Joined May 2021

- Tweets 4,059

- Following 0

- Followers 3,958

- Likes 1,081

137 Photos and videos

Jun 2

Wrong answer. If payback periods are 5-10years for these data centers, and about 1-2yrs for low-cost producers of the raw materials that go into the data centers, the winners will be the producers of the raw materials.

To focus on the simple, liquid, investable themes - select copper and uranium developers and miners are where you want to focus your investments.

Jun 1

Nicolai Tangen, CEO of Norges Bank Investment Management pressed IBM CEO Arvind Krishna directly on whether AI is a bubble (Save this).

And Krishna responded with what has become known inside financial circles as the $8 trillion math problem.

A single gigawatt of AI data center capacity filled with accelerators, liquid cooling, and power infrastructure costs roughly $60 to $80 billion to build and populate.

The industry has committed to more than 100 gigawatts of buildout globally.

That is $6 to $8 trillion in capital expenditure and because AI grade hardware depreciates on a five-year cycle, that entire sum must be effectively replaced and refreshed every five years.

To service the interest on $8 trillion in capital at a conservative 10% borrowing rate, the AI ecosystem would need to generate approximately $800 billion in annual profit, a number that currently exceeds the combined net income of every large technology company in the world.

Goldman Sachs estimates $7.6 trillion in aggregate AI CapEx between 2026 and 2031 alone, and Reuters Breakingviews has flagged that even if the capital is available, physical bottlenecks power permits, land, cooling infrastructure, and electrical grid connections mean that half of the planned data center projects are being cancelled or delayed before they ever go live.

Krishna also raised a second, structurally distinct concern that markets have largely ignored.

He argued that the largest foundation models, GPT, Gemini, Claude, Llama are converging toward commodity status.

When a product is a commodity, switching costs collapse.

When switching costs collapse, pricing power evaporates and margins compress regardless of how much capital was spent building the capability.

Morningstar's equity research team conducted a review of 132 technology companies in 2026 and found that AI had caused moat rating downgrades across roughly 40 major stocks concentrated in enterprise software, IT services, and SaaS with Adobe, Salesforce, Workday, and ADP among the companies whose competitive moats have materially weakened.

The implication is that the companies spending the most on AI model development may be building an asset that is simultaneously the most expensive to produce and the most difficult to monetize with durable margins.

This bear case is serious but it is also incomplete and that is what makes Krishna's framing so important to understand precisely.

When pressed further, Krishna explicitly said he does not believe there is an AI bubble in the technology itself only in a subset of the infrastructure capital that is being deployed against speculative assumptions rather than proven demand.

He draws the same analogy, the fiber optic overbuild of the late 1990s. Dozens of companies went bankrupt laying cable that nobody was using.

And yet that exact "wasted" infrastructure became the physical backbone of every cloud company, every streaming service, every mobile network, and every modern AI training cluster that followed.

The builders lost, the infrastructure won.

And the companies that were built on top of it, Amazon, Google, Netflix, Salesforce compounded for two decades.

The question, as Krishna framed it, is not whether AI is real.

It is which capital deployment earns a return versus which gets stranded and crucially, whether you own the stranded assets or the companies built on top of them.

On winners, Krishna was direct that distribution is the moat on the consumer side, and enterprise is wide open.

The data supports this, Meta with 3.3 billion daily active users across Facebook, Instagram, and WhatsApp is building AI into a distribution network that no startup can replicate at any cost.

Meanwhile, the productivity evidence arriving in real time is beginning to challenge the bear case's revenue projections.

Jensen Huang just showed on stage at Computex that GitHub commits, the universal measure of global software output nearly tripled in the first months of 2026, effectively converting $3 trillion in developer salaries into $9 trillion in productive output.

That is measurable, real time economic value already flowing through the system and it feeds directly back into token demand in a compounding loop that Krishna's static CapEx math does not fully capture.

1

11

1,213

Jun 2

Resource Nationalism 2.0

With this strategy, they work to nationalize the cash flows instead of the assets…

2

11

1,496

May 9

Early in my career, I remember the China-based CLSA autos analyst telling me that “everything is illegal in China - they just choose to enforce laws when it is convenient, but anyone can go to jail at any time.”

