Co-Founder / Managing Director @Stack_Talent | AI Data CTO Leaders

Joined June 2009

- Tweets 508

- Following 1,764

- Followers 1,472

- Likes 1,649

4 Photos and videos

Jun 13

Excellent and, sadly, true

Jun 12

If someone from 1996 asked to see a news headline from 30 years in the future, they would be profoundly disappointed

4

Greg Ambrose retweeted

Jun 6

“I’m Jake Tapper, tonight correspondent Laura Loomer dives into Hunter Biden’s deranged trolling, Kellyanne Conway reveals Joe Biden fell asleep watching TV again, and Ian Miles Cheong confirms Biden is the reason he’s never left Malaysia. Those stories and Catturd, tonight.”

352

2,688

19,914

873,188

Jun 2

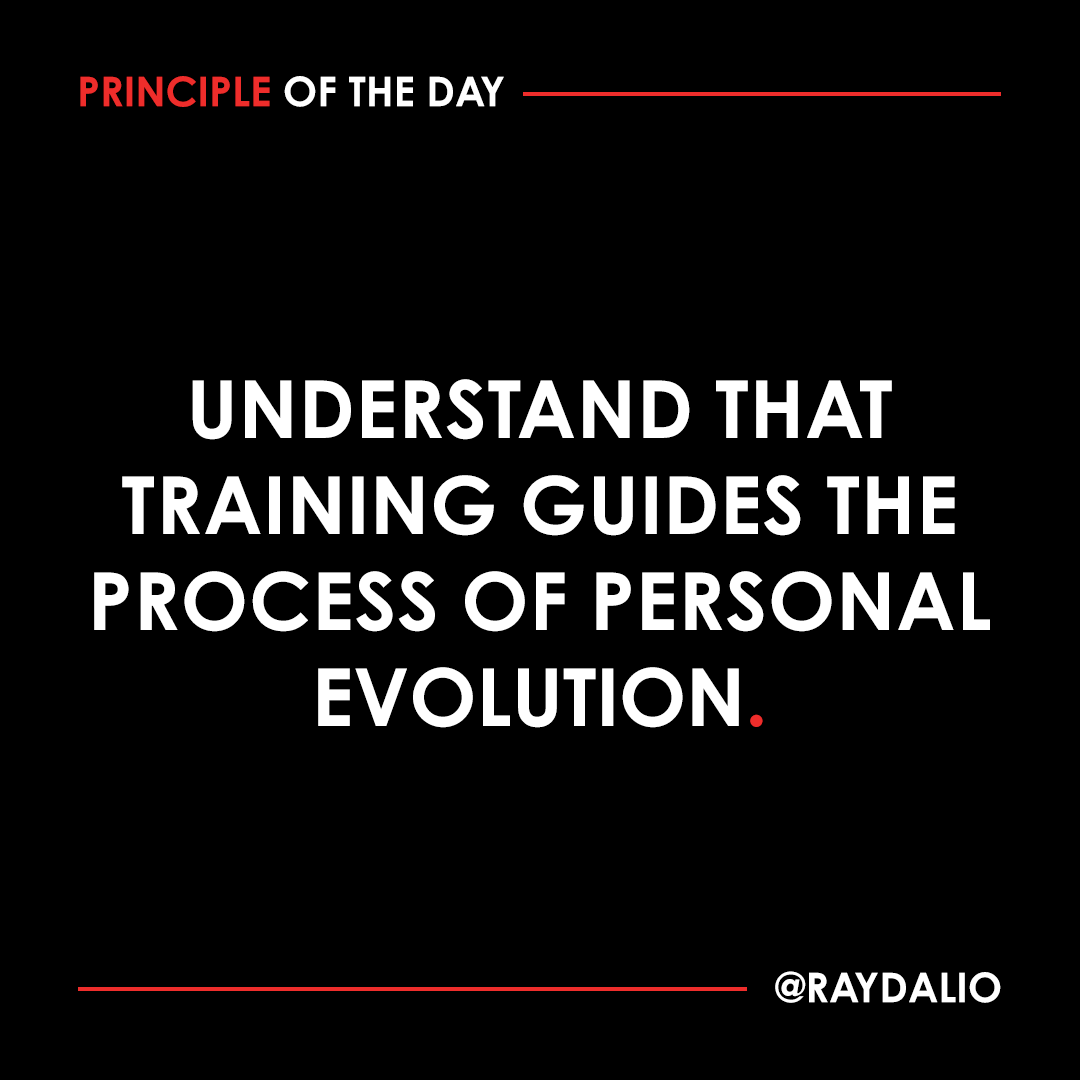

Wise words

Trainees must be open-minded; the process requires them to suspend their egos while they discover what they are doing well and what they are doing poorly and decide what to do about it. The trainer must be open-minded as well, and it's best if at least two believable trainers work with each trainee in order to triangulate their views about what the trainee is like. This training is an apprentice relationship; it occurs as the trainer and trainee share experiences, much like when a ski instructor skis alongside his student. The process promotes growth, development, and transparency around where people stand, why they stand where they stand, and what they can do about improving it. It hastens not just their own personal evolution but the evolution of the organization. #principleoftheday

11

Greg Ambrose retweeted

May 31

It’s like a meth family moved in….

2,544

19,723

160,296

6,639,290

May 31

A very good read and true: "Technology changes. Human behaviour doesn't"

The Railway Bubble Explains AI Better Than Most People Think

The railway bubble is one of the best ways to understand what’s happening with AI today.

The railway boom began with a real breakthrough.

Before railways, moving goods and people was slow, expensive, and limited. Goods travelled by horse carts, canals, and ships. People moved at a much slower pace. Markets were mostly local. A region’s economic value depended heavily on how easily raw materials, workers, and finished goods reached other places.

Then railways arrived.

Distance began to shrink.

Trips once measured in days took hours. Coal, steel, food, and manufactured goods moved faster and cheaper. Cities expanded. Workers reached new places. Trade routes shifted. Entire regions became more valuable because they were connected to railway networks.

So the early excitement made sense.

Railways changed the world.

The first railway companies showed investors what was possible. Investors saw speed, scale, and profit. Governments saw national development. Promoters saw a chance to raise money. The public saw a future unlike the past.

