The leader in AI Risk Infrastructure for fraud & AML. Detection, investigation, & decisioning in one intelligent solution.

Joined May 2019

- Tweets 911

- Following 105

- Followers 565

- Likes 438

262 Photos and videos

Pinned Tweet

Mar 10

A New Era. A New Unit21 🚀

The math of risk and compliance is broken.

Transaction volumes have exploded. Alert queues are overwhelmed. And traditional systems mostly create noise. “More of the same” is no longer a strategy.

A new era of financial crime requires a new architecture to defend against it.

Today, we’re introducing a new Unit21: AI Risk Infrastructure

The Shift

Passive monitoring tools are no longer enough. Most systems simply record the work—they don’t actually execute investigations end to end. They don’t automatically tune your system for better fincrime detection. Until now.

The AI Evolution

AI isn’t just another feature. It’s a new operating model.

We’ve built AI Risk Infrastructure that acts as a force multiplier for financial crime teams.

AI Agents that:

𝗣𝗲𝗿𝗳𝗼𝗿𝗺 𝘁𝗵𝗲 𝘄𝗼𝗿𝗸 — eliminating manual data hunting

𝗦𝗵𝗼𝘄 𝘁𝗵𝗲 𝘄𝗼𝗿𝗸 — providing instant, transparent context

𝗘𝗺𝗽𝗼𝘄𝗲𝗿 𝘁𝗲𝗮𝗺𝘀 — delivering finished investigations, not just alerts

The future of fraud prevention and AML isn’t about how many alerts you generate. It’s about how much risk you resolve—with precision and automation.

A new era is here.

Read more from our COO, Tyler Allen: hubs.li/Q04685H_0

1

3

316

Jun 12

Summer kickoff at Unit21 HQ ⚽

We wrapped up the week with a summer luncheon, World Cup watch party, and churros to cheer Mexico on. 🇲🇽

Good food, good game, great team.

Behind the celebrations is a team fighting financial crime for institutions across 90 countries. Turns out they also take FIFA very seriously.

USA plays later today - let's go! 🇺🇸

We're hiring across the team. Come join us:

