81 Photos and videos

Place 2 to 10 are a bunch of losers. Can’t even reach $500B

24

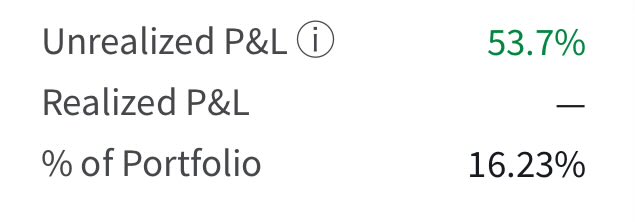

This $hrow

May 12

$HROW is one of my longterm positions. Drama is guaranteed with every earnings report, and it’s worth understanding why investors here constantly swing between euphoria and depression.

My thesis: Harrow has built a unique platform for ophthalmic medications in the U.S., the largest portfolio of prescription eye care products in the North American market. The company is currently in the phase where these products are being aggressively rolled out, while new ones are simultaneously being added. The potential is enormous: VEVYE addresses a DED market with 16 million diagnosed U.S. patients, IHEEZO a TAM of over 14 million annual procedures at less than 2% penetration.

So why does Harrow disappoint so often? Because there is a crucial difference between growth in units sold and the resulting revenue. VEVYE prescriptions grew 25% in Q1, IHEEZO units 18%, TRIESENCE 136%, yet total revenue declined 8%. This phenomenon is called a volume-value gap: unit volumes are growing, but net revenue per unit lags behind.

The reason is what I’d call the “sow now, harvest later” phase of pharma commercialization. Harrow is deliberately sacrificing short-term revenue and profit to capture market share, through copay programs, low barriers to entry, and aggressive coverage deals. A new VEVYE patient is acquired today at a high upfront cost, but then refills approximately 9 times per year at significantly better net prices. Management is convinced this investment will convert into stable, recurring revenue within 2-4 quarters. The ~30% ASP improvement starting in Q2 reported yesterday is a first concrete signal that this normalization is actually happening.

On the investor base: Over the past few weeks, I noticed several accounts on X jumping into this stock, accounts I’ve mostly seen chasing quick trades with surface-level theses. Their analysis was shallow, buzzwords without understanding the gross-to-net dynamics or the seasonal phasing structure of Harrow’s revenue. I suspect yesterday’s earnings report is flushing exactly these investors out. That’s healthy.

On the $250 million quarterly revenue target by end of 2027: Honestly, one has to doubt whether it will be achieved within that exact timeframe, my own bottom-up model arrives at around $200 million for Q4 2027 depending on the scenario. But I consider it highly likely that Harrow reaches this level by 2028 at the latest, once BYOOVIZ and OPUVIZ scale and G-MELT enters the market. CEO Baum himself has acknowledged: “My timing may occasionally be off by a quarter or even two”, but his long-term track record speaks for itself (stock 700% over 5 years).

The key point: Once this sowing phase is behind us, Harrow becomes a compounder with a deep moat, regulatory-protected products (Orange Book patents through 2039), 9x refill economics, and a scalable platform onto which every acquisition can immediately plug in. Their platform is becoming the go-to distribution partner for pharma companies looking to commercialize ophthalmic products in the U.S.And all of this in a market with extremely strong structural tailwinds: the aging U.S. population is driving cataract surgeries, DED diagnoses, and retina injections structurally higher, regardless of economic cycles. The real story starts in H2. Everything until then is mostly noise

1

773

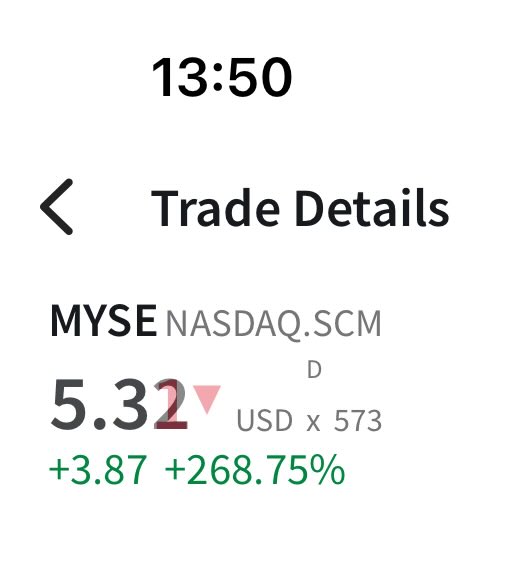

Obviouly I am down right now. Also obivious this stock will go to 90$...80$... 70$