I always remember that when I see “corruption purges” in China. They are ALL on the take - but if they run afoul of the boss, they disappear - quickly and forever.

What else did these guys do - or not do? Lots of “corruption purges” going on in China these days…

theguardian.com/world/2026/m…

3

3

12

2,820

May 9

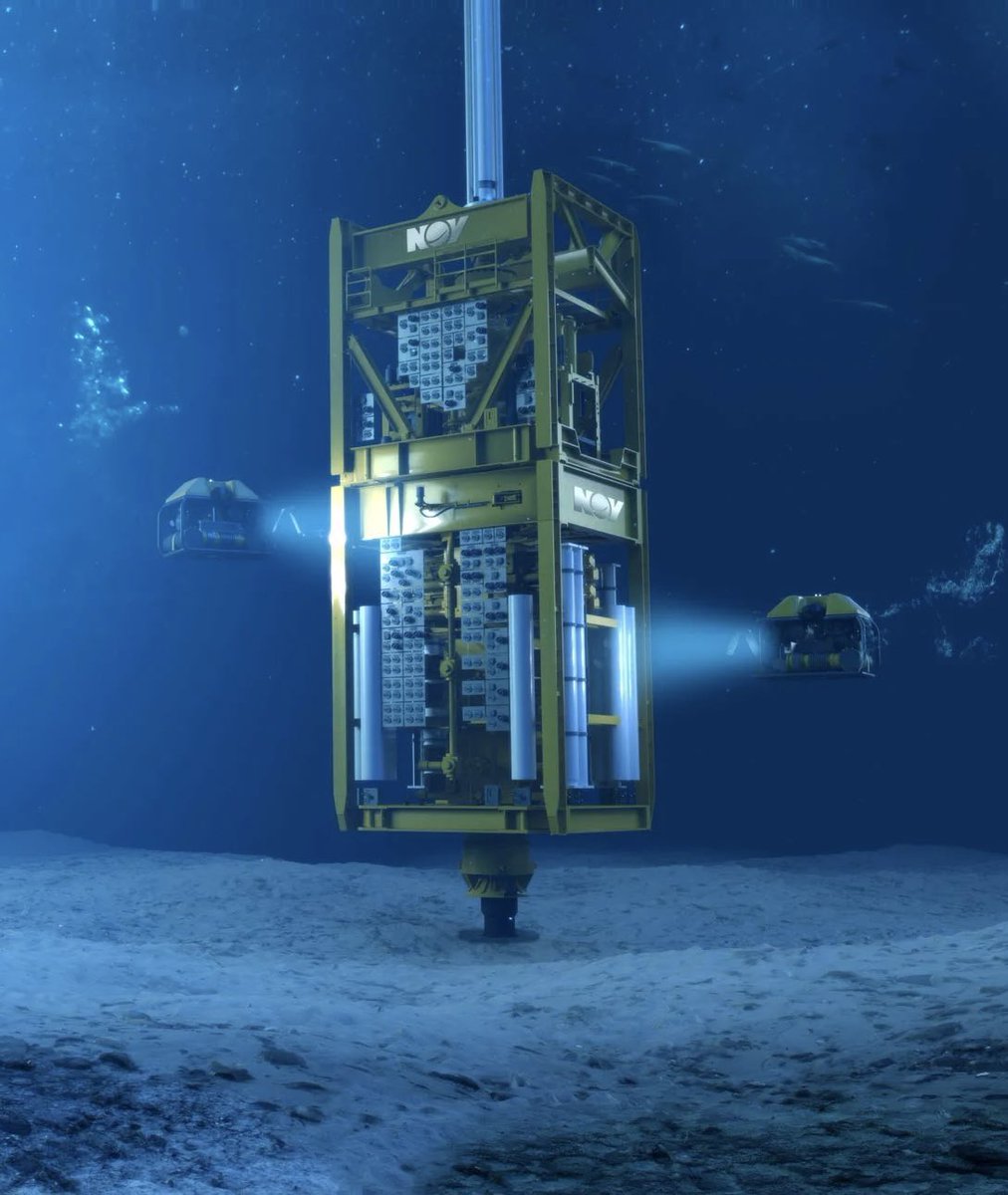

Those of us who were big investors in Anadarko or $BP back in April 2010 certainly got an education in BOPs!