linkedin.com/company/unit21/…

#TeamCulture #WorldCup #Hiring

43

Jun 11

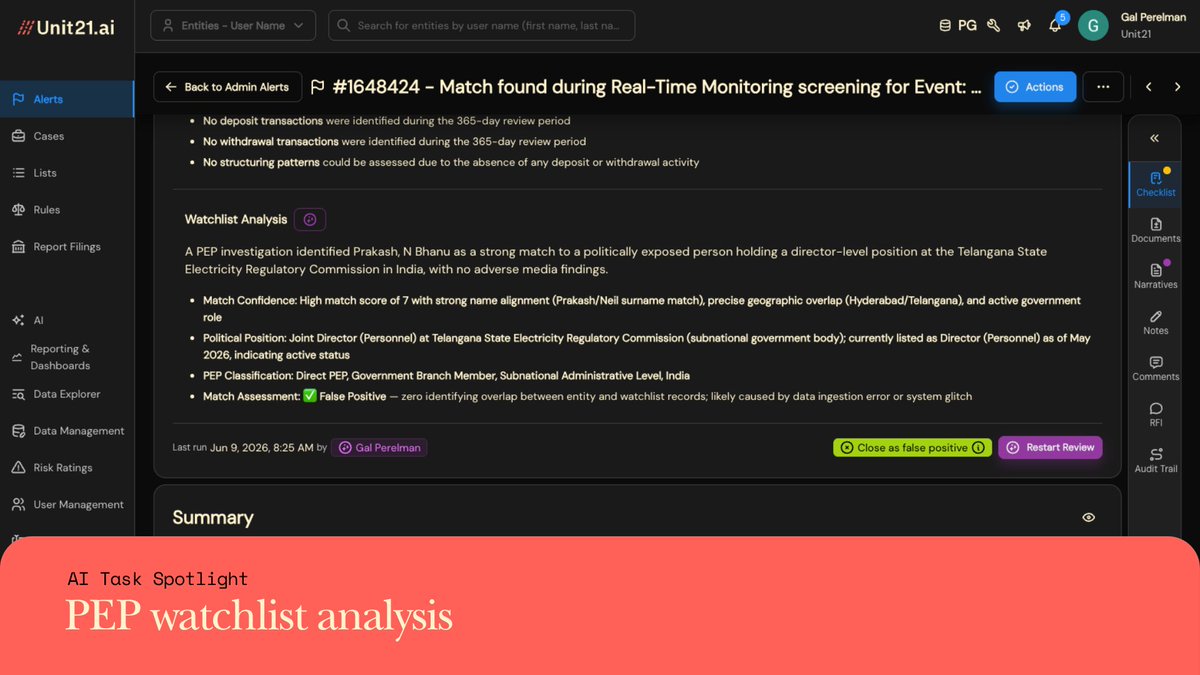

PEP investigations are high-stakes by default. The obligation isn't just to flag the individual, it's to understand who they are, what they do, and who they're connected to.

That baseline research happens on every alert, every time. Manual by default. Time-intensive under any caseload.

Meet our AI Task for PEP Watchlist Analysis: an agent that verifies the match, researches the individual's political position and adverse media, checks family associations and related parties, and surfaces a recommendation with source links directly on the alert.

The work gets done. Your investigators make the call.

Read how it works → hubs.li/Q04l52f_0

27

Jun 10

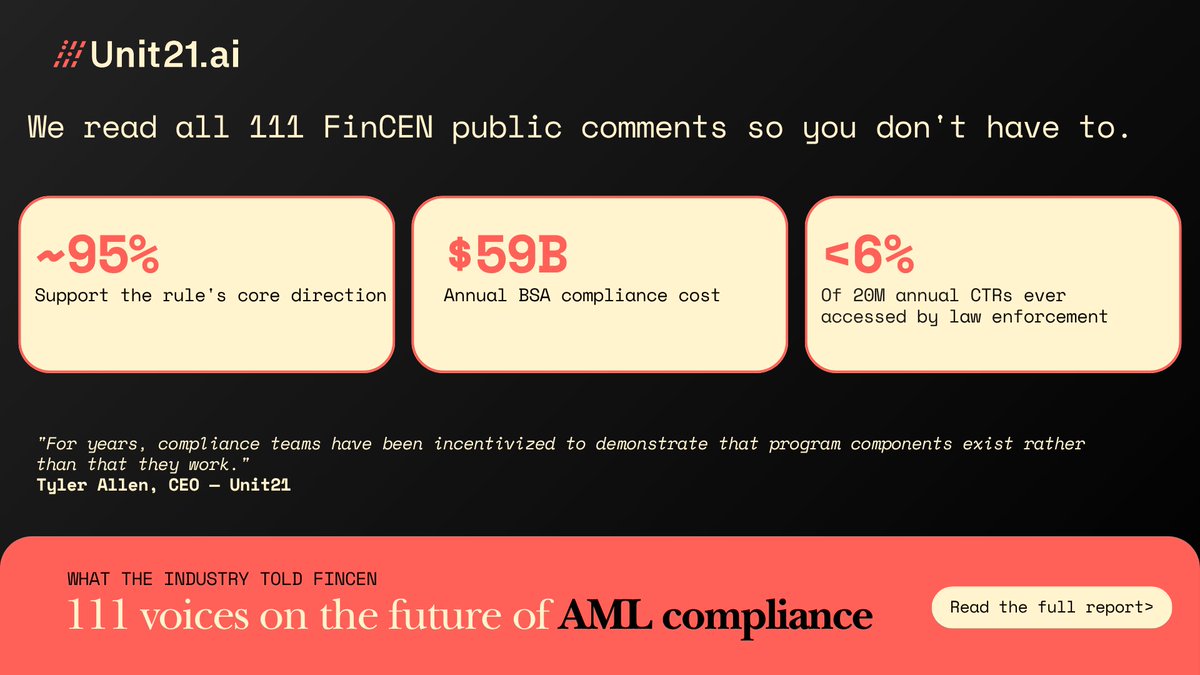

FinCEN's comment period just closed.

We submitted a comment. Then read all 110 others.