I was serious about that. $intc

150

Worst Investor (Goal: 10x in 5 years) retweeted

Apr 29

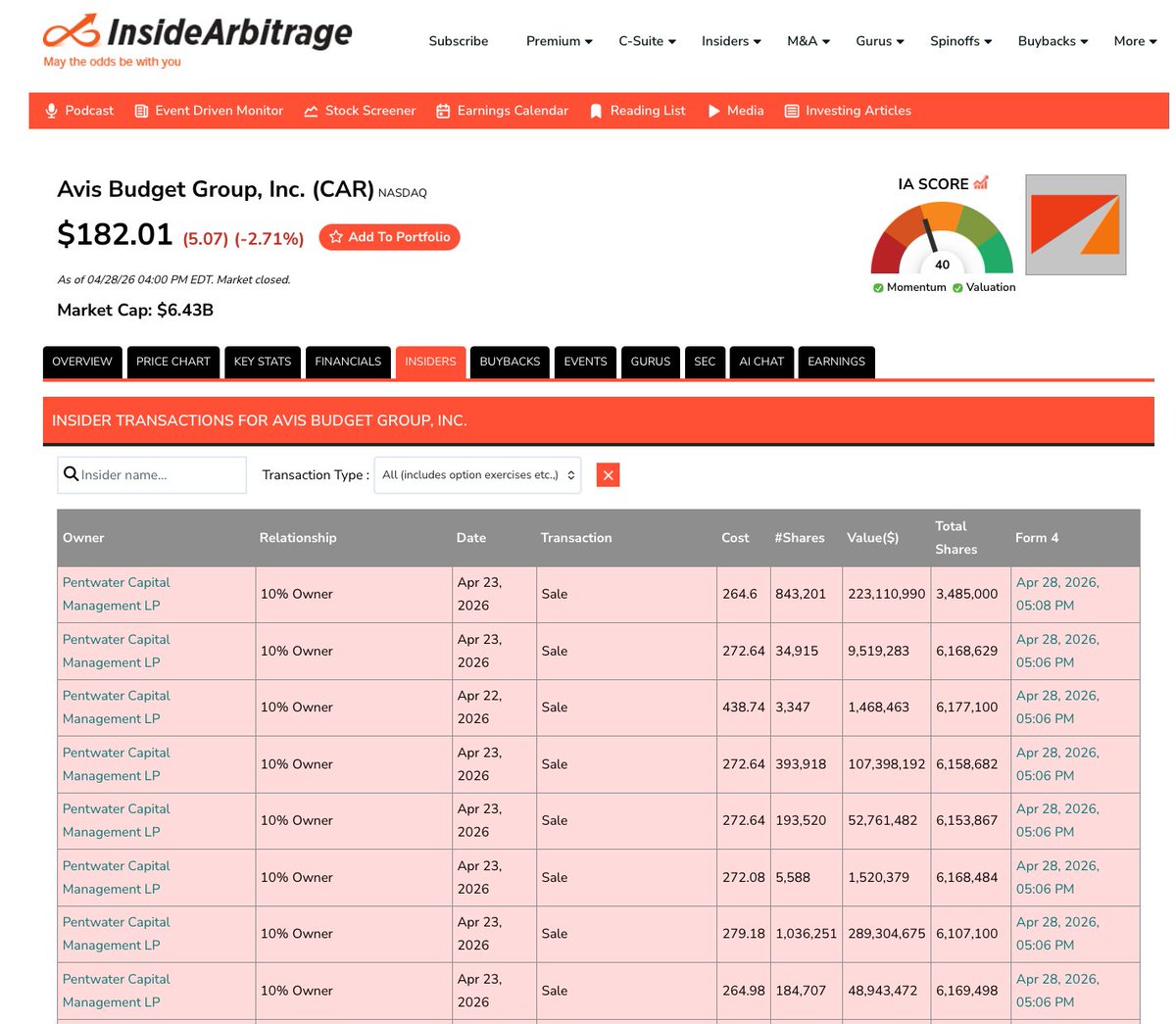

