Student of life! Learning never ends! No post or RT is an investment recommendation. Do your own research.

Joined November 2021

- Tweets 2,232

- Following 234

- Followers 722

- Likes 4,816

Photos and videos

Jun 12

Thank You Chris!

Jun 11

15

2,256

Jun 12

$TBBB BBB Foods Inc. is Mexico's equivalent of Aldi. Bueno, Bonito y Barato ("Good, Nice, and Affordable")

The business model is similar to Aldi and Lidl: small stores, limited SKUs, high inventory turns, and heavy private-label penetration. Perfect pick for your defensive side of portfolio. Will be a beneficiary of Americas reindustrialization.

Some Chat GPT dig:

What makes the story attractive?

1. Exceptional store growth

The company has been expanding at a remarkable pace:

Year-end Stores

2023 ~2,288

2025 3,346

Q1 2026 3,469

Management opened 574 net stores in 2025 and 123 more in Q1 2026 alone. For 2026, guidance is approximately 590–630 additional stores.

2. Revenue growth remains very strong

Recent results show:

Period Revenue Growth

FY2025 36.1%

Q4 2025 34.4%

Q1 2026 33.4%

Same-store sales growth has also remained unusually strong for a mature retailer:

Period Same-Store Sales Growth

FY2025 18.3%

Q4 2025 16.6%

Q1 2026 16.0%

Mar 6

1

2

626

Jun 12

Masterclass part II

Jun 11

Two more things:

1. I’m hearing is that there was a privately negotiated “make-whole” to induce old convert holders to get called early. If that’s the case, the make-whole premium could’ve been in cash or stock and could’ve been on sweetheart terms better than stipulated in the original make-whole matrix. I’ve executed many a private “flush out” transaction in the past to allow companies to equities their debt. Certainly, if the make-whole was from additional shares, that could explain some of the earlier selling in the week.

2. Because $PCT is very difficult to borrow, bookrunners sometimes line up a term borrow facility and offer the synethic delta hedge as part of a “Happy Meal” to arbs. I don’t know for certain, but it would not surprise me if this was part of the deal especially since the additional share issuance would help unwind the synthetic short in short order.

Either or both of these possibilities would explain a lot of the price action from the prior days but also would bolster my belief that whatever hedging needed to be done has already been done.

1

18

1,997

fred thomas retweeted

Jun 11

$PCT Convert Arb 101, 6/11/26:

After speaking with some of my old convert arb coverage today (I did convert arb for over two decades in a former life), here’s my 2c on the new convert deal and share offering.

Old convert was on 100% delta, except for Sylebra’s $50 mm outright position. Net delta shares “to cover”: ~13.5 mm

New convert also sold on 100% delta, net of $36 mm over allotment (“shoe”) and net of Sylebra rolling into $50 mm of new bonds. Net delta shares to short: ~21.9 mm.

Theoretical net amount to short: 7.8 mm

New share issuance of 17.7 mm shares was placed at least 80% into “strong hands”/LT holders, which leaves only 3.5 mm sh up for churn. Between the 7.8 mm “to short” and the 3.5 mm up for churn that’s 11.3 mm shares potentially for sale.

Total dilution is about 14%. Sh out was 180 mm before today, and after today, it’s about 206.3 mm. Between that and today’s massive “volume” of 37 mm shares and stock decline, situation looks heavy right?

It’s the OPPOSITE, and here’s why:

Having been in this market for almost 25 years, I can tell you that these offerings are almost always preceded by folks “in the know” pre-positioning. Stock declined from $14 over the last several days to be priced at $8.21 today. You think that was a surprise to the arbs? I wouldn’t count on it.

Of the 11.3 mm shares “for sale” I am willing to bet that 50-75% of that was hedged in the prior couple days. Arbs likely OVER-hedged into today and net COVERED today.

Why was the volume so heavy? That’s another thing outsiders don’t get. When convert deals are sold “on swap” to arbs, the volume is double counted — buyers buy with a delta hedge and the sellers sell with a delta hedge. Today’s deal also involved an old deal getting unwound “on swap,” so the volume could have been artificially 4x’ed just based on these swap transactions.

The upshot of this is that I think the technicals are very asymmetric to the upside, and contrary to what it looks like, I think there is little to no overhang from this. I bought risk reversals today and effectively doubled my delta exposure today.

Finally, prior to today, my biggest fundamental concern for this company was their funding gap next year, and it made me queasy that they seemed to be counting on warrant exercise to close that gap. Today, they closed that gap, and even though I think they could have executed better, I think the fundamental story just got a lot more compelling as well.