111 organizations weighed in on the biggest AML overhaul since 2020 - major banks, fintechs, crypto firms, and trade associations.

Some of what they said was expected. A lot wasn't.

Full breakdown → hubs.li/Q04kYGVt0

4

37

Jun 9

Fraud is evolving faster than most teams can respond.

The attackers have industrialized and most compliance teams are still fighting back with tools built for a different era. Rules that take weeks to update, tickets for every change, and detection logic that assumes fraud never evolves.

Chartis evaluated 40 fraud vendors in 2026.

Unit21 came out as a 𝗖𝗮𝘁𝗲𝗴𝗼𝗿𝘆 𝗟𝗲𝗮𝗱𝗲𝗿 𝘄𝗶𝘁𝗵 𝘁𝗵𝗲 𝗵𝗶𝗴𝗵𝗲𝘀𝘁 𝗔𝗜 𝘀𝗰𝗼𝗿𝗲 𝗮𝗰𝗿𝗼𝘀𝘀 𝗮𝗹𝗹 𝘃𝗲𝗻𝗱𝗼𝗿𝘀 𝗲𝘃𝗮𝗹𝘂𝗮𝘁𝗲𝗱.

Not because AI is a feature we bolted on. Because it is the infrastructure.

See what that actually looks like in practice: hubs.li/Q04jBZNB0

1

16

Jun 8

"Constrained tradeoffs without a safe harbor."

That's how Eric Ellis, former OCC BSA Policy Director, describes the reality of FinCEN's effectiveness mandate for compliance teams.

If you're trying to figure out what this NPRM actually changes for your program, this webinar with @AmerBanker is worth your time.

