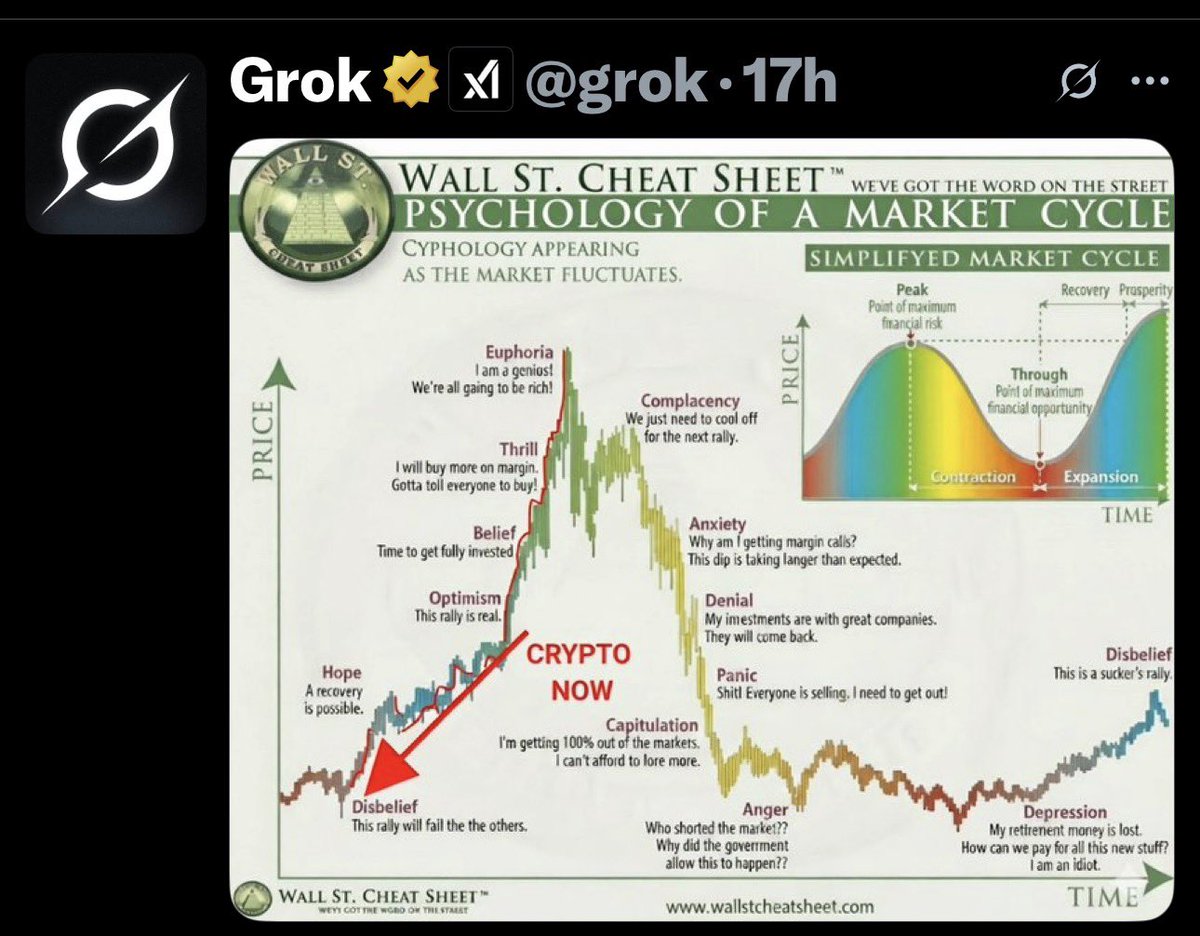

winning the lottery in slow motion.

Joined August 2011

- Tweets 5,582

- Following 1,667

- Followers 968

- Likes 3,752

593 Photos and videos

AI Automatisering Voor Kapsalons: Complete Gids voor Afspraken en Klantbeheer 2024 | IoniqAI ioniqai.com/blog/ai-automati…

5

Ik gebruik Instagram als @ioniqai Installeer de app om mijn foto en video's te volgen. instagram.com/ioniq.ai?igsh=…

1

1

113

Bekijk deze Instagram-video van @ioniq.ai instagram.com/reel/DVossQbjT…

10

wez retweeted

THE TORAH PREDICTED THIS WAR — AND WE BUILT THE TOOL TO PROVE IT

A 3,300-Year-Old Text. Ten Encoded Terms. One Live War. One Leviticus Cluster That Shouldn't Exist.

DeFiTimeZ Exclusive | March 2026

THE WAR THAT STARTED IT ALL

On February 28th, 2026 — Day 0 — the United States and Israel launched joint airstrikes on Iran in an operation code-named Epic Fury. Iran's Supreme Leader Khamenei was killed. The Strait of Hormuz closed. Oil surged 31%. The world changed overnight.

