24, student from Norway Focused on US growth stocks & Bitcoin. Certified firefighter

Joined February 2019

- Tweets 7,732

- Following 1,544

- Followers 6,854

- Likes 120,122

704 Photos and videos

Pinned Tweet

Mar 6

My first deep dive in English: An in-depth look at $IREN.

(Link below)

I’m breaking down everything an investor needs to know, while mapping the roadmap to a potential $800 per share (20x). 🚀

This 12,000-word deepdive includes: Everything about the company, Interviews and Unknown facts uncovered by Onlyfrans .

Special thanks to, @FransBakker9812, @Agrippa_Inv, @bitcoinbutcher1, @McnallieM and @jiahanjimliu for the content they provide.

48

66

538

262,405

Jun 13

Well written by Lando!

The repricing of $IREN from a bitcoin miner to a AI infrastructure company will happen soon :)

i believe in 96 months Iren will have 0 bitcoin mining revenue

4

3

71

15,572

Jun 10

Fundamentals are getting better for $IREN every day.

Patience will be rewarded when they go from 134M ARR to 14B ARR in 18-24 months🔥

Jun 10

4

2

122

16,321

Jun 10

The moat is building for $LMND and the competitors are sleeping.

Well done @shai_wininger and @daschreiber

Jun 10

Just launched LTV13, our most capable prediction model ever.

Version 13 sharpens Car prediction specifically, giving our systems a much clearer view into the future: with higher resolution down to the individual policy, and up to 57% better precision than the previous model.

1

23

5,549

Jun 9

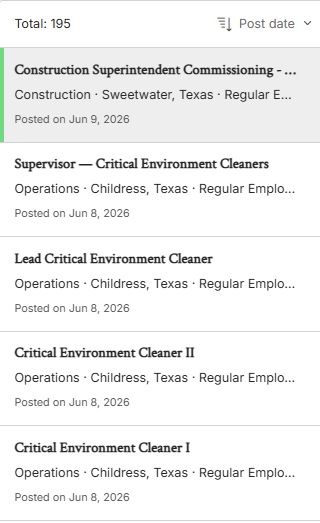

New job listings for $IREN.

They are looking for some cleaners for Childress, to maintain highly sensitive operational spaces.

