Joined February 2021

- Tweets 8,249

- Following 840

- Followers 411

- Likes 116,285

1,389 Photos and videos

PosableActionFigure retweeted

Jun 2

946

1,971

8,746

569,444

PosableActionFigure retweeted

Next move - apply for this job, post about the application & interview experience & put it all on record in a 425 filing. 😂

4

4

87

1,394

PosableActionFigure retweeted

I pay my taxes.

You pay YOUR taxes.

If we don't pay our taxes, its simple: You get fined, or you go to jail.

Unless you name is trump: He, and his family, were somehow just given blanket pardons for any and all tax crimes -- past, present or future.

THIS IS A HUGE SCANDAL.

881

10,591

29,419

283,185

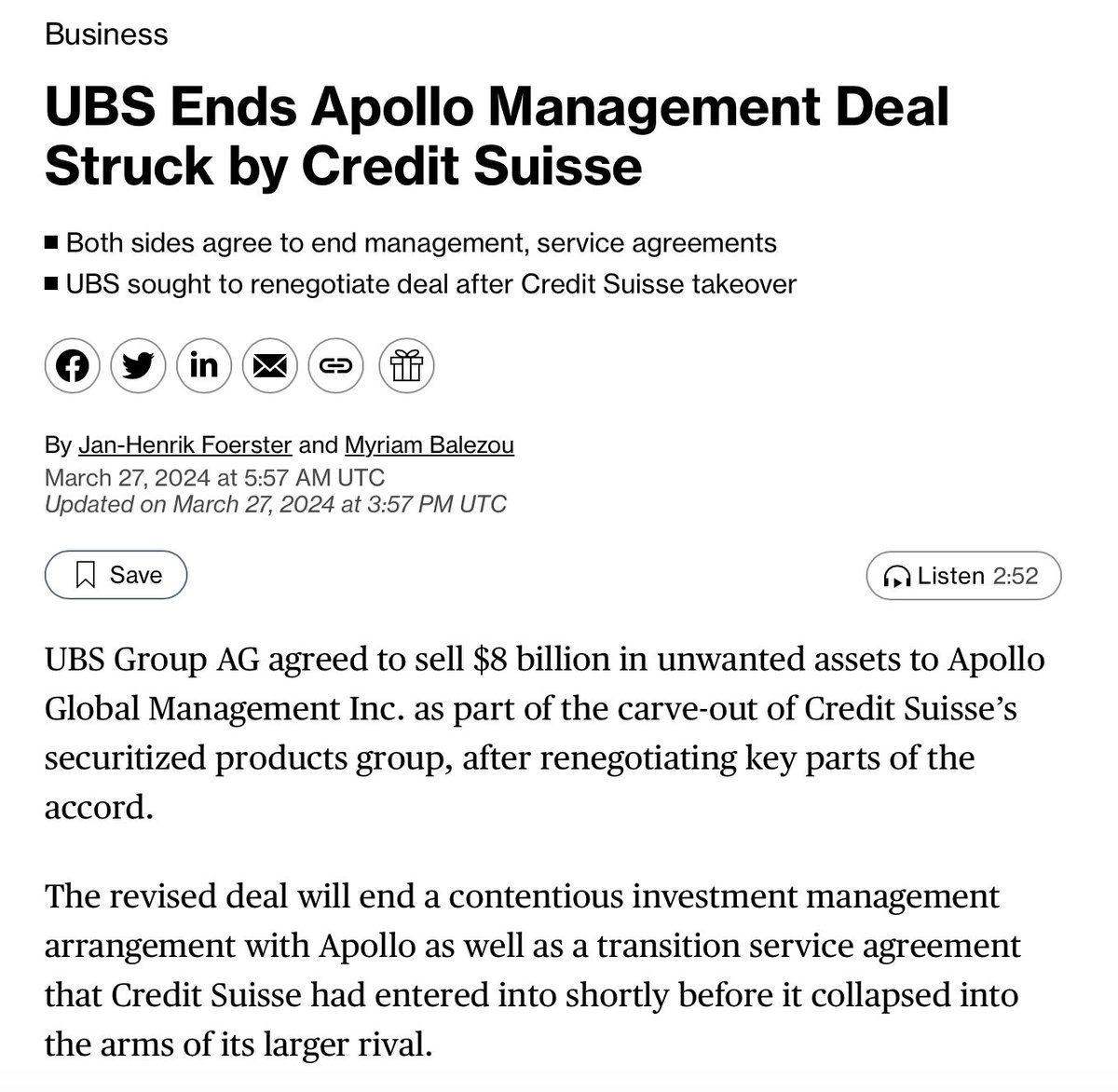

The Federal Reserve just terminated enforcement actions against UBS Group AG and Credit Suisse over the Archegos stuff.

It's totally confirmed... we live in a fraudulent market! $GME

2023: UBS swallows dying Credit Suisse and inherits the entire toxic sludge.

March 2024: UBS ends the Apollo management deal and dumps $8 BILLION in “unwanted assets” from Credit Suisse’s Securitized Products Group straight to Apollo.

The bag was officially passed.

22

146

517

57,337

PosableActionFigure retweeted

May 13

FULL INTERVIEW: @ryancohen explains his plan to acquire eBay.

He unpacks his pitch to institutional investors, why eBay is so horribly run, and how Ryan plans to create billion in shareholder value.

