Focused on helping clients build multi-generational family businesses. Founder at @FusionCPAs. Entrepreneur, Tax Dude, Family Guy, NetSuite Nerd, e/acc Luck

Joined July 2009

- Tweets 5,481

- Following 3,974

- Followers 6,055

- Likes 7,276

308 Photos and videos

Pinned Tweet

Tax season is one of the most intense times of the year inside an accounting firm.

Long hours.

Tight deadlines.

Lots of pressure.

But interestingly, it’s also when younger staff tend to learn the most.

When things get intense, the learning curve compresses.

You can read about something for months, or you can experience it under pressure and understand it much faster.

Sometimes the most challenging periods are also the most valuable learning environments.

6

270

I got off a call last week with a guy starting a franchise. Career salaried employee, first time owning a business.

Smart, prepared, good questions.

He said what they almost all say: "I'll handle the bookkeeping myself for now."

I told him honestly, I get it. Year one is expensive and you want to protect every dollar. And maybe you're in the 5% who can actually pull it off. But 95 to 99% of the time, the moment the business gets any traction, bookkeeping becomes the last thing you want to do. You're selling, hiring, putting out fires. QuickBooks sits there. Transactions start running through personal accounts. Receipts go missing. Then tax season is cleanup season instead of planning season.

There are about http://1.5 ways to do QuickBooks right and about 2,000 ways to do it wrong. You can get into the 2,000 very fast.

What I actually told him: give it a try. But raise your hand the second you know you're not going to keep up with it. The two things that matter most early on are simple. Get a dedicated business checking account and a business credit card, and run every transaction through them. That's it. If we can see the transactions, we can capture the deductions. If everything's running through your personal accounts, we're flying blind.

The recordkeeping isn't exciting. It's just the thing that makes everything else possible later.

2

3

73

My kids are 2 and 4. In twenty years they're adults. That math has been hitting me lately.

I think a lot about the cycles of all of it. The cycles of the business, the cycles of family, the stage your kids are in versus the stage you're in versus the stage the firm is in.

My wife and I talk about this five times a day, honestly. The family blueprint and the business blueprint are the same conversation for us. I don't really separate them.

The thing I keep hearing from older entrepreneurs, people who've been doing this for thirty or forty years, is that the regret isn't usually about the work. It's about the stage of family they were too busy to notice while they were building.

That's stuck with me.

Today's a post-tax-season Tuesday. I'm walking around with a headset instead of glued to a desk. Meeting my wife for lunch in a bit. These are my favorite kinds of days.

A 2-year-old won't be 2 again next month.

1

1

85

Most people see the tax return as the finish line. It's actually the starting line. That return is the whole year compressed onto a few pages.

What you made, what you invested, how you structured things, what worked, what blew up.

It's a roadmap for the next twelve months if you treat it like one.

The question isn't "is it filed." The question is what actually happened here. Why did we owe what we owed? What drove that number, was it a one-time event, or is it baked into how the business is structured? What does this tell us about cash flow, investment timing, owner comp, the entity setup?

If you file it and move on, you're throwing away the most useful financial document your business produced all year. If you sit down with your CPA and read it like a roadmap, the next twelve months get a lot less reactive.

51

Most tax penalties have nothing to do with complexity. It's timing.

Every tax season we get the same call.

"Can you file our return? Deadline's next week."

Short answer: no.

Not because we don't want to help. Because it's not possible to do it properly.

We need time to actually review the financials, ask the questions that surface the real issues, validate the data, figure out what you actually owe versus what the software thinks you owe.

That doesn't happen in a week.

What happens in a week is rushed work, errors, late filings, penalties. And honestly, the penalty isn't the worst part. The worst part is the planning year you already lost.

If you're calling a CPA the week before a deadline, the filing itself is only part of what's missing.

The work that actually moves the needle is entity structure, owner comp, depreciation timing, retirement contributions, and that work happens months earlier.

Filing is the output. The planning is everything that fed into it.

1

4

88

Trevor McCandless, CPA retweeted

Apr 27

This is 1 of the best interviews I’ve watched in years.

