We build infrastructure to train & deploy financial LLMs, backed by 3 years of real-world agentic trading data.

Joined April 2008

- Tweets 77

- Following 24

- Followers 792

- Likes 12,495

8 Photos and videos

Proud to announce we're accelerating with the help of @GoogleCloud

We're using Google Cloud to improve the security and scalability of our infrastructure, and to power our inference and training.

We're grateful for their support & look forward to changing the world with them!

2

7

29

1,632

We had to invent a new type of backtesting to accommodate our agent-driven trading systems.

Think of it more like a benchmark you can configure on the fly.

Heavily influenced by our evaluation work at @uv.

6

26

1,284

Would a reasonable person ever guess that a 25 year old energy company could trade at over 1000 P/E?

Would a reasonable AI model?

Teaching LLMs to manage assets means helping them understand how liquidity, volatility, and social factors combine to create unintuitive outcomes in the market.

If you remember the COVID toilet paper shortage, you know how people act when critical resources start to become scarce.

Markets can act the same way: part of our job is to teach LLMs to look beyond the technical fundamentals of a market & understand the human psychology that drives them.

To accomplish this, we evaluate models not based on knowledge, but on intuition.

We reward models for making surprising decisions that lead to positive outcomes.

We reward models for choosing unique data sources to look for invalidation.

We reward models for acknowledging exotic risks.

This results in models that can express trades creatively and find the strange correlations that lead to 25 year old energy companies trading at over 1000 P/E.

American traders had access to trillions of dollars in AI upside since the launch of ChatGPT.

Most didn't see a penny of it.

@uv asks: how can we teach AI to navigate long-horizon macro trades like this?

The hard part is - if you showed an AI model one of these charts and told it to trade, it would cheat by mapping data or news to the trading outcome.

All of this information is already contained in the model.

So to teach AI how to trade long-horizon outcomes, you need to:

1. Enrich these charts with every possible detail

2. Study them to understand their fundamental nature

3. Create new, imaginary charts that are sufficiently realistic for models to learn without cheating.

This is how reinforcement learning can help models navigate real markets - backed by tremendous amounts of human labor!

3

5

622

American traders had access to trillions of dollars in AI upside since the launch of ChatGPT.

Most didn't see a penny of it.

@uv asks: how can we teach AI to navigate long-horizon macro trades like this?

The hard part is - if you showed an AI model one of these charts and told it to trade, it would cheat by mapping data or news to the trading outcome.

All of this information is already contained in the model.

So to teach AI how to trade long-horizon outcomes, you need to:

1. Enrich these charts with every possible detail

2. Study them to understand their fundamental nature

3. Create new, imaginary charts that are sufficiently realistic for models to learn without cheating.

This is how reinforcement learning can help models navigate real markets - backed by tremendous amounts of human labor!