That’s how the bubble began.

First came real innovation.

Then came the early winners.

Then came the story everyone wanted to believe.

“Railways are the future.”

And they were.

But the market slowly turned a true idea into a dangerous assumption.

“Railways are the future, so every railway company must be valuable.”

That’s where things went wrong.

Money rushed into almost every railway project. New companies appeared quickly. Promoters proposed routes everywhere. Investors bought railway stocks less because they understood each business, and more because railway stocks were rising.

The quality of the project mattered less.

The price mattered less.

The expected return mattered less.

Exposure to the future became the only thing people cared about.

That is classic bubble psychology.

A real technology creates real winners. Investors then stretch those early wins across the whole sector. Capital gets careless. Valuations break away from reality.

As railway mania grew, more routes were approved. Some made sense. They connected major cities, industrial hubs, ports, and high-demand areas.

Many others didn’t.

Some lines copied routes already in place. Some connected weak markets. Some were built mainly because money was available. Some existed more for speculation than long-term profits.

The world needed railways.

It didn’t need every railway, in every location, at every price.

That was the mistake.

The infrastructure had value. The capital allocation didn’t.

Then reality arrived.

Railways were expensive to build. Land had to be bought. Tracks had to be laid. Bridges, tunnels, stations, and engines required huge sums of money. Costs rose. Many companies needed more funding than expected. Profits took longer to arrive. Passenger and freight demand wasn’t strong enough to support every route.

Investors eventually understood the future was real, but the returns were not spread evenly.

The best railway lines survived.

The strongest operators became valuable.

Weak projects collapsed.

Share prices crashed.

Speculators were wiped out.

Money raised in a wave of excitement turned into losses.

That’s the main lesson.

Railways didn’t fail.

The railway bubble failed.

The technology survived. The infrastructure stayed useful. Railways kept transforming economies for decades and became one of the foundations of industrial growth.

But investors who bought the wrong railway stocks at the wrong prices still lost money.

That’s how bubbles work.

They are not always built on fake ideas.

Many of the biggest bubbles begin with real technology, real innovation, and real productivity gains.