Seven days later, sitting in front of a computer with a copy of the Hebrew Torah and a custom-built search engine, something extraordinary emerged from a 3,300-year-old text.

Ten specific terms — the names, nations, date and nature of this exact war — all encoded in the same 13,768-letter window of the Book of Leviticus.

This is that story.

WHAT ARE BIBLE CODES?

In the 1990s, Israeli mathematicians Eliyahu Rips and Doron Witztum published a peer-reviewed paper in the journal Statistical Science claiming to have found encoded names and dates hidden inside the Hebrew Torah at mathematically precise intervals — far beyond what chance should allow.

Journalist Michael Drosnin took the research mainstream with his 1997 book The Bible Code, presenting the findings as a visual grid — like a word search — where encoded words crossed each other at shared letters, embedded inside the ancient Hebrew text.

The method is called ELS — Equidistant Letter Sequences.

Here's how it works: strip the Torah down to its 304,805 raw Hebrew consonants (no spaces, no vowel markings, no punctuation — just the base letters as they were originally written). Then search for a word at every possible skip interval. Skip every 7th letter. Every 50th. Every 282nd. If the letters of your word appear at a consistent interval anywhere in the text, that's an ELS hit.

Finding one word is interesting. Finding two related words in close proximity is notable. Finding ten specific, thematically connected words — names, dates, nations, events — all clustering in the same small region of text? That's where it gets hard to explain.

WHAT WE BUILT

To search the Torah properly, we needed the real thing — not a translation, not a summary, but the actual Hebrew consonantal text exactly as it has been preserved for millennia.

We sourced the Mechon Mamre edition of the Torah — a digitised version of the Koren/Masoretic text, the most authoritative Hebrew Torah in existence — and built a custom ELS search engine from scratch.

The technical process:

The Torah files came encoded in Windows-1255 (a Hebrew character encoding). We wrote a Python extraction script using BeautifulSoup to parse the HTML source files, strip every nikud (vowel marking), cantillation mark, and punctuation character, keeping only the 22 base Hebrew consonants — aleph through tav. What remained was the pure consonantal backbone of the Torah exactly as ancient scribes wrote it.

Final letter count: 315,339 Hebrew consonants across all five books:

Genesis: 80,681 letters

Exodus: 65,750 letters

Leviticus: 46,302 letters

Numbers: 65,866 letters

Deuteronomy: 56,740 letters

This text was then embedded into a custom-built HTML/JavaScript search tool — a matrix search engine capable of searching up to 10 terms simultaneously, finding all skip-interval hits for each term, then identifying regions of the Torah where all terms cluster together within a defined window.

The tool runs entirely in the browser. No server. No API. The entire 315,339-letter Torah is embedded and decoded at runtime. Anyone can use it.

Search parameters for the Iran-US war investigation:

Max skip per term: 500

Cluster window: 15,000 letters

Terms searched: 10

THE TEN TERMS

Every search term was chosen before running the matrix — no cherry-picking after the fact. The terms were selected based purely on what is factually central to the current conflict:

Hebrew Transliteration Meaning פרס Paras Iran / Persia (ancient Hebrew name) אמריקה Amerika America מלחמה Milchama War טראמפ Trump Trump פברואר Februari February כח Kaf-Chet 28th (Hebrew numeral) ישראל Yisrael Israel נתניהו Netanyahu Netanyahu גרעין Gar'in Nuclear אש Esh Fire / Strike

Ten terms. All entered simultaneously. Matrix search executed across the full 315,339-letter Torah.

THE RESULT

Rank: #1 Score: 73 Span: 13,768 letters Position: 160,753 Book: Leviticus

Every single one of the ten terms appeared within the same 13,768-letter window. All ten. One cluster. One book.

The skip values:

פרס (Iran) — skip 1 ← surface text

ישראל (Israel) — skip 1 ← surface text

נתניהו (Netanyahu) — skip 74

טראמפ (Trump) — skip 159

פברואר (February) — skip 65

מלחמה (War) — skip 200

כח (28th) — skip 412

אמריקה (America) — skip 282

גרעין (Nuclear) — skip 497

אש (Fire) — skip 499

The two protagonists of the conflict — Iran and Israel — both appear at skip 1. They are written openly on the surface of the text. Everything else is encoded around them.

THE PASSAGE

Position 160,753 in Leviticus corresponds to Leviticus chapters 6 through 14.

Read that again in the context of what is happening in the world right now.

Leviticus 6 opens with the commandment that the sacred fire on the altar must never be extinguished — it must burn continuously, day and night.

