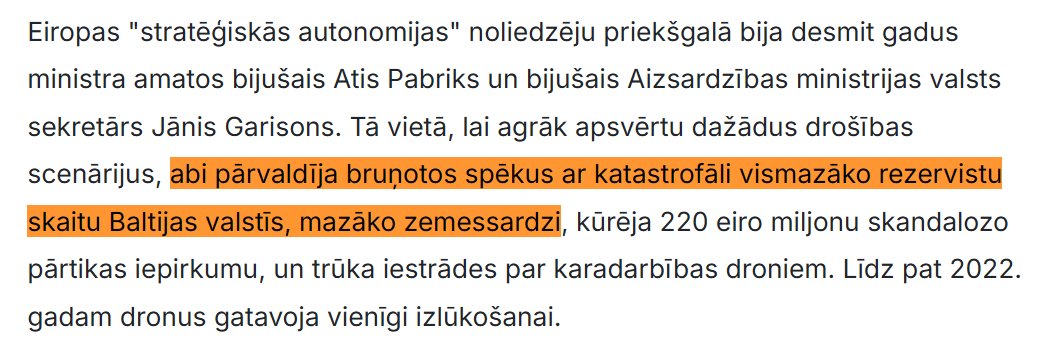

SIF apmaksātie kursiki Viesnīcu koledžā krievijas valodā. Kuras valsts skolniekus viņi apmāca krievijas valodā? Vai krievijas skolniekus?

Vai nu @IZM_gov_lv mums melo, ka visa izglītība notiek latviešu valodā vai arī @siflv pārkāpj likumu un finansē izglītību krievijas valodā?

18

30

272

Artis Schlossberg retweeted

1940. gada 15. jūnijā Lavrentijs Berija atgriezās no Kremļa un savā dienasgrāmatā rakstīja: "Koba (Staļins) pieņēma galīgo lēmumu par Baltiju. Teica - gribi vai negribi, bet [viņus] vajag sovjetizēt. Atstāt nevar. Arī nāksies pārvietot."

Gadu vēlāk - 1941. gada 14. jūnijā - viņi to izdarīja.

15 424 cilvēki vienā naktī. 5263 arestēti un nošķirti no ģimenēm. Vairāk nekā 650 vēlāk nošauti. No bada, slimībām un cita iemesla dēļ nomira vairāk nekā 3400, bet izsūtījumā nomira vairāk nekā 1400 cilvēku.

|

Šodien viņus pieminam. Un arī skaidrojam, jo faktus vēl aizvien cenšas sagrozīt.

Viens no visizplatītākajiem mītiem: ka izsūtāmo sarakstus esot sastādījuši vietējie – “greizsirdīgie kaimiņi” vai vietējie “stukači”. Tā nav patiesība. Visus izsūtāmo sarakstus sagatavoja čeka un zem katra lēmuma par deportāciju ir čekista paraksts. Operāciju vadīja PSRS valsts drošības komisāra vietnieks personīgi.

Šis mīts ticis mērķtiecīgi izplatīts, lai tā novirzītu atbildību no Kremļa uz Latviju un tā pārvērstu padomju impērijas okupācijas režīma organizētu noziegumu par "savstarpēju rēķinu kārtošanu”.

Šodien mēdzam dzirdēt aicinājumus “to visu atstāt pagātnē”. Nē. Mēs savu vēsturi nedrīkstam atdot tiem, kuri grib “atmazgāt” padomju okupāciju, relativizēt komunistisko teroru un pārrakstīt Latvijas vēsturi tā, lai agresors izskatītos pēc “atbrīvotāja”.

Šodien Krievija Ukrainā dara to pašu. Kopš 2022. gada Ukrainā pārvietoti ap 4,7 miljoniem cilvēku. Ukrainas bērni nolaupīti, deportēti un nodoti adopcijai krievu ģimenēs, Krievija mērķtiecīgi mēģina izdzēst ukraiņu identitāti.

14. jūnijs ir piemiņas diena. Tā ir diena, kurā mēs sargājam patiesību - nosaucam vārdā noziegumu, okupāciju un atbildīgos. Kamēr to darām, tikmēr Latvija nav zaudējusi ne atmiņu, ne mugurkaulu.