3

3

86

10,821

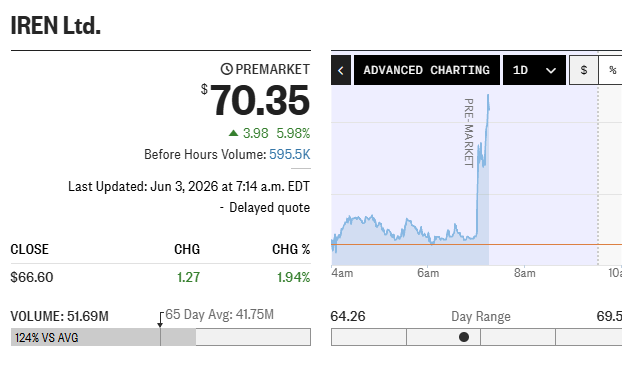

Jun 3

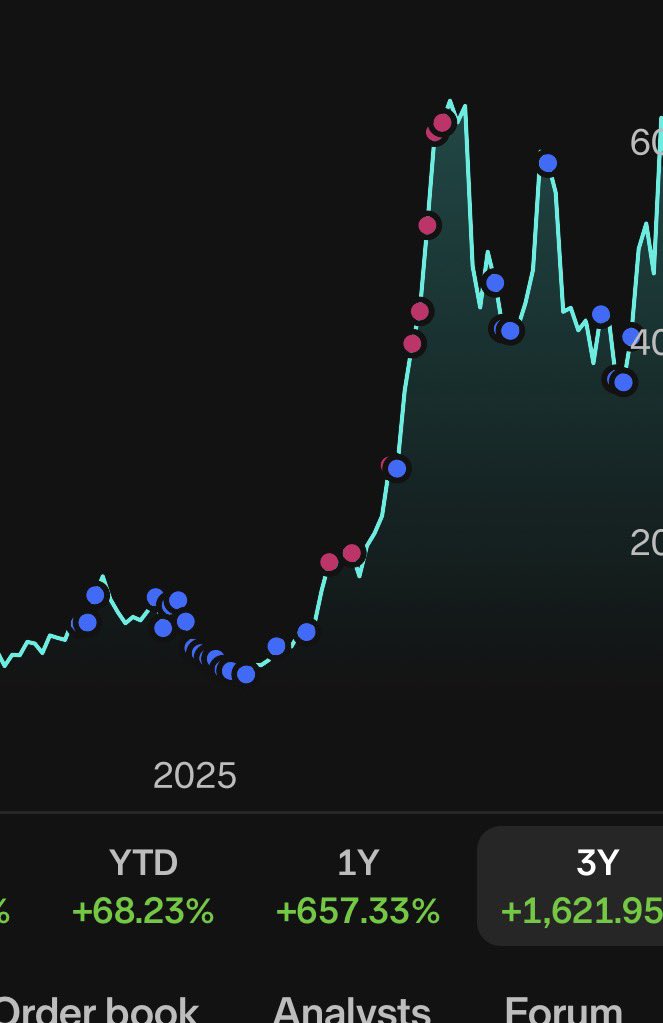

Do we see a new ATH today for $IREN ?👀

Pushing $70 in premarket!

Jun 3

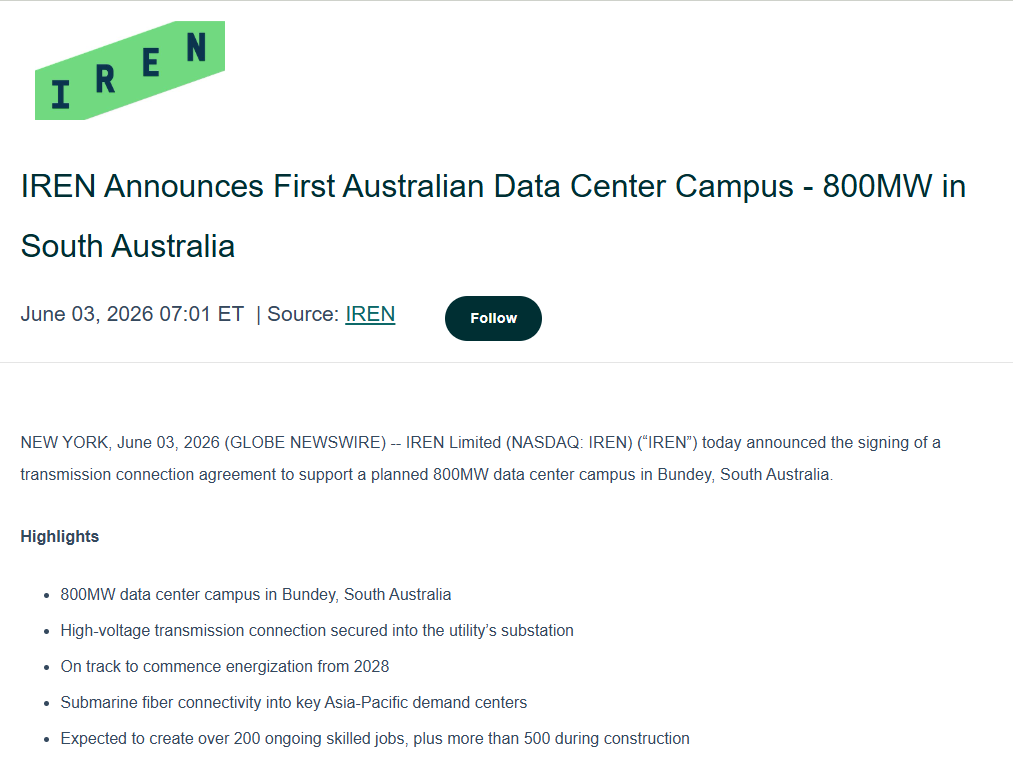

NEW 800MW DATA CENTER IN SOUTH AUSTRALIA🔥

Energization in 2028 for $IREN !