Full conversation → hubs.li/Q04jZcQ10

1

23

Jun 5

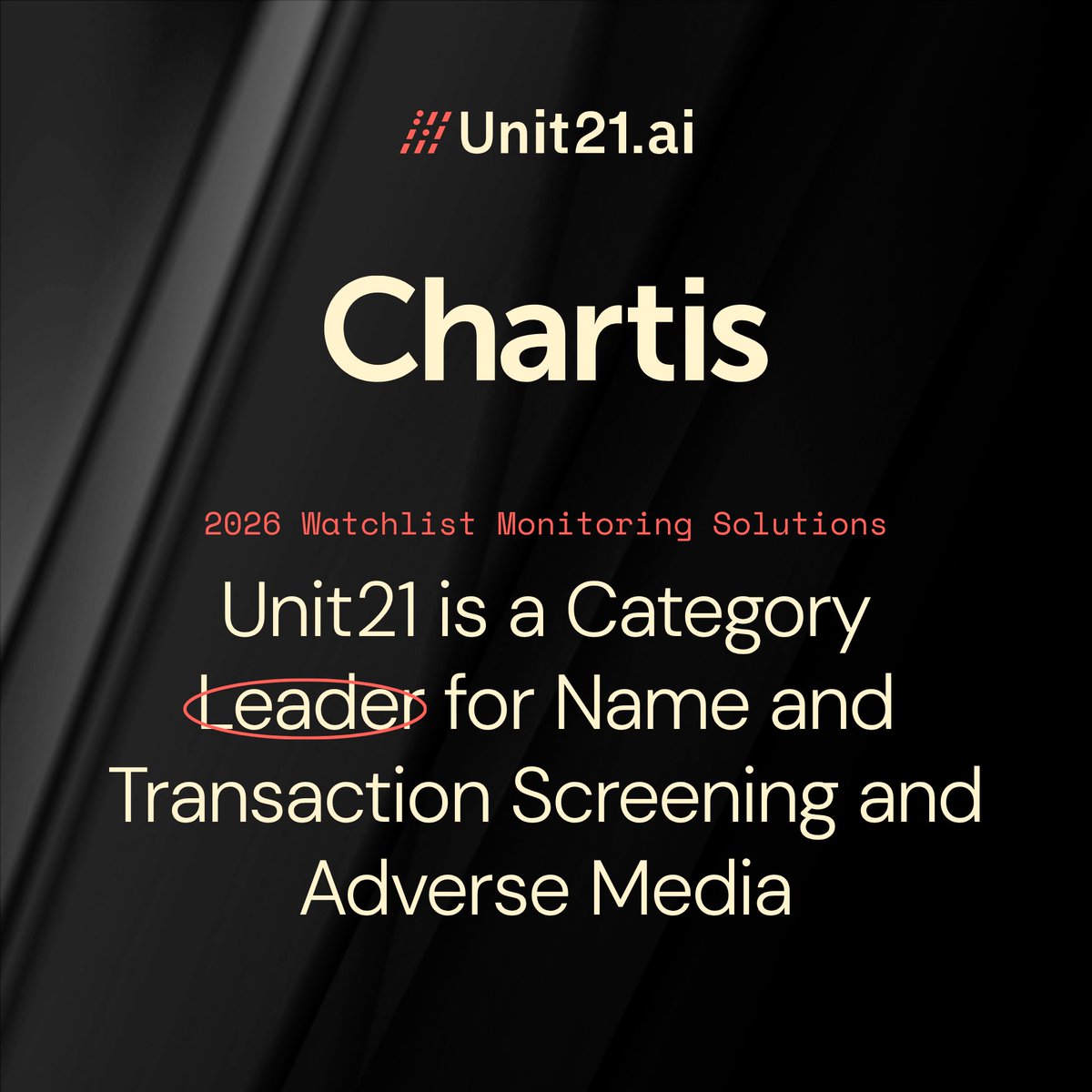

Unit21 has been named a Category Leader in the Chartis 2026 Watchlist and Adverse Media Monitoring Quadrant.

The recognition reflects a simple but persistent problem: most watchlist screening programs have gaps, not from missing tools, but from having too many.

Here's what a fragmented program looks like:

- One vendor for ongoing monitoring, another for onboarding

- Manual processes for ad hoc checks

- No coverage at the payment level

- Three systems to piece together for a single audit trail

A complete program covers all five moments in the customer lifecycle where screening needs to happen: onboarding, ongoing monitoring, ad hoc checks, payment screening, and sanctions AI Agent, in one interface, with one audit trail.

What that looks like in practice → hubs.li/Q04kjsMQ0

1

18

Unit21 retweeted

Jun 3

Essentials: AI is already cheaper than your compliance team

Everyone talks about AI replacing analysts.

The more interesting question is whether AI is actually cheaper.

In my conversation with Tyler, CEO of @unit21inc , he shared a comparison that caught my attention. A fraud or compliance review handled by a human analyst can cost $30–40 per hour internally and significantly more when outsourced. AI agents, when deployed correctly, can perform the same work at a fraction of the cost.

But the bigger insight was not about cost reduction.

Many companies still think of AI as a tool they can deploy once and forget. That is not how this technology works. Fraud evolves. Criminal behavior changes. Models improve every few months. AI systems need continuous tuning, monitoring, and adaptation.

Tyler made another point that resonated with me.

The companies getting the most value from AI are not treating it as a top-down initiative where management builds workflows and employees simply follow them. They are giving employees the ability to understand, adjust, and improve AI systems themselves. The people closest to the problem are often the ones best positioned to optimize the solution.

The conversation left me with a simple conclusion:

The debate is no longer AI versus humans.

The debate is whether organizations can learn and adapt fast enough to work alongside AI.

That may become a bigger competitive advantage than the technology itself.

1

2

2

103

Jun 2

Transaction monitoring. Market abuse rules. STR filings. Regulator expectations that keep evolving.

MiCA authorized is not the same as MiCA ready.

On June 10, we're bringing together two practitioners who are living this right now for a candid panel discussion on what it actually takes to operationalize MiCA compliance at scale.

Joining the conversation:

↳ Eoin Kearns, Head of Compliance & AML, @moonpay — led MiCA compliance from inception, launched across the EEA, and has spent the last year working directly with the AFM to uphold their commitments

↳ Calley Jansen, Head of Financial Crime Intelligence, @BVNKFinance — on the operational front lines of MiCA: transaction monitoring, market abuse rules, alert efficacy, and governance

Moderated by Emily Garza, Chief Customer Officer, Unit21.

