Joined August 2019

- Tweets 463

- Following 306

- Followers 2,578

- Likes 395

26 Photos and videos

$SPCB up ~20% today!

SuperCom just signed and launched a national electronic monitoring contract in Sweden with a customer-published budget of $75 million.

Almost like I called this one.

$SPCB Great find! It looks like the Swedish contract could be worth up to 700m SEK ($76 million) compared to the $17 million SuperCom mentioned in their press release. This notice doesn't name SuperCom because it is the original competition announcement, but the evidence that this is them is convincing:

1. Duration: The contract term matches perfectly. Both the tender and SuperCom's contract are up to 9 years.

2. The deadline to enter the competition was in January 2025, and SuperCom announced the win in March 2026. This aligns exactly with the company’s statement that the evaluation process took "over one year".

3. The 700m SEK figure in the notice represents the maximum spending limit for the entire nine-year term. SuperCom reported the lower $17 million figure because it reflects the government’s initial budget for the core program only. This explains the specific language in their press release regarding "opportunities to grow the contract value meaningfully if additional programs are added." Between that and the earnings call, where the CEO stated we can expect growth on top of the $17 million, this find by @Slapper10101 essentially confirms the significant upside potential of this contract.

3

24

3,519

$SNWV Sanuwave -40% today. Ouch.

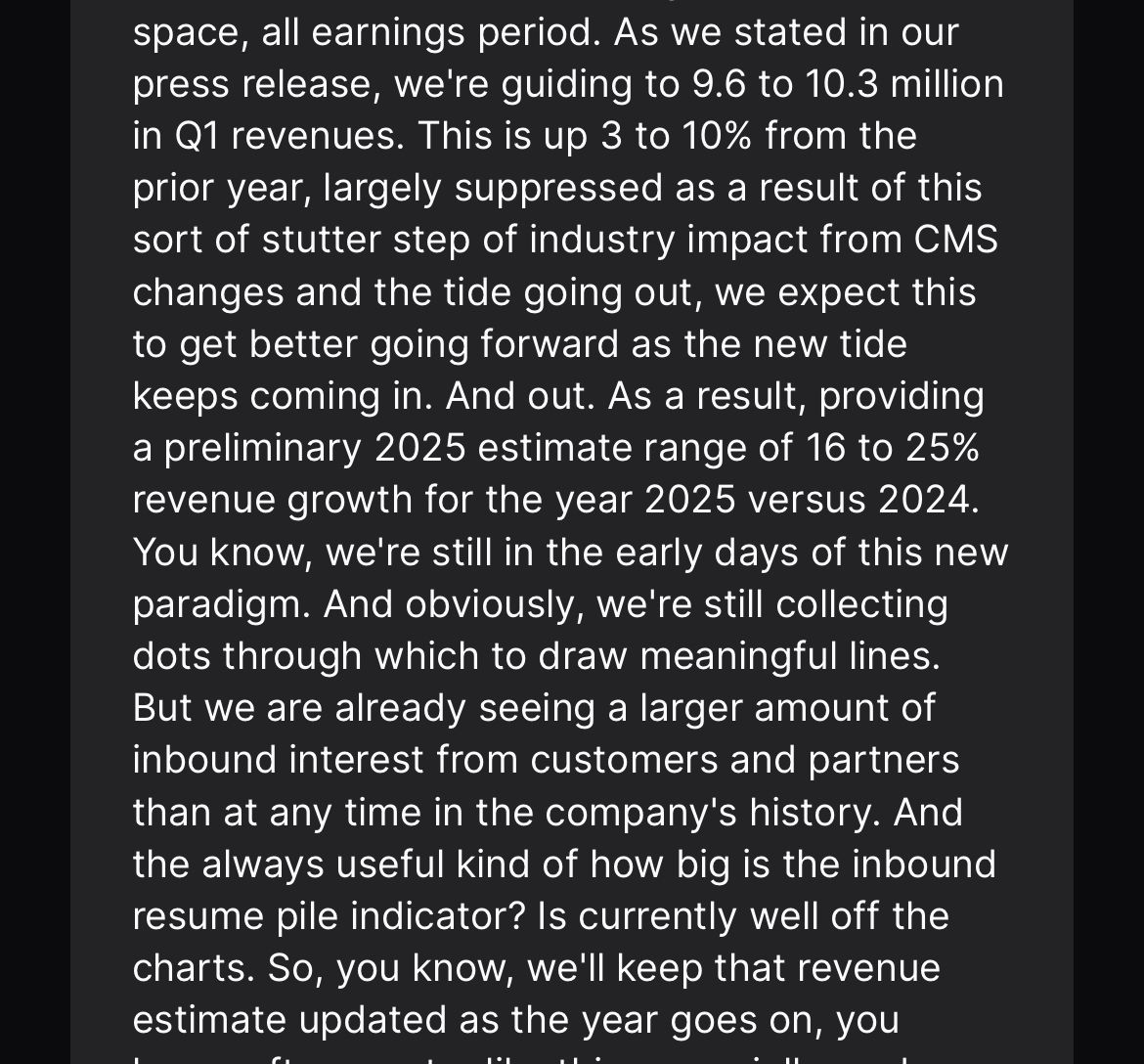

They cut guidance from $11.1m–$11.6m to $8.5m–$9.5m. That's a 20–25% reduction, which is massive. The real question is whether this is a structural problem or just a rough quarter.