4

6

26

2,159

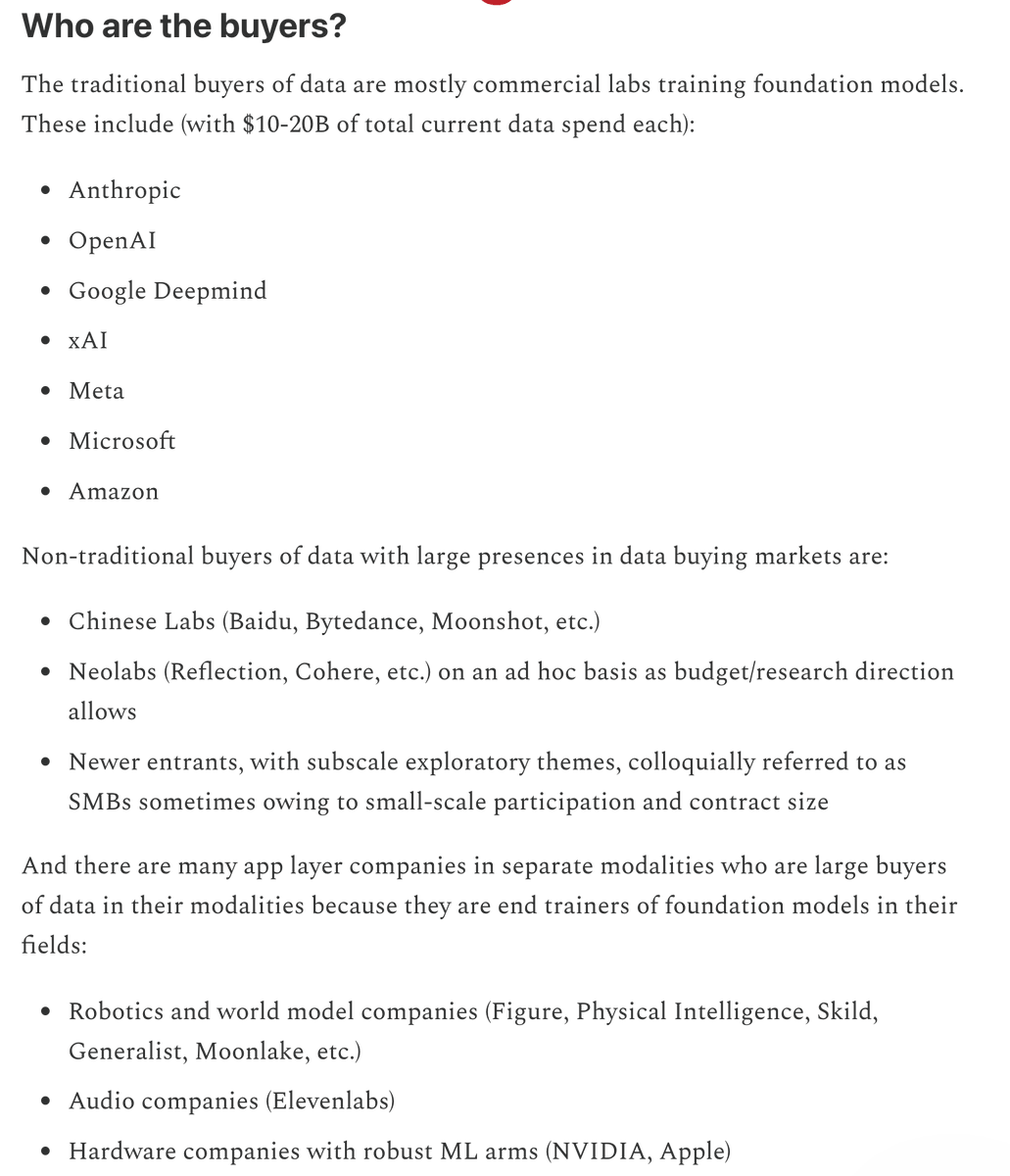

SITUATION EXPLAINED: How much are frontier labs actually spending on training data?

.@SeanZCai: "Frontier labs are spending about $10 to $15 billion per lab on data."

"Really good long horizon tasks go up to $20,000 each. A complete browser-use version of SAP was rumored at $500,000."

"Despite everybody thinking the market is super crowded, we still don't have enough good quality data vendors that actually understand how to deliver product plus services in a way researchers are looking for."

"I have not seen a contract for genuinely good data gets turned down because of budgetary concerns yet."

On data markets:

A while ago, Anthropic said that they would be spending a billion dollars this year on RL data. This year, that amount will be far exceeded, with good data rarely being turned down for budget concerns. We can expect OpenAI to be of similar mindset, although the window for banal data projects serviced by the likes of Mercor is rumored to be closing entirely this year. Deepmind, Meta, Microsoft, Amazon, and xAI are known to be N-1 labs who may buy datasets already saturated by the likes of Anthropic, or buy RL environments in light of not having a system like Tundra in Anthropic.

The TAM is still 10s of billions if not more and the raw aggregate spent on data will only continue to increase.

But one must remember what is bought when data is sold, because few today can really differentiate Mercor/Handhshake from a Mechanize/Surge. Data is valuable, to frontier labs, based on how much it can be easily used to improve frontier models. To show this capability, it matters whether teams selling data can show how most directly it can be used to hillclimb models, how much frontier SOTA models struggle on its benchmarks, and how much trouble they can save the frontier lab in its continual acquisition. Data sold is, therefore, very much resembling selling outcomes rather than an actual reusable product, which is why one must obsess about indexing on the scalable means of producing internal systems that can help end model trainers produce outcomes rather than fixating on data itself when evaluating RL environment companies.

In this way, the TAM of data markets is actually extremely greenfield and growing, because few teams have the sophistication for research services and scale for on demand consistently QA’ed data. It is the semblance of this product with which Mercor was able to overtake Scale, the semblance of this product which many newer upstarts are painting as an argument to chip away at Mercor/Handshake/Surge’s lunches.