No legal explainers. Just practitioners who've built it, talking honestly about what works.

📅 June 10 | Register → hubs.li/Q04jsdN90

67

Jun 1

Appreciate the feature, @yespress_io. Quietly doing the work. 🤝

May 30

Unit21 quietly files roughly 5% of every SAR in America. Most banks have never heard of them.

Our cover story on @unit21inc

yespress.io/unit21?utm_sourc… via Yespress

24

Unit21 retweeted

May 30

The hardest part about AI agents making payments is not the transaction itself. It’s proving intent, identity, and liability at the same time when there is no human directly pressing the button anymore.

What Tyler said during our conversation stuck with me because the industry is entering a world where fraud detection is no longer just about checking passwords, OTPs, or suspicious IP addresses. AI agents will operate from devices, behave like humans, and in many cases even imitate normal customer patterns better than fraudsters ever could.

That changes the entire risk model.

An AI agent making a payment for me might actually look legitimate because it knows my normal behavior, transaction sizes, merchants, and habits. So the decision engine starts relying less on one signal and more on layered intelligence across device behavior, transaction history, behavioral patterns, and agent detection.

The interesting part is that “this is an AI agent” does not automatically mean “this is fraud.”

It simply becomes another signal in the flow.

@unit21inc

1

2

3

98

Jun 1

Unit21 was just named a Category Leader by @ChartisRsch and ranked #1 in AI across 40 fraud vendors.

We earned best-in-class scores in workflow, modeling, case management, and configurability.

If you're evaluating fraud platforms in 2026, this report is worth reading. It maps the market and explains what separates the leaders from the rest.

