Joined January 2020

- Tweets 13,783

- Following 974

- Followers 13

- Likes 9,338

10 Photos and videos

RT @rajuidesai: Repono Ltd...

20 yrs Ril Ind Ltd contract is big for me....

thehindubusinessline.com/com…

20

yash retweeted

I am sure by the time Bengaluru’s Namma Metro reaches @BLRAirport it will be time to move the airport to a new location. It’s been more than 18 years since Kempegowda Intl Airport was opened on May 24, 2008. Pathetic! @CMofKarnataka @DKShivakumar @PMOIndia @AshwiniVaishnaw

80

163

1,031

64,786

yash retweeted

Jun 16

Nearly every company on this map traces to a single decision made in Pasadena in 1930.

That year the Guggenheim family paid to bring Theodore von Kármán to Caltech to run its aeronautics lab. His graduate students, a crew known on campus as the Suicide Squad, lit their first liquid rocket motor in a dry riverbed north of the Rose Bowl on Halloween 1936. That test site became JPL.

The aircraft industry stacked in around it. Lockheed, Douglas, Northrop, and Hughes built planes across the same basin through WWII and the Cold War. Each generation of engineers trained here, then trained the next batch, then sent their kids to the same schools.

The talent never left. That is the whole story of this map.

SpaceX headquarters sits at 1 Rocket Road in Hawthorne, inside the old Northrop plant that built aircraft on that spot for 70 years. The same building once turned out 747 fuselages. Elon put the rocket factory there because the workforce was already standing in the parking lot.

You can move a headquarters with a single post. No one has figured out how to move tens of thousands of aerospace engineers and the knowledge sitting in their heads. When the SpaceX HQ move to Texas got announced, this map barely lost a dot.

The startups are new. The cluster feeding them is almost a century old, and it compounds every year a fresh graduate walks out of Caltech or USC into the company next door.

35

282

1,519

154,297

yash retweeted

Jun 15

A 90-year-old ex-serviceman from Tehri Garhwal has been separated from his family for 25 years. He is working at a dhaba in Mukerian, Punjab. Help bring him home.

Pratap Singh Parmar, a retired Indian Army soldier originally from village Mangsu Chauras in Tehri Garhwal, lost contact with his family around the year 2000. For 25 years, this 90-year-old veteran has been living alone, earning his keep at a roadside dhaba in Mukerian, Punjab.

His son is believed to be Vinod Parmar, a teacher in Rudraprayag, who may have been searching for his father all these years.

If you recognise him or know his family, please contact immediately.

Rakesh Sharma (Dhaba owner), Mukerian, Punjab

Mobile: 8750491866

A soldier who served his nation deserves to spend his last years with his loved ones. Do your bit.

51

687

1,100

43,588

yash retweeted

Jun 16

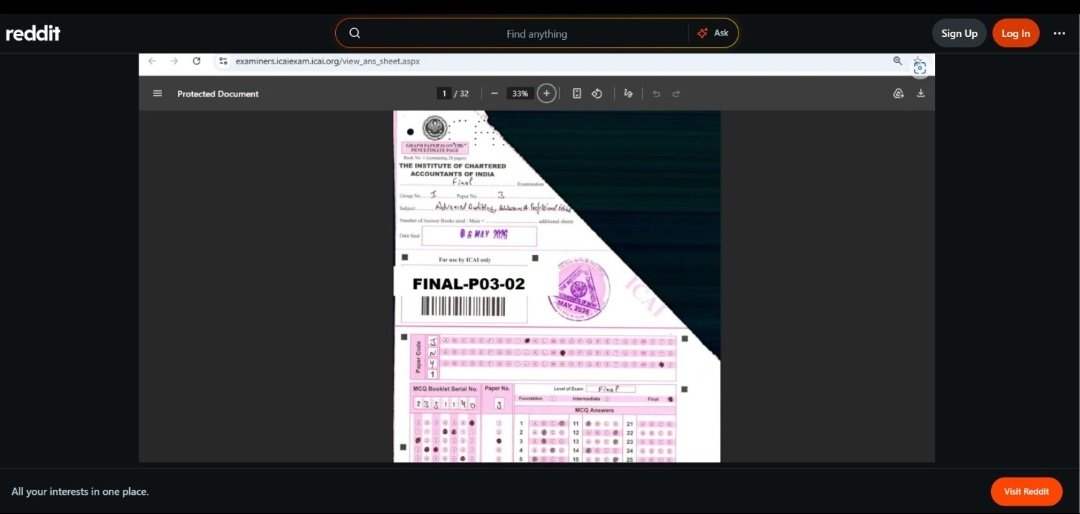

🚨Very Shocking

ICAI Examiners portal hacked.