The bubble forms when investors confuse the future of the technology with the future returns of the stocks.

Railways changed the world.

Railway investors still lost money.

The internet changed the world.

Dot-com investors still lost money.

Now AI has taken the place of railways.

AI is real. It will change productivity. It will affect software, research, coding, automation, defence, healthcare, finance, content, and robotics.

But that doesn’t mean every AI company deserves any valuation.

The tracks and stations of the railway era have been replaced by GPUs, data centers, power contracts, cloud spending, and private AI valuations.

The story is once again simple.

“AI is the future.”

And that statement is likely true.

But the dangerous assumption is back too.

“AI is the future, so every AI asset must be valuable.”

That is where investors need discipline.

The question is not whether AI is real.

The question is whether future AI revenue will justify the amount of money being poured into chips, data centers, energy infrastructure, cloud contracts, and private valuations today.

History doesn’t repeat perfectly.

Human behaviour does.

Every generation believes its bubble is different because the technology is new.

The pattern usually stays the same.

Real innovation.

Early winners.

A story everyone repeats.

Capital rushing in.

Overbuilding.

Valuations getting stretched.

Reality returning.

A crash.

Survivors become infrastructure.

Speculators get wiped out.

Railways were real.

AI is real too.

But a real technology still turns into a financial bubble when capital loses discipline.

That is the lesson from railway mania.

The future might be right.

The price might still be wrong.

1

7

Greg Ambrose retweeted

May 29

CONAN AT HARVARD: “No university in our nation has produced more Nobel laureates or white collar criminals… so whether you choose good or evil, know that you are among the very best.”