$GME $EBAY

352

1,074

5,327

676,744

PosableActionFigure retweeted

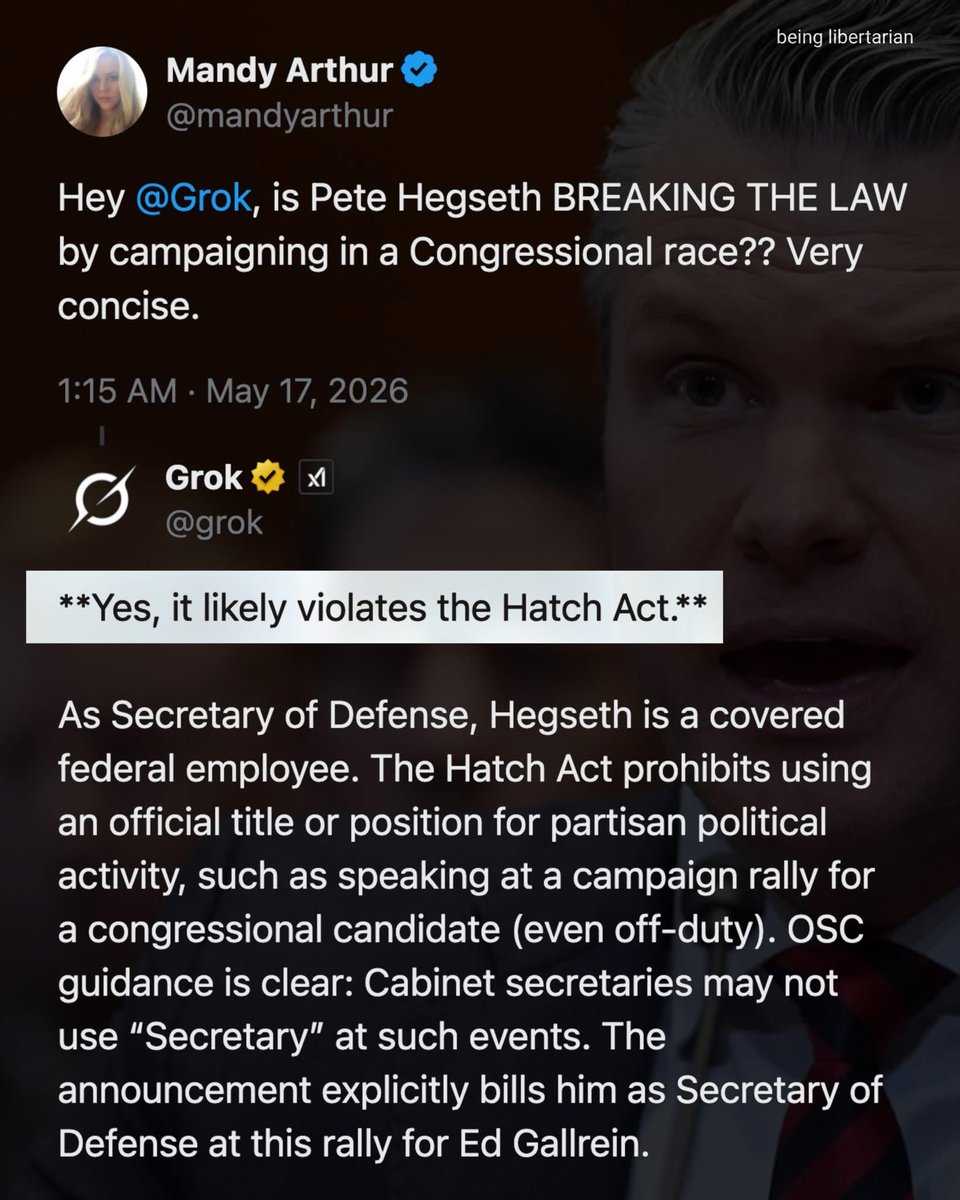

It's kinda suspicious that a group of billionaires are spending 10s of millions of dollars trying to unseat a single Republican Congressman from Kentucky who just happens to be one of the few members of Congress that refuses to be a puppet of a foreign nation.

116

1,658

11,060

69,814

PosableActionFigure retweeted

May 12

How much crisis must a company have to necessitate an entire FTE named “Head of Financial & Crisis Communication” @eBay @ryancohen

1

2

54

2,292

PosableActionFigure retweeted

May 12

In light of $EBAY rejecting the $GME offer this morning against their fiduciary responsibilities, let's take a look at Paul S. Pressler, the board Chair, who is a shining example of what failing upwards looks like in corporate America.

He has been a director since 2015. Chairs the Corporate Governance & Nominating Committee. Has been Chairman of the Board since 2020.

He was present throughout the 2019 stalking crimes, and now sits as Chairman of the full board. In 2019, he chaired the Compensation Committee, making him central to one of the most controversial decisions in the company's history: a board meeting was convened specifically to consider whether to activate the clawback provision on Devin Wenig's exit package, and the board voted not to proceed. That package was worth approximately $57 million. During a September 2024 deposition in the civil litigation, eBay's Director Ethics Counsel testified under oath that Wenig's departure was a firing, not a resignation, and that it was directly related to the stalking scandal. Despite this, the board publicly framed the exit as a mutual decision for months, a characterization that governance critics argue constitutes a material misrepresentation to investors.

