I am a frugal human model. You are welcome to feed me new data and information. I do not need your deep research. Unless it is really deep.

Joined October 2013

- Tweets 1,359

- Following 760

- Followers 547

- Likes 26

32 Photos and videos

Pinned Tweet

Jun 1

这才是我想要的答案

“Don't be afraid to give up the good to go for the great.”

— John D. Rockefeller

1

2,101

DegenQuant retweeted

You don't need to aggressively gamble to make it big in the stock market. You just need to survive long enough until you catch a big narrative early, find a stock before others do, or patiently build a position that finally pays off. Survivable risk until one trade delivers.

54

28

752

35,949

需要算账才能做多的,而且已经涨过了而且没继续涨了的,非常危险。可能会dip deep. $AAOI

Guys we need to talk about $AAOI...

$AAOI is one of the most controversial stocks in the world and I enjoy the disagreement.

Pretty cool that's it up 3x since I went long with many thousands of investors riding it with me up some portion of that gain on @joinautopilot.

But what's cooler is that I think it's still asymmetrical here.

So let's break it down and figure out where we're at $170/share today.

Management argues they can get to $471M in monthly transceiver revenue by Q2 2027.

If you're new to photonics, this is because transceivers are one of the hottest commodities in data centers right now (they translate electricity to light) and 3 hyperscalers are working with $AAOI on this.

At management's 40% gross margin target, that's ~$5.6B in annualized revenue. Run past opex, interest, tax, dilution, we might land around $14-15 in EPS on that run rate.

That's a 2028 number though because 2027 is the ramp mid year, so let's call it bull case $9 of EPS in 2027.

So at $170/share right now, on these calcs, you're paying 19x 2027 earnings, falling dramatically to 12x for 2028.

Don't trust management? Fair. Haircut both the revenue and the margin target by 30%, let's say we get to $4B at a 28% gross margin instead of $5.6B at 40%.

You still land near ~$6 in EPS, just over the analyst mean estimate for 2027E. That's 28x at $170, still WAY cheaper than $LITE and $COHR trade right now.

$LITE is at a 50x NTM forward PE per Fiscal AI.

$COHR is at 47x NTM forward PE per Fiscal AI.

You're paying a fraction of the multiples of its peer group for a faster growing business because execution is still a huge question mark.

If you are an asymmetric trader like me, you might have a large concentrated position in $AAOI for these reasons.

I do believe the stock at $170 is still a solid entry point and I began loading again heavily in the 160's.

319

Long fracking, long oil field service

1

233

我居然独立总结过出来大部分 看来我是有点开悟了

107

DegenQuant retweeted

Jun 12

“I never use valuation to time the market. I use liquidity considerations and technical analysis for timing. Valuation only tells me how far the market can go once a catalyst enters the picture to change the market direction.”

— Stanley Druckenmiller

10

91

569

27,315

DegenQuant retweeted

Jun 13

泵浦激光器,比EML还紧缺的隐形瓶颈,被市场严重低估的紧缺环节,Coherent 2026年3月停止对外销售980nm泵浦芯片,全部自用做EDFA。Lumentum产能被英伟达/谷歌/微软锁死,供需缺口50-60%。价格从80美元暴涨到300美元仍一货难求,Lumentum CEO原话:“泵浦激光器的产能约束比EML还严重。”

1.6T光模块对泵浦的需求是800G的2-3倍。2026年全球1.6T出货1200万只,仅此一项就需要6000万只泵浦激光器。加上DCI互联每50公里就要一个EDFA放大器,每个放大器需要2-4只泵浦。AI算力爆发。数据中心间DCI链路暴增。泵浦需求指数级增长。

国产替代在加速:华工科技980nm泵浦模块月产能5000只,年底扩至2万只。长光华芯泵浦芯片良率提升至75%。但国产厂商电光效率和可靠性与海外仍有2-3年差距,预计2027年才能真正缓解行业缺口。