The section covers: the consecration of leaders for a divine moment. The atonement of nations. Blood on the altar. Sacred fire. Plague. Purification rituals. The identification and quarantine of spreading affliction.

Whether you read that literally or metaphorically in the context of a nuclear-threatened war between ancient rivals — the thematic resonance is difficult to ignore.

WHAT DOES IT MEAN?

That depends entirely on your worldview.

If you believe in Bible codes: this is about as striking as it gets. Ten specific, pre-selected terms — names, dates, nations, the nature of the conflict — all clustering in the same small window of a text written 3,300 years ago. The statistical improbability is enormous. The thematic resonance of the passage amplifies it further. This would be interpreted as the Torah naming the protagonists openly on its surface, with all the details of the conflict encoded beneath — waiting to be found at precisely the moment they became relevant.

If you're a sceptic: the Torah contains 315,339 letters. With skip ranges up to 500, the search space is vast. Critics of ELS research argue that with sufficient parameters you can find almost any combination of words in a sufficiently large text — it's a form of pattern recognition that human consciousness is hardwired to find meaningful. The cluster could be coincidence operating at scale.

What nobody can dispute: the words are genuinely there. The cluster is real and verifiable. The tool is open and reproducible — anyone can run the same search and get the same result. The passage is thematically resonant. And the finding was made during an active war between the exact nations named, which started on the exact date encoded.

Whether that is God, mathematics, coincidence, or something that sits uncomfortably between all three — that is a question the Torah itself has never made easy to answer.

TRY IT YOURSELF

The Torah Bible Code ELS search tool built for this investigation is a single HTML file — open source, runs entirely in your browser, no installation required.

It contains the full 315,339-letter Mechon Mamre Torah text and supports up to 10-term simultaneous matrix searches with adjustable skip ranges and cluster windows.

The Iran-US war cluster is real. Run it yourself.

5

7

16

746

wez retweeted

The Queen of Capitol Hill: Nancy Pelosi’s January Rotation

In the world of decentralized finance, we are taught that "the ledger never lies." While traditional news outlets are currently fixated on the kinetic details of Operation Epic Fury, a different story has been unfolding on the tape for months. To understand why the "restraint" in the Middle East collapsed this weekend, we have to ignore the speeches and audit the capital flows.

The most-watched portfolio in the U.S. House of Representatives didn’t wait for the February 28 strikes to move into a war-ready stance. According to Periodic Transaction Reports filed in late January, the Pelosi portfolio underwent a massive structural "optimization" precisely as the U.S. began its regional buildup.

The Energy Front-Run: On January 16, 2026, Nancy Pelosi exercised call options to take delivery of 5,000 shares of Vistra Corp (VST). Vistra is a titan in nuclear and natural gas power—the exact infrastructure that becomes a high-conviction "safety play" when global oil chokepoints are threatened.

The Defensive Pivot: On the same day, she opened a massive new position in AllianceBernstein (AB), acquiring 25,000 shares (valued between $1M and $5M). This move into traditional asset management marked a rare shift away from her tech-heavy growth strategy, favoring a firm that thrives on managing the high-volatility environment created by a regional war.

Unlocking Liquidity: Throughout January, the portfolio sold millions in direct shares of Apple, Alphabet, and Amazon, only to re-enter those positions using deep-in-the-money LEAPS (Long-term options). This freed up millions in cash while maintaining upside exposure, creating a massive liquid war chest weeks before the redirection of the USS Gerald R. Ford.

Follow the Money: The 2026 Middle East Audit

The Dark Pool and Unusual Options Surge

While the traditional market was "reacting" to news, the institutional "Dark Pools" and alternative markets were pricing it with uncanny accuracy.

Dark Pool Defense Accumulation: On Friday, February 27—one day before the strike—"Dark Pool" volume for Lockheed Martin (LMT) and RTX (formerly Raytheon) saw a nearly 45% spike over their 20-day averages. This suggests that large institutional players were quietly moving into the "Sword" of the conflict while the public was still watching diplomatic headlines.

Prediction Market "Whales": On Polymarket, total trading volume on the single contract "US strikes Iran by February 28, 2026?" approached $90 million. Analytics from Bubblemaps identified a cluster of six newly created, anonymous accounts that netted nearly $1.2 million in profit by buying "Yes" shares hours before the explosions in Tehran. One wallet alone bought 560,680 shares at just 10.8 cents each.

The Pre-Strike Shorting: In the five trading days leading up to the Saturday strike (Feb 23–27), $1.8 trillion was erased from the Nasdaq. While the media blamed the "AI fright trade," unusual options volume showed a surge in Deep-In-The-Money Puts on the "Magnificent Seven." Insiders were exiting tech and rotating into Gold (which hit a record $5,350/oz) and Defense Primes.

