Western Arable. Grain marketing specialists, established 1993 serving Gloucestershire, the South West of England, South Wales & beyond. 01242 680414.

Joined August 2012

- Tweets 373

- Following 346

- Followers 116

- Likes 58

114 Photos and videos

In summary; gross margin tables are a guide, not a budget. AHDB stresses using your own figures, watching #milling and #malting premiums, and weighing 3–5 year rotational & SFI options rather than chasing a 1 yr ranking. via @AHDB_Cereals ahdb.org.uk/news/analyst-ins… #grains #oatt

17

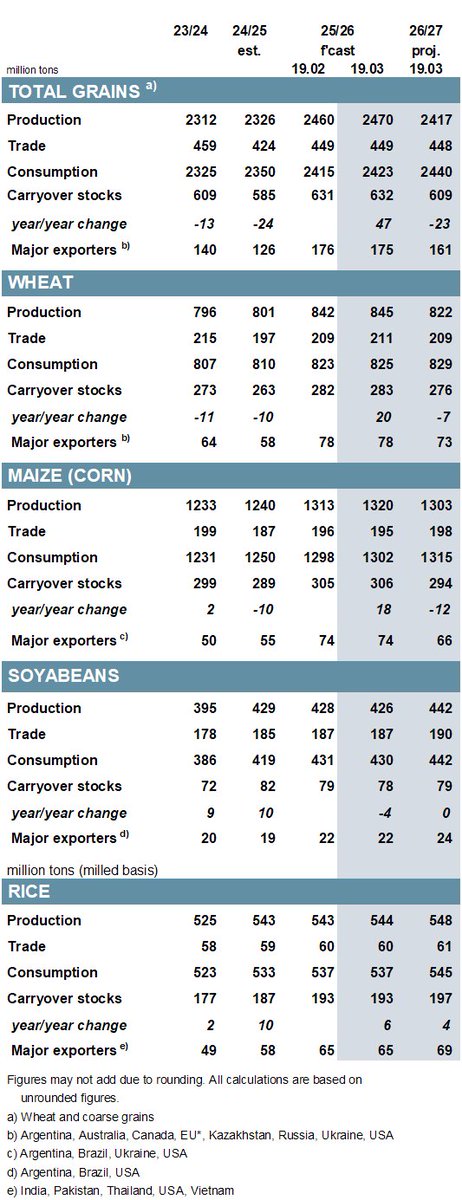

UK #oats milled are up 6.7% Jul–Mar YoY. Closing oat stocks 16.7% higher, consistent with robust demand for oat-based products. The overall H&I usage numbers point to a demand-led easing in the UK #cereals balance. (via @AHDB_Cereals) ahdb.org.uk/cereals-oilseeds… 3/3

35

Tomorrow sees our first moisture meter clinic. 10am-3pm here at the grain store. Join us for coffee and tea, cakes & a chat, plus Origin Soil Nutrition will be here to talk fertiliser options for the autumn. w3w.co/amuse.robes.durations