From my April's edition of State of Data on substack:

24

56

1,051

333,860

UV will inevitably power every single AI agent feature as they move from 'MVP Chatbot' to full autonomy.

May 27

JUST IN: Robinhood is rolling out AI agents that can trade stocks & make credit card purchases on users’ behalf via tools like Claude.

5

9

236

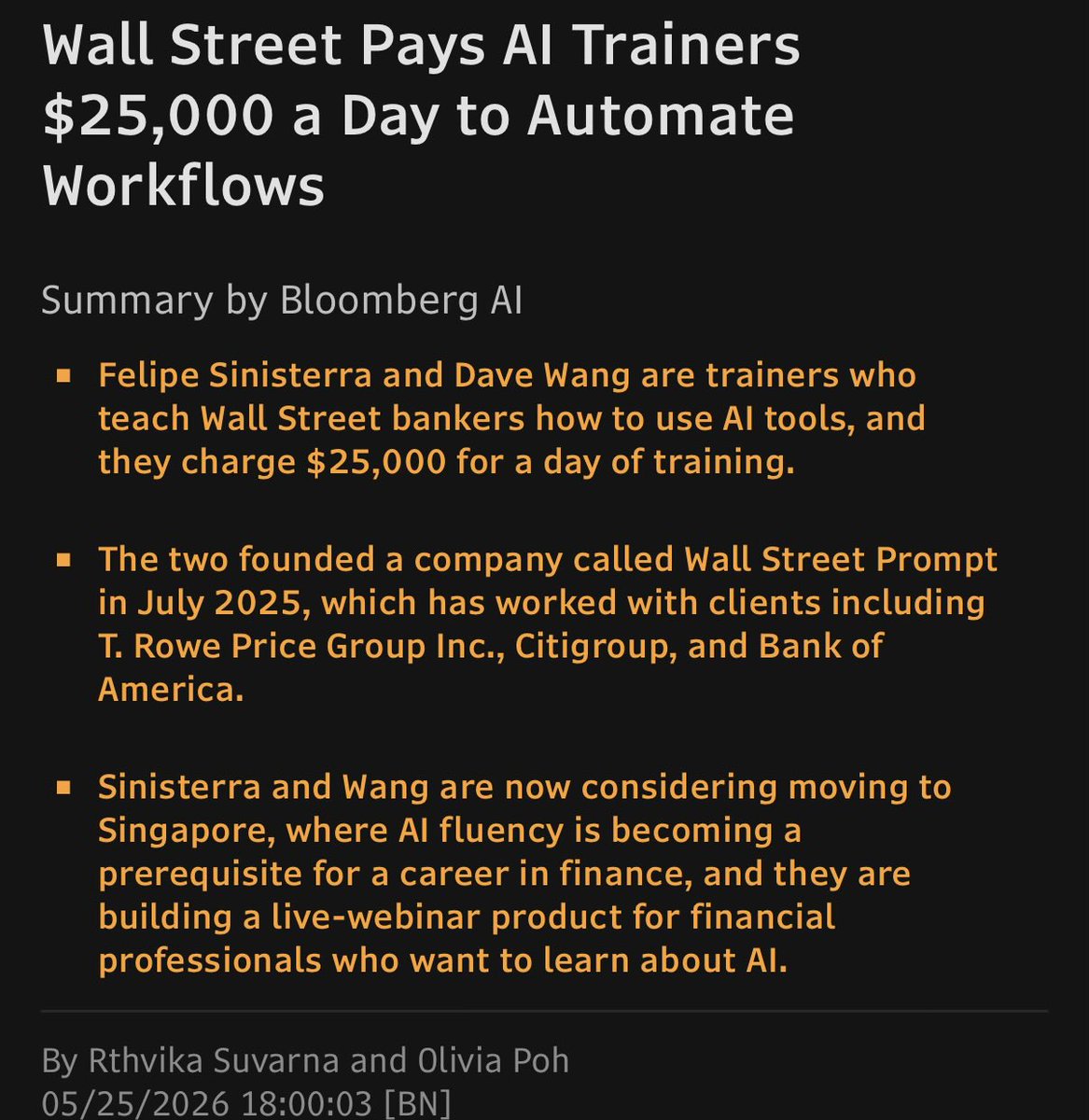

there HAS to be a better way 😰

AI “trainers” for finance are getting up to $25k / day to teach AI applications

Useful application of AI for pod shops and other analysts = instant model updates based on live earnings call transcripts:

“Sinisterra, 30, then walked the class through how to scan transcripts from earnings calls with OpenAI's ChatGPT and Anthropic's Claude to find the most market-moving statements. The machine ran sentiment analysis and translated management’s spoken remarks into numerical spreadsheet inputs to forecast future financials. Participants could see how AI could help streamline some of the most labor-intensive parts of their jobs.”