The CEO's explanation: widespread CMS reimbursement clawbacks on skin subs and allografts have been far worse than expected, pushing wound care practices out of business. Some of those closures are flooding the secondary market with used Snwv systems, cannibalizing new system sales.

Is this the full story?

What comforts me is that applicator volumes are on pace for a record Q2 consumable shipment volume. That means the entire guidance cut came from system sales, not consumables. My rough math suggests new system guidance dropped from ~145–165 units down to ~50–80. For context, 168 systems were retired as "discontinued" in Q4'25, and some of those have most likely found their way back into the market. That explains part of the shortfall. Combine it with capital-constrained practices pulling back due to reimbursement chaos, and I believe this is most likely the reason for this guidance miss.

My one real concern is whether the market is shifting to a competing product. I haven't found any evidence of that. If you have, let me know.

So to me this looks like a short-term headwind, not anything that breaks my thesis. And the fact that consumables are tracking toward a record quarter actually reinforces the core thesis. The install base is being used. Practices that own the device are running more treatments.

Currently Sanuwave is trading at under 2x sales, 80% gross margins, and meaningful operating leverage ahead as the company scales. Even if you assume just 50 new systems added per quarter (same as the lower end of this horrible quarter) going forward, that's 200 annually, a roughly 15% increase to the 1,382 active install base, and should be quite proportional to the growth in consumable revenue. That's the conservative case.

The bull case is actually more interesting. Once the reimbursement uncertainty clears, I think new system sales accelerate hard. Ultramist just got added to Healogics, the largest wound care clinic network in the US. They're onboarding large resellers who ignored the device before because skin sub commissions were so fat there was no reason to push anything else. The salesforce has been expanded. These are things that didn't exist a year ago.

Would I buy here? Honestly yes, but my position is already large and I try to ride winners rather than double down on pain.

Looking forward to hearing Morgan Frank at MCC's event on Thursday. That call will tell us a lot.

Not financial advice. DYODD.

1

32

2,680

May 22

$MET.MI is up 30% today. Up 60% since I first pitched it. And yet:

- EUR 11m market cap

- Extremely illiquid (18% free float)

- Reports in Italian only

- Still trading at 1.7x OCF

- Revenues 45% YoY

- Net Income 56% YoY

The part most people are missing: one segment was just 7% of revenues in 2025 but likely contributed >20% of EBITDA. This year it grew 71% YoY.

Nobody's talking about it. Full update coming on Substack soon.

1

1

10

1,455

SpruceHill Capital retweeted

May 17

$SNWV

Peak skin sub disruption caused distributor churn and slower sales cycles the last few quarters. Management says bottom is in.

Q1 3% YoY growth

Q2 guided 10-15% growth

FY 26 guided 16-25% growth

“We've been seeing a great deal of engagement from some large systems right now.”

3

1

15

2,979

SpruceHill Capital retweeted

May 14

$SPCB reported a record quarter with a big jump in margins. EBITDA run-rate is now $13.4 million and it's about to soar as Sweden kicks in. Trades at ~2X '26 est EBITDA (ex-rcvbls) and should be 20 X. One massive new metric reported by SPCB is ARR growth of 180% YoY. Wow.

1

10

41

5,828

May 13

$SNWV: Today’s reaction to the results confirms that this stock was irrationally oversold along with the rest of the industry. There were no positive or negative surprises in the results, yet the stock is up 20%. So much for "efficient markets"

3

11

1,973

May 12

$SPCB I don’t think people understand the magnitude of this!

May 11

Big news for $SPCB, which has the national electronic monitoring contract in Germany. Germany requiring domestic violence offenders to wear ankle bracelets. Prior to this, the Germany contract already had an expected value of 3X that reported by SPCB.

asiae.co.kr/en/article/world…

6

1

18

4,625

SpruceHill Capital retweeted

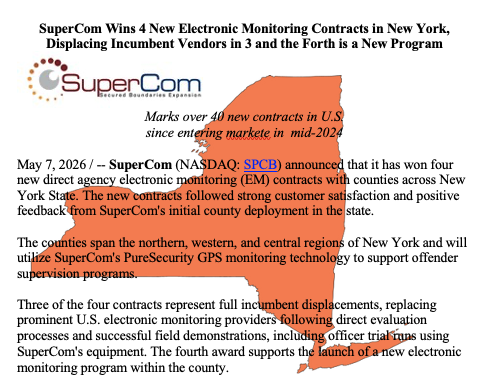

SuperCom $SPCB Wins 4 New Electronic Monitoring Contracts in New York, Displacing Incumbent Vendors in 3 and 1 new Program Launch

Brings SuperCom's US market wins to over 40 since entering market in mid-2024

prnewswire.com/news-releases…

1

1

12

1,168

$SPCB SuperCom is the winner of the Swedish contract worth up to 700 million SEK!

I called the person in this article and she said its supercom. (Im from sweden)

3

1

19

8,013

$SPCB Great find! It looks like the Swedish contract could be worth up to 700m SEK ($76 million) compared to the $17 million SuperCom mentioned in their press release. This notice doesn't name SuperCom because it is the original competition announcement, but the evidence that this is them is convincing:

1. Duration: The contract term matches perfectly. Both the tender and SuperCom's contract are up to 9 years.

2. The deadline to enter the competition was in January 2025, and SuperCom announced the win in March 2026. This aligns exactly with the company’s statement that the evaluation process took "over one year".