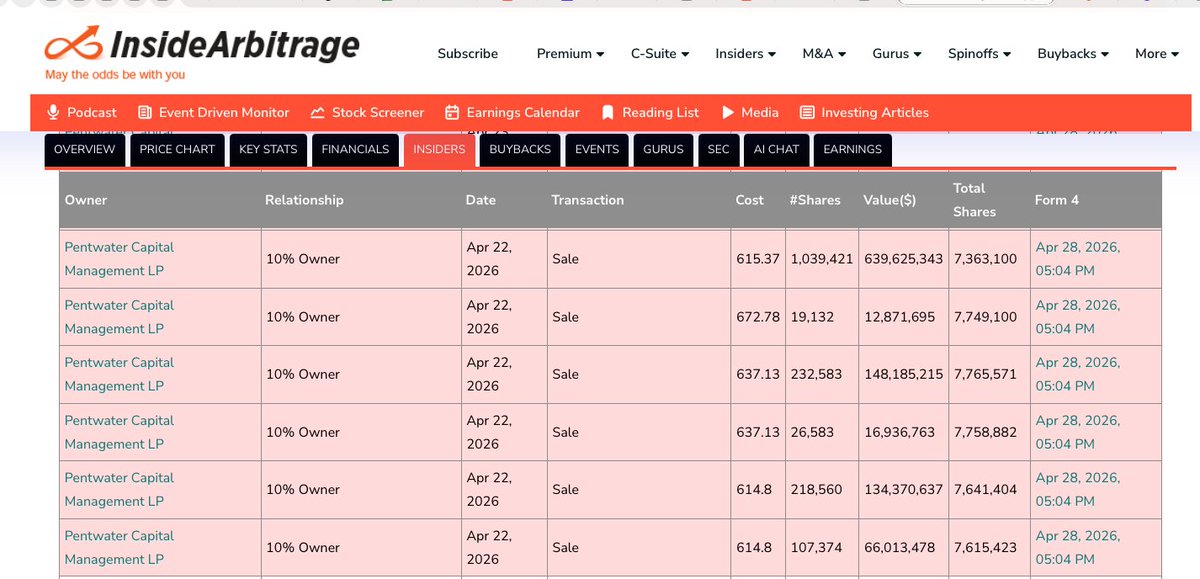

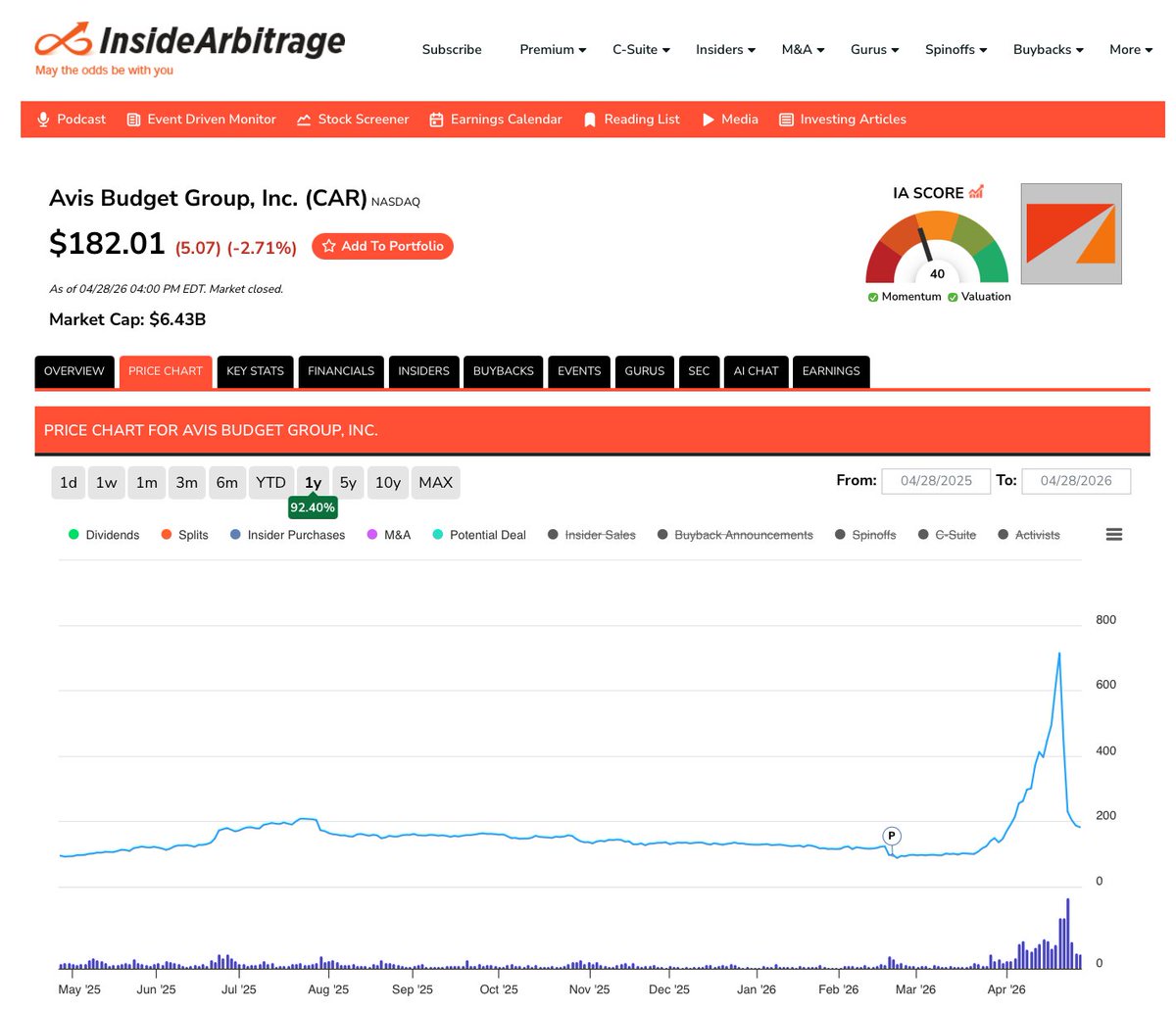

And now they are selling. It is amazing that they managed to sell over $1 billion of $CAR at prices north of $600.

Total sales were $1.75 billion. An absolute home run for Pentwater Capital.