.

If anyone knows @BenSasse or knows how to get in touch with him, please tell him THANK YOU for giving this time amidst his circumstance.

What a gift.

(& Scott Pelley & @60Minutes - 🫡)

50

266

4,391

346,177

This 100% my experience thus far

Apr 24

Sorry to anyone who thought AI would mean we’d work less (at least for now). AI makes it easy to explore more than you did before, and so you start doing far more as a result.

I regularly have seemingly small things that end up quickly consuming 3 hours because the agent made it easy to get started, but you still have to do the rest of the work to complete the project.

This is work that I wouldn’t previously have handed out to anyone else, it’s just stuff that never got done because it took too long to do fully manually. And, counterintuitively, for some of these tasks as AI gets good enough at doing them, it even becomes economically worth it to hire someone to do it on an ongoing basis with agents. But until you could try doing them at a low cost you would never have tried.

This is why AI won’t automatically reduce work in the way we imagine because work isn’t static. Most companies have far more they can do than they have today, it was just hard to get started on it all because of the natural constraints of time and labor availability.

2

3

75

Trevor McCandless, CPA retweeted

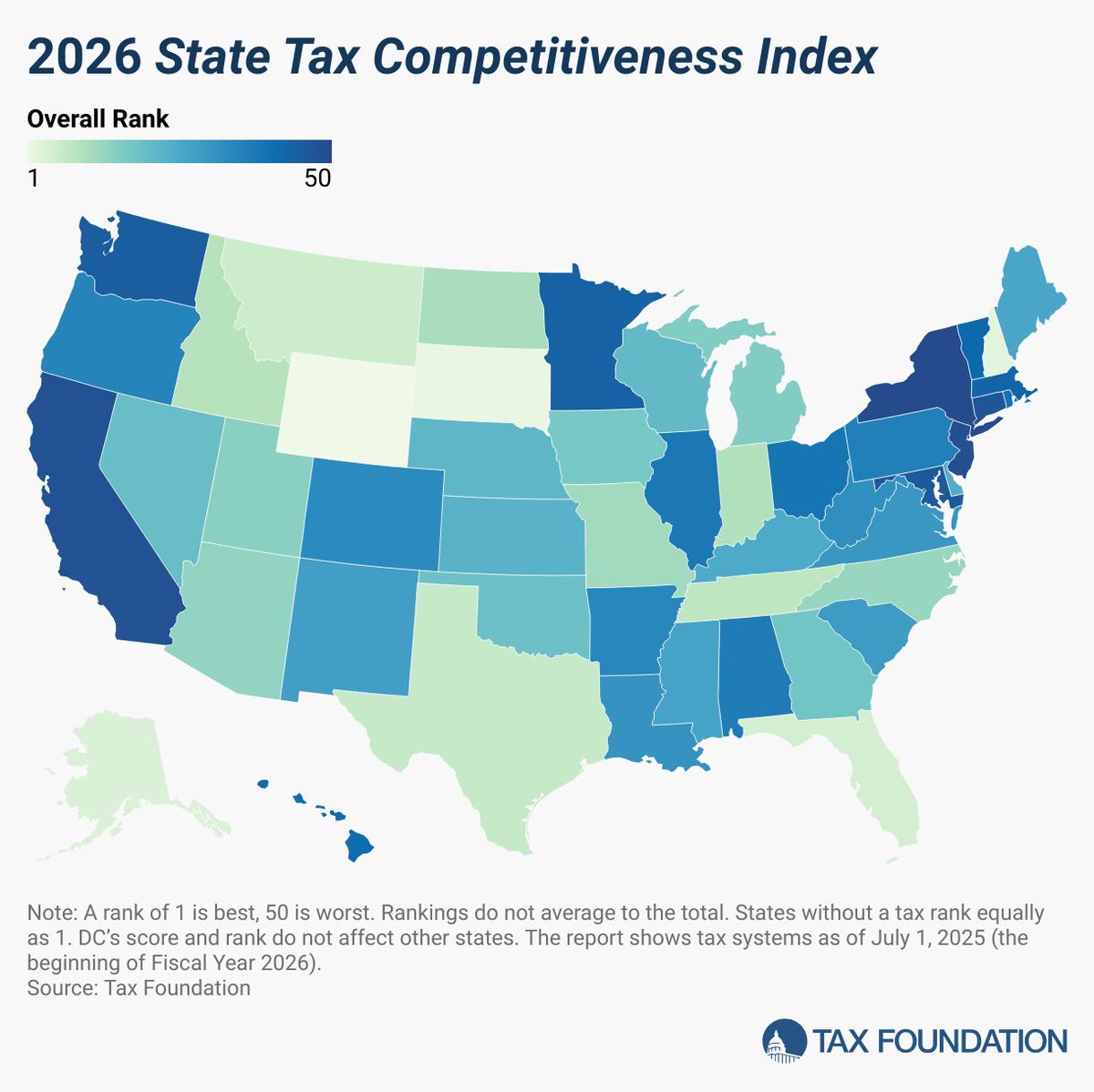

Apr 8

The 10 lowest-ranked, or worst, states in this year’s State Tax Competitiveness Index are:

41. Hawaii

42. Vermont

43. Massachusetts

44. Minnesota

45. Washington

46. Maryland

47. Connecticut

48. California

49. New Jersey

50. New York

Explore the interactive tool: hubs.ly/Q049R9GR0

91

258

711

493,732

Early in my career I went to every networking event I could find.

Meetups.

Happy hours.

Anywhere I could go to help grow the business.

It was a wide net approach. Over time I realized something.

The strongest opportunities usually come from more intentional relationships.

- Smaller groups.

- Curated introductions.

- Conversations with people you actually want to know better.

Less randomness. More intention.

1

1

232

There’s an aura of constant pivoting in the air right now.

Deciding what deserves our attention and what doesn’t is a major skill:

- New AI tools.

- New marketing strategies.

- New ops solutions.

There’s always something new being talked about.

The challenge is figuring out how to compartmentalize the noise.