26

15

206

23,522

fred thomas retweeted

Jun 11

Agree.

As an ex-convert arb, I can tell you that most delta-hedge pre-positioning is done ahead of time and/or via “happy meals” where hard to borrow stocks (like this) are often made available to short via a special swap facility in order to get hedges to buy the convert.

Sell the rumor/buy the fact is the likely outcome in these situations.

3

3

24

4,631

Jun 10

$PCT 7m shares covered from 3 weeks ago. Price at peak short was below $7. We could go lower from here.

5

1

21

3,533

Jun 3

$PG It should work for Dawn @ProcterGamble

Jun 3

$PCT performs in the most demanding applications because the product IS virgin quality. Currently there are ZERO mechanically recycled resins that work in hinge applications (it is extremely tough!).

Like Bruckner for film, Stacktech is a gatekeeper in the injection molding space and brands look to them for assurance a product works as advertised.

Stacktech works with many of the large brands, and there is now exactly ONE resin that will meet regulatory mandates and have the product quality to work in hinge applications.

There are some hints/ interesting products listed on StackTeck’s website:

1

34

1,823

fred thomas retweeted

Jun 3

$PCT performs in the most demanding applications because the product IS virgin quality. Currently there are ZERO mechanically recycled resins that work in hinge applications (it is extremely tough!).

Like Bruckner for film, Stacktech is a gatekeeper in the injection molding space and brands look to them for assurance a product works as advertised.

Stacktech works with many of the large brands, and there is now exactly ONE resin that will meet regulatory mandates and have the product quality to work in hinge applications.

There are some hints/ interesting products listed on StackTeck’s website:

Living hinge caps are one of the toughest tests for recycled polypropylene.

PureCycle and StackTeck have now successfully produced living hinge caps using up to 100% PureFive® recycled PP resin, with lids passing hundreds of flex cycles without failure.

purecycle.com/blog/purecycle…

5

20

127

15,257

Jun 3

Bill, so much alpha in this statement. If I understand who's on the other side of the trade and has picked the wrong ticker, then, there is plenty opportunity there to harvest yield. $PCT

Jun 3

they only respect pain fred, the real covering will only happen higher. that has been the pattern for the last couple years. they dont do research and dont cover on weakness, only strength. amatuers.

32

3,784

Jun 3

Some minor Leaguers covering.

1

15

1,199

May 29

$SBUX Starbucks is using PE for cold drinks and Seda paper lids for hot beverages in EU. There is less incentive to change when they have a favorable mix for mass balance there. rPP lids are for North America. Here they use 3% recycled plastic in customer facing packaging. They are hoping to get that to 50% in 4 years. Hell they will be knocking on Purecycle door and begging for some PureFive®. (😀IMHO)