Jun 13

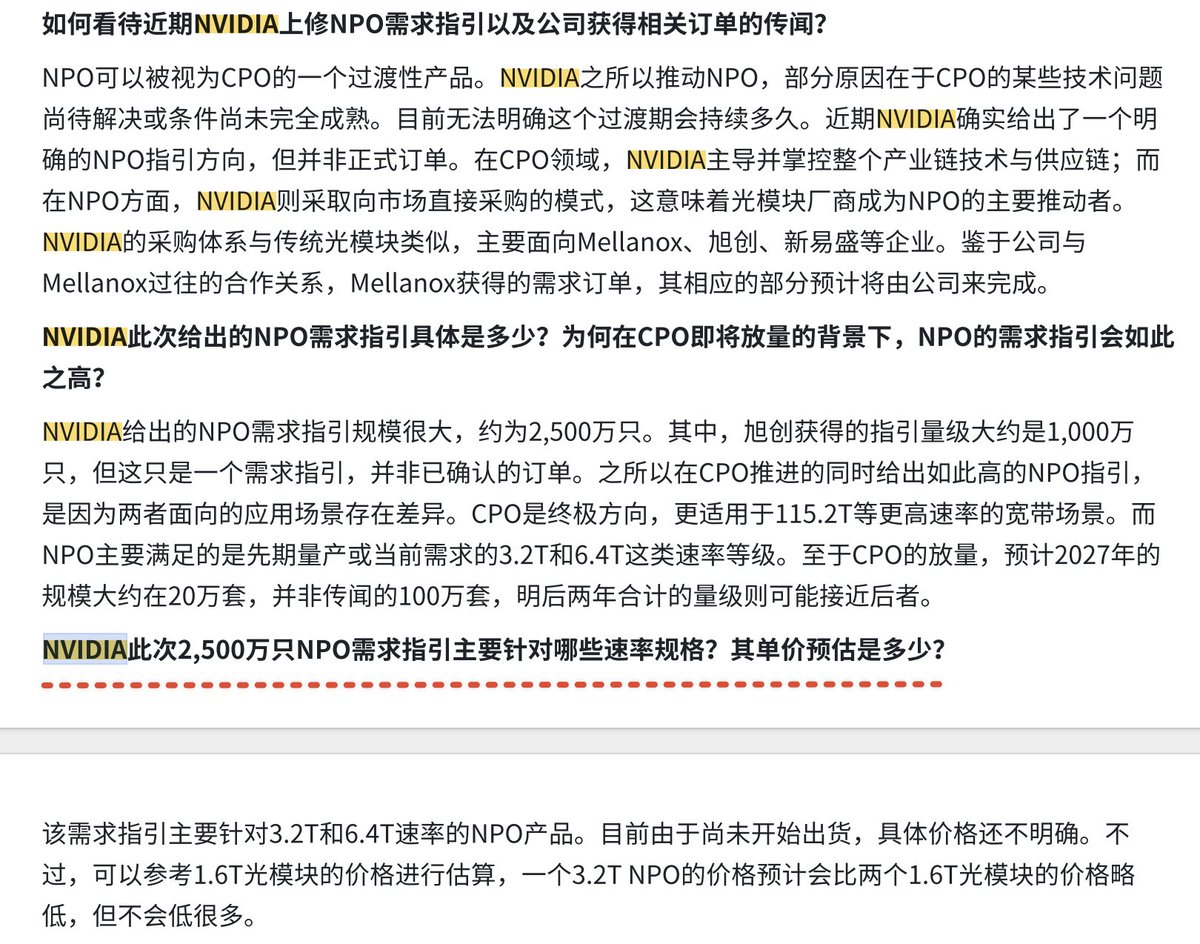

英伟达给了 2500 万只 NPO 需求指引?

旭创1000万只指引,约160亿美元=1140亿人民币。旭创2025年全年营收382.4亿,光NPO这一块相当于现有体量的3倍。打五折也有570亿,相当于再造一个半旭创。

这就是牢美开了新易盛和中际旭创二倍做多的理由了?