Some of these shifts will matter. Some won’t.

2

775

For a long time, business growth leaned heavily on digital channels.

SEO.

Online content.

Paid ads.

Those tools still matter, but something interesting is happening right now. Many founders are rediscovering something that used to be obvious.

Relationships are always the best. Especially the in person kind.

The challenge is they’re not scalable. Which means many entrepreneurs are now thinking more intentionally about how they build relationships that actually matter.

1

4

572

One thing we do internally when a lot of ideas start flying around is simple.

We brain dump them.

Every idea.

Every possible opportunity.

Every potential initiative.

Just get it all out.

Then we step back and ask a simple question:

Is there a real opportunity here, or is this just another shiny object?

Sometimes writing the ideas down is enough to see the difference.

2

363

In several founder groups I’m part of, the same conversation keeps coming up.

Tools people thought were three to ten years away suddenly feel like they’re arriving right now.

AI tools.

New platforms.

New automation.

Naturally, the question becomes: What does this mean for my business?

We all crave optimizing our inherent inefficiencies that live in manual, repetitive tasks.

Many are experimenting where it makes sense, but many of us are also very wary of the lack of holistic frameworks and security.

The general feeling is that we are at the inflection point where that enterprise agent system is on our doorstep.

It’s both exciting and exhausting at the same time, lol.

1

495

Trevor McCandless, CPA retweeted

Even when an accounting firm handles both the accounting and the tax for small businesses, we still need the owner’s participation in the process.

You’d think everything runs smoothly.

But in any given month there can be a number of transactions that your accountant is just going to need more clarity on. This is where continuous communication helps save time in the long run.

1

2

621

Trevor McCandless, CPA retweeted

Health insurance premiums for employees are killing the COGS line item for labor costs.

Anyone used the crowd sourcing health insurance providers like @JoinCrowdHealth before?

1

1

2

532

Trevor McCandless, CPA retweeted

There's no better classroom than tax season. For new staff especially, the pressure is real, the stakes are real & honestly, you'll learn more in these few months than years of school.

6

10

108

12,262