202

7,542

90,375

2,620,909

May 27

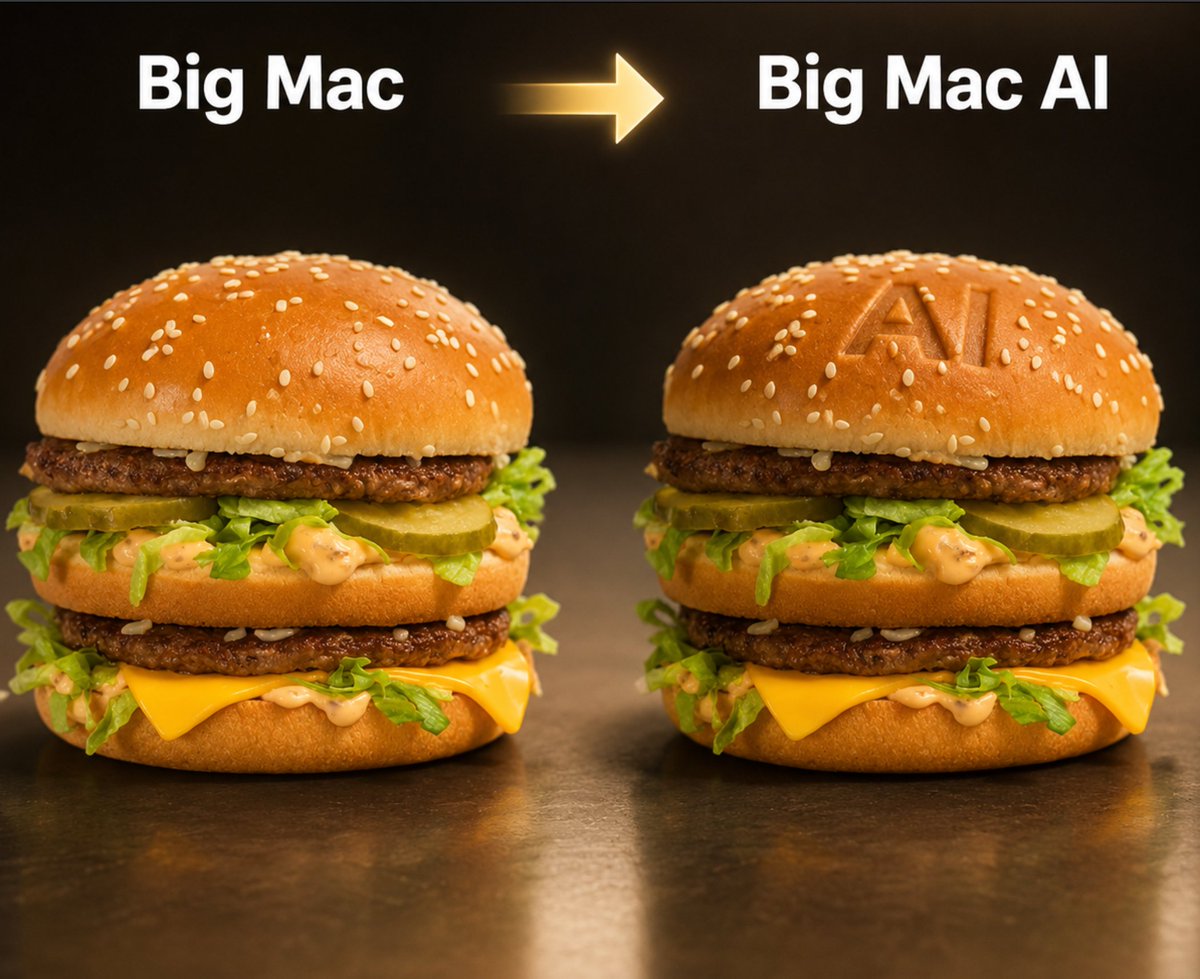

Yes - I am changing my name to Greg AI. I'll take me 800% raise now

I have an idea for how to make McDonald’s / $MCD stock shares soar: just announce a new product called the “Big Mac AI.”

Then every person in the kitchen would become an AI kitchen service. And McDonald’s would have the highest amount of AI workers on the planet!

14

May 27

Norm was the best!

Well, the magazine P.O.V. came out this week, with a list of the best and worst jobs to have in the next century.

Their three best were, in this order: Multimedia Software Designer, Management Consultant, and Interactive Advertising Executive.

While their worst, for the third year in a row... Crack Whore.

1

92

Greg Ambrose retweeted

May 25

I am 95% done with a deal to buy a new house. The remaining 5% of negotiations are focused on the price and whether the owners are actually willing to sell

38

325

2,569

128,509

Greg Ambrose retweeted

My thoughts are that this prediction is not looking great.

1,082

1,993

13,918

526,705

Apr 24

Excellent - and true

Apr 24

The Iranians agreed to negotiate with Tony Schwartz?