以及机构上调了旭创目标价到 1650 的核心原因也是因为 NPO 要放大量。

14

19

117

42,225

Jun 13

New to technical analysis. How bullish is this weekly bull flag hammer prior high support? $MXL

1

387

Jun 12

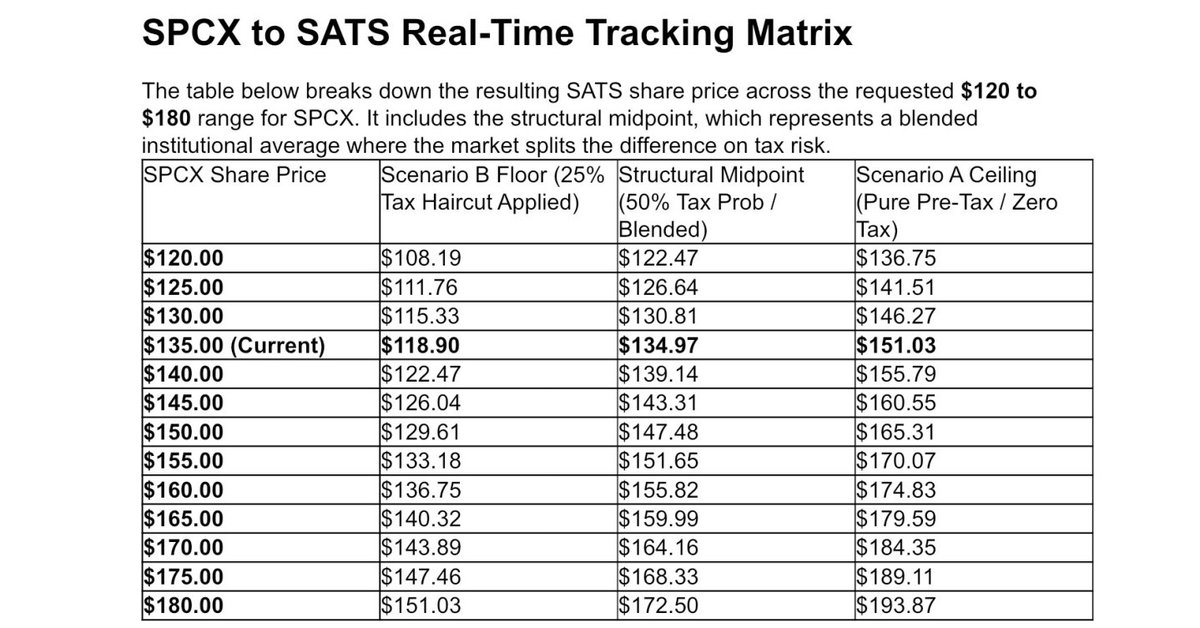

If you want to be a long term investor of SPCX, buy $SATS.

Its market cap is 32B, but its SPCX holding worth 43B, and they have other business worth about 30B, with ~15B debt.

The discount in $SATS now is caused by those who cannot sell SPCX (PE/VC/Employee/IPO). So they short $SATS to hedge.

The discount window will close when they are allowed to sell. The first batch will be unlocked when SPCX's price is above 30% of its IPO price ($135), aka $173.5, for 5 days.

$SPCX is now $175.5. So the probability that this discount disappear in next week is greater than 30%.

So buy $SATS, if you believe in Elon and in $SPCX.

23

15

296

91,346

Jun 13

Correction: the unlock schedule is here, not anything sooner than the first earnings

x.com/labubu_trader/status/2…

5

2,789

Jun 12

For a amateur stock, what makes it the top trading volume in R2K, way over its peers? $SPCX hedgehogs. SATS has 30% open short interest. When they cover their shorts, the upside is insane. The short hedgers will lose money here but they don't care because they made money from SPCX. That's the alpha we want to earn.

5

4,534

Jun 12

The NAV of $SATS is $180 as of now. It is traded at $108. Someone do the math. Even considered discount this is still insane.

5

5

27

4,515

Jun 12

Jun 12

If you want to be a long term investor of SPCX, buy $SATS.

Its market cap is 32B, but its SPCX holding worth 43B, and they have other business worth about 30B, with ~15B debt.

The discount in $SATS now is caused by those who cannot sell SPCX (PE/VC/Employee/IPO).

The discount window will close when they are allowed to sell. The first batch will be unlocked when SPCX's price is above 30% of its IPO price ($135), aka $173.5, for 5 days.

$SPCX is now $175.5. So the probability that this discount disappear in next week is greater than 30%.