3

18

48

1,088

Artis Schlossberg retweeted

Jun 13

Francuzi przyznają, że transport pociągiami wojskowymi z 🇫🇷Francji do 🇵🇱Polski trwa 45 dni; Europa chce zmniejszyć ten czas do 3 dni (jest to konieczne w obliczu zagrozenia od Rosji, ale sprawa jest skomplikowana).

bfmtv.com/economie/entrepris…

61

100

710

34,769

Artis Schlossberg retweeted

Europe through the perspective of raindrops 💧

Every drop in blue ends up in the North Sea, Baltic Sea, and Atlantic Ocean.

Every drop in red ends up in the Mediterranean and Black Sea.

5

34

180

7,951

Artis Schlossberg retweeted

Jaunāko laiku vēsturē tieši 1987. gada 14. jūnijs iezīmē starta šāvienu ceļā uz Latvijas neatkarību. Visi radošo savienību plēnumi, Mavrika Vulfsona runas un Tautas frontes manifestācijas Mežaparkā bija jau pēc tam. Ir nedaudz skumji un vienlaikus nožēlojami, ka daži kādreizējie Tautas frontes aktīvisti, kuri šodien ieņem ievērojami cienījamākas sociālās pozīcijas nekā kādreizējie “Helsinki - 86” dalībnieki, cenšas minimizēt šo neatkarības cīņu celmlaužu padarīto, noklusēt viņu ieguldījumu kopējā lietā un uzsvērt tikai savu devumu neatkarības atjaunošanas procesā. Viņiem būtu biežāk jāatceras, ka viņi gāja jau pa citu izlauzto ceļu.

Traģiskajam sēru datumam, 14. jūnijam, Latvijā ir arī gaišāka, iedvesmojošāka daļa - nra.lv/neatkariga/komentari/… via @nralv

2

15

40

1,929

Artis Schlossberg retweeted

If this is about human rights why doesn’t she also cut the North Korea flag?? It’s literally right next to it.

620

501

10,268

158,266

Artis Schlossberg retweeted

20h

China is deliberately choking the global supply of Indium Phosphide (InP), the material that makes every laser in every AI data center work.

Reuters confirmed: US officials have visited China multiple times to resolve this. China is still blocking export approvals on purpose. They want to maintain the bottleneck.

Chinese producers like Yunnan Germanium (002428.SZ) and Guangdong Xiandao are scaling capacity fast (Yunnan investing $28M to reach 450K wafers/year, shipments up 74% in 2025). But even if export approvals are granted, overseas shipments will be "limited."

Switching InP suppliers requires lengthy qualification cycles. You can't just find a new source overnight. 12-18 months...

This will help explain the recent price action in the below names.

WINNERS:

$SIVE.ST CW lasers ARE InP devices. Policy-duration shortage extends their 14-quarter laser supply constraint indefinitely. Every month China maintains this, SIVE's pricing power widens.

$LITE Substrates come from Sumitomo JX Advanced Metals in Japan. Entirely outside the China export gate. Their competitor's supply gets squeezed while theirs is control-immune. This is the cleanest relative advantage.

Win Semi (3105.TW) Only pure-play III-V foundry on earth. InP wafer fab capacity is scarce globally. Tighter substrates = their existing capacity commands higher pricing.

$AEHR Sole-source wafer-level burn-in testing for InP and SiPh devices. When every wafer is more valuable because the input material is scarce, the cost of shipping a bad one goes up. Testing intensity rises with scarcity.

AIXA (AIXA.DE) Makes the MOCVD equipment needed for InP epitaxy. Every country trying to build domestic InP capacity needs their tools. More fragmentation = more equipment orders.

$SOI.PA Photonics-SOI monopoly. InP scarcity makes the entire optical layer more expensive, increasing the value of every component in the stack including Smart Cut SOI wafers.

LOSERS:

$COHR Reuters specifically names Coherent as "mainly supplied by AXT." AXT manufactures IN China, inside the export gate. Even if approvals come, shipments will be limited. COHR carries a substrate risk that LITE does not. And switching requires lengthy qualification cycles.

