Joined December 2021

- Tweets 1,218

- Following 55

- Followers 91,092

- Likes 1,373

533 Photos and videos

Pinned Tweet

Mar 4

Welcome to the home for developers building on tx.

Discover technical content, builder resources, and community voices from the innovators building the future of tokenized finance.

12

32

125

11,381

RT @jaebersole1: Doing tokenized stocks right takes time. Rushing leads to delivery failures.

@SoloTex_com Stock Tokens — coming shortly v…

71

tx Developer Hub retweeted

May 27

Real world assets deserve a purpose-built destination.

One app. Every asset class. All in your pocket.

Stay tuned for more details.

39

92

223

14,349

May 19

RT @txEcosystem: tx leadership was fortunate to meet with SEC Crypto Task Force staff today.

The tx team presented materials focused on th…

82

2

tx Developer Hub retweeted

May 19

May 19

SEC Chair Paul Atkins: 🇺🇸“All U.S. markets will be on chain within two years.”

Looks like this happening very SOON!

17

48

137

12,577

tx Developer Hub retweeted

May 19

@txEcosystem is grateful for today’s conversation with the Crypto Task Force. Its members bring impressive technical and legal savvy, and we appreciate such thoughtful public servants engaging directly with industry. sec.gov/files/ctf-memo-tx-la…

May 19

Today, @txEcosystem met with the SEC to discuss the future of tokenized RWAs and blockchain-powered capital markets.

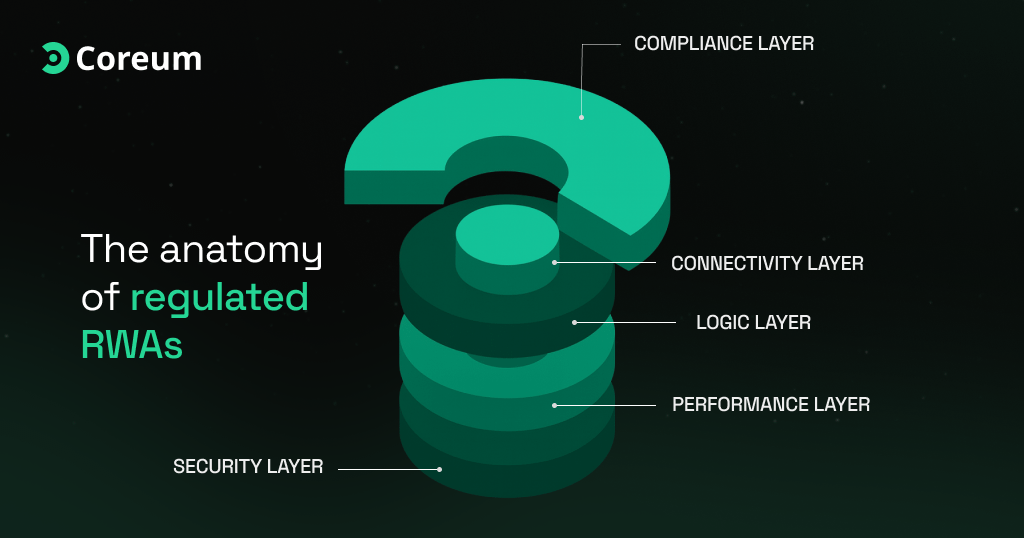

We shared TX’s vision for compliance-first infrastructure supporting regulated financial assets onchain through licensed partners.

The next era of finance will be built onchain.

15

57

144

11,569

May 19

RT @MikeMcC1uskey: Today, @txEcosystem met with the SEC to discuss the future of tokenized RWAs and blockchain-powered capital markets.

We…

124

1

May 8

RT @txEcosystem: Consensus Miami is in the books.

An energizing week of productive conversations, new connections, and shared conviction o…

54

May 7

RT @jaebersole1: Loving every minute with investors, media, and partners for @txEcosystem at @consensus2026. But grateful & still nostalgic…

33

May 6

RT @txEcosystem: Day 1 of @consensus2026 in motion.

The tx team is in the mix with builders, partners, and operators shaping the digital a…

59

tx Developer Hub retweeted

Apr 19

Migrate your liquidity from @osmosis to CruiseControl now!

From : app.osmosis.zone/pool/2501

To : app.cruise-control.xyz/trade…

Why? 🧵

4

18

35

2,609

tx Developer Hub retweeted

Apr 19

This weeks pod is with Ashley Ebersole, CoFounder and CLO of @txEcosystem.

Regulation isn’t blocking progress — it’s unlocking trillions by bringing in institutions like BlackRock and Fidelity. Tokenized real estate, credit, and more will enable seamless global investing with built-in programmable compliance. Fragmentation remains the main drag, but liquidity institutions = mainstream scale.