1

22

1,006

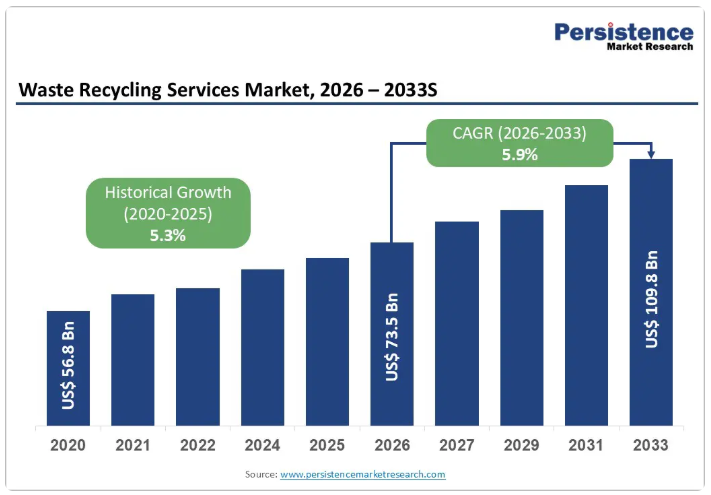

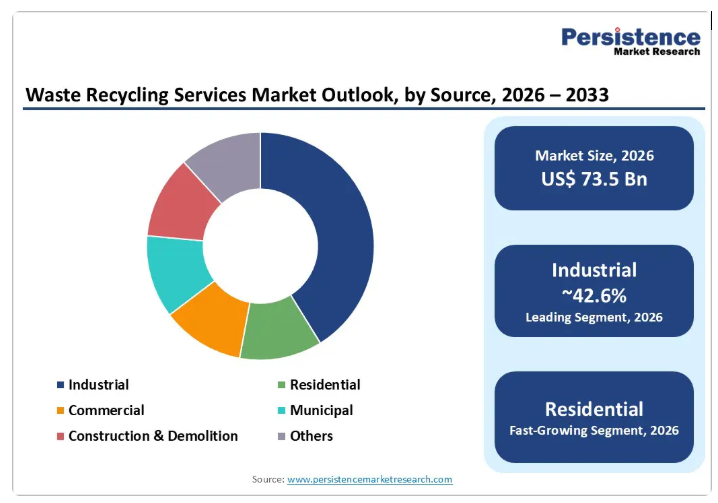

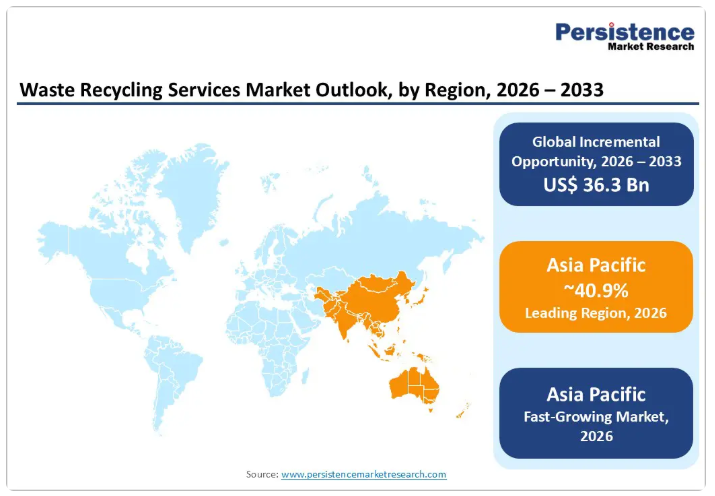

May 29

Waste Recycling Industry

For people interested in bigger picture. Link below.

3

1

16

879

May 29

$PCT Response from Dustin Olson to Beyond Plastics claims:

The recent discussion sparked by the Beyond Plastics report on the recyclability of Starbucks’ polypropylene (PP) cold cups raises a fundamental question for our industry: how should “recyclability” be evaluated in modern recycling systems?

Follow-up reporting from Antoinette Smith at Resource Recycling, Inc. explores some of the flaws of the original study by highlighting an important operational reality that many outside the industry may not realize. Recycling facilities are specifically designed to identify and remove contaminants like batteries, electronics, and metals from the stream. That matters because the study relied on battery-powered electronic trackers embedded inside cups to track their movement.

If a recycling system is intentionally designed to identify and remove electronics from the stream for safety and operational reasons, then the presence of a tracker can directly influence how that package moves through the system. In our Denver, PA sorting facility, we would also reject this piece of plastic with a tracker device to prevent further downstream contamination.

This doesn’t mean that we shouldn’t validate if recycling claims are true. But it should give everyone pause before jumping to conclusions based on a few isolated data points. Plastic is complex, these recycling systems are sophisticated, and cursory evaluations risk undermining the progress the industry is making.

It also reinforces a broader point. Recyclability is not determined solely by whether a single item can be traced from disposal to reuse. It depends on the system’s broader capabilities and scale. That capability grows with continued investment in sorting, processing, and end-market infrastructure. Every dollar put into recovery systems expands the set of materials that can be called “recyclable” in practice, not just in theory.

For PP, these systems and technologies are evolving rapidly. At PureCycle Technologies, we’ve seen firsthand how investments in PP recovery and processing infrastructure are expanding what’s possible. More material can be put into the recycling bin and recovered through advanced Materials Recovery Facility systems. End-market demand is growing, and brands are increasingly looking for recycled PP that can meet both sustainability and performance expectations.

Recycling is different today. It is more complex, more technical, and varies significantly by material and region. Progress isn’t a straight line, it’s bumpy, but companies like Starbucks and PureCycle are creating positive change and more should follow.

I encourage you to read Antoinette's full article that shares important commentary from fellow recyclers and key stakeholders in our industry. You’ll also see a few more of these photos with Starbucks cups being recycled by our team at PureCycle.

May 26

Industry response to Beyond Plastics

resource-recycling.com/plast…

3

4

42

4,912

May 28

I agree people may not like #13. But it could be the charm!

May 28

I dunno Fred, looks to me like you identified the legendary recycled PP cap to a beautiful $pct cup and handle! Break $13.50 and we appear to be going to $20 or $30 depending on whether you choose to use a linear or logarithmic y-axis. DYODD

5

1,485

May 28

Is PP thermoforming recyclable? How about HDPE?

May 28

Thermoforming retains its strength in plastics processing plasticsnews.com/end-markets…

4

748