The cost of computing has decreased, but the cost of thinking is what it always was...

Joined November 2013

- Tweets 2,270

- Following 1,248

- Followers 1,241

- Likes 41,330

364 Photos and videos

Pinned Tweet

Mar 16

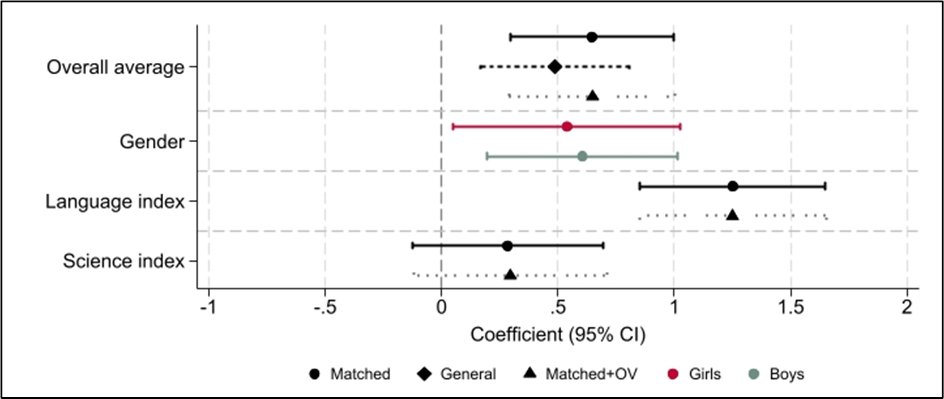

#econtwitterNew paper: An Olympic Opportunity? joint work with @EKyrkopoulou & @EliasPapaioann2

You know all about the #MovingtoOpportunity program, a randomized housing mobility project in five US cities.

Now, you are going to learn all about the #Olympic #Opportunity!

1

13

1,065

Christos Genakos retweeted

Jun 12

Στρατηγική είναι η υλοποίηση. Η φιλοσοφία που ενέπνευσε το gov. gr διαμορφώθηκε χρόνια νωρίτερα στο Λονδίνο, μέσα από ένα βιβλίο που έγινε το εγχειρίδιο του ψηφιακού μετασχηματισμού για κυβερνήσεις σε όλο τον κόσμο.

wired.com.gr/article/i-strat…

1

4

12

1,226

May 30

One more amazing @cepr_org Applied #IO at the #eternal #city with a fantastic lineup of #speakers and #Italian #food and #hospitality at Luiss Uni. Super 🙏 to @EmilioC_ & @fschivardi

1

13

609

Christos Genakos retweeted

Brexit will kill every prime minister who doesn't kill Brexit

179

1,386

16,776

384,200

☘️😱 𝝩𝝤 𝝖𝝙𝝞𝝖𝝢𝝤𝝜𝝩𝝤 𝝨𝝤𝝪𝝩 𝝩𝝤𝝪 𝝬𝝚Ϊ𝝛-𝝢𝝩𝝚Ϊ𝝗𝝞𝝨 𝝥𝝤𝝪 𝝚𝝙𝝮𝝨𝝚 𝝩𝝜 𝝢𝝞𝝟𝝜 𝝨𝝩𝝤 𝝥𝝖𝝢𝝖𝝝𝝜𝝢𝝖Ϊ𝝟𝝤 𝗔𝗞𝗧𝗢𝗥

🙇 Φοβερό! Ασύλληπτο! Μα είναι για break!

🚨 Αυτό είναι το buzzer-beater του Νάιτζελ Χέιζ-Ντέιβις που.... ξέρανε τη Βαλένθια μέσα στο σπίτι της, σε νεκρό χρόνο, κάνοντας το "πράσινο" 2-0 στα play-offs.

2

11

106

4,720

Apr 30

I found this post very #intriguing, I can't stop #thinking about it! In addition, #AI is re-drawing job (and likely firm) boundaries, because it is re-shuffling which tasks are #bundled together.

Any thoughts? @lugaricano @raffasadun @alexolegimas @I_Am_NickBloom @johnvanreenen

Apr 29

Milgrom and Roberts (AER 1990) noticed something that should have been obvious but wasn't. Firms modernizing their factories don't pick management practices off a menu one at a time. Just-in-time delivery, flexible machines, statistical process control, cross-trained workers; these arrive in clumps, or barely at all. The standard intuition is that you optimize each practice on its own and adopt what pays. The data suggested the practices were linked, not independently evaluated.