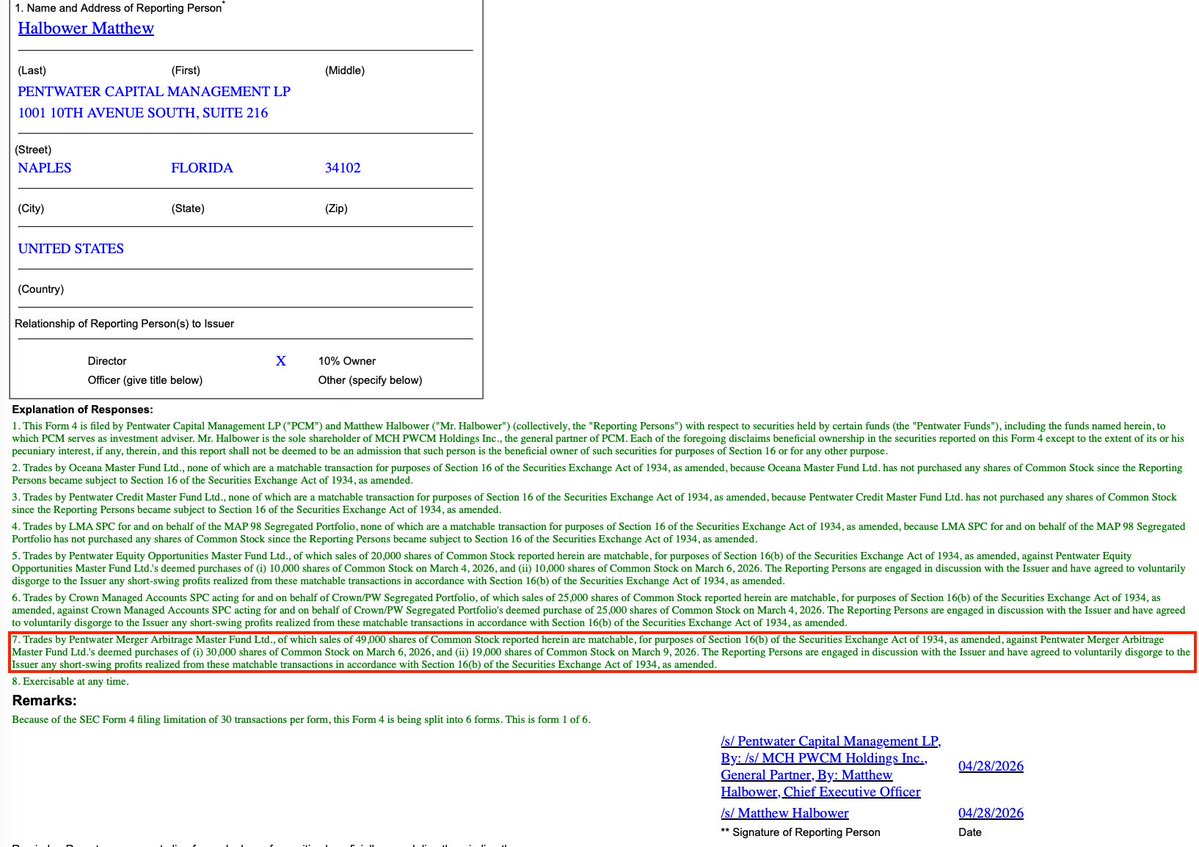

As expected, they are giving some profits back to the company because they violated the short-swing rule.

