Joined December 2011

- Tweets 10,762

- Following 29

- Followers 1,739

- Likes 8,617

880 Photos and videos

Pinned Tweet

15 Mar 2025

Earlier I was influenced & supporting a down to earth person who's d Top most leader of d party & now he became d MP & I think now he isn't ideological for me,Best wishes for his future.

I will always be an ardent follower of Baba Saheb.

Now I have no affiliation with any party.

1

3

3,075

Cc कुर्मी नरेश aka @noi_banglo सेठ जी

'A' name wale log boht chidchide hote hain..

Agr inka chidchidapn dooor Krna hai to inko jitna marzi kooto. Pitne k baad inki hekdi nikal jati hai,qki pyaar se to smjhte ni ye dhor log...🥀

1

41

भाई website को भी हाईड करना था साफ दिख रही है सेकंड पेज मे

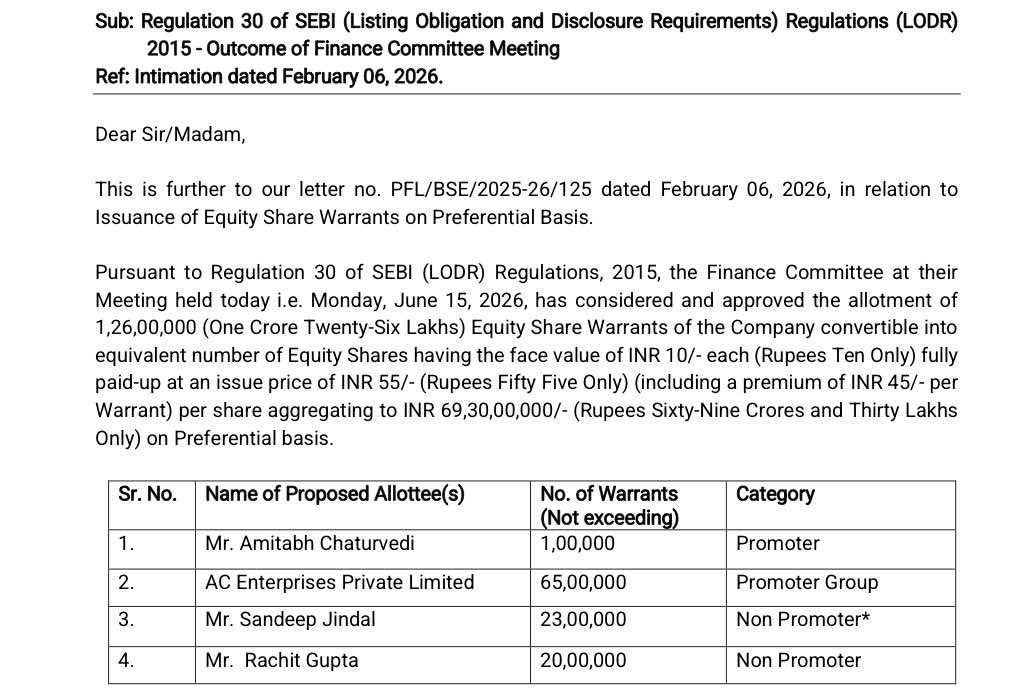

Promoter led warrant infusion of ₹69.30 crore

Market Cap : ₹ 393 Crores.

A BSE listed smallcap NBFC has approved the allotment of 1.26 crore equity share warrants on a preferential basis.

The structure:

- Each warrant converts into one equity share, face value ₹10

- Issue price ₹55 per warrant, including a premium of ₹45

- Total issue size ₹69.30 crore

- 25% received upfront, around ₹17.32 crore

- Balance payable on conversion, after six months and within 18 months from allotment

Who is putting in the money:

Promoter and Promoter Group take the largest chunk. The Promoter takes 1,00,000 warrants and a Promoter Group entity takes 65,00,000 warrants. Together that is 66 lakh warrants, around ₹36.30 crore.

One non-promoter allottee takes 23,00,000 warrants and will be classified as Promoter once the ongoing open offer completes. Counting him, the promoter-side commitment rises to 89 lakh warrants, around 71% of the issue, worth around ₹48.95 crore.

The balance goes to a set of non-promoter investors taking 20,00,000, 6,00,000, 5,00,000, 5,00,000 and 1,00,000 warrants respectively.

Why it matters:

A warrant is a forward commitment. The allottee pays 25% now and the balance only on conversion within 18 months. If they do not convert, the upfront 25% is forfeited. That puts promoter money at risk at a fixed price of ₹55 and signals conviction in the forward value of the business.

There is also an open offer running in the background, and one of the largest allottees is moving into the promoter category. That points to a shift in the ownership and control narrative.

No equity shares have been issued yet, so there is no immediate change in paid-up capital. Dilution flows through only as and when warrants convert.

Dis : Just for educational purposes.

2

Why did they file this petition??