May 8

Subsea Blowout Preventers (BOPs)

This is the technology that allows us to drill oil and gas wells under the sea, that red circle in the left image is an offshore worker for scale.

The image on the right shows a subsea BOP sitting on top of a subsea wellhead.

I guess most people have no idea that these systems even exist, so let’s have a look at what they are and how they work.

The purpose of a Blowout Preventer is to prevent blowouts. So what is a blowout?

Wells are so deep that the pressure at the bottom of the well can be 10,000-20,000 psi, this is 1,000x more pressure than atmosphere.

What that means is that wells always want to explosively vent their entire reservoir contents into the sky, and oil reservoirs typically contain a few hundred million tonnes of carcinogenic crude oil.

If a subsea oil well has a blowout, then you can accidentally poison an ocean. This famously happened to BP in 2010, when the Deepwater Horizon BOP failed.

When you drill a well, your “primary barrier” is your drilling mud. This is a heavy liquid that you pour into your well and the hydrostatic pressure of this dense mud is heavy enough to keep the contents of the reservoir at the bottom of the well.

A well is a deep hole filled with a mud that has a density of 1.0 - 2.4 kg / litre, the denser the mixture of mud, the greater the pressure at the bottom of the well.

The job of a drilling engineer is to keep the mud weight such that the contents of the reservoir stay put, without all the mud flowing into the reservoir.

If the density of the fluid in the well drops, eg it gets replace with oil or water instead of mud, then the pressure is such that the well will start to “unload”, which means it will flow to the surface.

A BOP is used as an emergency backup system, so that when the drilling mud has a problem you can slam shut the BOP valves and stop the well unloading.

Once a well starts to unload there is no force in nature to stop it. You get 1 shot at preventing the blowout.

Usually you will have drill pipe insider the well too, running from the rig all the down the riser and all the way into the well. This complicates closing the BOP somewhat, so BOPs are designed to shear drill pipe insider two when they close.

Drill pipe is 6in diameter toughened steel. Cutting it with a valve that also has to seal 10,000psi to avoid poisoning an ocean is no mean feat.

Doing this remotely under 2 miles of seawater is even more challenging.

But these systems exist, every offshore drilling rig has a BOP, it’s 450 tonnes of steel forgings, high pressure pipework, controls, and the most incredible sealing technology known to mankind.

Around 30% of the world’s oil supply is produced offshore using technology like this. This is the upstream industry that produces 1/3rd of all fuel, plastic, fertiliser, you name it, this is how we do it.

We’ve been doing this for 50 years.