Hacker has Access of 200K records.

Allegedly compromised access/data includes:

• Full remote code execution and superadmin control of the portal

• Answer sheets of all students who appeared in May 2026

• Ability to modify marks per question and on full papers

• Examiner profiles

• Marking schemes

This is very serious claim and This need immediate attention.

Don't believe in any rumours untill it is confirmed by ICAI.

Waiting for official clarification from ICAI.

15

22

148

44,562

yash retweeted

Jun 16

This 1.25-hour podcast featuring Ashish Chug, hosted by @kushallodha548 , could be a game changer in your stock market investing journey.

I've listened to it twice, and I highly recommend it to all young investors.

youtu.be/_W-CNN3rcvY?si=_zxd…

1

24

124

11,031

yash retweeted

Jun 15

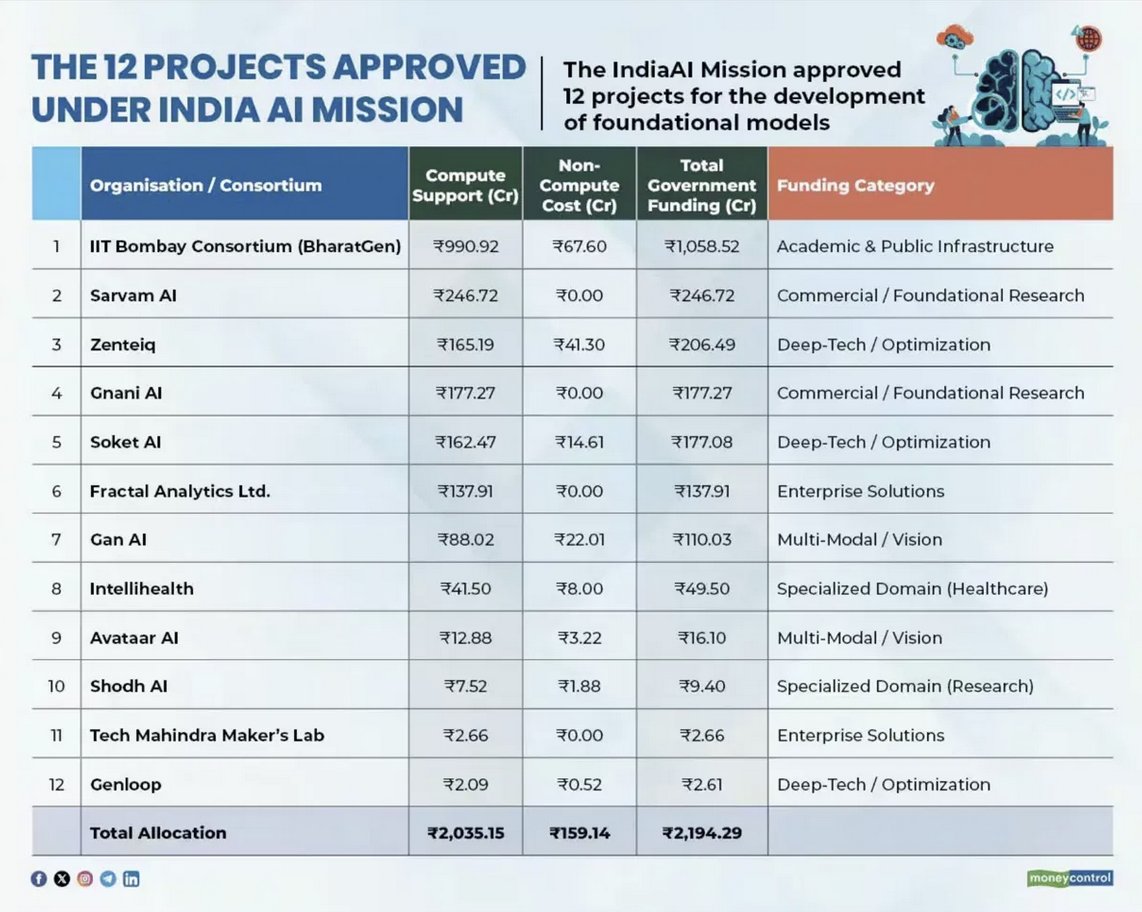

An Indian with deeper analytical approach, responded to my post on babus being responsible for Indian lack of progress in AI. From his list I left #1 and #3 alone coz they are an educational institutes. Although, I must say that for #3 (Zenteiq) with Rs 206 Crore funding, a static website with no information does not instill confidence.

My views on Sarvam being a Nandan brokered nepo enterprise are clear from my earlier posts. You can self device on why Tech Mahindra is getting this government funding, as the company is nothing but another body shop.