Download full report👇hubs.li/Q04jBZNB0

20

May 29

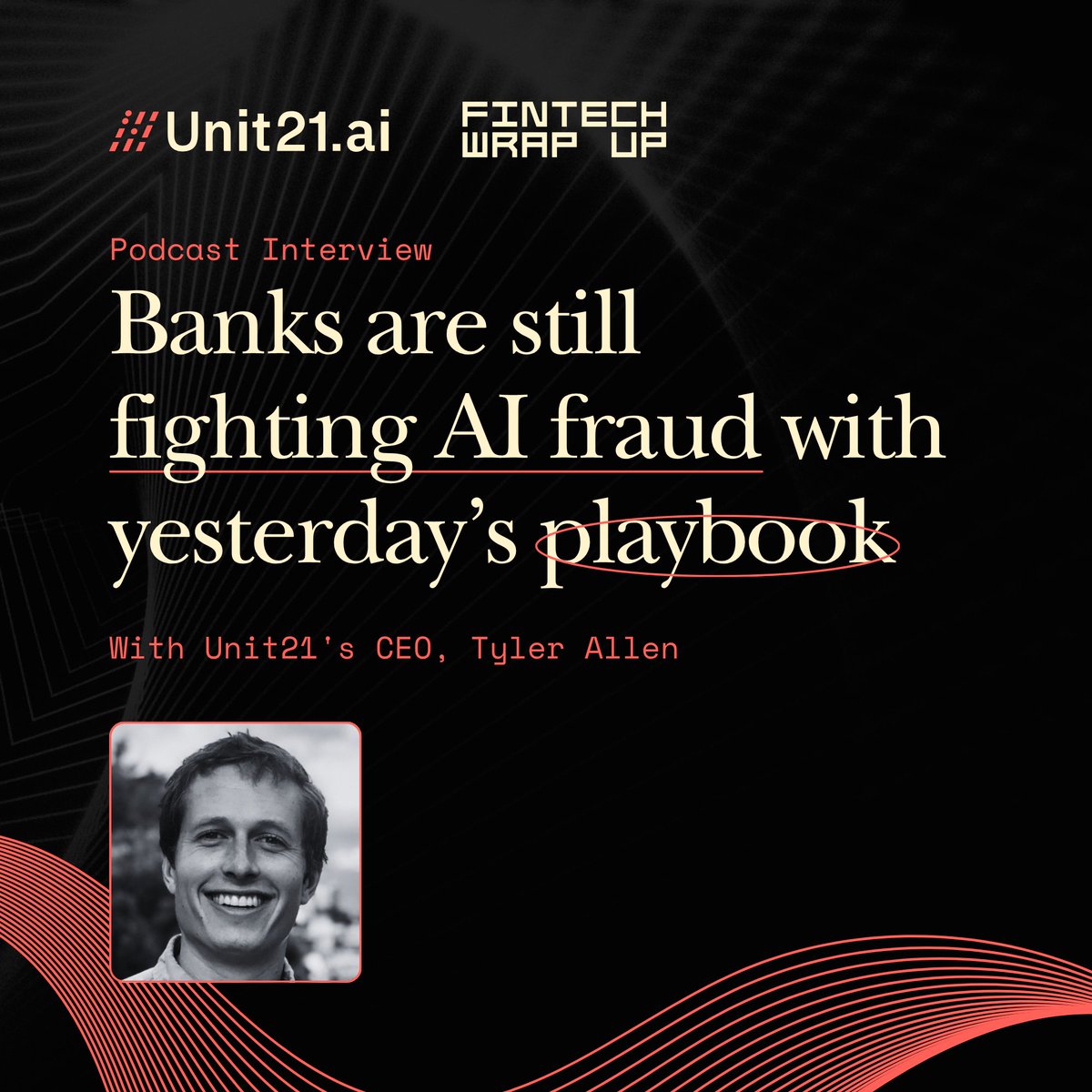

Banks are still fighting AI fraud with yesterday's playbook.

Our CEO Tyler Allen sat down with @samboboev from Fintech Wrap Up Podcast to talk about why that's a problem - and what it actually takes to fix it.

In this podcast, he covers:

↳ Why rules-based systems and ML models aren't enough anymore

↳ How AI agents are changing fraud and AML operations

↳ The future of Know Your Agent and regulatory readiness

↳ Why compliance teams may go AI-native faster than expected

Worth a listen 🎧 → youtube.com/watch?v=N1v3YiLZ…

1

2

3

96

Unit21 retweeted

May 28

Fraud teams used to spend months building detection logic, tuning rules, and manually reviewing edge cases, but Tyler explained how fast that workflow is changing when AI can now generate and deploy fraud rules from a simple text prompt instead of requiring analysts to understand data models, SQL queries, or complex dashboards.

What stood out to me is that the future of fraud infrastructure may not even look like software people actively use every day. The system quietly runs in the background, monitors behavior, deploys detection logic, flags anomalies, learns from feedback, and only pulls humans in when something truly unusual happens.

That changes the role of fraud teams completely.

Instead of spending hours configuring systems, teams start focusing on oversight, exceptions, and strategy while AI handles repetitive operational work at scale. A company processing millions of transactions per day cannot realistically rely on manual reviews and static rules anymore when fraud patterns shift weekly and attackers already use AI themselves.

The interesting part is that fraud software is slowly becoming less of a dashboard and more of an invisible operating layer for compliance, risk, and decision-making.

@unit21inc

1

1

4

97

Unit21 retweeted

May 27

Tyler made an interesting point on the podcast when we discussed AI in fraud protection.

Last year, many financial institutions were still treating AI agents as experiments inside innovation labs. Now more than 50% of financial services companies are already deploying them or actively trying to move into production environments as quickly as possible.

What changed is simple. Fraudsters are already using AI at scale. They can launch thousands of synthetic identity attempts, phishing campaigns, or account takeover attacks in minutes, while traditional fraud teams still rely on workflows built for a slower internet.

The pressure is no longer about whether companies should adopt AI for fraud prevention. The pressure is whether they can adapt fast enough before attackers widen the gap even further.

What also stood out from Tyler’s point was how quickly the market sentiment changed in just 12 months. Moving from roughly 10–20% adoption to the majority of organizations exploring deployment shows how fast financial infrastructure decisions are now shifting once operational risk becomes impossible to ignore.