8

1,862

May 9

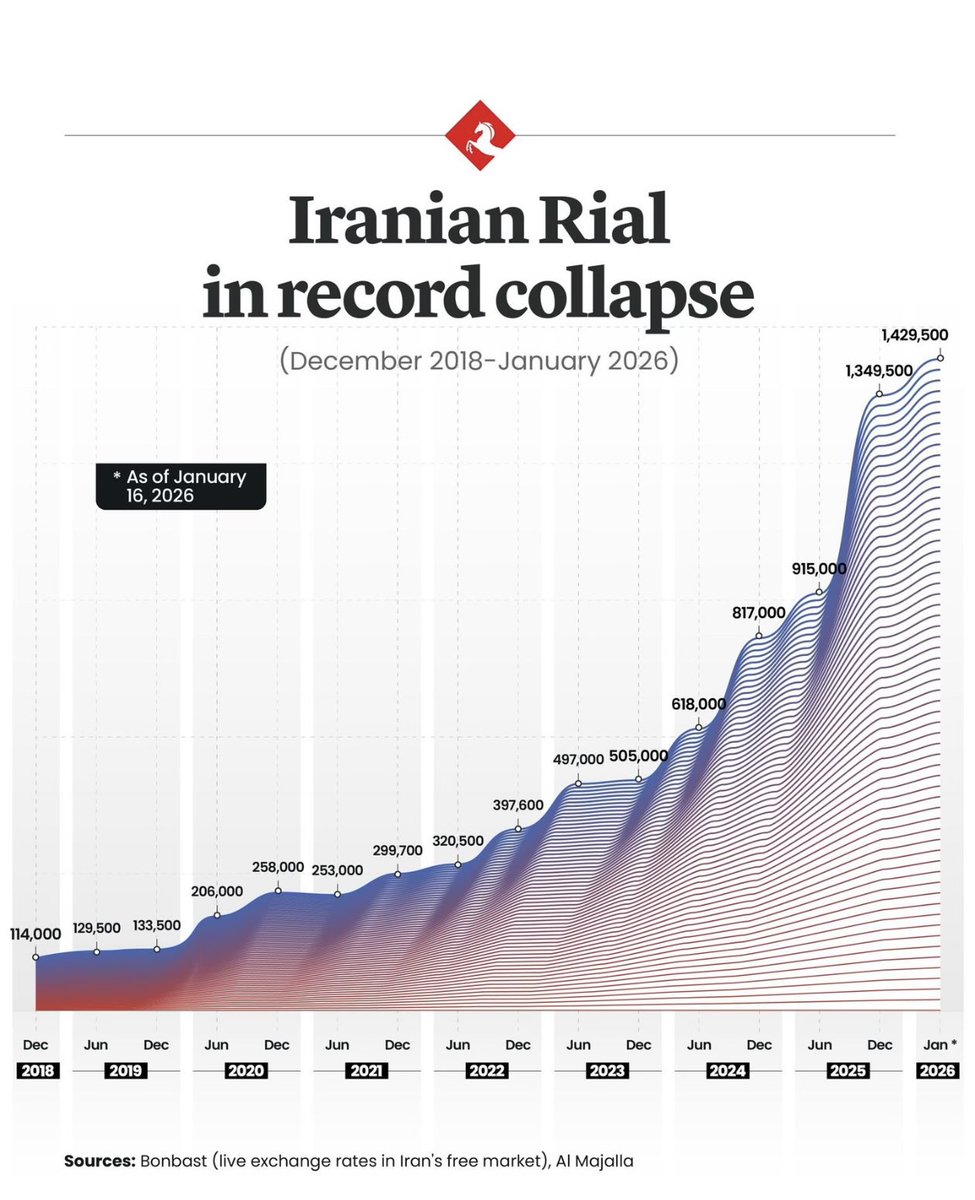

Reason #1 why the status quo is unsustainable for Iran (and this is even old data)…

May 9

I hear this quite a lot--if Iran can withstand US pressure, what's to stop them from continuing this standoff indefinitely?

The leadership wants a deal to end the war--resolving the confrontation on favorable terms is the endgame, and ultimately why they fought the war as aggressively as they did.

A perpetual state of "no war, no peace" is not their preference. Nor is it sustainable.

3

5

1,736

May 9

Resource nationalization 2.0…

May 8

Lula just signaled the biggest shift in Brazilian critical mineral policy in 50 years.

The Brazilian Chamber passed a bill 24 hours before the May 7 White House meeting that restricts raw mineral exports, creates a R$5 billion processing fund, and offers a 20% tax credit for refining plants built on Brazilian soil.

This is the same playbook Indonesia ran in 2014 with nickel, scaling that industry from $1 billion to $30 billion in nine years.

Brazil is running it on 25 minerals at once.

Read the full breakdown here...

x.com/drewcrawford_/status/2…

2

22

3,592

May 9

Great margins - until they run head-first into the wall of raw materials energy constraints.

Then, those margins migrate upstream…

1

11

1,329

May 9

I’m deeply disappointed that there do not seem to be any good public explorers / developers / miners / processors of magnesium to invest in.