Their answer, formalized using lattice methods from Topkis (1978), is that the practices are complements: each one raises the payoff of the others. Cross-trained workers gain little without flexible machines, and process control is wasted without just-in-time. The right unit of analysis is the bundle, not the individual practice. With complementary practices, the optimum moves coherently. When conditions favor modernization, all of them rise together, and mixed configurations underperform either coherent system.

That much is the paper. What I find more interesting, three decades on, is what it points to.

Complementarity is one of the forces that pulls attributes inside a single boundary. Features get bundled into one product when they're complementary in consumer use. Practices get bundled into one management system when they're complementary in production. Activities maybe get bundled into one firm when they're complementary in some deeper sense. Where attributes are independent or substitutable, they tend to separate out and trade through markets. So there's a unifying meta-theme: complementarity is one driver of where we draw circles.

But here's where I get less sure. The classical theory of the firm (Coase, Williamson) doesn't explain firm boundaries with complementarity. It explains them with transaction costs and asset specificity, the friction of contracting and bargaining when people can hold each other up. Hart's incomplete-contracts work gets closer to a unified picture, since residual rights matter precisely when complementary investments need protection. But the transaction-cost story and the complementarity story aren't obviously the same story.

Or maybe they are. The right primitive may not be either of them in isolation. Transaction costs in the Williamson sense include haggling, information asymmetry, and adaptation costs. Once you allow information asymmetry into the picture, what looks like "complementarity" might just be an artifact of imperfect information about how attributes actually interact. Or complementarity might be the primitive, and transaction costs are the symptom: we draw firm boundaries around complementary activities because the alternative — contracting around complementarity through the market — is too hard.

I don't have a settled view. The puzzle is whether we need a unified theory of where boundaries form (around features into products, practices into systems, activities into firms) or whether each kind of boundary has its own logic. Milgrom and Roberts gave us one piece. The rest is open.

Paul Milgrom and John Roberts, "The Economics of Modern Manufacturing: Technology, Strategy, and Organization," American Economic Review 80 (June 1990): 511-528.

cc @DAcemogluMIT @profholden @ben_golub @florianederer — what do you think the right primitive is for explaining where boundaries form? Complementarity? Transaction costs broadly construed (including information asymmetry)? Something else? Or are these distinct questions that shouldn't be unified at all?

2

159

Apr 28

You think, it's just an oil shock? Think again! Amazing work from @evgenia_passari et al!

1/13 As Middle East tensions escalate, markets fixate on oil prices. But our new research suggests the economic fallout from Iran conflict goes way beyond oil as the Strait of Hormuz—a critical chokepoint—remains closed, with some countries facing harder recoveries than others 🧵

2

2

393

Christos Genakos retweeted

His dancing is even worse than his economics.

But his politics are worse than his dancing.

Guess it was always going to happen… Yanis Varoufakis dancing at a conference in Moscow to the viral techno track about himself, made by Russian DJ Sasha Melior.

5

5

88

8,199

Christos Genakos retweeted

Mar 25

Today we celebrate Greece’s Independence Day, a moment to honor the country’s history and enduring spirit. 🇬🇷

Ελευθερία και Δημοκρατία – Freedom and Democracy.

Χρόνια πολλά σε όλους τους Έλληνες!

58

283

1,681

36,269

New CEPR Discussion Paper - DP21319

An Olympic Opportunity

Christos Genakos @CGenakos @Cambridge_Uni, Eleni Kyrkopoulou @Yale @unipimun, Elias Papaioannou @EliasPapaioann2 @LBS

ow.ly/k71150YxZ4a

#CEPR_PE #EconTwitter

1

4

1,271

Mar 23

Big shout for this one! Such an #inspiring #story in the crazy times we live...