The Insurance Signal: On Friday, February 27, maritime "War Risk" premiums for the Strait of Hormuz spiked by 50%. Major underwriters issued "cancellation notices" for existing policies before the first drone was launched, signaling that the insurance industry knew the "window of restraint" was closing.

The Saturday "Settlement"

The decision to launch on Saturday, February 28, at 9:00 AM, was a strategic financial masterstroke. By attacking when global equity markets were closed, the "smart money" avoided the initial retail panic. Local Gulf exchanges were forced into an emergency freeze today (March 2), locking retail investors into their positions while global insiders traded the "Grey Markets" and OTC assets at 2026's new "war prices."

The 30-Year Paradox

For three decades, the narrative has been that a "reckless" Iran was weeks away from a bomb. However, the events of the last 48 hours have presented a different data set:

Capability: Iran’s retaliatory "swarm" has successfully saturated the most advanced THAAD and Aegis defense systems in the region.

The Timing: This capability—the ability to paralyze global shipping—was not built in a week.

The Question of Intent: If the goal was destruction, the capability existed for years. Yet, this "swarm" was only unleashed after the Saturday morning "decapitation" strikes.

We are presented with two sets of facts. On one hand, a series of pre-planned financial moves by political insiders and a massive military resupply that began in mid-January. On the other, a 30-year period of Iranian military restraint that only ended when the "pre-emptive" strike occurred.

Was the attack a response to a sudden, imminent threat? Or was the threat used as a catalyst for a long-planned regional and financial restructuring that the "Queen of Capitol Hill" and prediction market whales were already betting on in January?

What do you think happened? 👇👇👇

1

4

9

258

wez retweeted

The End of the Banks Has Started?

For years, we’ve been told that the banking system is safe, resilient, and well-capitalized. When cracks appear, regulators repeat the same reassurance: this is isolated, this is contained, this is not systemic.

Then, quietly, another bank closes its doors.

Late on Friday, U.S. regulators shut down Metropolitan Capital Bank & Trust, a small Chicago-based institution. By Monday morning, depositors were protected, accounts transferred, and the story was already fading from headlines. The Federal Deposit Insurance Corporation stepped in, as it always does, to stabilize the situation.

From the outside, the system worked.

But beneath the surface, a deeper question is forming — one that’s becoming harder to ignore.

Has the end of the traditional banking model already begun?

A system built for a world that no longer exists

Small and regional banks were designed for stability, not speed. Their business model relied on modest returns, long-term relationships, and predictable economic conditions. They didn’t chase extreme profits. They didn’t take outsized risks. They played by the rules.

That’s precisely the problem.

In today’s environment, playing it safe is no longer enough. Rapid interest-rate changes, rising funding costs, and volatile asset prices have compressed margins to the point where there is little room for error. When a shock hits — whether from rates, liquidity, or confidence — smaller banks absorb the impact first.

They don’t fail loudly.

They fail quietly.

Usually on a Friday.

Confidence, not capital, is the real battleground

Banking has always depended on trust. What’s changed is how fast that trust can disappear.

Depositors no longer wait in lines. They move money with a tap. Information — and fear — spreads instantly through social media, group chats, and financial forums. A rumor today can become a withdrawal wave tomorrow.

Even a well-run bank can’t survive if confidence breaks.

This creates a brutal reality: solvency matters less than perception. And perception is no longer controlled by institutions or regulators — it’s controlled by the crowd.

Regulation protects the system, not the bank

When regulators intervene, the message is subtle but clear.

Depositors will be protected.

The system will be stabilized.

The institution itself is expendable.

This is not a criticism of regulators — it’s their mandate. Stability comes first. But over time, this approach produces an unintended consequence: consolidation.

Each small bank failure quietly strengthens the largest players. Deposits flow upward. Power centralizes. Risk concentrates.

Ironically, the very actions meant to reduce systemic risk may be increasing it.

The uncomfortable truth no one wants to say out loud

The financial system no longer rewards restraint.

It rewards:

Scale

Speed

Access to emergency liquidity

Political and institutional importance

Small banks are trapped in a contradiction. They are expected to be conservative, yet compete in a high-velocity, high-risk environment. When stress appears, they are too small to be rescued and too important locally to fail without damage.

That is not mismanagement.

That is structural failure.

Why this matters beyond banking

This is bigger than one bank closure.

It speaks to a loss of faith in centralized financial intermediaries — a slow erosion, not a sudden collapse. Each “contained” failure chips away at the assumption that the system works for everyone equally.

And that erosion is happening at the same time as alternatives are maturing.

Bitcoin doesn’t close on Fridays.

Stablecoins don’t depend on local branch confidence.

Self-custody doesn’t require trust in management decisions you’ll never see.