$AAOI Demand is not the issue; laser/EML/InP component supply is. If AAOI cannot secure enough laser chips, capacity ramp can slow.

$AXTI AXT is a US-listed InP substrate maker that manufactures in China. Their entire equity value is an export-approval question. If approvals flow, massive upside. If they don't, the business model breaks for Western customers.

We are watching real-time supply chain warfare over AI supremacy. The companies that own the physical bottlenecks in this chain benefit every time the world fragments.

Reuters: U.S. officials have visited China multiple times and urged the Chinese side to resolve the InP export controls, but China is still causing delays in export approvals.

As a result, U.S. photonic chip manufacturers that need InP are facing difficulties.

However, China does not appear to be particularly favoring domestic Chinese companies over U.S. companies operating in China. China wants to maintain the bottleneck the U.S. is facing in InP, so most Chinese domestic InP producers are focusing on the domestic market.

Chinese InP manufacturers such as Yunnan Germanium and Guangdong Xiandao are both in talks with Chinese authorities to secure export approvals, but even if approvals are granted, overseas shipments are likely to remain limited.

31

64

467

105,007

Artis Schlossberg retweeted

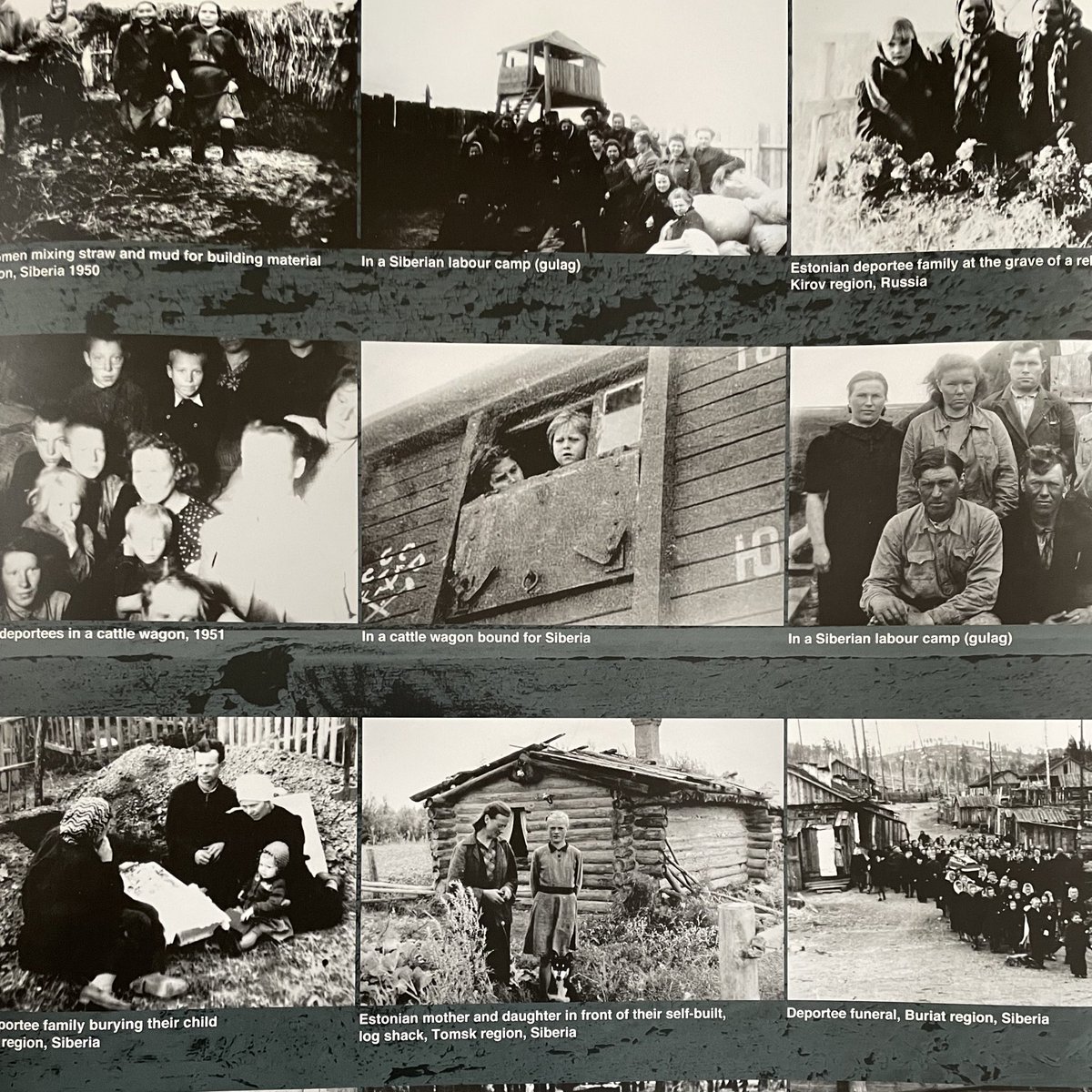