imdb.com/title/tt4807408/?re…

55

Christos Genakos retweeted

Read the latest @LSEblogs post "Everything you thought you knew about local markets is wrong" by @CGenakos and @thkampouris

blogs.lse.ac.uk/businessrevi…

1

1

122

Mar 19

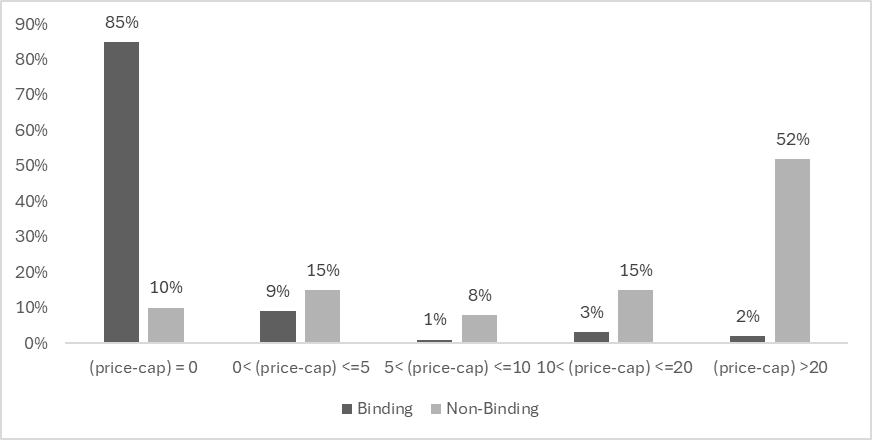

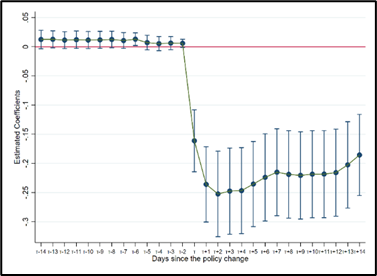

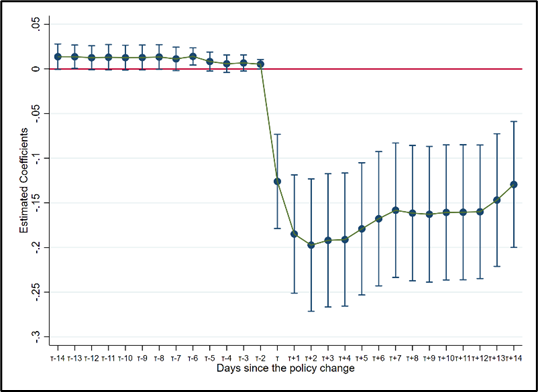

#econtwitter new wp: The Impact of #Price #Ceiling #Regulation: Evidence from #Retail #Gasoline joint work with @Stella_Papadok & Georgios Gatsios

Hey, it’s not everyday that your #research is in #sync (unfortunately) with what’s going on around the #world, so let’s dive in!

2

1

7

319

Mar 19

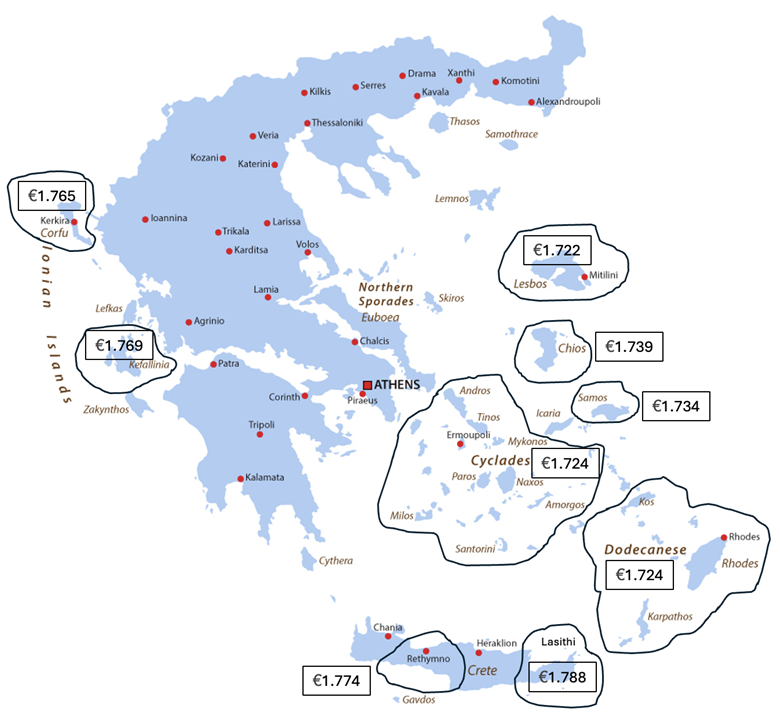

Also of interest my previous work where we show that Maximum Markup Regulation can also lead to focal point collusion: onlinelibrary.wiley.com/doi/…

42