This doesn’t mean banks disappear tomorrow. But it does suggest something more subtle — and more dangerous for the old model.

So… is this the end?

Not a collapse.

Not a sudden reset.

But a long, quiet transition.

The end of banking as we knew it may not come with a bang. It may come with a series of polite press releases, insured deposits, and forgotten headlines — until one day people realize they stopped trusting the system long ago.

And once trust is gone, no amount of regulation can bring it back.

1

1

9

93

🚨Stop guessing. Start Reading."

Why did that protocol rug? Why is this yield farm sustainable? Our magazine breaks down the 'Why' so you can focus on the ROI DeFiTimeZ is where the $DFTZ community gathers to share alpha, discuss the latest issues, and grow the ecosystem together

9

Most traders are playing catch-up. At @DeFiTimeZ we’re tracking the flow before the pump. If you’re tired of being the last to know, you’re in the right place. The clock is ticking—get in the room where the moves happen

$DFTZ #DeFi DeFiTimeZ.com t.me/DeFiTimeZ

25

wez retweeted

Jan 12

Liquidity Breaks Before Systems Do

When people imagine a financial collapse, they picture chaos. Bank runs. Market crashes. Currency failure. Headlines screaming that everything is over.

That’s almost never how it starts.

Systems don’t break loudly.

They break quietly — when liquidity disappears.

Liquidity isn’t money in the abstract. It’s money in motion. It’s the ability to borrow, lend, settle, and transfer without friction. When liquidity is abundant, everything looks stable. When it tightens, stress appears long before collapse is visible.

This is the part most people miss.

What liquidity actually means

In simple terms, liquidity is how easily value moves through the system.

It’s:

banks willing to lend

markets willing to trade

counterparties willing to settle

confidence that obligations will be met

A system can look solvent on paper and still fail if liquidity dries up. Assets may exist, balance sheets may appear healthy, but if no one is willing to transact, the system freezes.

That freeze is where crises begin.

History repeats this pattern

In 2008, the first problem wasn’t insolvency. It was liquidity. Banks didn’t know who was exposed to what, so lending stopped. Overnight markets seized. Central banks stepped in not because everything had collapsed, but because it was about to.

In 2020, markets didn’t crash because assets vanished. They crashed because liquidity disappeared. Even U.S. Treasury markets — the deepest in the world — experienced stress. Again, emergency facilities appeared almost instantly.

More recently, regional bank stress followed the same script. Confidence weakened, deposits moved, and liquidity tightened. Intervention followed.

Different triggers. Same mechanism.

Liquidity breaks first.

Why central banks obsess over liquidity

This is why central banks respond so aggressively to early signs of stress. They aren’t trying to save speculators. They’re trying to keep money moving.

Once liquidity stops:

credit contracts

defaults cascade

prices gap violently

trust evaporates

At that point, it’s no longer manageable.

So they act early. They inject reserves. They open facilities. They promise support.

Not because the system is healthy — but because liquidity is fragile.

Who feels it first

Liquidity stress doesn’t hit everyone equally.

It shows up first where buffers are thinnest:

small and mid-sized banks

small businesses dependent on credit

consumers relying on revolving debt

emerging markets dependent on external funding

Large institutions are protected by access. Smaller participants are not.

This is why crises feel “sudden” to the public. By the time households feel it, the system has already been under strain for months.

Why this matters now

After years of emergency measures becoming permanent, liquidity has become more sensitive, not less. Markets are conditioned to support. Withdrawal of that support, even partially, creates outsized reactions.

At the same time:

debt levels are higher

funding costs are more volatile

trust is more conditional

That combination makes liquidity the most important variable in the system — and the most fragile.

The quiet consequence

When liquidity becomes uncertain, behaviour changes.

Banks become cautious.

Lending standards tighten.

Settlement risk is reassessed.

Access becomes selective.

And when access becomes selective, alternatives begin to matter.

Not because the system has failed — but because relying on a single channel becomes risky.

This is where parallel rails, neutral settlement systems, and assets outside traditional credit structures start to attract attention. Not as replacements. As options.

The signal most people ignore

A system doesn’t warn you before it breaks.

But liquidity does.

When money stops moving freely, when lending becomes conditional, and when access depends on who you are rather than what you hold, stress is already present.

Collapse, if it comes, is just the final chapter.

Liquidity is the story before the story.

What comes next

If liquidity is the first thing to fail, the next questions become obvious:

why governments protect it at all costs

why inflation is often chosen over default

and why controls don’t appear overnight, but creep in quietly

That’s where this series goes next.

Because understanding liquidity isn’t about predicting disaster.

It’s about recognising how systems really break.