Dan comment: “The Bundey campus is able to serve global and regional AI demand, as well as South Australias own growing need for AI compute. We look forward to partnering with the Government of South Australia

13

121

7,119

Jun 3

With the new South Australia site, $IREN now have 5,8GW of grid secured power!🔥

In the last 6 months, this has increased from 2,91GW to 5,8GW, ~100% increase in less then 6 months!

Jun 3

NEW 800MW DATA CENTER IN SOUTH AUSTRALIA🔥

Energization in 2028 for $IREN !

Dan comment: “The Bundey campus is able to serve global and regional AI demand, as well as South Australias own growing need for AI compute. We look forward to partnering with the Government of South Australia

3

9

183

11,734

Jun 3

NEW 800MW DATA CENTER IN SOUTH AUSTRALIA🔥

Energization in 2028 for $IREN !

Dan comment: “The Bundey campus is able to serve global and regional AI demand, as well as South Australias own growing need for AI compute. We look forward to partnering with the Government of South Australia

7

12

202

33,680

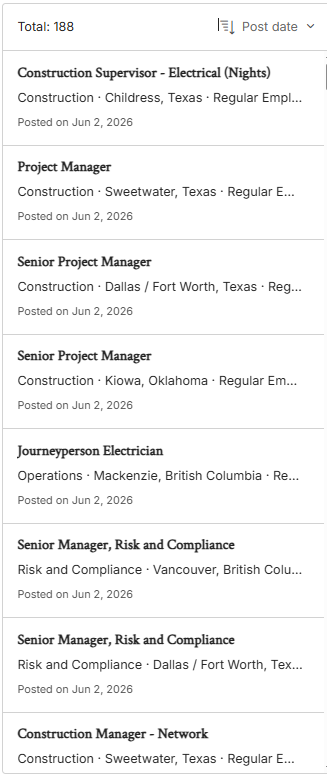

Jun 2

Alot of new job listing for $IREN today.

Interesting to see they have started Construction hiring in Kiowa, OK.