Apr 14

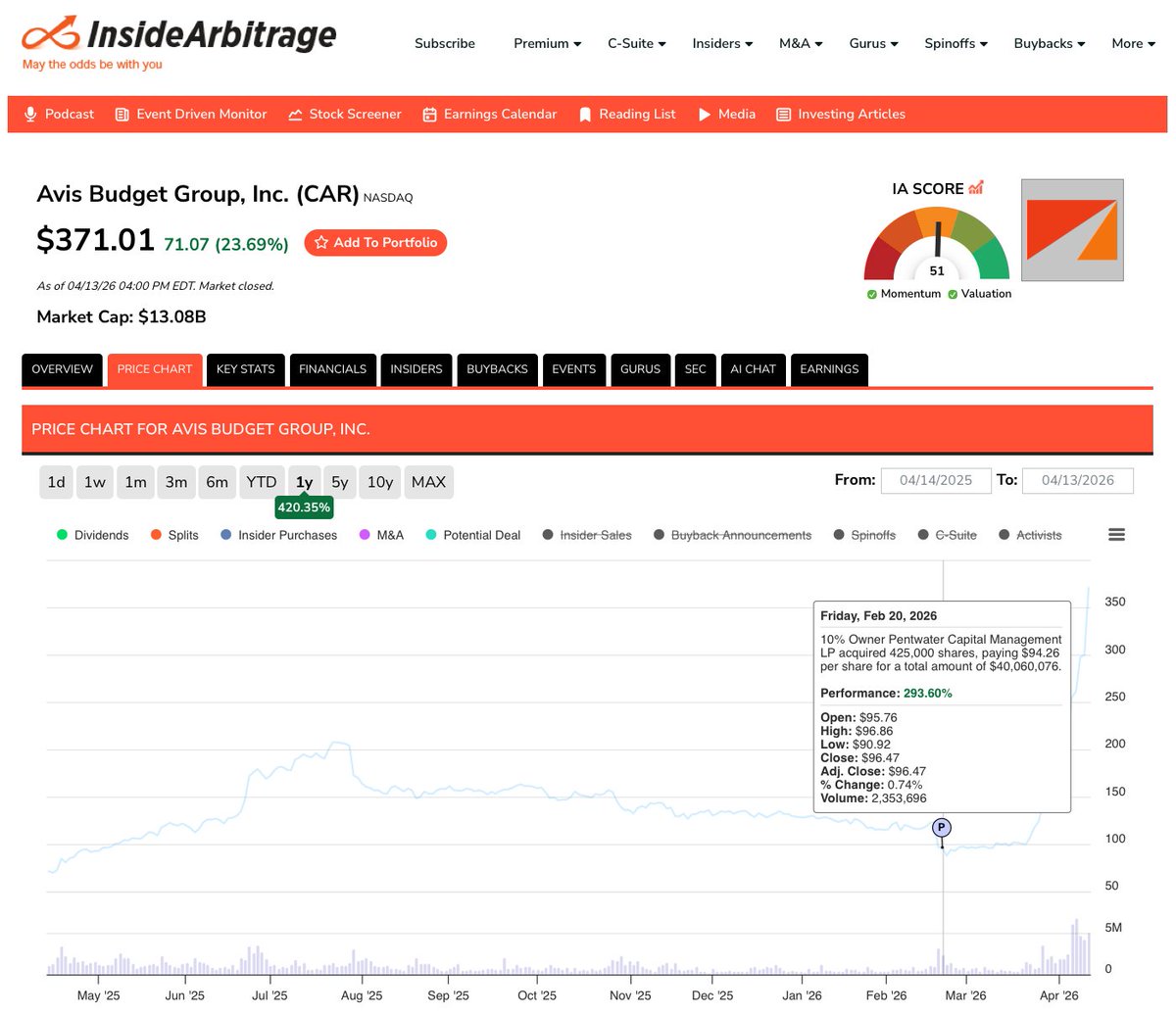

The best timed insider purchase ever?

And that too by a merger arbitrage focused fund.

18

36

331

168,867

Worst Investor (Goal: 10x in 5 years) retweeted

Apr 26

$NOW will go down as the greatest dip-buying opportunity of 2026…

Currently down -62% from ATH’s, markets are pricing LLM’s to replace software.

The CEO of ServiceNow strongly disagrees, & even just recently bought $3M worth of shares.

Jensen Huang, the $NVDA CEO is also bullish on $NOW and believes LLM’s will become apart of software.

$180 incoming within a year time.