I went through rest of them and I am going to show you how all of them are actually a result of nexus between Babu and outsiders to fleece Indian taxpayers.

27

131

509

34,645

yash retweeted

🇮🇳|Heartbreaking scenes from #AndhraPradesh: Mango farmers are dumping their produce on the roadsides because prices have crashed so low that even harvesting, labour, and transport costs are not covered.

This is not a natural market failure. It is engineered destruction of small farmers.

HARSHER TRUTH WITH EVIDENCE:

The Andhra Pradesh government, under policies aligned with BILL GATES FOUNDATION, AMAZON, and WEF, is actively pushing corporate-controlled agriculture that squeezes small farmers out.

•- Gates Foundation MoU (March 2025): The state signed a formal agreement with the Bill & Melinda Gates Foundation for AI-driven precision farming, satellite-based systems, and data platforms in agriculture. This benefits big tech, seed/pesticide corporations, and supply chain giants while marginalizing smallholders.

Source: The Hindu - thehindu.com/news/national/a…

•- WEF C4IR Andhra Pradesh: The state partnered with the World Economic Forum for Fourth Industrial Revolution initiatives, including AI and digital transformation in agriculture that favour export-oriented corporate models over traditional farming.

Source: WEF initiatives and state announcements.

•- Corporate Retail Dominance (Amazon & others): Policies enabling big retailers and processors to control supply chains crush farm-gate prices through middlemen and contract farming, with no effective MSP protection for mangoes like Totapuri.

Governments take billions in the name of farmer welfare while implementing policies that hand control to global corporations. Farmers are left dumping their own harvest on roads while elites and their partners profit from the crisis.

This is deliberate, documented policy against the people ruthless consolidation of food control. Small farmers pay with their blood and sweat for the empire’s agri-tech agenda.

52

317

399

32,544

yash retweeted

Jun 14

A policy affecting 140 crore people; signed at 8PM, announced at a press conference the next morning.

No White Paper. No Parliamentary debate. No public consultation. No independent impact study.

Just a minister, a pen, and a family business waiting on the other side.

Let’s talk about what this “policy” actually is:

→ Son Nikhil’s company Cian Agro: ₹18Cr → ₹523Cr revenue in one year

→ Their stock: ₹37 → ₹638. A 2,184% surge; while “the file” was being drafted

→ Son Sarang: Director at Manas Agro. Also in ethanol. Also quietly booming.

Father writes the regulations. Sons hold the equity.

And we’re supposed to call this a “national dream.”

In any functioning democracy, a minister with direct family financial interests in a sector CANNOT unilaterally regulate that sector.

That’s not politics, that’s a constitutional principle.

Where is the Lokpal?

Where is the Prime Minister?

Where is the Parliament?

The dream isn’t about ethanol.

The dream is about a country where accountability has been fully, quietly, abolished.

#WATCH | Nagpur, Maharashtra: Union Minister Nitin Gadkari says, “Last night at 8 PM, I signed the file, finalising the regulations to legally authorise the use of 100% ethanol. I am delighted to share that I, along with Hardeep Singh Puri, had the opportunity to launch the 100% ethanol-compatible version of the WagonR—Maruti Suzuki’s best-selling car. Regarding motorcycles, Hero MotoCorp—which accounts for three out of every five motorcycles sold—has launched two flex-fuel models capable of running on 100% ethanol. Following this, companies like Toyota, Suzuki, MG, and Hyundai will launch 100% ethanol-compatible vehicles within the next month and a half. Thus, ethanol will serve as a viable alternative to petrol. People used to laugh when I spoke of this dream, and some friends even criticised it...Soon, we will launch a pilot project in Nagpur featuring a hydrogen pump and two hydrogen-powered buses. The public will be able to ride these hydrogen buses, which will be powered by green hydrogen extracted from water using an electrolyser. That day is now near.”

235

2,686

7,973

197,631

yash retweeted

Jun 15

Classic case of AI nonsense threads

SEBI mandated proposed uniform stock prices bands across exchanges and not prices !

@ETMONEY dont leave everything to interns !!

2

6

64

15,051

yash retweeted

🚨 A man got fined ₹500 at Kalyan station after his platform ticket expired while waiting for a train that got delayed 5 hrs.

Platform tickets cost ₹10 and let you stay on the platform for two hours. If you go over, you're supposed to buy another or face a penalty (₹250).

The incident has reignited discussions on railway regulations, with calls for fines on delayed trains.

(📷 -adityasinghchauhan01)

74

188

1,627

93,306

yash retweeted

Jun 15

2000 km Completed in 33 days and 23 Hours.

Running Across India from Kanyakumari to Karakoram

Not by talent.