The job listings have been ramping up alot lately

3

5

129

17,821

Jun 1

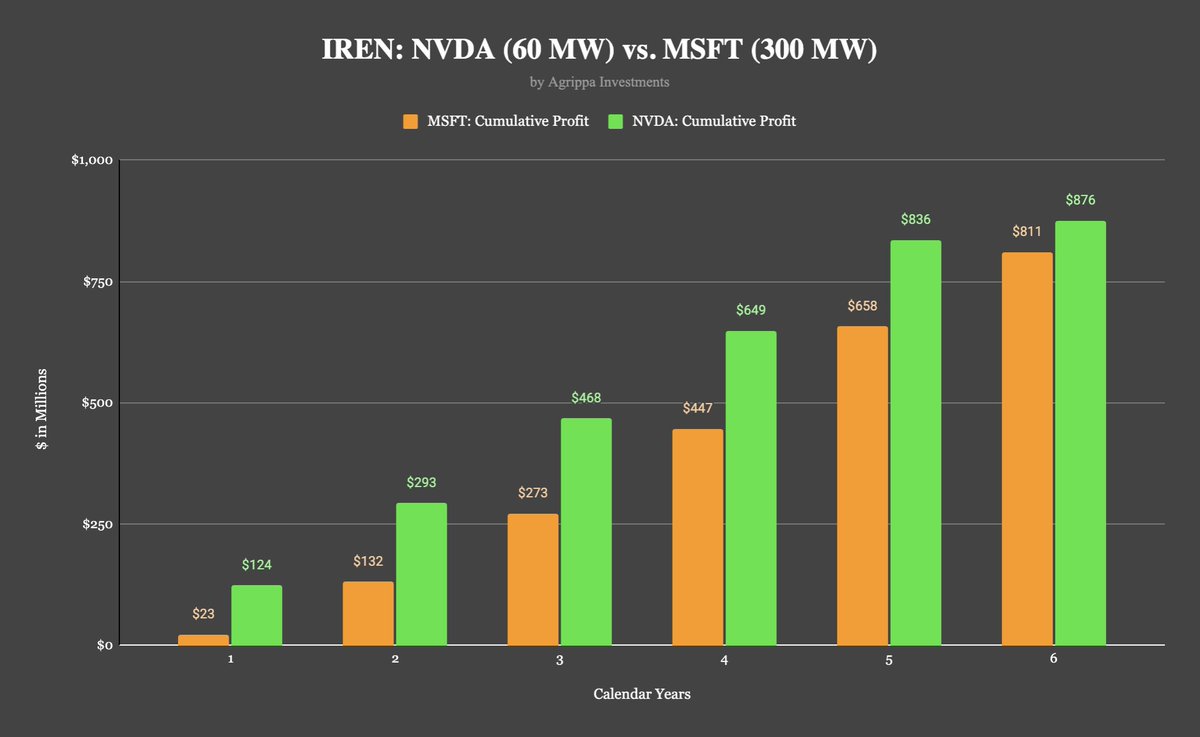

The future is bright for $IREN, and I am happy $IREN still has <10% of its capacity locked in contracts. Everyone has been asking "WEN DEAL" but management has done the right thing and waited, because the economics have become way better now!🔥

Most $IREN investors don't yet grasp how profitable the 60 MW $NVDA deal actually is.

Despite being just 20% of the MW capacity, it yields more cumulative net income than the 300 MW $MSFT agreement.

This is a direct result of $IREN locking in stronger terms.

Now that $IREN is quickly establishing itself as one of the premier cloud providers with the deepest pipeline in the industry, I expect future deals to land at similar profit margins.

Considering the price action since last earnings, the market clearly hasn't priced that in yet.