15

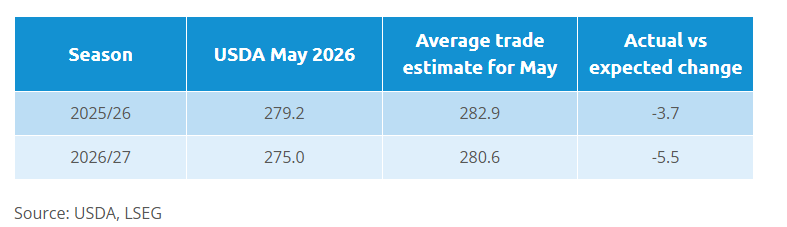

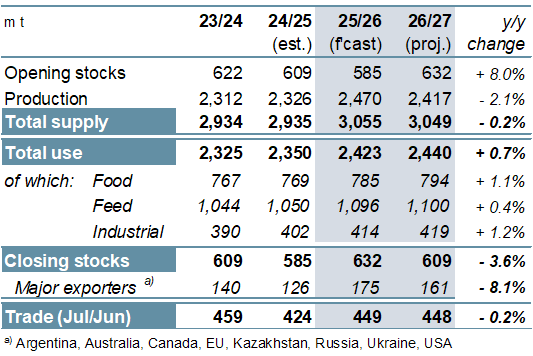

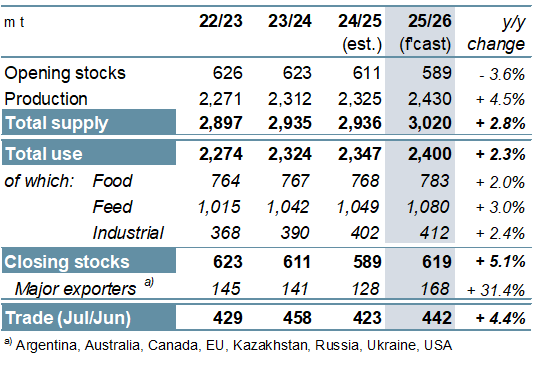

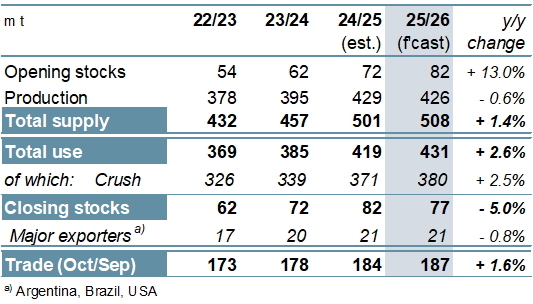

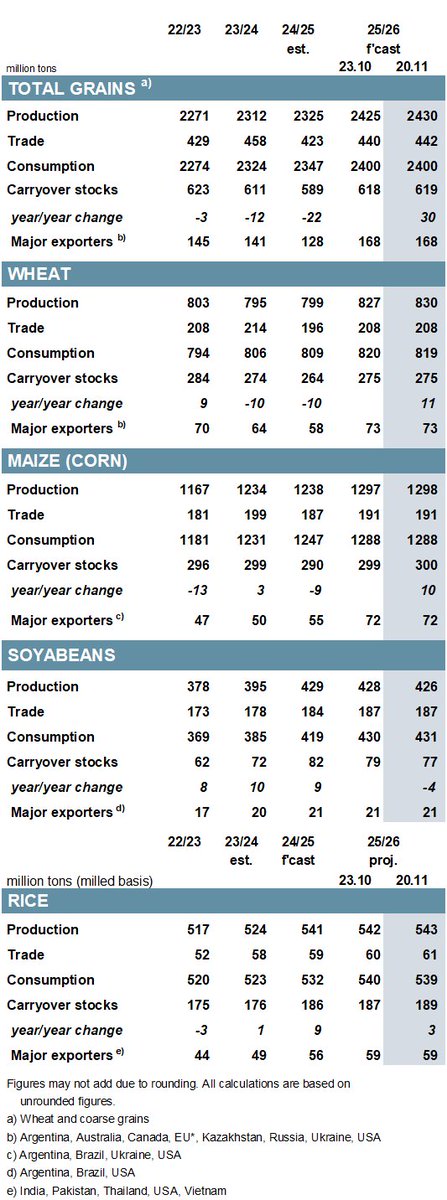

Even after the #WASDE cuts, 26/7 world #wheat stocks sit about 1.3% above 5 yr av, which may cap rallies unless weather risk >. #Soybean & #OSR stocks are more comfortable, but crude & biofuel demand are > prices. via @AHDB_Cereals 3/3 #oatt #grains ahdb.org.uk/news/wheat-ralli…

87

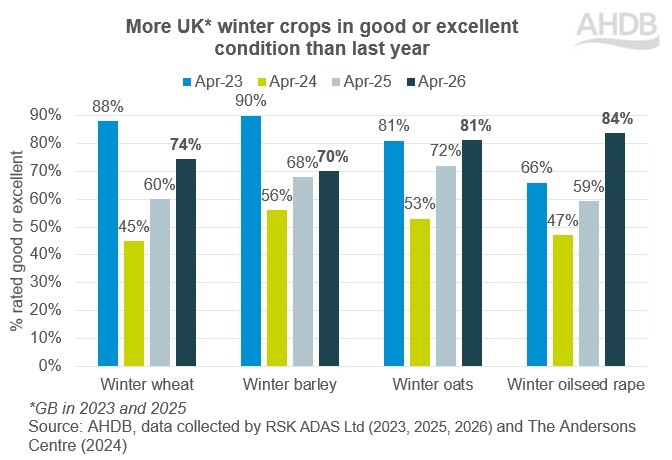

UK winter cereal crop conditions have dipped since late March, but still better than the same time in 2025 and above 2022–24. The recent rainfall over the BH wknd will have helped. ahdb.org.uk/cereals-oilseeds… (via @AHDB_Cereals) #oatt #grains #wheat #barley #OSR

100

@AHDB_Cereals have today published their April crop dev update: 75% of UK winter #wheat rated good/excellent (down from 82% in March but well above 60% last year), with dry conditions in much of England key to yield risk. 1/2 #oatt #grains #arable

1

1

35

70% of UK winter #barley is rated good/excellent (52% good, 18% excellent), down sharply from 85% last month and only slightly above 68% a year ago, with conditions varying markedly by region. 2/2 #oatt #grains #arable ahdb.org.uk/cereals-oilseeds…

44