Pressler's committee also oversaw a quiet exit for former SVP Wendy Jones, who was interviewed by eBay's internal investigators on August 30 and September 6, 2019 in connection with the criminal conduct and was nonetheless allowed to remain employed through December 2020. Jones ultimately received compensation packages totaling over $11 million upon her eventual departure. Pressler became Chairman in May 2020, taking the seat from outgoing Chairman Thomas Tierney immediately after those decisions were made.

The board waited until February 26, 2026 to reform its committee charters governing risk, audit, governance, technology, and compensation. That restructuring happened one day after the Steiners' civil lawsuit settled with undisclosed terms. eBay had not restructured governance at any point after the crimes became public in 2020, after entering a federal deferred prosecution agreement admitting to six felony offenses in January 2024, or at any time while the civil trial was pending. Critics at the time noted that reforming governance while litigation was active could have made those drafts discoverable and usable as evidence by the plaintiffs' attorneys. Pressler, as Chairman, would have been the chief architect of that timing decision.

Currently, Pressler chairs the Corporate Governance and Nominating Committee, the same committee that oversees Aaron Johnson, eBay's Chief Ethics Officer. Johnson was copied on the August 2019 "Whatever. It. Takes." email from then-Communications Chief Steve Wymer before the crimes occurred. His promotion to lead company ethics, under Pressler's oversight, has drawn sustained criticism from governance observers.