3. The 700m SEK figure in the notice represents the maximum spending limit for the entire nine-year term. SuperCom reported the lower $17 million figure because it reflects the government’s initial budget for the core program only. This explains the specific language in their press release regarding "opportunities to grow the contract value meaningfully if additional programs are added." Between that and the earnings call, where the CEO stated we can expect growth on top of the $17 million, this find by @Slapper10101 essentially confirms the significant upside potential of this contract.

4

4

27

19,177

Apr 28

With SuperCom $SPCB, I believe there is a lot of misunderstanding. Therefore, I posted my latest thoughts about the Q4 and annual results on my Substack. It isn't quite as black and white as I initially thought. Go check it out, link in bio!

2

20

2,433

SpruceHill Capital retweeted

Apr 28

Huge quarter for $SPCB. Record revenue of $7.5 million before Germany and Sweden kicked in. 2026 is set up to be a blockbuster. Net debt now well <1X trailing EBITDA and positive net cash including receivables. $1.44 EPS run rate. $3-$5 EPS potential in '26 implies a $100 stock.

3

3

28

4,264

Apr 28

$SPCB Called it! For those following me, already knew this was the case

From FY25

"Revenue increased 1% year-over-year. The period reflects a lower contribution from our largest customer; excluding this impact, underlying revenue growth was approximately 40% year-over-year."

$SPCB: I believe SuperCom’s underlying business is growing at a rapid 80% yoy, but this is currently hidden by the accounting of the Romanian contract. Because of specific rules, 80% of that contract’s value was recognized during 2023 and 2024. Let me explain why:

SuperCom uses a cost based accounting method. At the beginning of a contract, they estimate the total cost of the project; they then recognize revenue as a percentage of the costs incurred. Because the company's European contracts are heavily weighted toward the beginning, SuperCom incurs most costs early when producing and delivering hardware. As a result, the majority of revenue is recognized at the start of the contract.

The Romanian contract was worth $33m with a four year duration. The annual report shows a massive jump in revenue and a customer concentration of 50% in 2023 and 53% in 2024. I am confident this customer is the Romanian government. By my calculations, roughly 80% of the total contract value was recognized as revenue in 2023 and 2024.

If we assume that 10% of the contract is recognized in 2025 and 10% in 2026, we can normalize the data. By excluding the 53% from the Q3 2024 YTD figure and my estimate of $2.25m from the Q3 2025 YTD figure, we see adjusted revenues of $10m and $18m. This indicates that excluding the Romanian deal, the company actually grew 80%. This growth likely stems from the U.S. business, as gross margins have expanded from 48% in 2024 to 61% YTD Q3.

I posted a full write-up about SuperCom on my substack. Link in bio

7

2

25

6,497

SpruceHill Capital retweeted

Apr 20

$SNWV Soon the market will realize how the massive changes in the wound care market is benefitting Sanuwave. Currently it can’t see the forest for the trees.

Mar 27

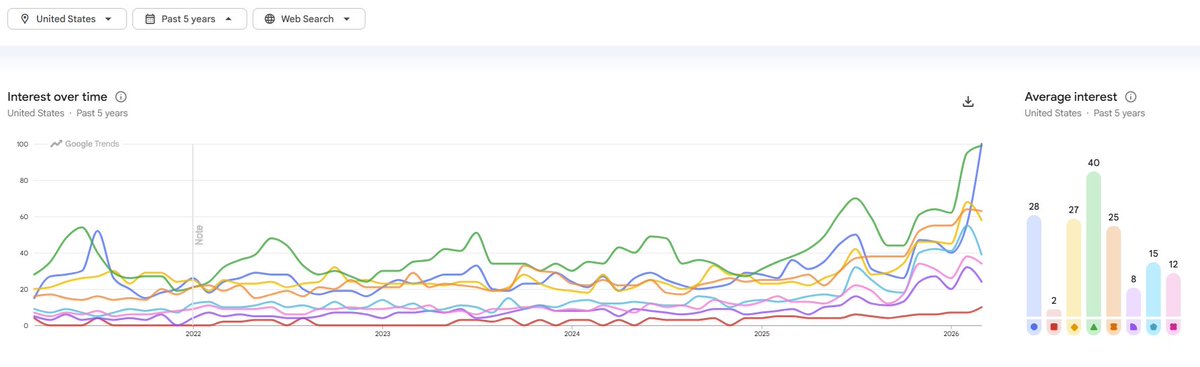

$SNWV - Run the Google search data (filtered, negated and categorized if needed) and you can see the demand going through the roof.

1

1

12

7,751

Apr 19

My full portfolio breakdown is now live! Transparency is a priority for me, and I can honestly say I have never been more excited about my portfolio. I promise that if you check out the latest Substack, you will walk away with at least one high-conviction investment idea.

