Advocate for consumer financial protections. Director of Financial Services, Consumer Federation of America. Otherwise, reading working on my serve. OmO!

Joined May 2020

- Tweets 1,150

- Following 889

- Followers 574

- Likes 320

47 Photos and videos

Apr 22

Literally, I have heard from banks that they are scared about having an #SPCP, or even not calling in existing loans. For opponents of "regulatory overreach," the #CFPB's radical #ECOA final rule is a prime example of a regulator telling banks how to lend. consumerfed.org/press_releas…

1

420

Apr 14

So, OpenAI is buying a personal financial management tool (#pfm). Wouldn't it be nice if there were a rule giving people personal #financial data rights? Like a #cfpb #Section1033 rule? pymnts.com/acquisitions/2026…

1

2

71

Feb 17

To the @WhiteHouse claim that the #CFPB costs consumers billions... the cost of regulation is: your car comes with brakes, those brakes meet safety standards, someone inspects them, and car companies pay a price when they manufacture dangerous vehicles. @consumerfed

1

7

106

Feb 17

If the White House's critique is that the #CFPB costs consumers money, why has it reversed $19 billion in CFPB-granted relief for consumers this year?

4

11

411

Feb 10

The #Bitsika card perfectly illustrates how some #fintechs and their partner banks see KYC evasion as a product differentiator. They add risk across the #payments ecosystem. bitsika.com/

1

3

347

Adam Rust retweeted

Feb 9

This is such an important connection.. linking BSA and consumer protection feels like a real path to stopping harm and getting victims actual redress. Great work pushing this forward.

1

22

Feb 10

Yesterday, @SenWarren @SenatorDurbin @ChrisVanHollen @RepPressley @RepCasten stood with advocacy groups & the @NTEUnion to #DefendCFPB. They know Congress represents people, not billionaires. Thank you for your leadership for the #CFPB. @BorrowerJustice @RealBankReform

🚨LIVE NOW: 1 year after the Trump Admin took over the CFPB @SenWarren @SenatorDurbin @ChrisVanHollen @RepPressley @RepCasten & @SenSchumer are joining us to say #DefendCFPB and #BorrowersNotBillionaires!