Before joining eBay's board, Pressler served as President and CEO of Gap Inc. from 2002 to 2007. Former employees interviewed by BusinessWeek characterized his tenure as "total system failure." Gap recorded its third consecutive dismal holiday shopping season under his leadership, and the board moved to remove him in January 2007 after months of investor pressure and public calls for his ouster from Wall Street. Founder Don Fisher had publicly defended Pressler in the months before the termination, but the defense did not hold. The board's post-departure statement that it needed someone with "deep retail expertise" was widely read as a direct indictment of Pressler's qualifications for the role. His exit triggered immediate speculation about a sale of the company. He collected $14.5 million in severance.

Pressler served as Chairman of David's Bridal from 2012 to approximately 2018, during the period when the company was owned by private equity. By the time of his departure, David's Bridal carried approximately $760 million in debt. The company filed for Chapter 11 bankruptcy in November 2018 to restructure over $400 million of that obligation. It subsequently filed for bankruptcy a second time in April 2023, this time laying off more than 9,200 employees with no funds expected to be available to unsecured creditors. The structural financial condition of the company at the time of its first bankruptcy was built during Pressler's chairmanship.

As an eBay shareholder myself, I am calling for Paul Pressler to resign immediately. No golden parachute either.

35

237

1,177

38,274

PosableActionFigure retweeted

Feb 26

Prepare yourself for a proposition from $GME to increase the total authorized share count. I know that might make some of you uncomfortable, but hear me out because there's a very logical reason this is coming, and it's actually bullish. If you disagree or hate this idea, please give me the courtesy of reading my logic before you have a mid-life crisis in the comments.

Right now, GameStop has ~448m shares outstanding against 1bn authorized. That's a 44.8% issued-to-authorized ratio. Sounds like plenty of headroom, right? Not when you factor in what's already committed:

- 171.5m shares tied to RC's performance options

- ~43.5m shares from the $1.3Bbn convertible notes ($29.85 strike)

- ~77.8m shares from the $2.25bn convertible notes ($28.91 strike)

That alone brings the fully diluted count to ~741m, or 74% of the authorized ceiling. And that's before a single acquisition dollar gets raised.

So why would RC want to increase the limit now, while there's still room? Because good capital allocators do not wait until they are maxed out. They plan ahead, and there is clear precedent for this.

RC has shown you exactly how he thinks about this.

In January 2023, RC built a stake worth several hundred million dollars in Alibaba and personally pushed management to increase their buyback program from $40bn to $60bn. He told them they could hit double-digit sales growth and ~20% FCF growth over five years, but the shares were undervalued and the buyback was not aggressive enough. Alibaba listened and expanded the program.

He also invested the vast majority of his personal wealth into Apple after selling Chewy, becoming one of Apple's largest individual shareholders (roughly $800m plus at peak). When sources close to RC described his Alibaba thesis to Reuters and the Wall Street Journal, they specifically pointed to Apple's capital return program as the blueprint RC wanted Alibaba to follow. RC called Apple “the strongest business in the world” and cited “disciplined capital allocation” as a core investment principle he learned from Buffett. He bought his first Apple share at age 15.

The through-line here is pretty clear to me: RC is acutely aware of shareholder value mechanics, issued-to-authorized ratios, and capital discipline. He does not want to be forced into raises when his back is against the wall. He would rather have optionality.

Buffett operated the exact same way, and there is direct precedent here. Berkshire Hathaway has 1.65m Class A shares authorized but only roughly 523,000 outstanding. That is a 31.7% utilization rate, and Buffett has maintained that kind of headroom for decades. He did not do that because he planned to flood the market with stock, but because he wanted the flexibility to act when opportunity appeared without going back to shareholders for emergency approvals.