4

4

10

356

wez retweeted

3 Oct 2025

Set a reminder for Interviewing Ben from SEDL banking App $SEDL #Dundies $DFTZ @BenfromWA! x.com/i/spaces/1lPKqvDwbPbGb

4

5

13

757

wez retweeted

3 Sep 2025

☀️ Good Morning!

Opportunities don’t wait—today is the perfect day to move closer to your goals. 🚀

Stay sharp, stay positive, and keep building. The best is yet to come. ✨

#GoodMorning #Crypto #DeFi

#Dundies $DFTZ

8

3

12

255

wez retweeted

30 Aug 2025

What if I told you there’s a token that destroys itself every time money touches it? 🔥

Sounds insane, right? 👇👇👇👇👇👇👇

1

2

4

147

wez retweeted

28 Aug 2025

🟧 #Bitcoin sits near $113K after shaking out weak hands at $108K.

But here’s what most won’t tell you 👇

⚡ None of the 30 major bull-market top indicators are flashing red. Every single one is still open — meaning the data shows we haven’t hit the cycle peak yet.

⚡ Cycle models are projecting $135K–$230K BTC before a real top.

⚡ Short-term resistance: $116K–$118K.

⚡ Key support: ~$108K.

So why does mainstream coverage still scream “bubble” every time BTC dips? Because the narrative is easier to sell than the truth.

👉 The truth is: Bitcoin consumes less energy than the legacy banking system. The truth is: every cycle, the crowd is shaken out while the patient few hold on to life-changing gains.

This isn’t financial advice — it’s a reminder that knowledge is power. Indicators show strength.

Momentum remains. And if you’re reading this, you’re already ahead of the majority who will only wake up at the very top.

Stay curious. Stay free. 🟧⚡

#BTC #Crypto #DFTZ

1

3

5

232

wez retweeted

28 Aug 2025

Crypto vs. Banking: The Future of Money Is Already Here

For over a century, the banking system has been the gatekeeper of money. They decide who gets access, what it costs, and how long it takes to move. But in the shadow of glass towers and marble lobbies, a new contender has emerged: crypto. While banks rely on control, crypto thrives on freedom. And when you put them side by side, the cracks in the old system become impossible to ignore.

Accessibility & Control

Banks tell us they’re here for everyone, yet over a billion people worldwide remain unbanked. Why? Because the system demands paperwork, government IDs, proof of address, and credit histories. In other words—permission. If you don’t fit their mold, you’re excluded.

Crypto flips this script. With nothing more than a smartphone and an internet connection, anyone can create a wallet and hold value. There are no middlemen to approve or deny you, no banker deciding your worthiness. For the first time, access to financial tools is a right, not a privilege.

And here’s the hidden truth the banks don’t want front and center: they profit from exclusion. The fewer people who qualify, the more fees they can extract from those inside. Crypto doesn’t punish you for being different—it empowers you to take part, permissionlessly.

Transaction Speed & Cost

If you’ve ever sent money internationally, you know the pain: days of waiting, unpredictable fees, and multiple banks taking their cut along the way. The system is so outdated it still relies on legacy networks like SWIFT, built decades ago.

Crypto makes this look medieval. A Bitcoin or stablecoin transfer can move across borders in minutes. No hidden intermediaries, no inflated conversion fees. The only real cost is a small network fee—transparent and predictable.

Think about it: banks hold your money, then charge you for the privilege of moving it. Crypto lets you move value the way email lets you move words—instantly, globally, without permission.

Trust vs. Code

Banks thrive on one word: trust. Trust us to hold your savings, trust us to lend responsibly, trust us not to collapse. History shows how fragile that trust really is—financial crises, government bailouts, money laundering scandals. Time and time again, trust has been broken.

Crypto doesn’t ask for blind faith. It runs on open-source code, visible for all to inspect. Transactions are verified by a decentralized network, not a boardroom. You don’t need to “trust” Bitcoin; you can verify it with math.

That’s why crypto feels threatening to banks—it replaces trust in people with trust in protocol. And once you’ve seen that code can do the job better, it’s hard to go back.

Scarcity vs. Inflation

The banking system runs on fiat money, which can be printed endlessly. When central banks flood the economy with new cash, the value of what you hold shrinks. Inflation is simply legalized theft of purchasing power.

Bitcoin is the opposite. It has a hard cap of 21 million coins, forever. No politician, no central banker, no billionaire can change that. This programmed scarcity turns Bitcoin into “digital gold”—a hedge against a system that bleeds value every year.

Ask yourself: would you rather store your wealth in a system where supply is infinite, or one where supply is fixed and predictable? The answer is obvious. And maybe that’s why adoption keeps growing—because people are waking up to the rigged game of inflation.

The Verdict

Crypto isn’t just an alternative; it’s a mirror held up to the flaws of banking. Where banks exclude, crypto includes. Where banks delay, crypto accelerates. Where banks demand trust, crypto offers proof. And where banks inflate, crypto preserves.