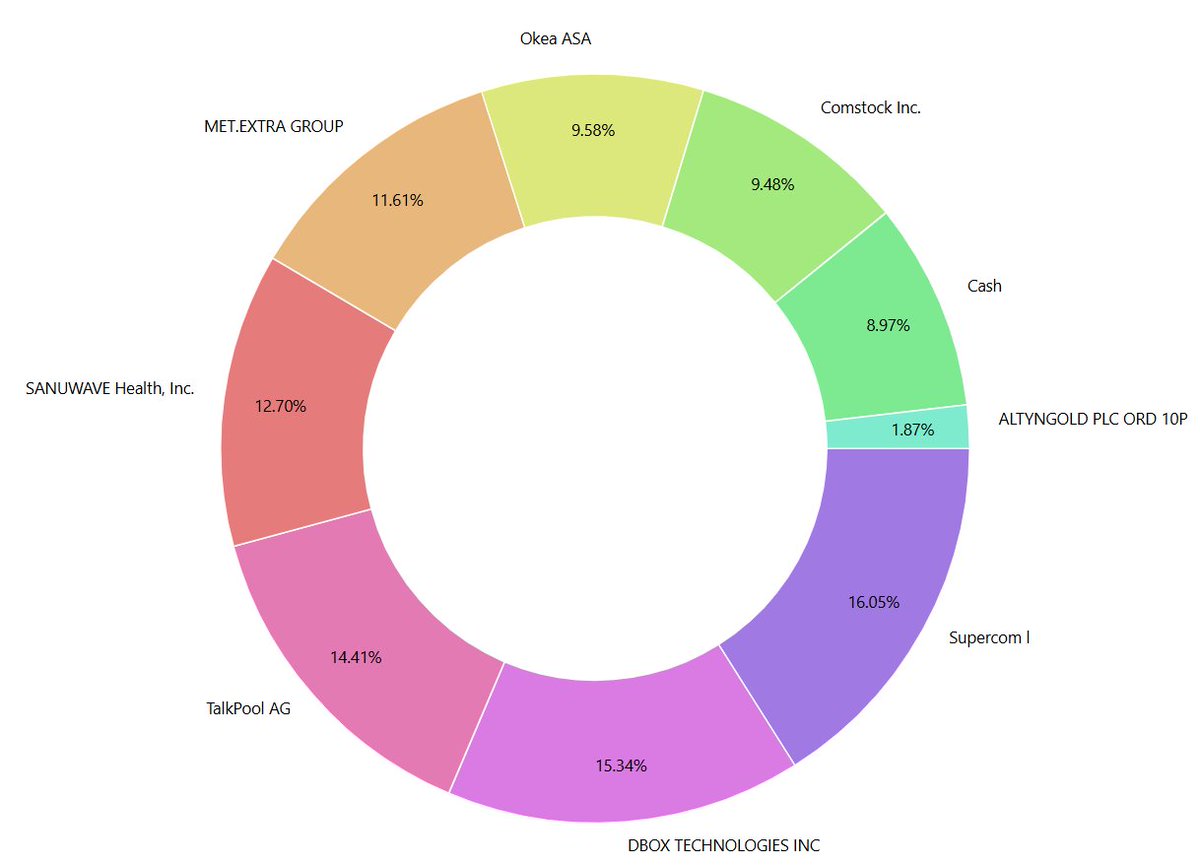

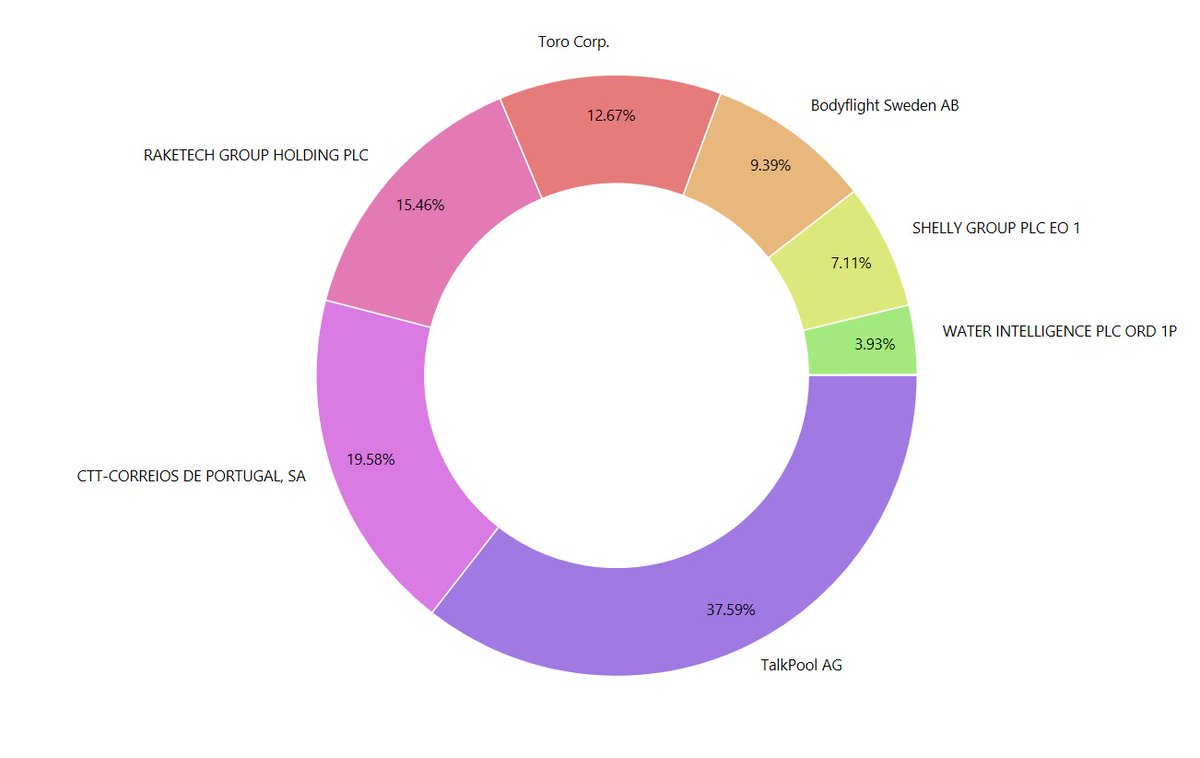

The Current Portfolio:

SuperCom $SPCB: 16%

D-BOX Technologies $DBO.TO: 15%

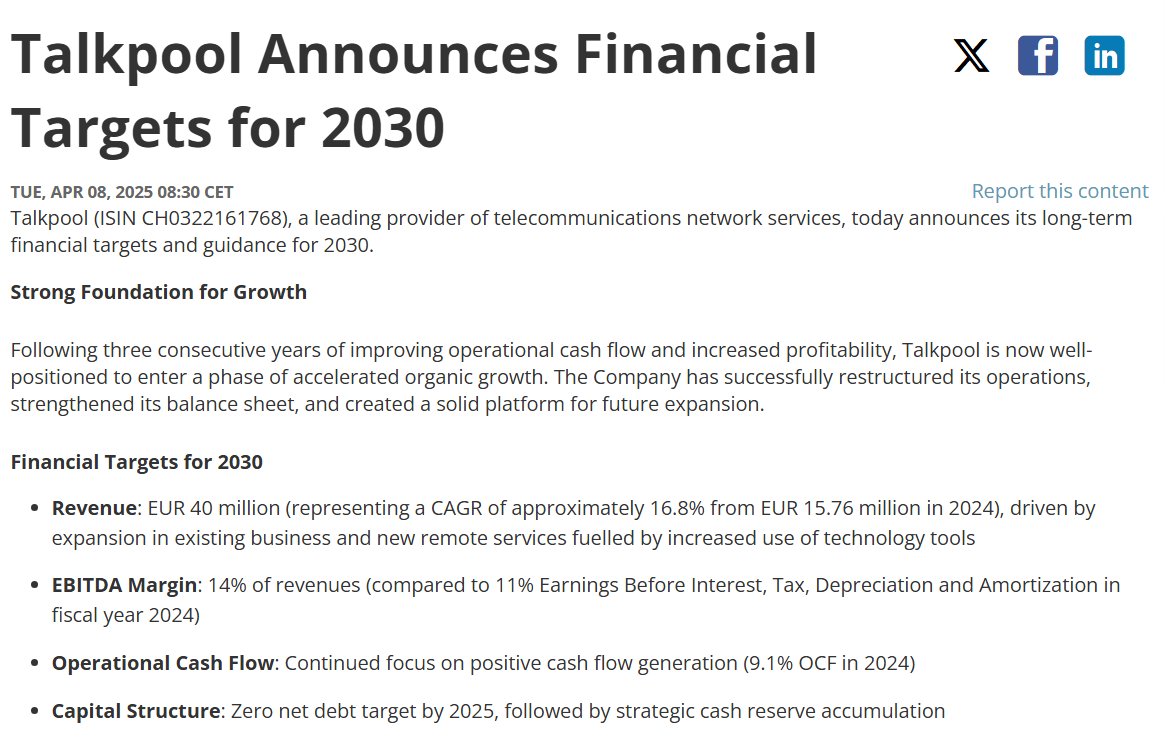

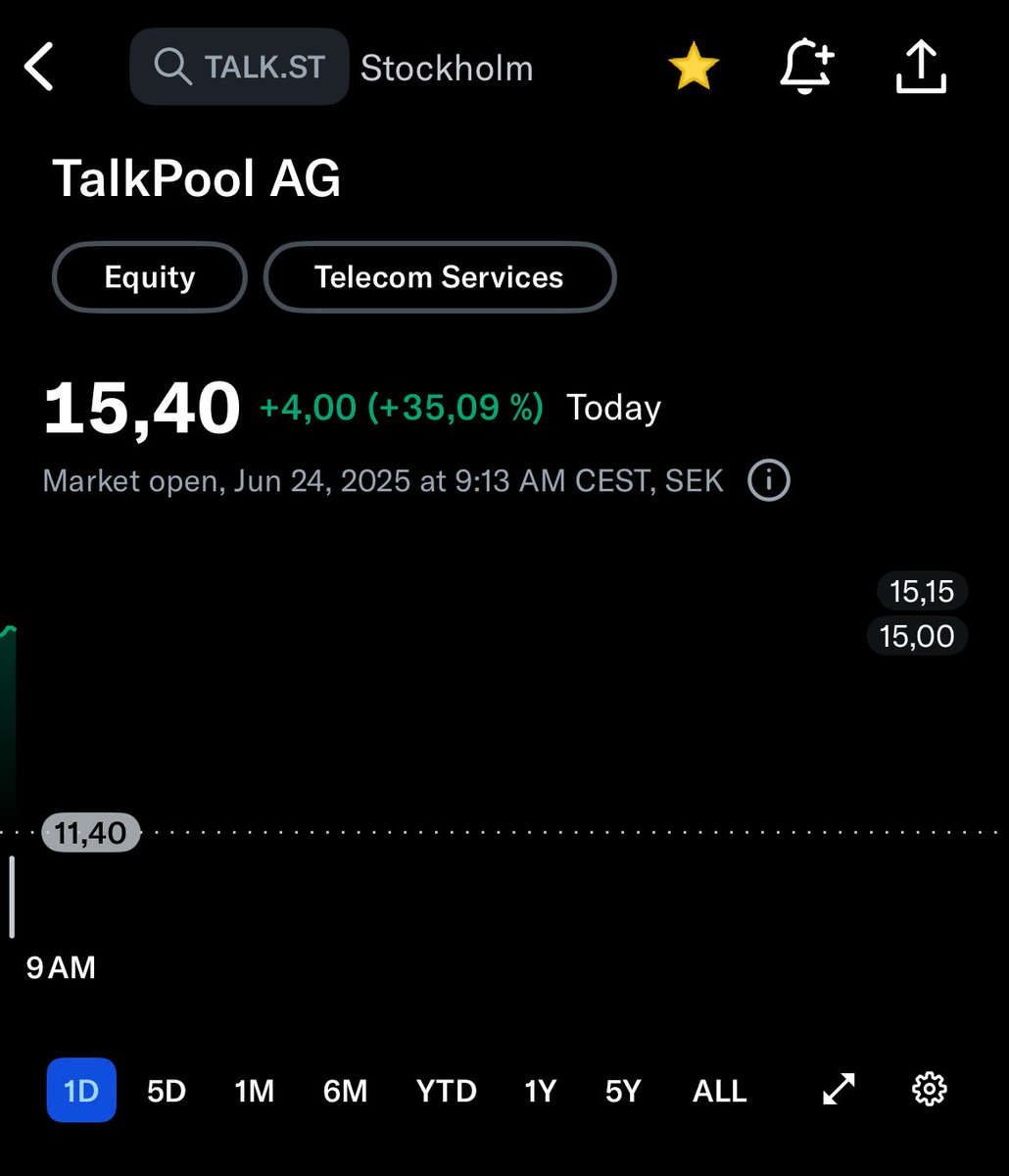

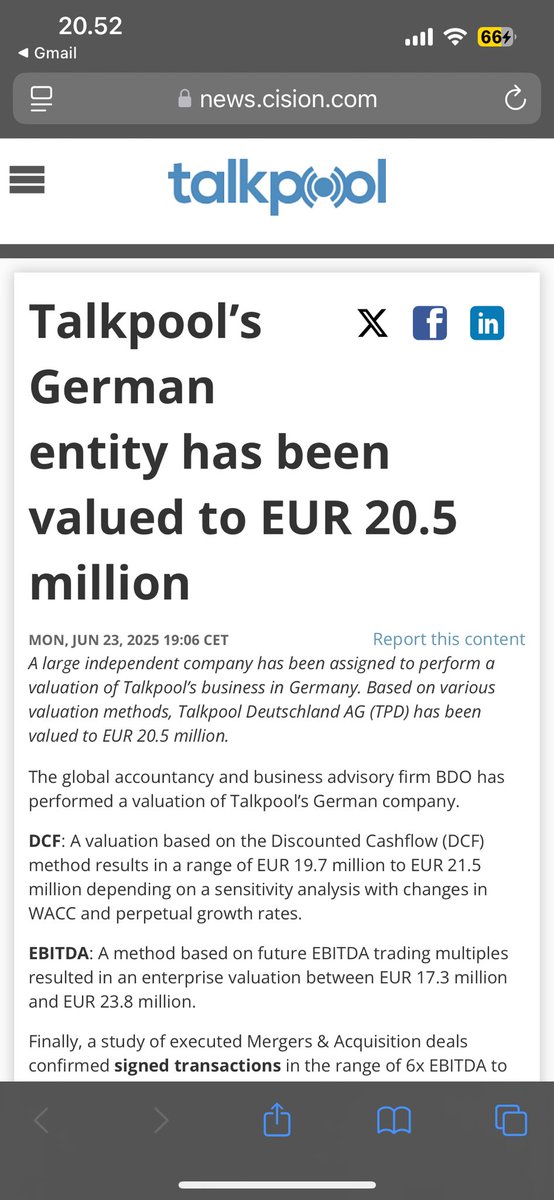

Talkpool AG $TALK.ST: 14%

Sanuwave Health $SNWV: 13%

Met.Extra Group $MET.MI: 12%

OKEA ASA $OKEA: 10%

Comstock Inc. $LODE: 10%

Cash: 9%

AltynGold PLC $ALTN.L: 2%

Substack link in bio!