@unit21inc

1

3

2

84

May 28

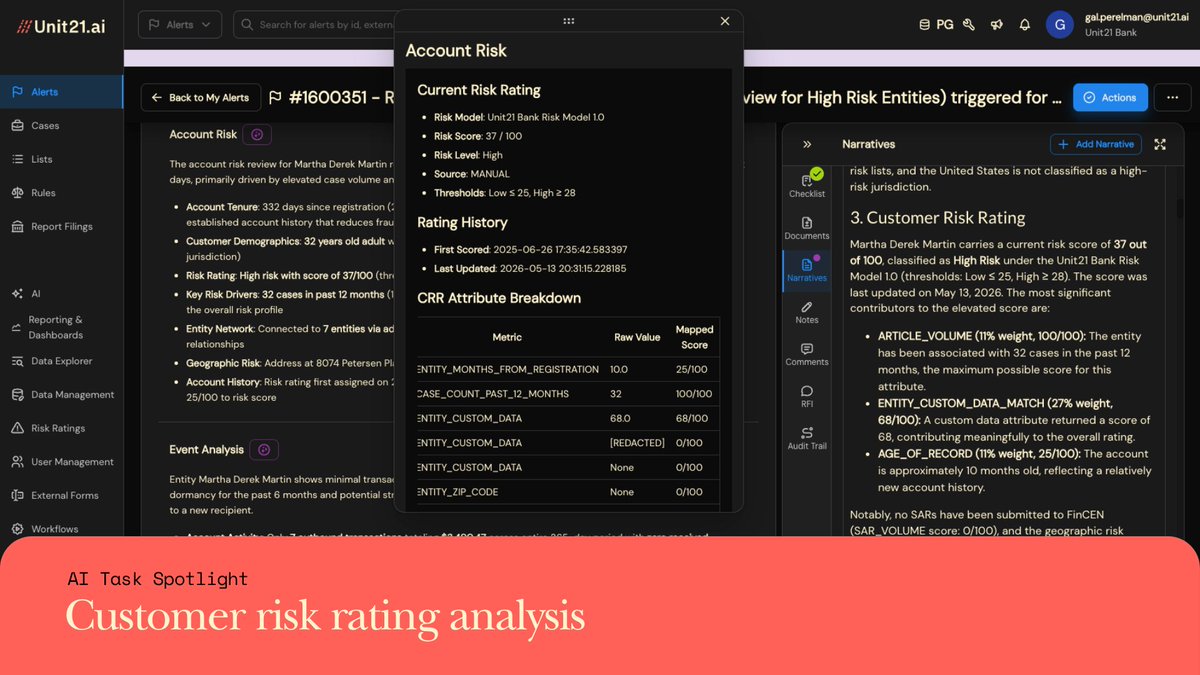

𝗬𝗼𝘂𝗿 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲 𝗽𝗿𝗼𝗴𝗿𝗮𝗺 𝗯𝘂𝗶𝗹𝘁 𝗮 𝗖𝗥𝗥 𝗺𝗼𝗱𝗲𝗹.

Weighted attributes. Configured thresholds. A score for every customer. And when an investigator opens an alert, they see: High. 82/100. That's it.

They don't see that SAR_VOLUME is carrying 20% of the model weight and scored 100/100 because this customer filed two SARs in the last 12 months.

They don't see that AGE_OF_RECORD scored 0/100 because a 66-month-old account is considered low-risk by your model's configuration.

They see a number. They don't see the reasoning behind it.

So they can't document it. They can't challenge it. And when an examiner asks why a case was escalated, "the CRR was high" isn't a sufficient answer.

𝘛𝘩𝘪𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘱𝘳𝘰𝘣𝘭𝘦𝘮 𝘰𝘶𝘳 𝘊𝘶𝘴𝘵𝘰𝘮𝘦𝘳 𝘙𝘪𝘴𝘬 𝘙𝘢𝘵𝘪𝘯𝘨 𝘈𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘵𝘢𝘴𝘬 𝘴𝘰𝘭𝘷𝘦𝘴.

The moment an investigator opens a flagged alert or case, the task automatically surfaces the full attribute-level breakdown: each factor's weight in the model, its individual score, the underlying metric, the raw entity value, and the mapped score. The complete logic chain, already there, before the investigation begins.