The fight isn’t just about money—it’s about who controls the future. The choice is no longer between old and new. It’s between control and freedom.

1

3

4

162

wez retweeted

27 Aug 2025

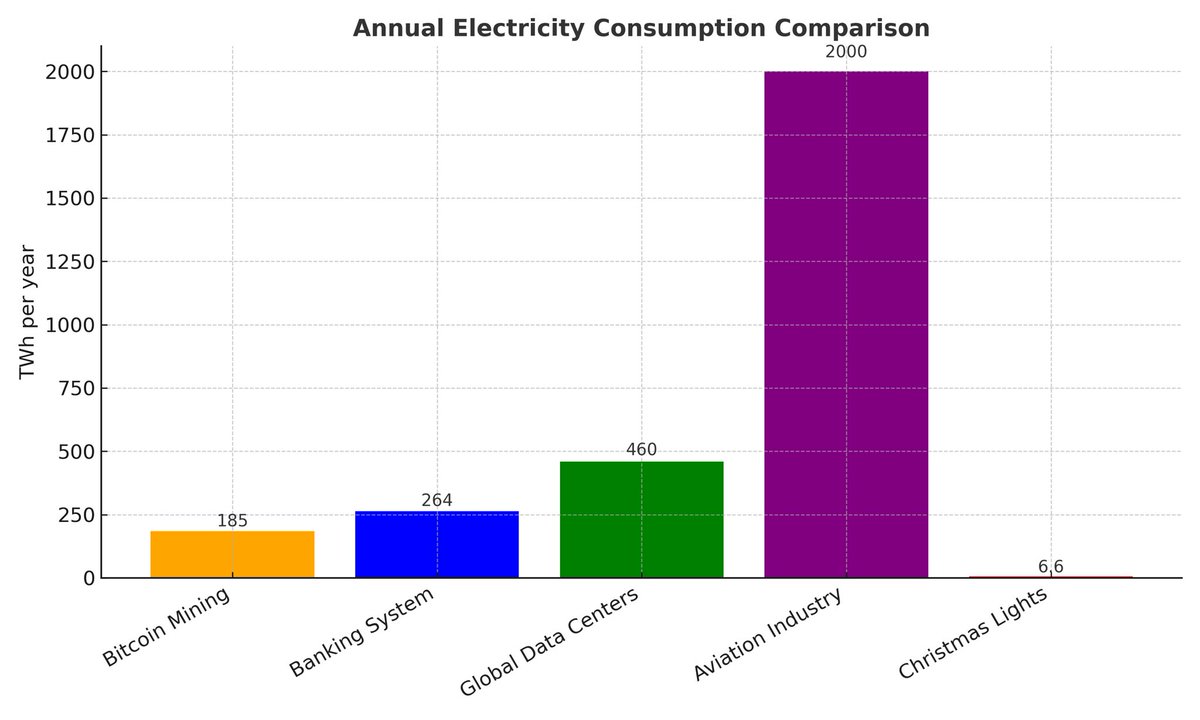

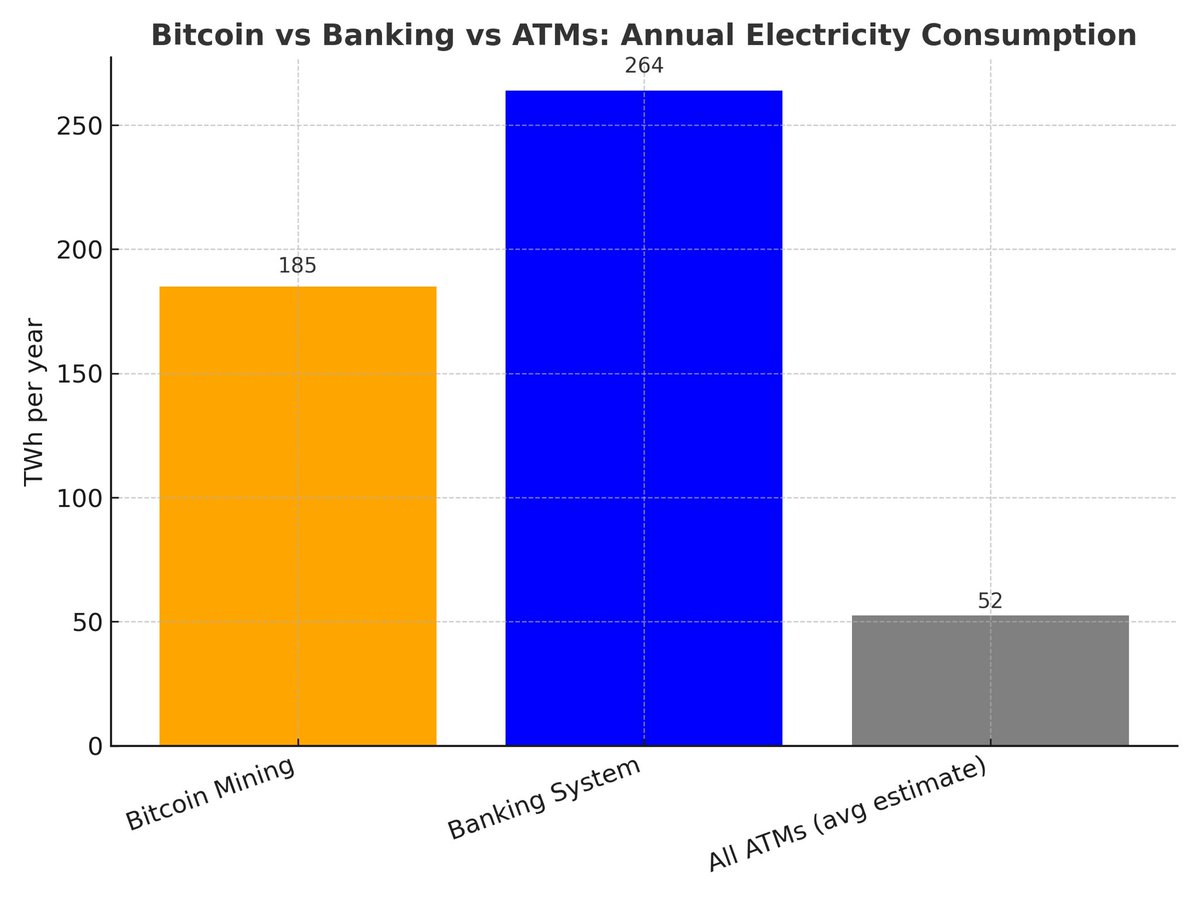

Banking vs. Bitcoin: Who Really Consumes More Energy?

Critics love to claim Bitcoin is an “energy hog.” The headlines practically write themselves: “Bitcoin uses more electricity than small countries!” But here’s the twist—what about the traditional banking system it was designed to disrupt?

⸻

Bitcoin’s Energy Appetite

A single modern miner, like an Antminer S19 Pro, draws about 3.25 kW nonstop. That’s ~78 kWh per day, or 28 MWh per year per unit.

Zoom out to the whole network:

•Current hashrate: ~950 EH/s

•Equivalent machines: ~4–6 million ASICs (depending on model efficiency)

•Global annual consumption: ~185 TWh

That’s no small figure. But is it actually more than banking?

⸻

Banking’s Hidden Energy Bill

The global banking system is a vast, physical operation. Beyond offices and branches, it runs armies of servers, payment networks, and millions of ATMs.

One major analysis estimated the banking sector consumes ~264 TWh per year. That’s 1.4× Bitcoin’s footprint.

The breakdown:

•983,000 bank branches worldwide

•~2.9 million ATMs

•Global HQs, central banks, and the BIS itself

•Payments, data centers, compliance systems