Not by luck.

Just discipline, consistency, and showing up every single day.

Onwards to Karakoram.

#Day33 #RunAcrossIndia #RunForDreams #KanyakumariToKarakoram #tributetobravehearts

44

51

610

10,834

yash retweeted

Jun 15

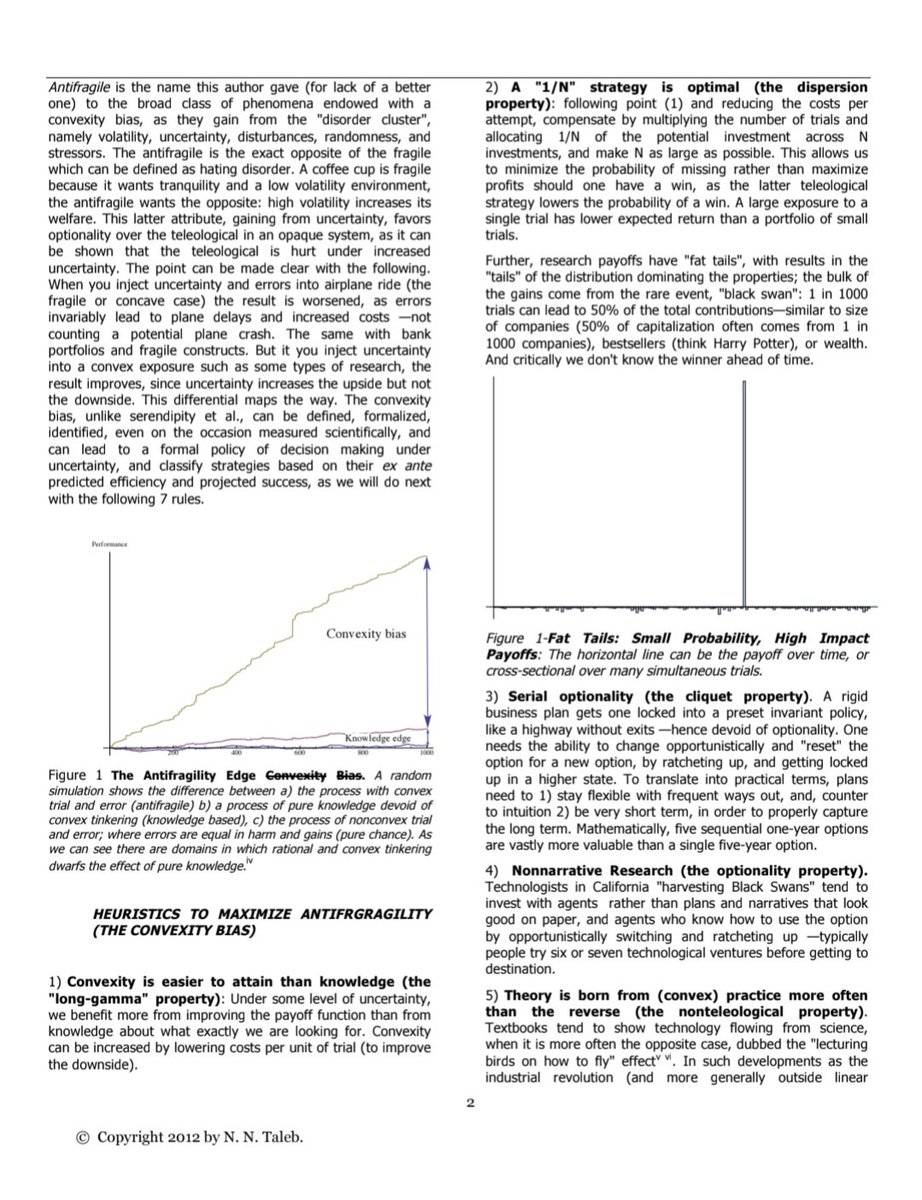

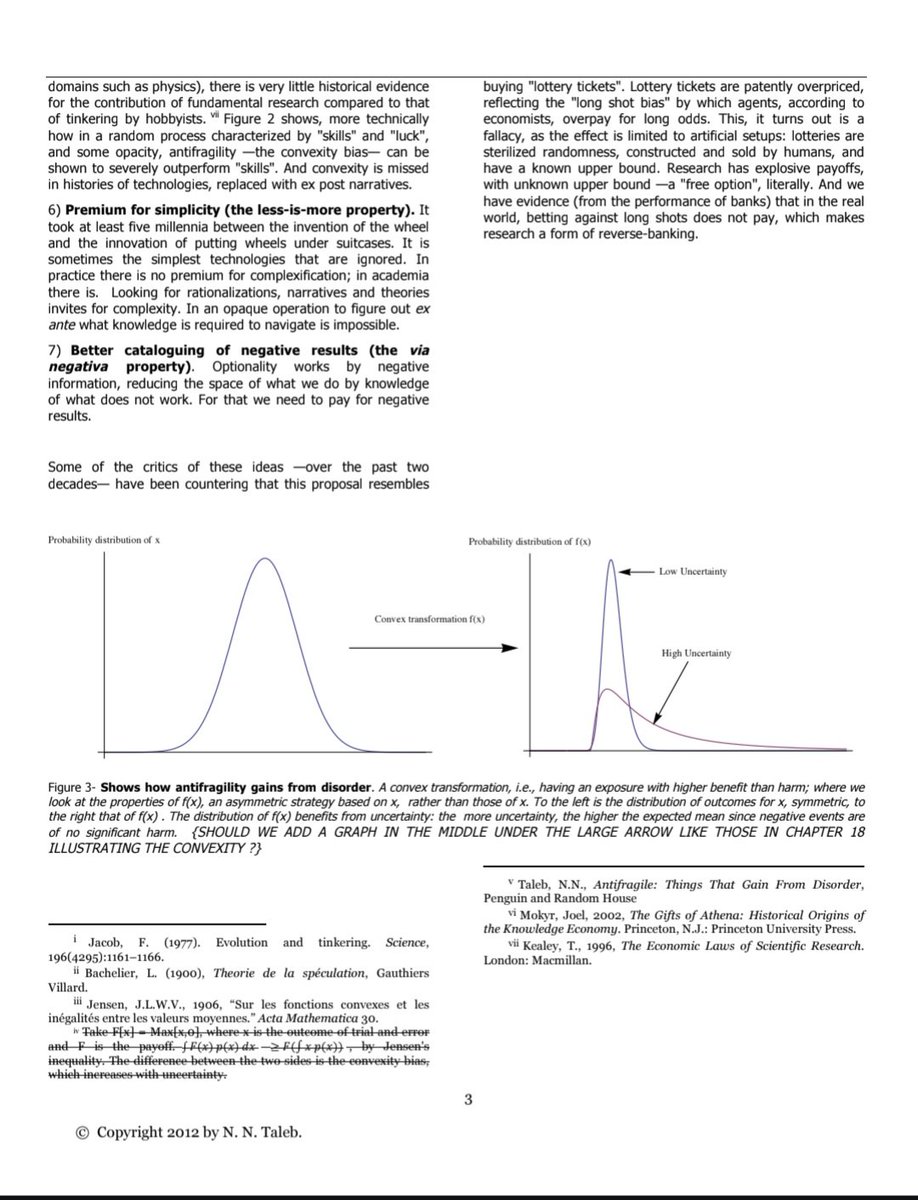

Created an infographic.

16 Sep 2025

2 years of MBA < Wisdom in these 3 pages.

1. Convexity

2. Antifragility

3. Optionality

4. Trial-and-error

5. Uncertainty

6. Payoff

7. Nonlinear

8. Tinkering

9. Heuristics

10. Asymmetry

Don't ruin the essence by asking ChatGPT to summarize it.

1

4

26

4,335

yash retweeted

6 years ago, we uploaded our first SOIC video.

No studio. No fancy setup. Just one belief: investing is a skill, and any skill can be learned.

People told us to make short videos and chase algorithms. Instead, we spent hours breaking down businesses, industries, valuations, and investing frameworks.

Honestly, we didn't know if anyone would watch.

More than 500,000 learners did.

To everyone who has watched a video, attended a webinar, enrolled in a course, or been part of this journey.

Thank you. This anniversary belongs to you. ❤️🙏

To celebrate our 6th anniversary, we're opening SOIC Membership at our best price.

Inside you'll find the entire roadmap to becoming a complete investor:

📌 Personal Finance

📌 Financial Statements, Ratios & Forensic Analysis

📌 Valuation, DCF, Bull/Base/Bear Scenarios & Portfolio Construction

📌 Entry & Exit Frameworks

📌 Stock Screening & Idea Generation

📌 Sector Deep Dives

Plus two bonuses: SOIC Market Signals and our AI Masterclasses for Investors.

✰ Anniversary offer pricing (Valid till 22nd June)

1-Year Membership — ₹13,499 (regular ₹18,499)

Coupon code: THANKYOU6

3-Year Membership — ₹26,499 (regular ₹33,499)

Coupon code: THANKYOU06

Pick your plan and apply your code here: learn.soic.in/learn/SOIC-Cou…

If you've been waiting for the right time to take your investing education seriously, this may be it.

Here's to the next 6 years of learning, compounding, and becoming better investors together.