21

Apr 6

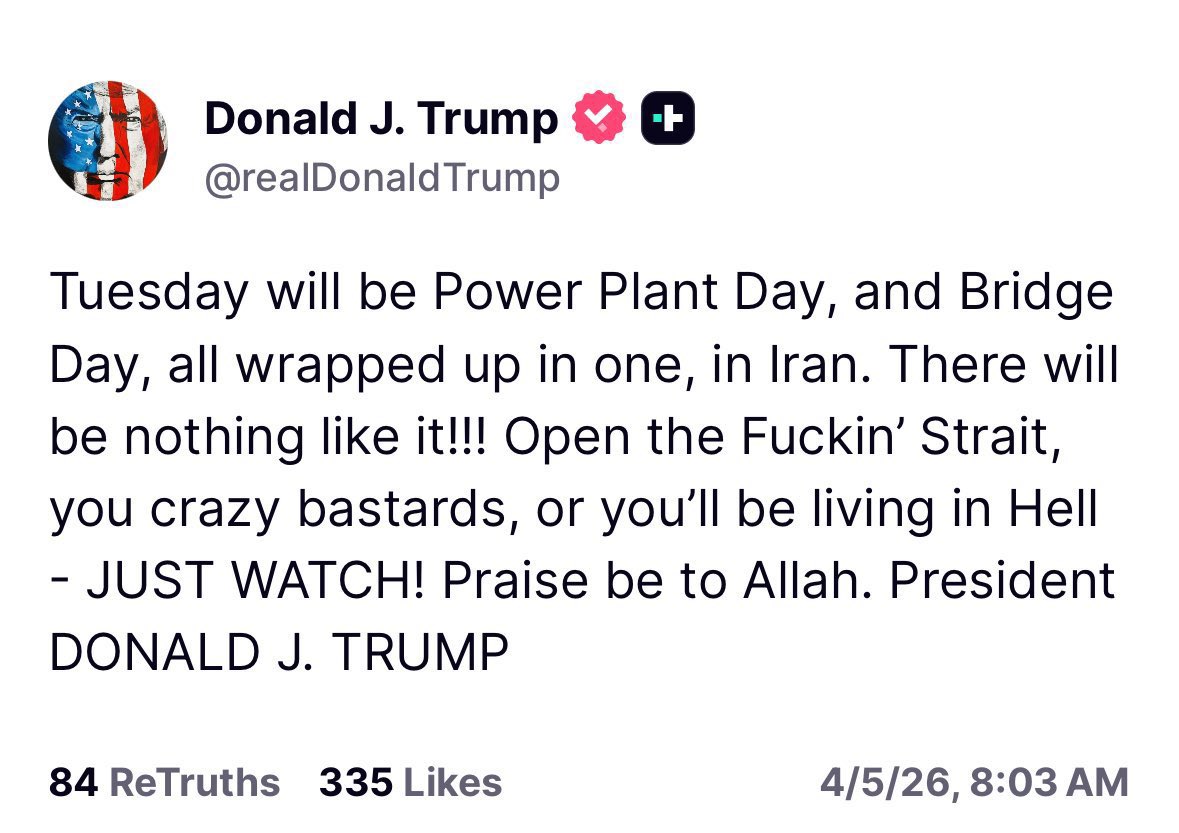

Wow. Just wow

On Easter morning, this is what President Trump posted.

Everyone in his administration that claims to be a Christian needs to fall on their knees and beg forgiveness from God and stop worshipping the President and intervene in Trump’s madness.

I know all of you and him and he has gone insane, and all of you are complicit.

I’m not defending Iran but let’s be honest about all of this.

The Strait is closed because the US and Israel started the unprovoked war against Iran based on the same nuclear lies they’ve been telling for decades, that any moment Iran would develop a nuclear weapon.

You know who has nuclear weapons?

Israel.

They are more than capable of defending themselves without the US having to fight their wars, kill innocent people and children, and pay for it.

Trump threatening to bomb power plants and bridges hurts the Iranian people, the very people Trump claimed he was freeing.

On Easter, of all days, we as Christians should be reminded that the son of God died and rose from the grave so that we can be forgiven once and for all of our sins. Jesus commanded us to love one another and forgive one another. Even our enemies.

Our President is not a Christian and his words and actions should not be supported by Christians.

Christians in the administration should be pursuing peace. Urging the President to make peace.

Not escalating war that is hurting people.

This NOT what we promised the American people when they overwhelmingly voted in 2024, I know, I was there more than most.

This is not making America great again, this is evil.

58

Greg Ambrose retweeted

3 Apr 2025

It’s going unnoticed because so much other news is happening, but the war drums are beating again in D.C. The warmongers worry this is their last chance to get the white whale they’ve been chasing for thirty years, an all-out regime change war against Iran.

A new Middle East war would be a catastrophic mistake. Our military stockpiles are depleted from three years of backing Ukraine. Our effort to reshore manufacturing has only just begun and will take years to bear fruit. War would worsen our already immense deficit and national debt. Iran is larger than Iraq, Syria, and Afghanistan combined. A war would not be easy and could easily become a calamity.

Thanks to President Trump’s restraint during his first term, America has a golden opportunity to pull away from Middle East quagmires for good. We shouldn’t throw that opportunity away so that sone D.C. has-beens can feel tough by sending young Americans to die yet again.