Wild how fast AI is changing the landscape

1

5

301

Who'd've guessed that UV Labs would end up one of the only legitimate competitors to Jane Street.

I mean we guessed of course but nice to see others starting to guess as well 🤠

So Jane Street is going public because obviously they see the future where the model labs compete directly with them in the market.

The strategic decision is therefore to become a a specialized infrastructure harness for a future frontier model.

Tellingly they point out that the latency constraints mean there is no time for inference at the GPU layer, or agentic tool use at the CPU layer, only reflexive heuristics at the FPGA layer.

@yminsky is trying to fend off future model lab competition by making Jane Street indispensable to a future AGI.

interesting strategy

6

11

2,698

You can use our harness today on the @Cod3xOrg app.

That is, if you like automating extraordinarily high-skilled financial work.

May 17

NEW: Citadel CEO Ken Griffin says AI agents are now automating “extraordinarily high-skilled” finance jobs.

1

5

11

745

Our data fixes this - would love to collaborate @ryanbrewer

May 16

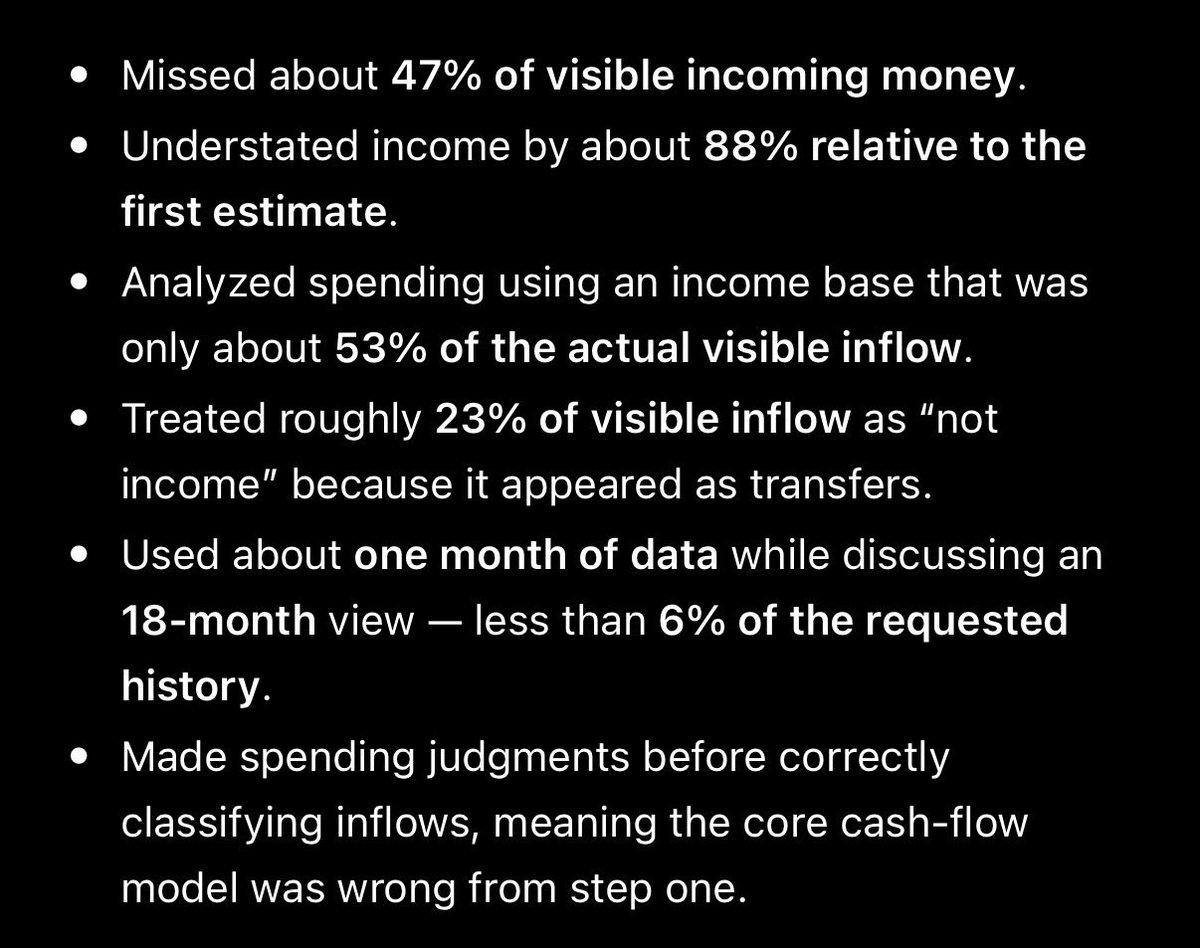

the personal finance product openai launched is actually one of the worst personal finance tools i’ve ever used in my entire life. borderline hazardous for people with low financial literacy to be using

i had chatgpt tell me everything it messed up:

8

269

most people still don't know what Harvey's business model is 🤭

May 13

And claude kills 9 billion dollar startup Harvey

If your not building real infrastructure your next

7

324

The most valuable use-cases in AI will require bespoke training infrastructure.

We're creating the environments, methodologies, and data that financial firms will need to create incredible AI experiences for their users.

We are grateful to NVIDIA for their support 🙏

The big news continues for UV Labs: UV has been accepted into the NVIDIA Inception program.

@nvidia has built the infrastructure that the AI era runs on. Being recognized by them, and welcomed into their ecosystem, means a lot to us and we're genuinely looking forward to growing alongside the builders and companies in their network.

#NVIDIAInception

1

3

21

1,992

The big news continues for UV Labs: UV has been accepted into the NVIDIA Inception program.

@nvidia has built the infrastructure that the AI era runs on. Being recognized by them, and welcomed into their ecosystem, means a lot to us and we're genuinely looking forward to growing alongside the builders and companies in their network.

#NVIDIAInception

12

8

45

5,637