7

5

170

19,149

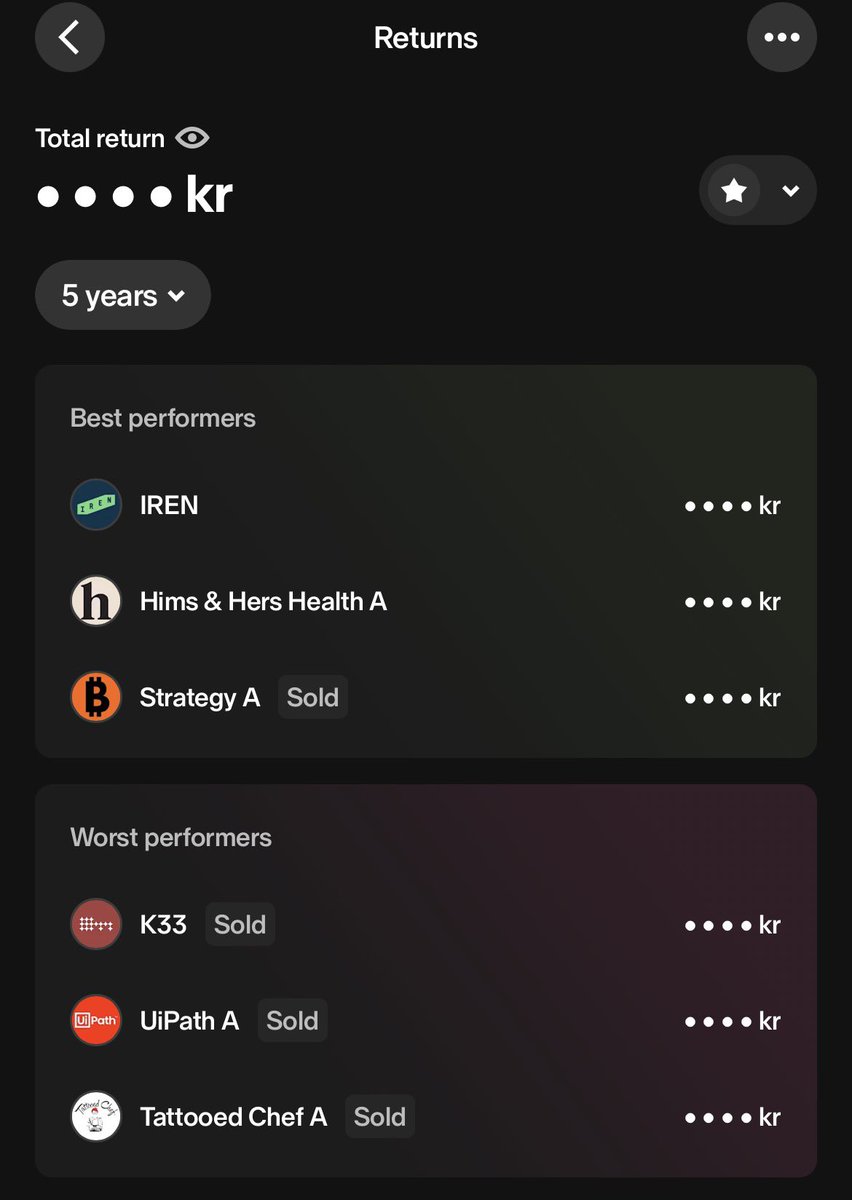

May 31

My biggest winners and losers👀

The most important rule in protecting my capital? Avoiding capital destruction.

I only commit to large positions when the risk/reward profile offers a heavily protected downside combined with massive upside potential.

To put this into perspective, here is a breakdown of my portfolio over the last 5 years:

I have invested in 52 different stocks. I am profitable on 27 and have taken losses on 25.

My win rate is roughly 50%. The critical differentiator is position sizing—scaling heavily into high-conviction setups and keeping other positions small.

To illustrate this asymmetry, compare my two biggest winners ($IREN and $HIMS) against my two biggest losers in monetary value (K33 and $PATH):

My biggest winner ($IREN) is 62x larger than my biggest loser (K33).

My second-biggest winner ($HIMS) is 23x larger than my second-biggest loser ($PATH).

The mathematical advantage of this strategy is extreme:

The profits from $IREN alone are roughly 17.3x greater than the combined sum of every single loss in my portfolio. In fact, any single one of my top 4 most profitable positions could entirely cover the cumulative losses from all 25 underperforming stocks over the last 5 years.

It might sound counterintuitive given the high growth potential of these names, but my entire strategy is fundamentally built around protecting the downside.

7

58

5,789

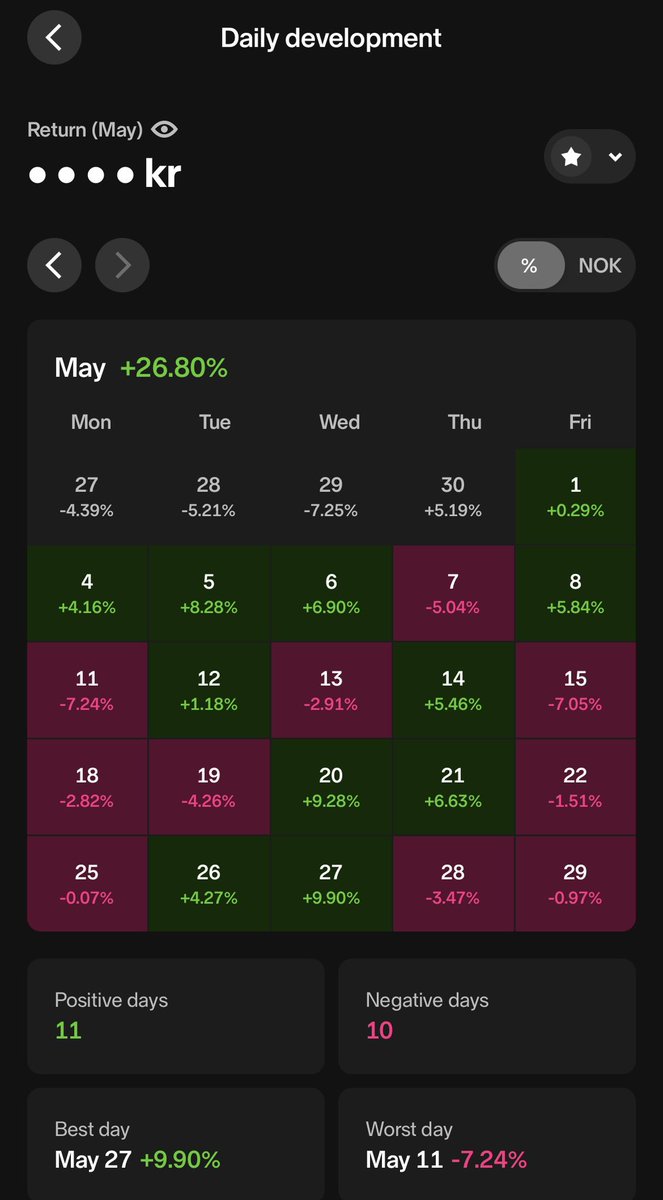

May 30

May has been an amazing month for me measured in returns🔥

My return was 27%, and May pushed my YTD returns to 16,31%.