Magnesium is one of the key themes I’ve been following, but no way to express the view with public mkt liquidity.

Am I missing anything?

May 9

Magnesium isn’t rare but China produces 88% while the West shut down its own capacity in the 90s and never rebuilt it

In 2023, China produced 830,000 metric tons of magnesium - 88.4% of global output.

That figure has held for two decades, while EV adoption accelerated, while lightweighting became a strategic requirement, and while magnesium content per vehicle began rising from its baseline of approximately 5 kg toward China's mandated target of 45 kg by 2030.

Magnesium is not a rare or exotic material. It is one of the most abundant elements in the earth's crust. It can be extracted from magnesite - which China has in vast domestic reserves - and from seawater, present everywhere.

The United States and Europe produced significant quantities of magnesium from seawater until the 1990s, when Chinese output scaled rapidly, driven by lower energy costs and government subsidies, it flooded export markets and made Western production uneconomical.

The industrial infrastructure was dismantled. The process knowledge was not maintained. The supply chain dependency became structural.

The stakes go beyond automotive. Magnesium is a critical input for aluminium, titanium, and steel alloys. Military equipment relies on it.

The list of sectors where a supply disruption would have immediate consequences is long.

The EV industry expanded rapidly on the assumption that critical materials would remain accessible through global trade.

That assumption is now being re-examined across rare earths, battery minerals, and semiconductor inputs.

Magnesium has not received the same attention. It should.

❌ Don't leave your insights to chance with the X algorithm

✅ Subscribe for free to my weekly newsletter about all things Gigacasting and magnesium Thixomolding: industryarsenal.com 📬

7

17

3,320

May 9

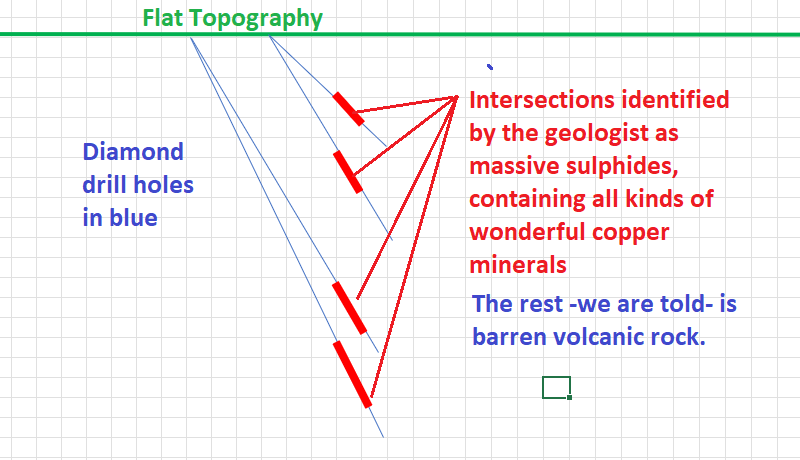

Excellent analysis and explanation by Professor Ringdahl :)

Take some time and read through this once or twice.

Thanks for putting this together @NeilRingdahl!

May 8

1) From Drilling to Open Pit Optimization For Dummies.

(An updated 🧵)

Imagine you have project and hire a truly great geologist who has drilled some fantastic looking sections based on a small surface anomaly he found from a surface geochemistry sampling program.