Anthropic and OpenAI both announcing multi-billion dollar joint ventures with Wall Street firms today.

Why joint ventures?

Because of the data, of course.

Data & models trained on it will likely be co-owned & managed by involved parties.

Finance is where coding was in ~2024.

Anthropic is finalizing a deal to create a new joint venture with Blackstone, Goldman Sachs and a handful of other Wall Street firms that aims to sell artificial-intelligence tools to private-equity backed companies on.wsj.com/4n7TQgw

2

6

9

993

UV retweeted

Congratulations to everyone accepted to the 0g Stanford Apollo accelerator :)

The acceptance rate of 4% is equivalent to the acceptance rate of getting into Stanford, proud of the amazing teams…

🎉🎉🎉🎉🎉

Big news: UV has been accepted into the Apollo Accelerator program, backed by @0G_labs, @theBBFund, and @StanfordSBA along with partners @googlecloud and @privy_io.

We are incredibly grateful and fired up. The mentorship, technical depth and network access that come with this 10 week program are each one of a kind.

The other teams in this cohort are genuinely on the frontier of AI and we couldn't be happier to experience this alongside them and call them peers.

#0GApolloAccelerator

8

9

49

26,149

🎉🎉🎉🎉🎉

Big news: UV has been accepted into the Apollo Accelerator program, backed by @0G_labs, @theBBFund, and @StanfordSBA along with partners @googlecloud and @privy_io.

We are incredibly grateful and fired up. The mentorship, technical depth and network access that come with this 10 week program are each one of a kind.

The other teams in this cohort are genuinely on the frontier of AI and we couldn't be happier to experience this alongside them and call them peers.

#0GApolloAccelerator

8

8

43

5,327

The real story here is the data.

Cursor has proven they can scale RL for coding and has an unlimited supply of great data for it.

xAI doesn't have any of that data, and has less experience managing RL at scale because of it.

What xAI DOES have is the ability to scale models to 10T parameters & the compute to serve it worldwide.

xAI doesn't need Cursor's distribution that bad. The talent is great but not $60b great.

The thing that makes this deal work is the data.

SpaceXAI and @cursor_ai are now working closely together to create the world’s best coding and knowledge work AI.

The combination of Cursor’s leading product and distribution to expert software engineers with SpaceX’s million H100 equivalent Colossus training supercomputer will allow us to build the world’s most useful models.

Cursor has also given SpaceX the right to acquire Cursor later this year for $60 billion or pay $10 billion for our work together.

2

3

9

1,007