📺 WATCH: youtube.com/live/JUnEBdoCh_E

28

Jan 28

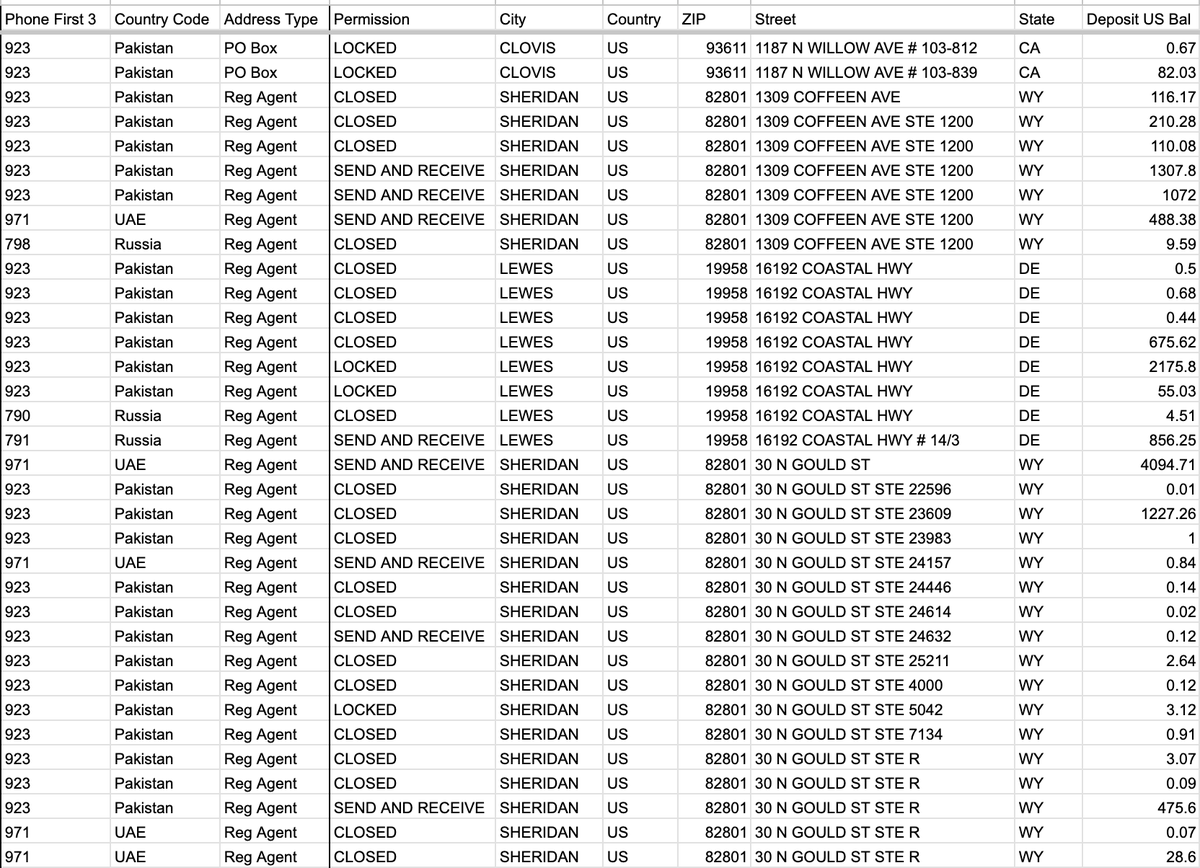

I have a new paper out today calling for greater linkage b/w BSA work against #IllicitFinance & #ConsumerProtection enforcement efforts to fight #scams. This is an opportunity for victims to receive redress. Do you know about funnel accounts? Learn more by reading my paper!

New paper from CFA examines the dramatic rise in #fraud & #scams and calls for closer coordination between consumer protection and the policing of illicit finance. By @AdamRust9

consumerfed.org/press_releas…

1

1

3

236

Jan 22

About to enjoy the @ncbudgetandtax Economy For All Summit .ncbudget.org/econ4all?snw=2&…

1

40

Jan 13

Notwithstanding that a #ratecap cannot occur without congressional action, limiting such a change to one year effectively requires deferred-interest cards for everyone. The main takeaway should be that financial services expenses need to be a part of the #affordability agenda.

41

Jan 13

Notwithstanding the Qs of if a #creditcard cap can be done by fiat (it can't), and if 10% is the right price...I hope the idea that costs for financial services are as much a part of the #affordability agenda as the price of eggs, rent, and transportation.

25

Jan 12

I'm kind of let down by Wall Street penalizing #creditcard banks today; usually, the wisdom of crowds leads to a more realistic analysis. Suffice to say, Congressional action, rulemaking, and court injunctions won't be done by next Tuesday.

25

Jan 6

So, when are the hearings to consider Stuart Levenbach's nomination to lead the #CFPB? consumerfed.org/press_releas…

1

209

16 Dec 2025

I enjoyed speaking this morning on personal #financial #data sharing & #Section1033 with @jpmorgan @fintechassoc and @PNCBank @bankpolicy and @thehill at "Modern Money: The Next Chapter of #Banking, #Regulation, and Financial Trust." #fintech #privacy #cfpb @consumerfed

16 Dec 2025

Now a panel on consumer data & open banking—examining how access, security, and innovation intersect—with:

- Natalie Talpas (EVP, @PNCBank),

- Kate Prochaska (MD, @jpmorgan),

- Adam Rust (@ConsumerFed)

- Angelena Bradfield (@FinTechAssoc).

#TheHillEconomy x.com/i/broadcasts/1Yqxolrpg…

2

5

163

19 Nov 2025

Government-by-loophole serves the interests of no one except those who want to evade the law. #CFPB #nomination #RussVought #Levenbach americanbanker.com/news/trum…

3

76

19 Nov 2025

If you understand kelp forests, you know what you need to know on FCRA, EFTA, and at least 16 other #consumerprotection laws. Right? americanbanker.com/news/trum…

1

2

63