8

2

35

2,809

Apr 17

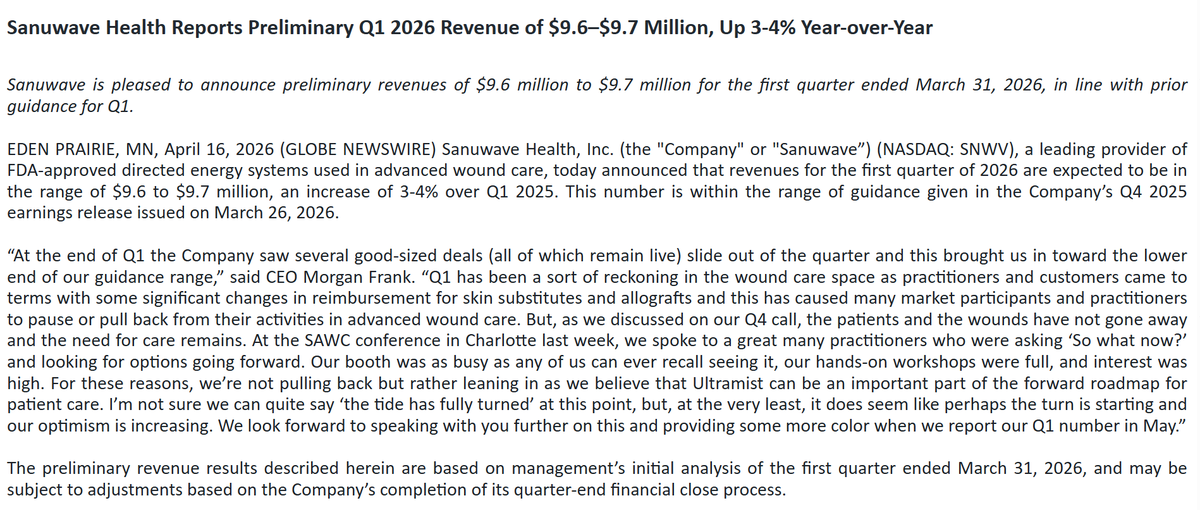

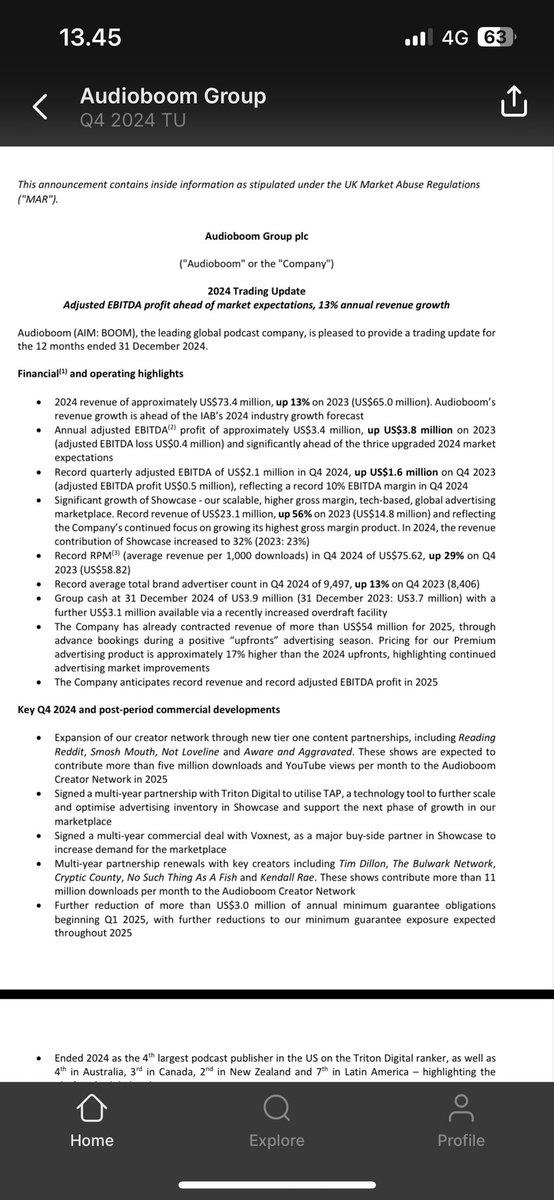

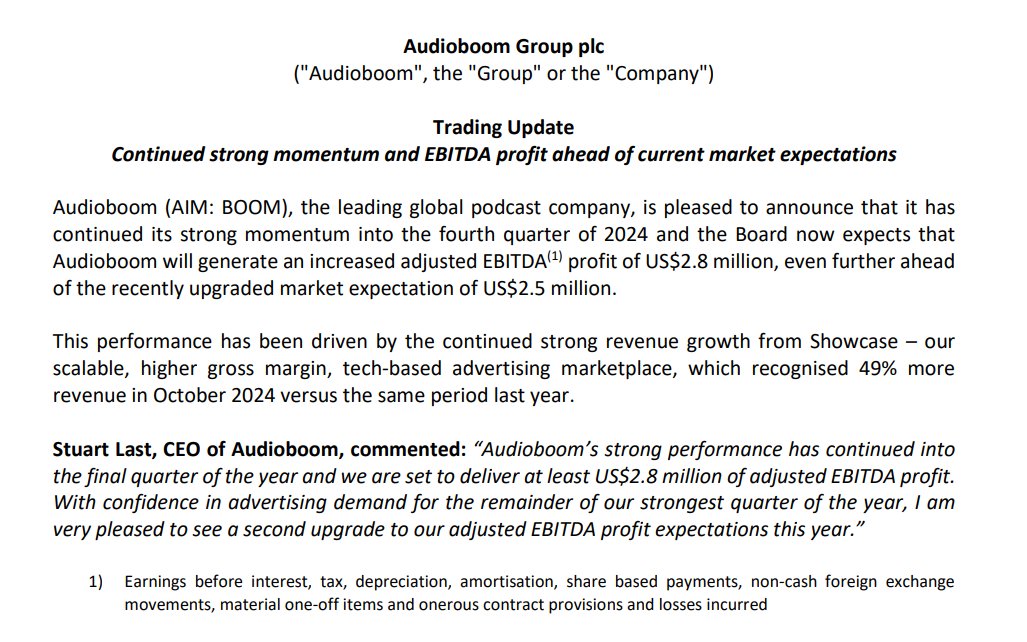

$SNWV is up >10% today following preliminary Q1'26 revenue of $9.6M–$9.7M ( 3-4% YoY). Although results landed at the lower end of the guided 3-10% range, as several large deals were pushed into Q2 but remain active. The market appears to be finally recognizing that the regulatory change is a major long-term tailwind for the company.