#Savarkar Filed 10 Mercy Petitions Before British, Revolutionaries Like Bhagat Singh Refused To Compromise : Grandnephew Tells Pune Court |

@NarsiBenwal

Satyaki Savarkar deposed in the defamation case filed against #RahulGandhi @RahulGandhi

Read - livelaw.in/news-updates/sava…

34

Ek converted batuwe ko daal dete trust me to agenda fit ho jata, lekin galti kar gaye

5

RT @indiain24hr: 🚨Visakhapatnam: 3 youths who harassed college students were given strict police action by Andhra Police. t.co/7xiT…

155

Badhiya hua 100 -200 padhne chahiye is macrohard ke

राजस्थान में अभिजीत दीपके को कई थप्पड़ मारे गए. ये बहुत गलत हुआ.

आप किसी का विरोध कर सकते हैं, लेकिन हिंसा करना सही नहीं है.

1

23

What kinda obsession this man has with ethanol.

केंद्रीय मंत्री नितिन गडकरी ने 100 प्रतिशत इथेनॉल ईंधन से जुड़े प्रस्ताव को मंजूरी दे दी है। इथेनॉल एक जैविक ईंधन है, जिसे गन्ने और अन्य कृषि उत्पादों से तैयार किया जाता है। वर्तमान में देश में E20 ईंधन का उपयोग हो रहा है, जिसमें पेट्रोल के साथ इथेनॉल मिलाया जाता है। हालांकि, 100 प्रतिशत इथेनॉल ईंधन का मतलब है कि वाहन पूरी तरह इथेनॉल पर चल सकेंगे। गडकरी ने इस फैसले पर खुशी जताते हुए कहा कि उन्होंने 100 प्रतिशत इथेनॉल फ्यूल से संबंधित फाइल पर साइन कर दिए हैं।

#NitinGadkari #EthanolFuel #GreenEnergy

10

🔆!! जय भीम!!!!नमो: बुद्धाय!!🔆 retweeted

राम जन्मभूमि मंदिर लूट में ट्रस्ट महासचिव चंपत राय जी की भूमिका भी संदिग्ध?

काफी सारे 'संघी-रक्त' रामजन्म भूमि मंदिर लूट में ट्रस्ट के महासचिव चंपत राय जी को क्लीन चिट देने, उन्हें ईमानदार साबित करने में जी-जान से जुटे हैं।

वैसे चंपत राय जी को हरिश्चंद्र घोषित करने वाले काफी संघी वो हैं, जिनका घर संघ/विहिप ही चलाता है। कुछ तो आईटी सेलिए बनकर प्रधानमंत्री के साथ अभी के विदेश दौरे पर भी गये हैं। तो ऐसे लोग इनका रोजी-रोटी ही मंदिर लूट और आम जनता के टैक्स लूट से चल रहा है, उनकी अपने मालिकों के लिए वफादारी समझी जा सकती है। परंतु धार्मिक हिंदू क्यों इनके पिछलग्गू बन कर पाप का भागी बन रहें?

वैसे चंपत राय जी से कभी मेरा भी निजी संबंध रहा है, परंतु भगवान श्रीराम के ऊपर नश्वर मनुष्य को रखने का पाप तो मैं नहीं कर सकता। इस पृथ्वी लोक से ऊपर भी एक लोक है, जहां मुंह दिखाना है।

हां, तो चंपत राय जी को क्लीन चिट बांटने वालों को दैनिक भास्कर और उसके रिपोर्टर राजेश साहू द्वारा एक्स पर किए इस पोस्ट को अवश्य पढ़ना चाहिए और चिंतन करना चाहिए कि क्या अभी भी नश्वर मनुष्य के पक्ष में खड़े होकर अपना कर्म बिगाड़ोगे? वहां तो तुम्हारे साथ कोई संघी नहीं जाने वाला है? वहां तो तुम्हारा कर्म ही तुम्हारे साथ जाएगा? तो वह पोस्ट यह रहा:- 👇

"कई लोग जानना चाहते हैं कि राम मंदिर में दान चोरी का मामला खुला कैसे? असल में कुछ दिन पहले चढ़ावे की गिनती करने वाली टीम में एक नया कर्मचारी शामिल हुआ था। 7 जून, 2026 को उसने नोटों की एक गड्डी छिपा ली। उसकी यह हरकत CCTV में रिकॉर्ड हो गई।

पूछताछ होने पर उसने चढ़ावे की रकम में हो रही चोरी से जुड़ी कई बातें बताईं। 9 जून को यह जानकारी सार्वजनिक हो गई और मामला सुर्खियों में आ गया। सपा प्रमुख अखिलेश यादव ने भी इसे मुद्दा बनाकर सरकार और ट्रस्ट को घेरा।

हैरानी की बात यह है कि मामला सामने आने पर चंपत राय ने बाकी ट्रस्टियों को इसकी जानकारी नहीं दी। हेरा-फेरी की जानकारी होने के बावजूद पुलिस में शिकायत भी दर्ज नहीं कराई।