At the 1995 Berkshire annual meeting, when shareholders questioned whether authorizing preferred stock would dilute them, Buffett said: “There is no downside to this proposal. It is an authorization. It is not a command to issue shares.” He also explained that shareholders are only diluted if Berkshire receives less in value than it gives, and he repeated that principle in multiple letters and Q&A sessions over the years. In later commentary he went so far as to say he would “rather prep for a colonoscopy than issue Berkshire shares,” underscoring how seriously he treats actual issuance versus simple authorization. The lesson is simple: Buffett authorized far more shares than he ever used, kept massive headroom at all times, but was extremely disciplined about when and why he actually issued stock. That is the model RC appears to be following.

Now let's do the math on what $100bn plus actually requires.

RC has told us the plan: acquire a publicly traded consumer company “significantly larger” than GameStop. He has described it as “transformational” and said this has “never been done before in the history of capital markets.”

GameStop currently sits at roughly $11bn market cap with roughly $8.8bn in cash. To get to $100bn by 2036 (the 10 year horizon of his compensation plan), he is going to need significantly more capital than what is on the balance sheet today. My estimate: at least another $20bn in equity and debt capital over the next 3 to 5 years. And honestly, that might be conservative if the vision is $100bn to $500bn.

Think about it through the lens of how the Mag 7 plan their growth. Meta, Google, Microsoft, Amazon, they are each telling shareholders and the market they are spending $60bn to $80bn per year for the next 3 years on AI infrastructure. They are planning capex 2 to 4 years out and asking for patience. The market rewards that kind of forward planning.

Now apply that same thinking to GameStop. This is not capex, but the principle is the same: how much capital does RC need to build a $100bn to $500bn conglomerate? The answer is: a lot. And it needs to come from a combination of cash flowing acquired businesses that can generate $4bn to $5bn per year, plus accretive equity raises and creative debt instruments (like those 0% converts).

If you assume $20bn in additional equity raises at an average price of roughly $25 per share, that is roughly 800m new shares. Add that to the 741m fully diluted count and you are at roughly 1.54bn shares, well past the current 1B authorized limit.

If RC wants to hover around a 60 percent issued-to-authorized ratio (which, based on his Alibaba and Apple track record, seems like a reasonable mental ceiling), he would need authorization for roughly 2.5bn to 3bn shares. My guess is we will see a proposal for 2bn to 3bn, likely the latter.

Here is the key point most people miss: increasing the authorized share count is not dilution. It is giving the board the legal runway to execute over a multi year period. Dilution happens when shares are actually issued, and RC has shown through his $35bn all or nothing compensation plan that he only wins if the stock goes up. His 171.5m options are worthless unless GameStop hits $100bn in market cap and $10bn in cumulative EBITDA. Every share he issues needs to be accretive to that goal or he is lighting his own paycheck on fire.

It takes money to buy whiskey. You do not build $100bn plus companies without capital. And it is far better to ask for authorization now, while utilization is at roughly 45%, than to come back begging when you are at 90% and the market reads it as desperation.

This is forward planning. This is the Berkshire playbook. Do not let it scare you.

125

255

1,559

191,436

PosableActionFigure retweeted

May 10

Part 3: The (MOASS)

Cohen told CNBC: “It’s similar to Berkshire Hathaway, except what Berkshire did in decades we’re attempting to do in a much shorter time.”

The most valuable stock in history. $600,000 per A share.

Nothing above it.

He picked the absolute upper boundary of the stock market and said:

‘that, but faster.’

For 5 years the community defined MOASS as the Mother of All Short Squeezes.

Cohen has never said squeeze.

He said Berkshire.

A structure, not an event.

2025 — Fuck Your Gamma Ramp

Converts: ~$4.2B at 0% interest. Conversion at $29.85 / $28.91.

Zero-yield bonds.

Buyers are being paid in something else.

Warrants: 1:10 ratio. $32 strike. Oct 30, 2026. Cash exercise only. ~59M warrants. $1.9B potential proceeds.

Comp package: 171.5M options at $20.66. Nine tranches, dual hurdles.

First tranche: $20B mkt cap $2B cumulative EBITDA.

Full vest: $100B mkt cap $10B EBITDA. No salary. No bonus. Zero guaranteed pay.