📌 NOTE: Existing SOIC Membership learners can reach out to us at info@soic.in for the SOIC Membership Renewal Plans.

6

6

148

14,802

yash retweeted

Jun 15

The LPG crisis may have faded from the headlines. Its impact hasn't.

When cooking gas supplies dried up, the migrant truck drivers who keep Navi Mumbai's Jawaharlal Nehru Port moving could no longer afford to eat. Many left. Container backlogs surged from 17,000 to 40,000. Perishable cargo rotted. Union Ministers held emergency meetings.

Three months later, India's biggest container port is still counting the cost.

Do read @purnima_sah_'s excellent deep dive in today's edition.

indianexpress.com/article/ci…

4

170

246

13,097

yash retweeted

Jun 13

x.com/i/status/1989669273531…

TIME TO REVISIT AETHER INDUSTRIES (NOT ATHER ENERGY)

AETHER INDUSTRIES

Study shared @839 now 1150 🔥 🔥

[LINK SHARED HERE]

Time to Revisit,

After reading and updating my Notes, I still think many investors are still asking the wrong question.

❌ "What will next quarter's revenue be?"

The better question is:

✅ "What is Aether trying to become by 2030?"

🧵👇

Most investors see:

🧪 Specialty Chemicals

🧪 Pharma Intermediates

🧪 Agro Chemicals

That's the past.

Management is building something much bigger.

Think about this.

Aether doesn't want to be a company that simply sells chemicals.

It wants to become a company that global innovators call first when they need:

✔ Research

✔ Scale-up

✔ Process Development

✔ Commercial Manufacturing

✔ Long-term Strategic Partnership

Huge difference.

The biggest clue?

Management's long-term vision.

🎯 70% Revenue from CRAMS Exclusive Manufacturing

Only 30% from traditional manufacturing.

Why does this matter?

Because the biggest wealth creators are not companies that manufacture products.

They are companies that become indispensable.

And now comes the interesting part.

🌍 Europe is struggling.

⚡ Energy costs remain elevated.

🏭 Manufacturing competitiveness has weakened.

Global chemical companies are actively looking for trusted partners.

And Aether is positioning itself exactly there.

Not as a vendor.

As a partner.

Most people are discussing Baker Hughes.

I am looking beyond Baker Hughes.

Most people are discussing Site 5.

I am looking beyond Site 5.

Most people are discussing FY27.

I am looking at FY30 in the long run. (Obviously going through mngmt updates)

Site 5 is not just another plant.

It is the bridge to the next phase.

🚀 New products

🚀 Semiconductor chemicals

🚀 Electronic chemicals

🚀 Material science opportunities

🚀 Exclusive manufacturing contracts

Quietly.

Without much noise.

Now ask yourself:

How many Indian chemical companies are talking about supplying semiconductor-related chemicals to customers in:

🇯🇵 Japan

🇰🇷 South Korea

🇹🇼 Taiwan

NOT MANY.

The most fascinating thing?

Management isn't expanding only factories.

They're expanding intelligence.

🔬 New labs

🔬 New engineering capabilities

🔬 Advanced analytical infrastructure

🔬 Massive R&D expansion

Because tomorrow's moat won't be capacity.

Tomorrow's moat will be complexity.

And complexity creates pricing power.

Pricing power creates margins.

Margins create cash flows.

Cash flows create compounding.

(YE TO RHYMING HI GYI) 😃

Of course, risks exist. 🔴

⚠️ Working capital remains high.

⚠️ Debt will rise.

⚠️ Capex execution must be flawless.

⚠️ Customer concentration must be watched.

No serious investor should ignore these.

But here's what keeps me interested.

The company isn't behaving like a chemical manufacturer.

It's behaving like an innovation platform.

And markets often take years to recognize that transition.

The market still values Aether based on chemicals sold.

I think the future value may come from problems solved.

And there is a very big difference between the two.

Sometimes multibaggers don't emerge because earnings suddenly explode.

They emerge because investors slowly realize:

"This business is not what we thought it was."

Aether may be entering that phase.

🚀🧪📈

DISCLAIMER = THIS IS NOT A BUY OR SELL RECOMMENDATION. SHARING ONLY FOR STUDY PURPOSES.

MORE DETAIL STUDY IN CLOSED GROUP.

REMEMBER @SHAREPURANA FOLKS, YOU ALL HAVE ONE OF THE POWERFUL TOOL.