While the entire wound treatment industry is in shock because Medicare is now paying 95% less for skin substitutes, there is one company that should see this as a massive tailwind. That company is Sanuwave $SNWV. They make a device that treats wounds pain-free (which is definitely not the industry standard), faster, and at a lower cost.

Sanuwave's share price has declined about 60% recently, following the negative sentiment across the whole sector. The company currently trades at 15x earnings. To give you an idea of their growth, in Q4 '25 alone, they sold 20% of the total number of devices they currently have in use. They operate a razor-and-blade business model where they sell the device first and then charge for the disposable applicators that have to be bought for every treatment.

There is a short-term headwind because some of their customers are going bankrupt due to the Medicare cuts. This means Sanuwave loses the recurring revenue from those specific companies as they wind down. However, since skin substitutes used to be extremely lucrative and now aren't, hospitals and physicians are looking for alternative ways to treat wounds.

The number of patients needing treatment hasn't fallen, so the CEO calls this a "land grab" where the companies that can provide a fast solution will grow rapidly. They are already getting help from larger resellers than ever before, most of whom weren't interested in Sanuwave back when skin substitutes were the big money maker.

One last note: their CEO is a hedge fund guy who is essentially betting everything on the company. He has 70% of his fund in it, takes a $1 base salary, and holds options that only realize if the stock price goes up.

I wrote a longer write-up about Sanuwave on my Substack. Link in bio.

2

22

3,927

Apr 16

The last stock I was supposed to write up was Abacus Global Management $ABX. I liked the bull thesis, but I recently sold my position as their aggressive accounting and related-party transactions started to bother me more and more. Here is what I could not get comfortable with:

There is no certain way for an investor to know if they are artificially inflating the value of their policies. They use mark-to-model accounting, and management decreased the discount rate from 20% (Dec 2024) to 13% (Dec 2025). This move directly inflates the prices of the policies sitting on their books. Therefore, it also records profits on the income statement, even though the underlying assets remain the same.

Counter-Arguments:

This decrease is based on historical and current realized gains, risk scores, duration, and demand for uncorrelated assets. On paper, the logic holds up. For instance, in Q3 ’25, the company received a 37% premium over book value on policies sold. Additionally, in a falling interest rate environment, it is natural for policy prices to rise and discount rates to fall.

Another argument is that they turned their book over 2.6x in 2025. They are getting premiums on those sales, which should theoretically prove the valuations are accurate.

However, the problem I cannot get over is that 828 out of 1,059 policies were sold to their own asset management companies. Management insists these entities are independent and overseen by auditors, but any management team would say that.

How can one be sure these asset managers are actually independent when it comes to the transaction?

The incentive to sell these to their own asset management arms at a premium is also massive. The discount rate they use depends on the premium they get for sold policies. If they sell to their own companies at an inflated price, they are not only able to record a higher premium, but they can also justify a lower discount rate to inflate the value of their entire balance sheet and book higher earnings.

It does not help that the CEO’s bonus is tied to Adjusted Net Income. Essentially, the CEO benefits directly from marking up the balance sheet and lowering the discount rate. While they do use auditors, valuing these policies involves extremely complex formulas. An auditor can verify that the math is correct, but can they prove the underlying factors and variables in the formula are in accordance to what the market would use?

If there's something I've misunderstood please correct me!

Final Note: This is absolutely NOT an accusation of fraud. I am stating that the accounting and related-party transactions create a setup where fraud is possible, and it shares similar characteristics with other companies that have faced such issues. I have zero incentive to push the share price down and would be happy to invest again if I could be confident they are not selling policies to their own asset management companies at inflated values.

8

1

24

6,121

Apr 15

New write-up is live on Comstock $LODE, a stock with >10x potential and downside protection through the sale of non-core assets estimated to be worth 1.5x its current market cap.

The business is hitting a major inflection point. As they open their first industrial-scale solar recycling facility this quarter, Comstock is positioned to become the leader in a market set to grow 10x by 2030.

Management plans to open 6 facilities over the next few years. One facility alone is estimated by management to produce $75M in FCF, which scales to a total of $450M in FCF against a current market cap of only $230M. On top of the core business and the asset floor, they hold a majority stake in an early-stage biofuel venture valued at $500M. This stake is possibly worth many-fold the current market cap if IPOd.

The market is still pricing in past skepticism, but the setup has changed. The CEO has explicitly stated that the dilution cycle is over. With $56M in cash and a massive asset-monetization program underway, the company has a significant financial cushion while they scale the main business.

To read the full write-up: Substack link is in my bio.

9

1

53

4,939

Apr 15

It's live! $LODE

Apr 14

My next write-up is about a case of extreme asymmetry. The core business alone has the potential to be a 10-bagger if successfully executed. On top of that, the company is liquidating non-core assets valued at 1.5x the current market cap. Futher, they also hold a massive stake in a separate venture worth multiples of the entire company if it successfully IPOs.

Stay tuned. Substack link in my bio.

4

34

6,244