1

4

1,069

May 9

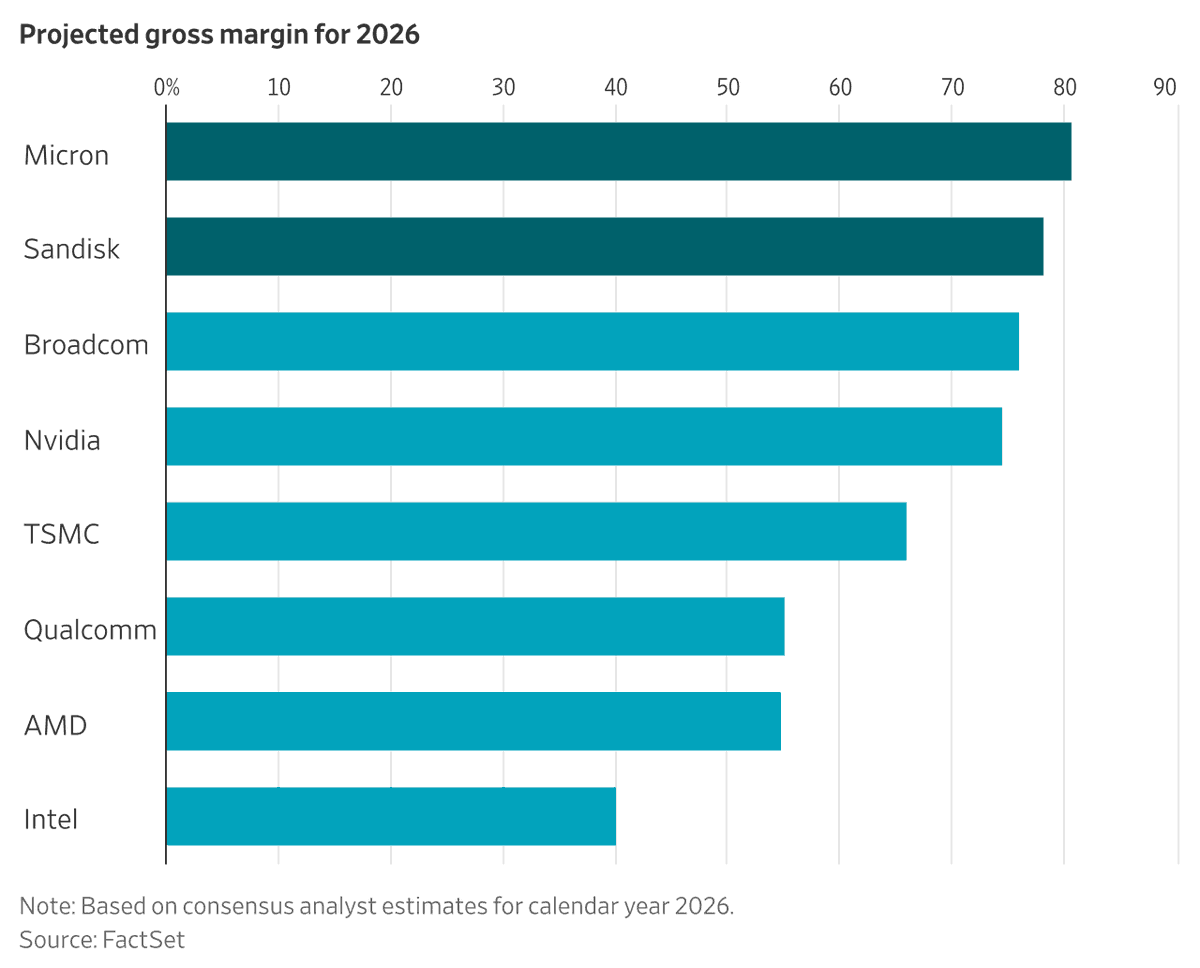

Raw materials AND processing constraints are the real bottlenecks for data centers, AI, etc, etc.

The cycle always follows the same pattern, with constraints and operating margins going upstream - eventually to the miners.

Invest accordingly!

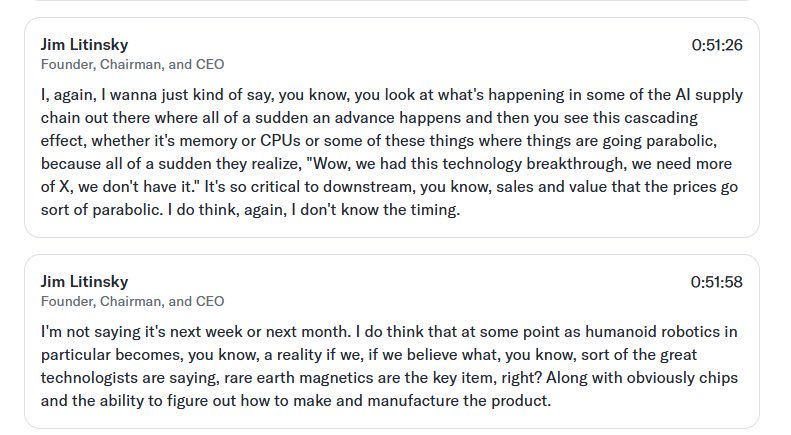

$MP CEO Jim Litinsky believes NdPr magnets could become the next “memory chip” style supply shock.