#AetherIndustries #Chemicals #CRAMS #Manufacturing #IndiaGrowthStory #Investing #StockMarket #Multibagger #SharePurana 🔥💎🚀

15 Nov 2025

1️⃣ What if I told you…

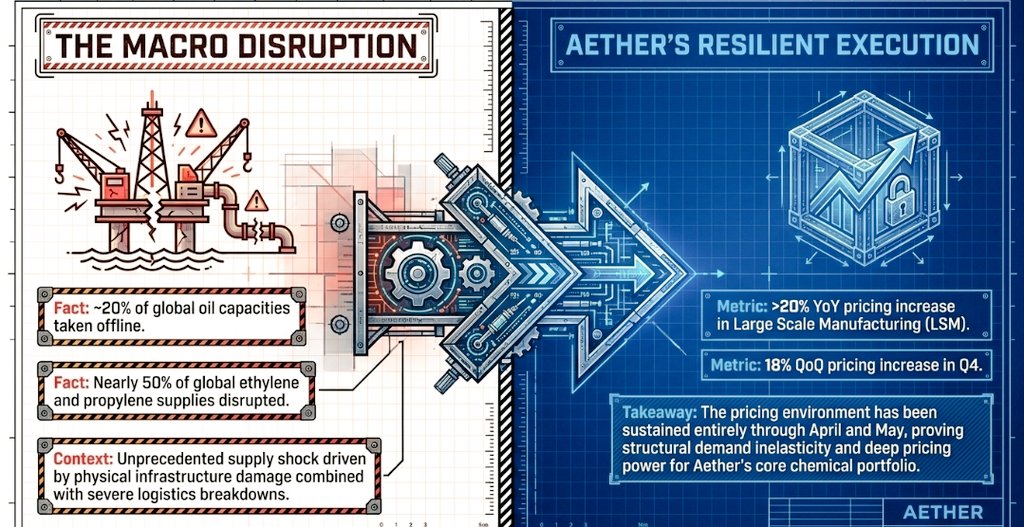

One specialty chemical company in India just delivered a quarter that looks better than most global peers?

Meet #AetherIndustries @ cmp839 a silent compounder that just entered a new growth cycle.

[MORE DETAILED STUDY SHARED IN CLOSE GROUP ONLY]

Let’s decode Q2 FY26 in the simplest way possible.👇

2️⃣ First, the headline number:

📌 Revenue up 38% YoY

📌 EBITDA up 70% YoY

📌 PAT up 55% YoY

And the best part?

Margins expanded sharply.

This isn’t a recovery…

It’s a transformation.

3️⃣ What changed?

Aether is shifting from:

⚪ Low-value molecules →

🔵 High-value Contract Exclusive Manufacturing (CEM)

🔵 High-end CRAMS (Contract Research & Manufacturing Services)

This alone is rewriting the company’s economics.

4️⃣ Revenue Mix Now:

🔹 48% CEM (highest ever)

🔹 9% CRAMS

🔹 41% LSM (Large Scale Manufacturing)

CEM CRAMS = 57%

Last year it was ~42%.

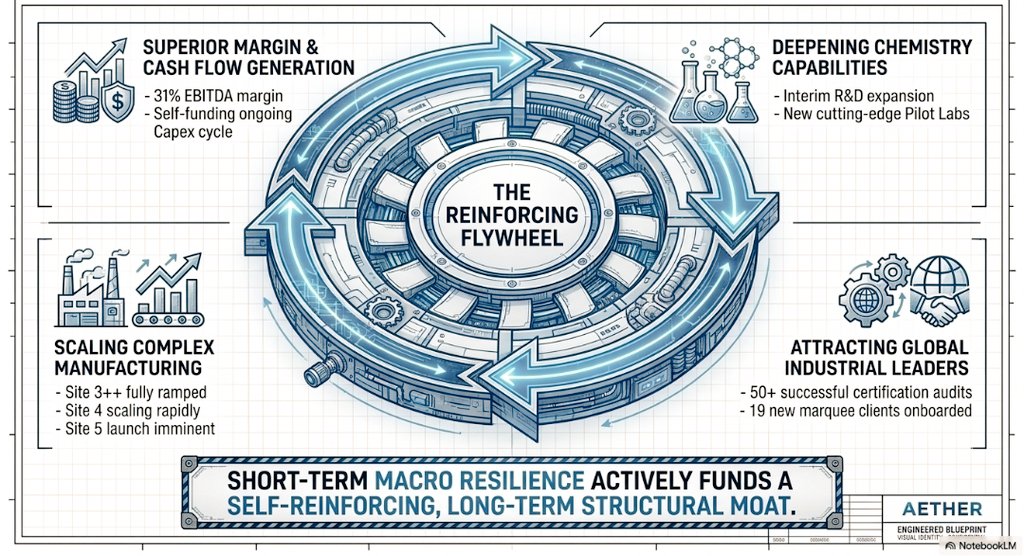

That is the real reason margins touched 31%.