So buy $SATS, if you believe in Elon and in $SPCX.

712

Jun 12

散户的悲哀,就是太依赖于timing。想投一个东西,必须的得清仓其他没什么错误的投资。如果timing不好投错了,两边挨打。我的大账户岿然不动,稳定增长。无税小账户,一会儿想干点这个,一会儿想干点那个,总是得把前面看好的给卖了。这不,这边又被SATS干了,那边清掉的仓位ripping。

1

310

Jun 12

OK, space stocks plunging because their function as $SPCX proxy has ended. What's next? A start of the new space era.

698

DegenQuant retweeted

Jun 12

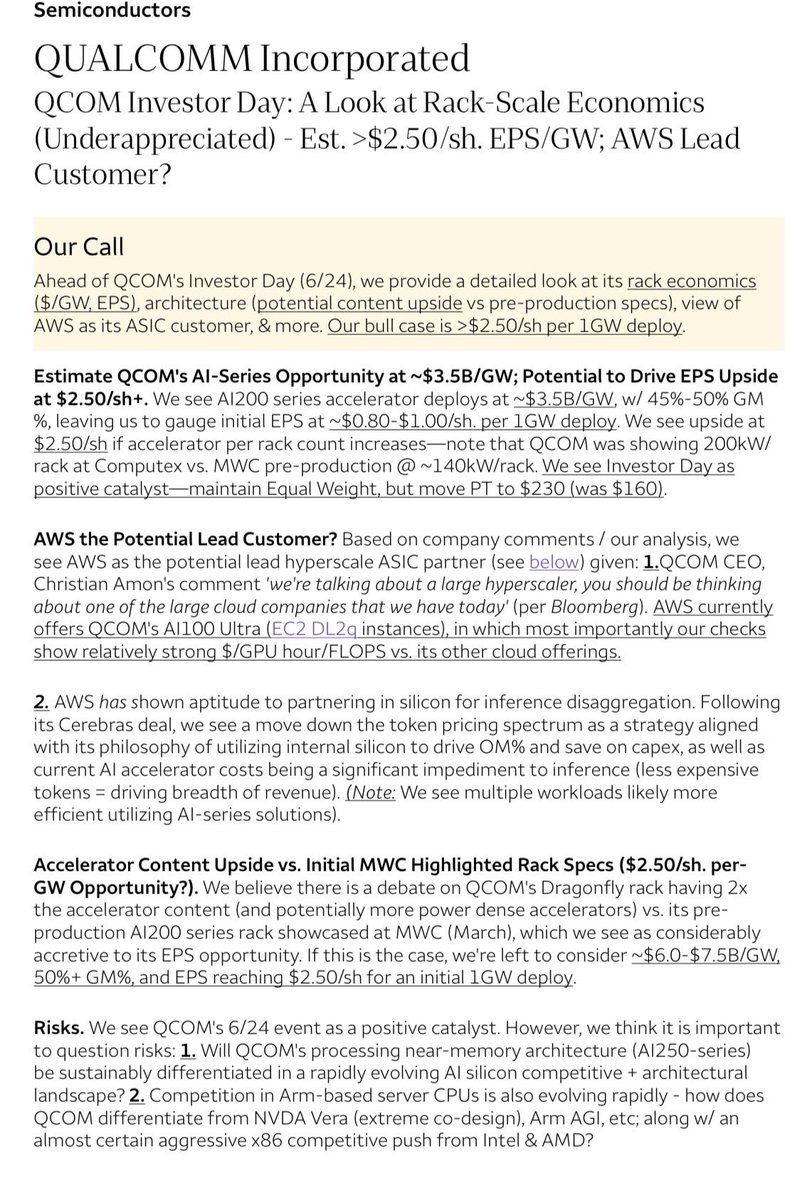

$QCOM Wells Fargo:

“Based on company comments / our analysis, we see AWS as the potential lead hyperscale ASIC partner”

May 27

$QCOM: Digitimes reporting:

"Qualcomm has "more than one" ASIC project customer."

"It is understood that another of the four major US cloud service providers (CSPs) is currently collaborating with Qualcomm on a project."

digitimes.com.tw/tech/dt/n/s…

3

17

91

16,058