In the early hours of this day 85 years ago, thousands of families across Estonia were woken by a knock on the door, only to be torn from their homes and deported to Siberia by the Soviet regime.

During the June 1941 deportations, around 10,000 Estonians, together with tens of thousands of Latvians and Lithuanians, fell victim to Soviet terror.

As we honour the victims of these crimes, we must also remember that Russia is using many of the same methods in Ukraine today — deporting children, terrorising civilians, and attempting to erase Ukrainian identity.

History teaches us that crimes left unpunished lead to further aggression. It is time to hold Russia accountable.

66

223

438

47,378

Artis Schlossberg retweeted

Paldies, šis ir svarīgs aspekts-kā strādā poilitbizness, kuram uz nācijas vajadzībām uzspļaut.

Tīrīt migrantu kabatas un pasliktināt pamatnācijas stāvokli ir metušies visi, gan augstskolas, gan celtnieki, gan pārējie darboņi...

Jun 12

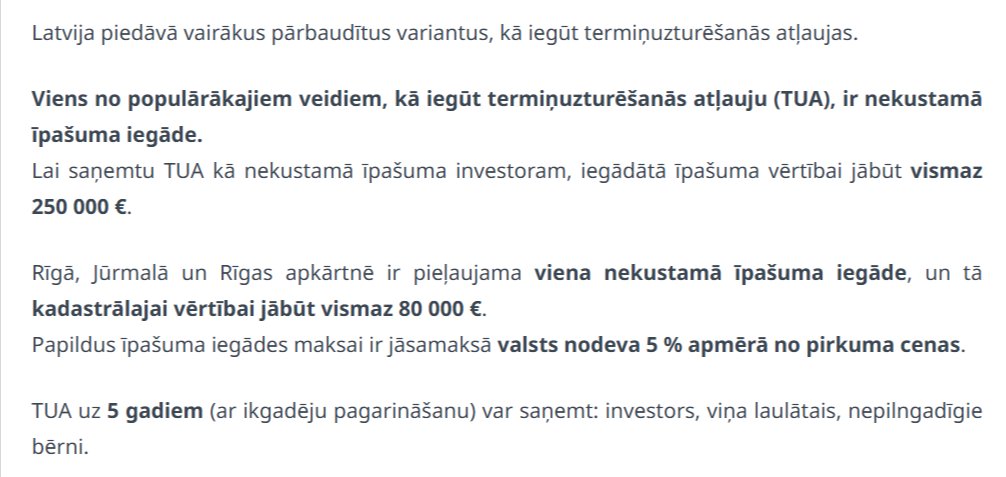

Saeima čakli nobalsojusi par "zelta vīzu". Nu re, draugi, izlasiet šo manu tekstiņu par to, kas šobrīd Eiropā un Latvijā ir tie, kas pasūta migrāciju. lasi.lv/par-svarigo/latvija/…

2

11

26

905

Artis Schlossberg retweeted

14.jūnijs. Melna diena Latvijai. Reta tā ğimene, kuru padomju represijas neskāra. Nekad netici komunistam. Mūslaikos viņi mēdz sēdēt visur. Vietvarās, Eiropā, ministrijās. Viņi vienmēr grib atņemt, pārdalīt, ievākties Tavā mājā un nestrādāt.

3

39

95

2,241