5️⃣ Why does CEM matter so much?

Because CEM =

✔ Long-term locked contracts

✔ Higher entry barriers

✔ Sticky customers

✔ High margins

✔ Global clients trusting you with sensitive molecules

This is where global specialty giants make money.

Aether is stepping into that zone.

6️⃣ Segment Mix is also interesting:

📌 Pharma – 36%

📌 Material Science – 19%

📌 Oil & Gas – 19%

📌 Agro – 13%

This diversification is rare.

No single sector risk.

The more pharma & material science grow →

the more stable margins become.

7️⃣ Biggest trigger? Expansion.

The company is preparing for the next 3–5 years of growth right now:

🏭 #Site5: Two new blocks → commissioning Q4 FY26

🏭 #Site3 : New CEM products → tied with US-based giant Milliken

🔬 R&D spend 7.23% of revenue → among highest in India

Aether is NOT expanding capacity randomly…

It is expanding after securing demand.

8️⃣ Profitability is cleaner than you think.

PAT margin is now touching 18% -

numbers you normally see in global specialty leaders.

9️⃣ The only red flag (and it’s temporary):

Heavy capex.

Working capital tightness.

Cash flow negative this year.

Why?

Because the company is building capacity for the next few years.

This is growth capex, not stress capex.

🔟 So what’s the bigger picture?

Aether is evolving from a chemical manufacturer →

to a deep-tech specialty partner for global clients.

This is the exact path followed by:

🔹 #PIIndustries (a decade ago)

🔹 #Divi’s Lab (two decades ago)

Both became long-term wealth creators.

1️⃣1️⃣ Future Return Potential (Educated Guess):

If earnings grow 20–25% CAGR (current trajectory):

📌 Stock can deliver 18–25% CAGR over 3–5 years.

If CEM blocks scale faster:

📌 Could be even higher.

Aether is not a “quick trade” stock.

It’s a slow compounding machine in the making.

1️⃣2️⃣ What investors should actually focus on:

✔ CEM mix rising

✔ Site 5 & Site 3 commissioning

✔ Pharma Material Science contribution

✔ Margin stability

✔ Client additions in US & EU

If these remain on track →

the stock will take care of itself.

1️⃣3️⃣ The real learning:

In specialty chemicals…

“You don’t chase companies that make chemicals.

You chase companies that make chemistry difficult for others to copy.”

Aether fits that mould.

1️⃣4️⃣ Final Word:

Aether isn’t the loudest company.

It doesn’t trend on Twitter.

It doesn’t appear in influencer reels.

But quarter by quarter…

it’s quietly turning into a specialty chemicals powerhouse.

Long-term stories are built exactly like this.

Disclaimer:

Educational thread only.

Not a buy/sell recommendation.

Consult your financial advisor before investing.

4

3

478

yash retweeted

Jun 14

We are fucked up badly with health & habits 🤐..

IVF sector in India is experiencing a massive structural boom, Indian IVF market is projected to grow from ₹11000 crore to over ₹40,000 crore by 2034, with CAGR of over 16%.

Bata drugs,Apollo,Rainbow, and hundreds of startup going aggressively in this.

Very new and interesting theme

Read,reserach and invest early.

#Gaudium IVF

1

6

39

8,689

yash retweeted

Jun 14

#SenoresPharma

FY 26 is Breakout Year

Revenue is up by 62%

EBIDTA is up by 96%

PAT is up by 108%

Management guidance is 30-40% Revenue and 50-60% PAT Growth in FY 27

I had earlier , But now !

2

3

88

7,591

yash retweeted

Jun 14

First Identify the "parts" that will deteriorate fast in the vehicle after "using 100% ethanol".

Identify the company(s) who will be manufacturing these "parts"

With my limited knowledge, i understand that "Engine" and "Pistons" in petrol and diesel cars will be affected immediately.

Jun 14

GADKARI APPROVES LEGAL USE OF 100% ETHANOL, CALLS IT A MAJOR ALTERNATIVE TO PETROL

INDIA CLEARS 100% ETHANOL FUEL AS AUTOMAKERS PREPARE TO LAUNCH COMPATIBLE VEHICLES

TOYOTA, SUZUKI, HYUNDAI AND MG TO ROLL OUT 100% ETHANOL-COMPATIBLE CARS AFTER POLICY APPROVAL

33

14

229

54,264

yash retweeted

Imagine the corruption!!

They are replacing perfectly fined footpath tiles with new one was there was no need for it so many places so don't even have footpath

Babus wont spare even 1 ruppes of corruption.

Location-delhi (What is the reason?? )

@DelhiPwd @CMODelhi @PMOIndia

27

110

863

17,675