1,914

15,922

62,836

16,320,274

Greg Ambrose retweeted

Mar 19

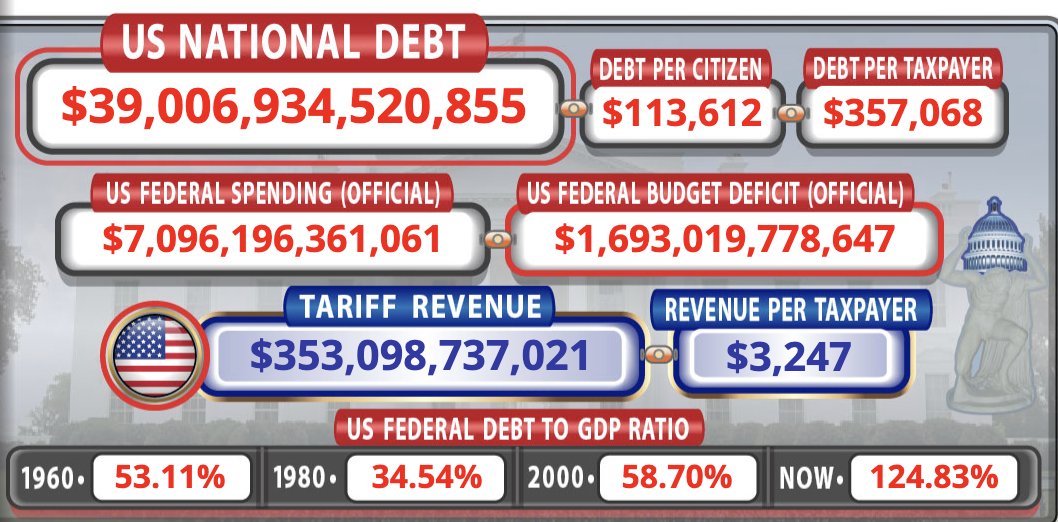

US just hit $39 Trillion in debt for the first time ever.

Warren Buffett on how to end it: “I could end the deficit in five minutes. You just pass a law that says that any time there’s a deficit of more than three percent of GDP, all sitting members of Congress are ineligible for re-election.”

Do you agree with him?

JUST IN 🚨: U.S. National Debt surpasses $39 Trillion for the first time in history 🚨 Congrats everyone, we did it 🥳🫂

34

309

928

59,982

Mar 19

So true

17

Greg Ambrose retweeted

Mar 6

Stack Overflow published a blog "Why demand for code is infinite"

AI is acting like a super-powered teammate, allowing development teams to dream bigger and tackle incredibly complex projects they wouldn't have attempted before.

Because teams can build so much faster now, companies are experiencing a "Cambrian explosion" of new AI apps and are frantically hunting for engineers to manage them.

They say the current shift with AI, moves developers from manually typing every line of code to acting as AI orchestrators who manage intelligent agents.

Human imagination constantly finds new problems, so the demand for custom software remains practically infinite.

Companies are now hiring for specialized positions like human-AI collaboration architects and domain-specific prompt engineers.

Junior developers can now skip basic syntax errors and contribute working features much faster.

The core of programming is shifting from pure memorization to high-level system design.

---

stackoverflow. blog/2026/02/09/why-demand-for-code-is-infinite-how-ai-creates-more-developer-jobs/

Mar 5

Citadel Securities published this graph showing a strange phenomenon.

Job postings for software engineers are actually seeing a massive spike.

Classic example of the Jevons paradox. When AI makes coding cheaper, companies actually may need a lot more software engineers, not fewer.

When software is cheaper to build, companies naturally want to build a lot more of it. Businesses are now putting software into industries and tools where it was simply too expensive before.

---

Chart from

citadelsecurities .com/news-and-insights/2026-global-intelligence-crisis/

80

182

1,309

189,408

Feb 26

Over 70% of candidates say the hiring process impacts their perception of a company. What innovative services would make it stand out for candidates? What can/should firms be doing that they are not now?

2

42

Greg Ambrose retweeted

21 Dec 2025

WALK IT OFF.

#WPMOYChallenge @idjmoore

681

7,551

28,695

2,068,013

Greg Ambrose retweeted

13 Sep 2025

"Lord, when was it that we saw you hungry or thirsty or a stranger or naked or sick or in prison and did not take care of you?’ Then he will answer them, ‘Truly I tell you, just as you did not do it to one of the least of these, you did not do it to me' (Mt 25)."

13 Sep 2025

Brian Kilmeade endorses euthanizing homeless people: "Involuntary lethal injection, or something. Just kill them."

170

1,264

5,019

215,724

Greg Ambrose retweeted

20 Jul 2025

I was a personal trainer for almost a decade. Honest to God, the number one thing I would tell my weight loss clients was to eliminate soda and fast food from their diets. Here, the "MAHA" Secretary of HHS is cheering on soda... at a fast food restaurant. Snake oil salesman.

2,620

3,231

28,133

1,277,183