Even ATMs pack a punch.

•In-branch terminals: ~6–7 kWh per day

•Standalone kiosks (with A/C, lighting): 57–93 kWh per day

That means some ATMs rival a miner one-to-one.

⸻

Face-Off: Who Uses More?

•Banking system: 264 TWh/yr

•Bitcoin mining: 185 TWh/yr

•ATMs alone: ~50 TWh/yr (average estimate)

So yes—banks as a whole burn more energy than Bitcoin.

⸻

Context Matters

Bitcoin is not alone.

•Global data centers: 460 TWh/yr

•Aviation industry: ~2000 TWh/yr

•Even Christmas lights: 6.6 TWh/yr

Against these, Bitcoin looks less like an outlier and more like a young industry.

⸻

The Real Question

Bitcoin does consume energy. That’s by design: proof-of-work is what makes it secure and decentralized. But energy is also the price of trust.

Banks enforce trust through staff, paperwork, and regulators. Bitcoin enforces it with math, miners, and code.

So the question isn’t whether Bitcoin uses energy. It’s whether the freedom and decentralization it provides are worth the cost of keeping the lights on.

⸻

✅ Bitcoin: 185 TWh/yr

✅ Banking: 264 TWh/yr

✅ ATMs: 50 TWh/yr

The numbers are clear. The legacy system consumes more — yet no one calls banks “wasteful.”

⸻

Final Thought

Decentralization isn’t free. But neither is the old financial empire. If anything, Bitcoin shows us how much efficiency can be gained when money is secured by open networks rather than guarded vaults.

DeFiTimeZ.com #Dundies $DFTZ

5

5

12

357