Had 11 green days, and 10 red days.

My best day was 10% and worst was -7,25%

I believe the best has yet to come for 2026🔥

7

72

6,516

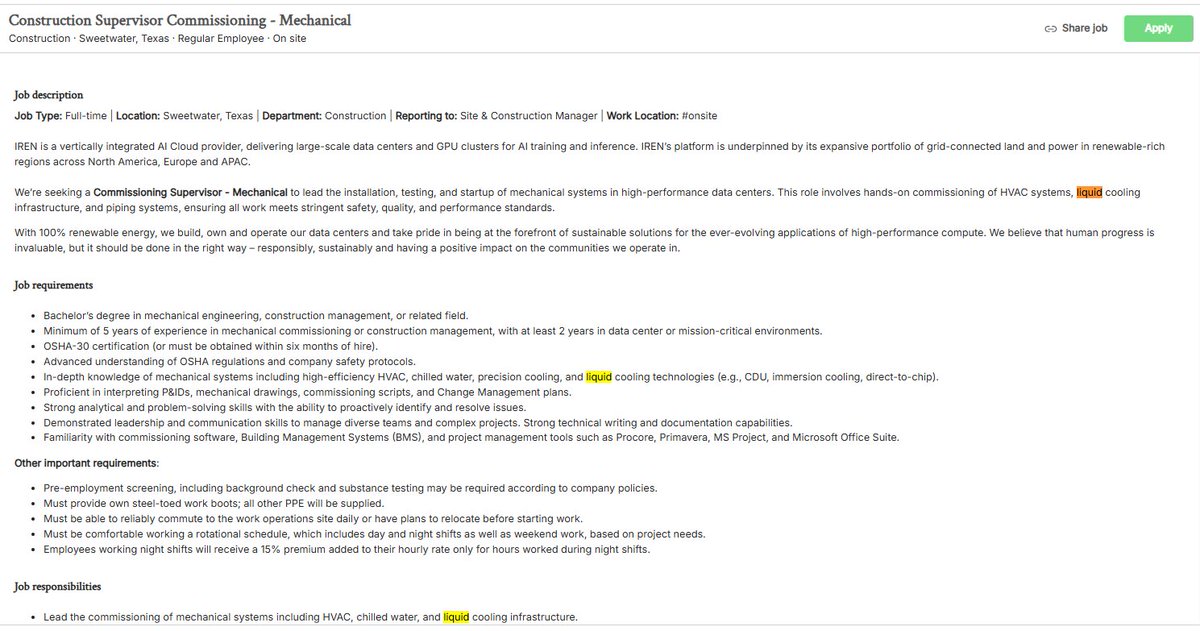

May 29

4 new job lisitings came in for $IREN the last hour. The Sweetwater ramp up continues.

We all know this, but the job listings confirms SW will be for Liquid cooling (see picture below related to the job description):

6

3

141

11,325

May 29

$IREN's >4000% AI growth in the coming 15 months with 5 new deals announced in the coming 6 months. The path to >$12B ARR and >$100 share price by 2027 👇

I believe the upcoming 6-9 months will be highly compelling for Iren, and I expect the stock to significantly outperform the broader market. This outlook is driven by numerous positive catalysts poised to push the share price upward, which I will outline below:

1. Exceptional AI Revenue Growth (>4000% over the next 15 months)

Over the next five quarters, Iren is projected to achieve triple-digit quarter-over-quarter (QoQ) growth, scaling revenue from $34 million to over $1.4 billion within this timeframe. According to calculations by @bitcoinbutcher1 , Iren is on track to reach an annual Recurring Revenue (ARR) exceeding $12 billion by the end of 2027. (check his post)