As AI, humanoid robotics, and advanced technologies scale, rare earth magnet demand could hit a point where the market suddenly realizes there simply isn’t enough supply.

1

18

1,180

May 9

It's also no surprise that many of these NGOs are unknowingly funded by mining companies and other groups who are threatened by the advent of deep sea mining with $TMC $OMEX and others...

A new paper in @NatureEcoEvo says what NGOs will not: targeting the development of seabed minerals with delay tactics has real costs in a world defined by trade-offs, and will likely cause irreversible harm to unique and biodiverse rainforest and coastal ecosystems.

nature.com/articles/s41559-0… #deepseamining

2

1,388

May 9

Reason # 5,832 why I don't typically like to invest in operating companies.

I always felt that Grasberg was much higher risk to $FCX than the market reflects.

That said, the lost revenues from Grasberg disappointing might juice copper prices enough so that $FCX still benefits.

But I'd still rather invest in the explorers / developers...

Freeport Indonesia pushed back the full restart of its giant Grasberg copper mine by a year, worsening supply constraints that are already impacting the global market for the metal bloomberg.com/news/articles/…

1

28

3,406

May 9

Energy is the biggest constraint when it comes to data centers.

In fact, energy is either the fuel (literally!) or the constraint for global growth. Current fundamentals are shaping up to be much more of a constraint - and not just for data centers in frontier markets...

Kenya🇰🇪 suspends $1 billion Microsoft data centre as energy shortfall raises doubts over Africa’s AI ambitions

Kenya’s plans to host a $1 billion data centre backed by Microsoft and UAE-based G42 have stalled, after President William Ruto said the country lacks sufficient power capacity to support the project.

1

5

855

May 9

This is the right call.

Investment flows are already moving into critical minerals energy.

More and more "commodity tourists" (aka, generalists) are starting to show up...

May 7

Steve Hanke, Professor of Applied Economics, says the world is rearming and arms need raw materials.

Since December, tantalum is up 133%, lithium spod 52%, niobium 28%, and gold is still heading to $6-7K. Move out of high tech, get into hard commodities. We're in a super cycle

6

1

36

3,490

May 9

From HODL to "never sell" to this.

Not exactly the diamond hands he advertises.

His aura (to the crypto bulls) is certainly cracking...

May 7

Buy more bitcoin than you sell.

6

533

May 9

"Compute" is just a derivative of energy critical minerals...

May 7

The CEO of the world's largest asset manager just said something that should reframe how every investor thinks about the AI trade.

Larry Fink, managing $11.5 trillion at BlackRock, stood at the Milken Institute Global Conference and said four words that matter, "We just don't have enough compute."

"The United States is short power. We're short compute. We're short chips. And there's going to be shortages in all three and memory, four things. I actually believe a new asset class will be buying futures of compute."

Think about what that means.

Fink is predicting that compute becomes a tradable commodity like oil, like grain, like natural gas where investors buy forward contracts on future capacity because the shortage is so structural and so predictable that a derivatives market will emerge to price it.

That is not a minor observation from a finance executive but rather the chairman of the most powerful capital allocator on the planet telling you that compute scarcity is a multi-year, investable megatrend.

The data backs him up completely.

Data centers will consume 70% of all memory chips produced globally in 2026.

Advanced HBM production from Samsung, SK Hynix, and Micron is sold out through 2026 and into 2027 and a single AI server consumes 10-20x more memory than a conventional workload server.

DRAM supply growth is running at just 16% annually while AI infrastructure demand is growing at 80% .