𝗔 𝘀𝗰𝗼𝗿𝗲 𝘁𝗲𝗹𝗹𝘀 𝘆𝗼𝘂 𝘄𝗵𝗮𝘁. 𝗧𝗵𝗲 𝗯𝗿𝗲𝗮𝗸𝗱𝗼𝘄𝗻 𝘁𝗲𝗹𝗹𝘀 𝘆𝗼𝘂 𝘄𝗵𝘆.

Edition 03 of AI Task Spotlight is live. Read how it works: hubs.li/Q04jfkbQ0

#AML #Compliance #CustomerRisk #TransactionMonitoring

1

26

May 27

New email. Same questions. Wait. Chase. Screenshot the thread. Upload it manually. Log it in a spreadsheet.

Every compliance analyst knows the drill.

That's not an audit trail. That's just hoping nothing goes wrong before the exam.

We built Request for Information (RFI) to fix it.

From any alert or case in Unit21, your team sends a secure, white-labeled form, sets a deadline, and receives everything back in the platform automatically. Full audit trail. No chasing. No manual uploads.

RFI is live. Read more: hubs.li/Q04h-zLF0

44

Unit21 retweeted

May 26

Tyler made an important point during our conversation that fraud teams are now operating in a completely different environment because AI gives attackers an unfair advantage in scale, speed, and experimentation.

A fraudster only needs one successful hit out of 100 attempts to make money. A bank or fintech cannot afford that same error rate because one hallucinated decline can block a legitimate customer from accessing financial services, trigger compliance issues, or destroy trust instantly.

That is what makes this shift so difficult for financial institutions.

The same AI acceleration helping fraudsters is also giving risk and compliance teams entirely new capabilities. Real-time behavioral analysis, adaptive onboarding checks, AI-driven monitoring, and autonomous investigation systems are moving from experiments into production infrastructure much faster than most people realize.

The question is no longer whether AI can support fraud and compliance operations.

The real challenge is how quickly regulators and financial institutions become comfortable allowing AI systems to participate directly in critical risk decisions while still maintaining accountability, explainability, and accuracy at scale.

@unit21inc

3

3

95

May 26

⏰This Thursday, nearly 800 compliance leaders are tuning into this conversation…

FinCEN's NPRM is reshaping what AML program effectiveness actually means - and the comment period closes June 9.

Before it does, join us and American Banker for a live, unfiltered conversation on what compliance leaders need to know.

Joining the conversation:

↳ Sarah Beth Felix, Palmera Consulting - recovering auditor, founder, and AML consultant who's seen this from every angle

↳ Eric Ellis, @FifthThird Bank - former OCC BSA Policy Director who's sat on both sides of the exam table

Spots are still open.

📅 May 28 | 1:00 PM ET

Register → hubs.li/Q04fH1vS0

35

Unit21 retweeted

May 25

One thing that keeps coming back in conversations around AI agents and payments is that the industry is still thinking mostly about capability, while the harder problem is governance.

An AI agent being able to execute a payment is not the difficult part anymore. The infrastructure already exists. APIs exist. Stablecoins exist. Real-time payment rails exist.

The real challenge starts when an agent makes a mistake, exceeds permissions, gets compromised, or negotiates on behalf of a customer and moves money autonomously. At that point, the question becomes very simple: who is responsible for that action?

That is why Tyler’s point about an “AI agent registry” is so interesting.

Not because registries are exciting technology, but because financial systems have always depended on trusted identity and accountability layers sitting underneath transactions. Merchants have IDs. Banks have licenses. Payment providers have scheme memberships.

AI agents currently have almost none of that structure.

I would not be surprised if companies like Visa, Mastercard, or Stripe eventually become part of this layer because they already sit in the middle of trust, compliance, permissions, authentication, and dispute management across global commerce.

@unit21inc

1

3

3

117

May 22

"Unit21 gives us the flexibility and control to move fast. We can tailor rules, test safely, and scale compliance as quickly as Rippling grows."

Their old compliance stack wasn't built for scale but with Unit21, they got real-time transaction blocking before funds settle, dynamic customer risk scoring, and a single workflow from alert to SAR filing.

Read the full case study → unit21.ai/customers/rippling

1

36