9

48

123

16,634

Apr 17

RT @txEcosystem: That's a wrap on @ParisBlockWeek 🇫🇷

Great conversations. Real signal on where real-world assets are headed. t.co/…

54

tx Developer Hub retweeted

Apr 16

Looking forward to joining Bitcoin.com News at 2:30. @ParisBlockWeek is the perfect venue to discuss the unification of growth, liquidity, and regulatory compliance that will drive the next growth phase of #onchain assets — led by #RWA tokenization. @txEcosystem

Apr 16

We’re live again from the Louvre for day 2 of our Paris Blockchain Week coverage. Bringing you real-time interviews with founders, exchanges, institutions, and builders shaping the next phase of crypto. Expect conversations on:

-Institutional adoption

-Tokenization & RWAs

-MiCA and European regulation -Stablecoins & onchain finance

Guests include:

-Myles Harrison of @AMINABankGlobal

-@F_Gregaard CEO of @Cardano_CF

-Vlad Maltsev from @WhiteBit

-Robby Yung (@viewfromhk) from @animocabrands

-Ashley Ebersole (@jaebersole1) from @txEcosystem

-@amarmic from @ParisBlockWeek

-Arthur Firstov (@soultaker_eth) from @Mercuryo_io

And more!

4

24

57

3,988

tx Developer Hub retweeted

Apr 16

A powerful aspect of #RWAs on-chain: asset-agnostic infrastructure.

Real estate data is a starting point.

Once @txEcosystem is live, each new asset makes the next easier and quicker.

That’s when things get interesting 🤯

From Records to Real Estate Markets: The Hidden Implications of Putting 160M Property Data On-Chain

The implications of TX partnering with Siftr to bring 160 million U.S. property, ownership, and mortgage records on-chain are much bigger than they appear at first glance.

While it may seem like “just data,” this move could reshape how real estate, finance, and even compliance systems operate over time.

🧠 1. Standardizing a fragmented system

Real estate data in the U.S. is extremely fragmented. Records are spread across thousands of counties, each with different formats, standards, and levels of accuracy. This creates inefficiencies for investors, lenders, insurers, and even governments.

By aggregating and structuring this data into a unified, verifiable system, TX Siftr are essentially attempting to create a single source of truth. That alone is powerful. It reduces:

data discrepancies

manual verification costs

delays in transactions

The result is a more efficient and transparent real estate ecosystem.

⚙️ 2. Enabling programmable real estate

Once property data is structured and accessible on-chain, it becomes programmable.

This means:

automated underwriting

instant risk scoring

smart contract-based lending

Instead of manually reviewing documents, systems could automatically evaluate:

ownership history

liens and mortgages

valuation trends

This is similar to how APIs transformed finance — but now applied to real estate.

💰 3. Unlocking new financial products

Clean, trusted data is the foundation for financial innovation. With this infrastructure, new products become possible:

fractional ownership platforms

on-chain mortgage markets

real estate-backed lending protocols

tokenized property funds

Importantly, none of these can scale without reliable data. This move is less about the end product and more about enabling everything that comes after.

🏦 4. Institutional adoption

Institutions (banks, hedge funds, insurers) care less about hype and more about data reliability and compliance.

Bringing verified property data on-chain creates a bridge between traditional finance and blockchain systems.

If the data layer is trusted, institutions can:

plug into on-chain systems

automate due diligence

reduce operational risk

This is a key step toward bringing institutional capital into blockchain-based real-world assets (RWAs).

🔍 5. Transparency and auditability

Blockchain introduces immutability — once data is recorded, it cannot be altered without trace.

For real estate, this means:

clearer ownership histories

reduced fraud risk

easier auditing

This could be particularly valuable in areas where records are inconsistent or disputed. Over time, it may even influence how governments manage land registries.

⚠️ 6. Limits and challenges

Despite the potential, there are important limitations:

Legal ownership is still off-chain

Property rights are enforced by governments, not blockchains.

Data quality remains critical

If the input data is flawed, the system inherits those flaws.

Regulatory hurdles

Integrating blockchain with real estate law is complex and slow.

So while this is foundational, it is not a complete transformation on its own.

🚀 7. Long-term trajectory

This move fits into a broader pattern:

Digitize real-world data

Make it verifiable and accessible

Build financial products on top

Gradually integrate legal frameworks

If successful, this could lead to:

faster property transactions

global access to real estate investments

more liquid real estate markets

📌 Bottom line

This partnership is not about putting houses on-chain today. It’s about building the data infrastructure required to eventually do so.

The real ramifications are:

👉 transforming real estate from a slow, fragmented system

👉 into a data-driven, programmable, and potentially global financial market

And like most infrastructure plays, its true impact won’t be immediate — but if it works, it could underpin an entirely new layer of real-world asset finance.

@txEcosystem

#SolomenteLabs

7

34

97

10,088

Apr 16

RT @txEcosystem: What will it take for blockchain to power real markets?

tx co-founder and CLO @jaebersole1 recently joined @AshBennington…

50