Now layer it.

Converts at ~$29.

Warrants at $32.

Comp milestones scaling $20B → $100B.

Each instrument is a price level.

Each level is an obligation for shorts.

Each obligation, when triggered, generates capital that compounds the business beneath it.

Not a spike.

A infinite staircase.

Every step higher than the last.

For 5 years retail screamed about gamma squeezes on weekly options and kitty memes.

@ryancohen built one himself.

59M warrants at $32 — MMs must hedge as delta rises near strike.

Converts force hedging into $29. Comp tranches above $20B trigger more.

Self-reinforcing. Structural. Sitting in public filings.

And it might not be one ramp.

DK-Butterfly’s §382(l)(5) NOL freeze expired Sept 29, 2025.

Eight days later — Oct 7 — GME warrants distributed.

The exact same day, Beyond Inc. (operating as BBBY) distributed its own warrant dividend.

BBBYW. Same 1:10 ratio.

Same cash-exercise-only.

$15.50 strike — exactly half of GME’s $32. Oct 7, 2026 expiry.

Filed under CUSIP 075896159 — legacy BBBY issuer code, not Beyond’s.

You couldn’t distribute before Sept 29.

Warrant trading creates ownership changes that trigger a 2nd change of control and zero out the NOLs.

Distribution happened the first business week it was legally safe.

And BOTH on the same day just doesn’t happen.

Beyond is opening physical BBBY stores through Brand House Collective. That’s COBE — Continuity of Business Enterprise. The §382 requirement to preserve NOLs.

Staggered expiries:

BBBYW Oct 7.

GMEWS Oct 30.

Same distribution day = simultaneous pressure onset.

Staggered expiries = cascading resolution.

I’m not saying Cohen designed this exactly.

I’m saying the instruments exist, the mechanics are what they are, and the timeline maps to NOL preservation with 8-day precision.

Buffett never had counterparties with infinite loss exposure trapped underneath a structural gamma ramp built into his own capital stack.

Cohen took the Berkshire playbook and added something Buffett never needed.

Berkshire is the most valuable stock in history. Cohen can’t say “we’re building something bigger.” He’d be dismissed.

So he names the highest reference that exists and says: that, but faster.

But MOASS has no ceiling.

Short selling carries infinite loss.

Build a compounding machine with a structural gamma ramp on a deadline, and there is no mathematical upper bound.

Berkshire is the upper boundary of what Cohen can say.

It’s not the upper boundary of the play.

MOASS was never a squeeze.

He built it instrument by instrument, filing by filing, brick by mother-fucking brick while everyone watched.

Then went on national television and told you.

The actual upper boundary doesn’t have a name yet.

I’m going to give it one.

The (Moon)

19

40

266

25,118

PosableActionFigure retweeted

Power to the players just met power to the sellers & it looks to be the beginning of a beautiful friendship.🤝

GameStop CEO @ryancohen takes eBay pitch direct to sellers sharing vision for the platform with Flipwise co-founder Justin Glow.

$EBAY $GME

valueaddedresource.net/ryan-…

30

188

924

21,749

PosableActionFigure retweeted

Ryan Cohen's full interview with @cvpayne today discussing GameStop's ambitious acquisition of eBay

69

450

2,333

148,510

PosableActionFigure retweeted

May 5

That’s the key point from Ryan Cohen’s interview. He explicitly said equity is going to be rolled into both GameStop and eBay shareholders. That rules out a standard acquisition.

This is Teddy. There’s really no other clean way to interpret that kind of language.

DK-Butterfly is the obvious vehicle, use it as the holdco, preserve the NOLs, and run a reverse merger that pulls both GameStop and eBay into the same umbrella. End result is one combined company, Teddy.

From there, the equity split basically falls into place:

51% to legacy BBBYQ (required)

~19.4% GameStop (40% of the remaining 49%)

~29.4% eBay (60% of the remainder)

Consolidation. Everyone rolls equity into the same structure and comes out owning pieces of the new combined entity.

104

251

1,223

140,129