Mark it…

90

118

1,599

344,499

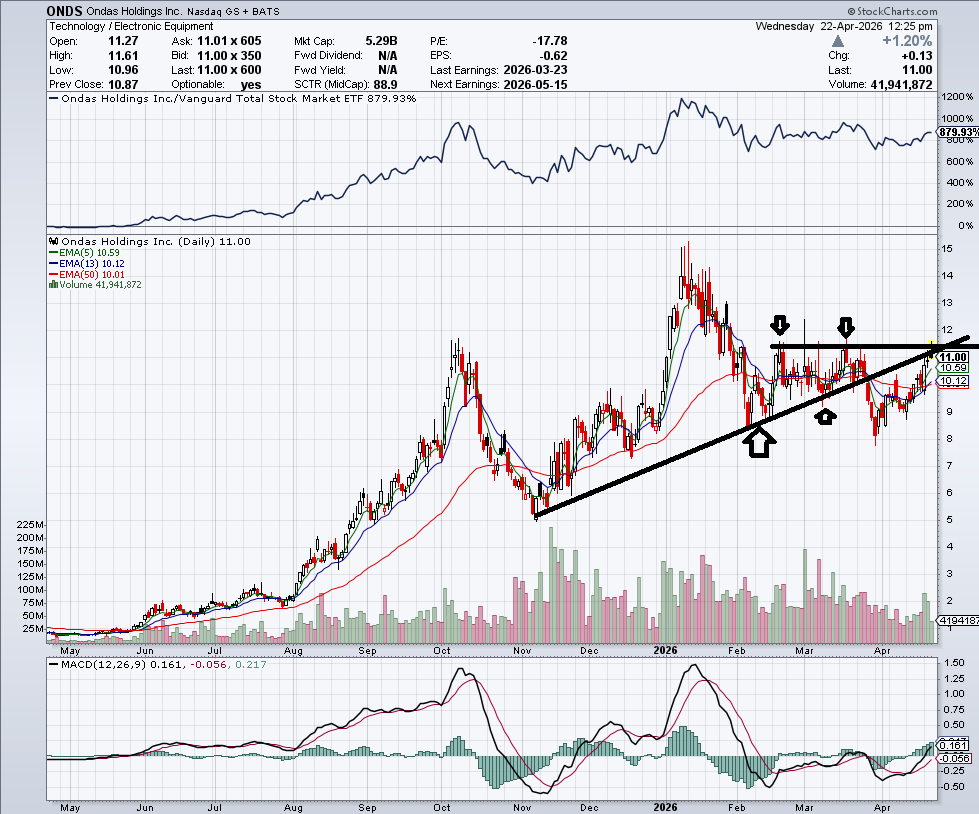

Tailing

Apr 22

one of my favorite short setups.. two resistance lines, converging.

This one is easy.. short here at $11

if the stock EVER closes above EITHER of those two black lines, you cover the short

excellent risk/reward set up

$ONDS (the failing drone/data networking stock)

60

Will be 100$ in three days. Just my feeling. I added to my long position $now

1

525

Worst Investor (Goal: 10x in 5 years) retweeted

Apr 21

$CAR There's a thing called the short-swing profit rule that states if you are above a 10% holder in a company any profitable trades that were held for six months or less are due to the company. Pentwater can't sell a lot of its shares here because the profits would be owed to Avis.

But there are around 2.4mm shares they acquired last year that they can sell and not be subject to short-swing.

10

11

140

40,484

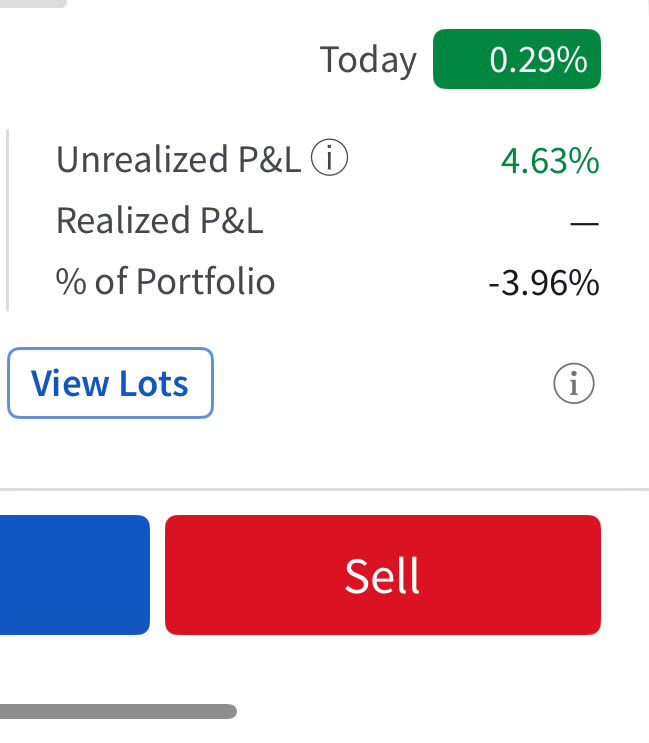

$CAR thinking about covering my shorts. Does that mean it’s the top?

1

396

long $MSFT stop just below EMA21. stops may change daily.

1

97

Added to my $car short. Come at me bro. Liquidate me bitch.

2

1

186

Opening my IBKR app to check if I have been liquidated $CAR

1

1

300