2. Anticipated Contract Announcements (5 deals in the next 6 months)

Over the next three months, I anticipate Iren will announce several contracts related to their 2027 capacity. Iren currently has an ARR of $4.4 billion, and over the next six months, I expect management to increase contracted ARR from the current $3.1 billion (as of May 29, 2026) to over $10 billion. This growth will be driven by multiple agreements utilizing their 2027 capacity. Below is an overview of these expected agreements:

Mackenzie (80MW):

Iren has purchased approximately 36,000 B300 NVIDIA GPUs, scheduled for delivery in the second half of 2026. This data center will begin generating cash flow for Iren within the year. While the GPUs have been procured, a formal customer announcement for this facility has not yet been made. Market speculation suggests these resources may be allocated to existing clients such as Fireworks AI or togetherAI. However, I am optimistic that Anthropic could secure this capacity, given that Mackenzie is likely one of the data centers offering the fastest time-to-compute. Industry observers are keenly aware that Anthropic is in urgent need of immediate capacity. I expect an agreement for Mackenzie to materialize in the coming months, which would subsequently boost the projected EOY 2026 ARR from $3.7 billion to $4 billion.

Canal Flats (30MW):

As Iren's smallest data center, Canal Flats is set to be retrofitted from Bitcoin mining to air-cooled AI capacity. Consequently, an announcement from Investor Relations regarding additional B300 purchases for this site is highly probable in the near term. This facility is expected to be operational by the first half of 2027, contributing an estimated ARR of over $300 million.

Horizon 5-6 (Liquid-Cooled, VR200):

In their Q1 report, Iren announced plans to build an additional 100MW of IT load utilizing liquid-cooled data centers. I suspect this capacity will be contracted to Microsoft, which is already a client for Horizon 1-4. The key differentiator is that Horizon 5 and 6 will be designed for NVIDIA's latest Vera Rubin models. Estimating the ARR contribution is difficult, as comparable contracts are not currently present in the market, but I anticipate this contract will be secured shortly. With Horizon 1-4 slated for completion by EOY 2026, it is logical to commence groundwork and expansion soon—a process significantly aided by having a committed client.

Childress 250MW (Air-Cooled, Retrofitted):

Iren also announced an additional 250MW of air-cooled capacity for Childress. This involves retrofitting existing Bitcoin data centers into air-cooled AI facilities. The strategic decision to prioritize air cooling is driven by the ability to offer faster time-to-compute, a critical focal point in today's market (again, highly relevant to companies like Anthropic). We already know that 60MW of this capacity is contracted to NVIDIA, leaving 190MW currently available. This remaining 190MW could contribute an additional $2.1 billion in ARR (calculated as $700 million ARR from the NVIDIA contract multiplied by 3).

Sweetwater (300MW to 1.4GW):

This facility has been designated as NVIDIA's "flagship deployment for NVIDIA's DSX architecture." An initial 300MW is scheduled for development in 2027, scaling up to a massive 1400MW data center over time. The immediate 300MW phase currently requires a committed contract. Iren has already completed significant groundwork for the site and secured grid connection approval in early May. This contract will involve NVIDIA's VR200 GPUs, likely making it the largest data center globally with a VR200 installation. This is the contract I am most anticipating due to its sheer scale, potentially exceeding $20 billion. While it is a long-shot, there is a possibility that the entire 1400MW could be leased to a single client. Such a scenario would imply a potential contract size of over $100 billion—a staggering figure considering Iren's current market capitalization of $22 billion.

3. Strategic Rerating: From Bitcoin Miner to Neocloud:

Despite being a strong proponent of Bitcoin myself, its current association does more harm than good for the company's valuation. Bitcoin is generally viewed unfavorably by Wall Street, resulting in the stock trading at significantly lower multiples compared to pure-play AI companies. As Iren transitions away from Bitcoin over the next 6-9 months, I expect the stock to undergo a significant rerating as the perceived risk associated with cryptocurrency is eliminated. This pivot will serve as a major positive catalyst; the company will shed its label as a mining operation and be formally recognized as a premier data center provider.

11

42

363

35,242

May 29

John Gross was an exceptional hire for the $IREN team. Looking forward to see his contributions on Sweetwater's VR200 design.