चंपत राय ने 12 जून को सोशल मीडिया पर वीडियो जारी कर सफाई दी। कहा- ट्रस्ट समय-समय पर चढ़ावे की राशि को ऑडिट कराता है। किसी तरह की कोई गड़बड़ी नहीं है।"

#SandeepDeo #AyodhyaRamTemple #AyodhyaDham #ayodhyarammandir #rammandir

9

79

174

3,945

हीरा सेठ जी @the_harkhani जी के सुरत से ही है ये हाई IQ वाले भाई

I have order 2 order where total weight will be 1 kg but i recived only 550 gms with combined of both product where i did not recived more than 460 gms of food its not about money it about hunger do proper justice

@zomato

@zomatocare

1

2

72

एक बार HELIUM AC वालों से बात कर लीजिये HELIUM वाले निकालते है 0.80 टन का लेकिन वो दवा करते है 160 square feet को ठंडा करने का 20000 का आता है इनका ac

heliumair.in/

मेरा रूम का साइज 12ft x14ft है मुझे AC लेना है

किस कंपनी का AC कितना टन का Ac सही रहेगा

जानकार लोग स्जेस्ट करें।।

16

वाह दीदी आप तो फुल फ्रंट फुट पर खेल रहे हो

दो किलों की एक सोने की गदा के चोरी होने की बात भी सामने आ रही है…

शाम तक विस्तृत जानकारी साझा करेंगे चोट्टों की…

11

जो भी शिला पूजन के वक़्त कोषाध्यक्ष थे उनकी उससे पहले की और उसके बाद की स्थिति देख लो पूरे देश मे सब कहानी पता लग जायेगी

Jun 15

पंडित जी वकील हैं,इनको लग रहा है चोरी महाकुंभ से शुरू हुई थी

पंडित जी कितने मासूम हैं

4

सर नीचे तो आना ही था ये भाव इतना टाइम नही चलना था और US हारा है कुल मिलाकर

Jun 15

क्रूड आयल की धार नीचे आने लगी ,

मतलब तो आप समझ ही गए होंगे !

3

वो तो साबित नही हुई और जो macrohard था उसने भी बयान बदल लिए और इस सरकार नें जो नीलामी करी है उसकी figures देख लेते एक बार

Jun 15

ज्यादा चोरी नहीं हुई है, आप लोग हल्ला मचाना बंद करिए

सिर्फ 200 करोड़ लपेटा है जो कि कुछ नहीं है

70 हज़ार करोड़ से लेकर 1 लाख76 हजार करोड़ की चोरी के जमाने में यह कुछ भी नहीं है

और दस बारह सालों में महंगाई भी तो बढ़ी है

रिलेक्स रहिए गाइज

11

CA साब वो एक है ना अमिटिया उससे दूर रहो आप अव्वल दर्जे का चू... है वो बाकि और कुछ नही कहना

Not a good news. Indirectly Porkis got funds which means they can excute their nasty plans like indulging India into a major conflict again. Bibi lost a big time, another loser is us. Winners Russia China Takes it all 🥺

11

नैतिकता होती तो देता

Jun 14

चंपत राय ने नैतिकता के आधार पर इस्तीफ़ा क्यों नहीं दिया? राम मंदिर के चढ़ावे में डकैती का मामला है, चंपत राय को कौन बचा रहा है ? एक मिनट, कहीं ऐसा तो नहीं कि चंपत राय किसी को बचा रहे हैं । ED, NIA, CBI का जैकेट पहन कर किसी विपक्षी नेता के घर के बाहर दिखने वाली टीम कहाँ है? ED का छापा क्यों नहीं पड़ा? डकैती की पुष्टि होते ही FIR क्यों नहीं हुई? कैश बरामद करन वाले कौन थे? अयोध्या में कितनी ज़मीन की ख़रीद बिक्री कैश में हुई है? सबका हिसाब कौन देगा?

3

बंसल अग्रवाल होते है

नाम:- चंपत राय

पद:- महासचिव, श्रीराम जन्मभूमि तीर्थ क्षेत्र ट्रस्ट

इनकी जाति यादव नहीं है, भूमिहार भी नहीं है, ब्राह्मण भी नहीं है, राजपूत भी नहीं है, कायस्थ भी नहीं है।

@grok तुम्हीं बताओ चंपत राय की जाति क्या है?

20

🔆!! जय भीम!!!!नमो: बुद्धाय!!🔆 retweeted

Jun 14

Mera bhi inke jaise boobs hai 🙌. Inke aur mere mai ek hi difference hai mai aise exercise nhi karta 🤗

18

8

37

3,424

SCCL, a company jointly owned by the Central Government and Telangana Government, is headed by an IAS, and eight other board members are also appointed by the CG & TG, whereas two board members are Secretary Level. Still, some people are saying that only TG is responsible.

9