The chip crunch, the power crunch, and the compute crunch are not temporary dislocations, they are structural, and they will get worse before they get better.

Fink also said something the bears keep getting wrong: "There is not an AI bubble. There is the opposite. We have supply shortages. Demand is growing much faster than anyone has ever anticipated."

This is why the Milk Road Pro portfolio is built the way it is, long the companies producing and supplying the constrained resources: chips, memory, compute infrastructure, and power.

Check out Milk Road Pro, link below to access our full thesis and plays.

2

14

1,414

May 9

Stan the Man continues his fall from grace.

Safe to say, he won’t be hosting meetings from a yacht at BMO anymore.

I remember about 15yrs ago, going to his yacht for a meeting, and Stan had just come out of his pool, still dripping wet in his swimsuit, to meet with us…

12

3,027

May 9

Crude oil is one helluva (high margin) drug!

Hard to just let it go…

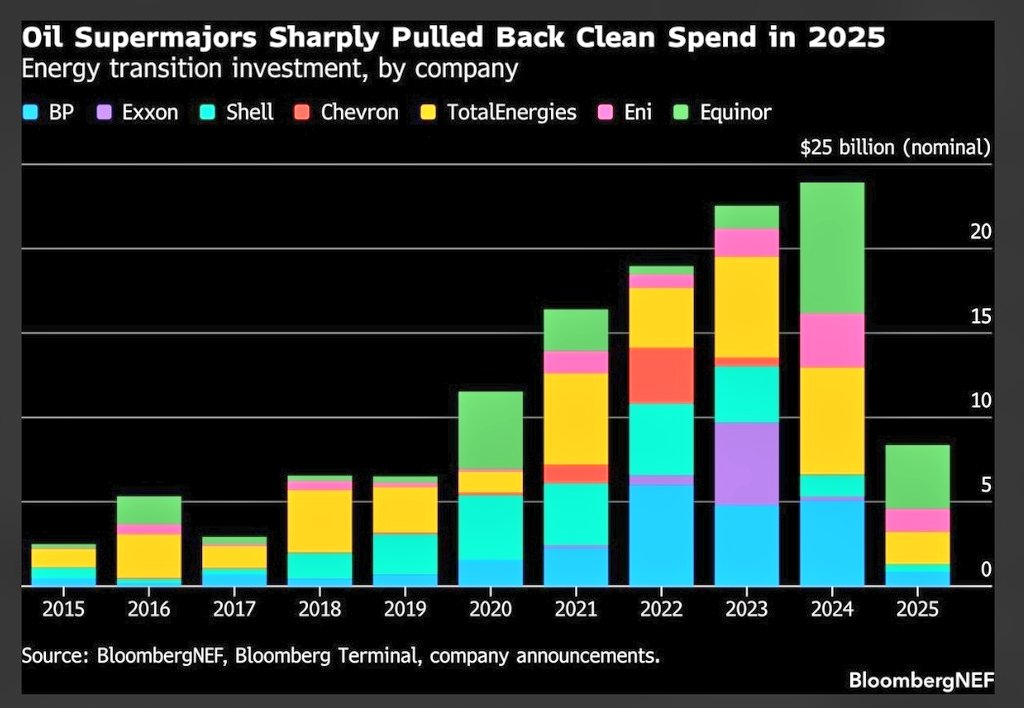

Spending on the so called green energy is shrinking fast . The U-turn is real .

1

11

1,333

May 8

I feel you!

The capital will flow to the sectors upstream of the semis/AI sector.

As margins compress and growth begins to fail due to constraints, investors will look for the next related trade.

And that’s where we are already sitting - with plenty of chips on the table!

May 8

I am confident enough in myself to say that I feel like I'm the only person not making life-changing money in semiconductors and AI stocks.

Like I completely missed it.

So now I feel the desire to buy "the next rotation."

I don't know.

Hope my insecurities help others.

4

1

34

8,284

May 7

Looks like a lot of things that will break…

China is waging a serious ‘war’ against Western car manufacturers. This is not normal bro. 😂

🏷️ $80,000

3

12

2,277