Like @Agrippa_Inv is saying, big props to the IR/media department!

Exciting times ahead, and Iren is adopting

May 29

$IREN’s new Innovation Officer

A few months ago, $IREN appointed John Gross as their new Chief Innovation Officer, a role in which he'll be pivotal to the development of the company's AI data centers.

The Wall Street Journal recently ran a piece on him that I think is worth commenting on.

Gross specializes in high-density & liquid cooling infrastructure, with over 20 years of experience in the space. That makes him a critical hire for $IREN, given their emphasis on designing & developing all data center infrastructure in-house.

What I particularly found interesting about the WSJ article is that it goes into Gross's approach and philosophy.

He comes across as a very hands-on guy and not some office dweller. He likes being on the ground where the actual liquid cooling tech is being installed and tested, working together with construction crews to fix problems that can't always be foreseen months in advance.

Great to see $IREN's CIO with this kind of attitude. Getting his hands dirty when he needs to and leaving his ego at the door. He's clearly all about pushing $IREN forward and getting things done.

He also pushes back pretty directly against the industry default, which has historically been very risk-averse.

He says the industry “loves innovation as long as it’s 10 years old”, which is pretty funny.

That risk-averse, slow mindset clearly doesn’t work in AI, where chip generations turn over every 12-18 months and thermal envelopes keep climbing.

This kind of attitude combined with $IREN's broader culture is what makes them a disruptive force in the industry that can really challenge the status quo.

Gross also called AI data center tech a bit of a poker game. You can't sit on the sideline waiting for the chip roadmap to be 100% clear, you have to read what's coming and place your bets early.

$IREN has clearly been great at this. Horizon was designed early last year to be future-proof for next-gen chips, more than a year before the official Rubin specs came out. Back then estimates were that Rubin would require densities of ~300 kW per rack, so $IREN's 200 kW design may have looked inadequate initially.

They were obviously proven right...

I know $IREN execs had a very tight relationship with $NVDA well before the official partnership was made public.

That kind of access gives you early visibility into where the industry is heading years in advance, and that's exactly where close ties to $NVDA pays dividends as it relates to developing next-gen infrastructure.

Gross also commented on $IREN's iterative improvement loop, where lessons from each build feed back into the next design cycle.

This reminds me very much of what David Shaw, $IREN's Chief Operating Officer, told me about a year ago when I visited the Childress site with @FransBakker9812 and a few other friends.

Shaw and the other ops execs really emphasized the same design and development philosophy of replication and continuous improvement.

Every individual new build is slightly different from the last as the team implements lessons learned from the previous one. That will mean Horizon 2 will have improvements over Horizon 1, Horizon 3 over Horizon 2, and so on.

The advantage of that approach is that it directly leads to faster, cheaper, and more robust builds, which is a critical trait when you're developing a gigawatt-scale data center portfolio.

This isn't something they started doing recently either. It has been part of the company's DNA since day one.

It only works because of $IREN's very flat hierarchy and very healthy work culture, which encourages every construction crew member to spot flaws or find better ways of doing things.

This is also how they managed to bring the development cost per MW of their air-cooled data center shells down from $750k/MW to $600k/MW.

Going forward this is going to be one of the key competitive differentiators.

While other neo-clouds heavily rely on a patchwork of developers across their data center pipeline, $IREN is the head contractor on 100% of their projects.

The amount of operational experience they'll accumulate as they rapidly scale will become unmatched and very difficult to catch up to.

I also must say, this WSJ article is a real win for $IREN on the IR and marketing front, and they deserve credit for setting it up.

The company's comms had undoubtedly been pretty weak leading up to the recent earnings call, but over the past 3 weeks they've gotten noticeably better imo.

From the CEO’s mega thread here on X that cleared up a lot of confusion to now this WSJ collab… these are real positive moves from the team and they're worth praising.

Overall the WSJ piece does a great job giving us good visibility into Gross himself and his role at $IREN, as well as the company's broader strategic positioning.

I really enjoyed going through it. Definitely worth a read.

partners.wsj.com/iren/buildi…

3

1

74

11,050