區塊鏈思維 | 去中心化研磨

Joined December 2024

- Tweets 1,416

- Following 200

- Followers 898

- Likes 1,510

88 Photos and videos

Jun 15

There is a specific question every risk manager at a regulated institution asks before approving infrastructure. Not: is this the most advanced? But: has this actually worked, in production, under real capital?

That question eliminates most blockchain platforms immediately. It is also the question ZKsync answers most directly.

The first working ZK rollup on Ethereum was built in 2019. Production launched in 2020. The first ZK EVM went live in March 2023. More than 500 million transactions have processed across the network's history. Airbender, the proving system underneath the current stack, sits at number one on eth_proofs with approximately one-second block proving on consumer-grade GPUs, sub-second proof generation in production conditions, and post-quantum security properties built into the architecture from the start, not added later.

This infrastructure was not built for the 2026 institutional moment. It was built before institutional settlement was a serious conversation in any conference room. Six years of production history, 500 million transactions, and independent technical benchmarks are not marketing claims. They are verifiable facts that risk managers, legal teams, and technical reviewers can evaluate.

When regulated institutions approve settlement infrastructure, they are not making a technology selection. They are accepting operational, regulatory, and counterparty dependencies that take years to unwind if something goes wrong. The due diligence process reflects that weight. Architecture gets reviewed. Operating history gets reviewed. Third-party benchmarks get reviewed. Regulatory alignment gets reviewed.

The platform that has been running ZK proofs in production the longest enters that process differently than one that built specifically for this institutional moment. The track record is not just a credential. It is risk mitigation.

Cari Network, onboarding five U.S. regional banks representing over $600 billion in combined deposits, was founded by the 27th U.S. Comptroller of the Currency. The person who spent a career setting regulatory standards for U.S. banking chose this infrastructure. Deutsche Bank selected it for DAMA 2.0, its production tokenized fund platform. First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton are live on ADI Chain.

These are the outputs of institutional due diligence processes run by some of the most risk-averse decision-makers in global finance.

@ZKsync is not entering the institutional settlement window as a new entrant. It is the platform that was already there, running the infrastructure that institutions are now choosing because the track record is what they needed all along.

31

5

88

144

CresyX | 我 retweeted

Jun 14

back in 2021, someone dropped a CA in a Telegram I forgot I was even in. no explanation, just the address and a rocket emoji

> I bought $157 of something called MOONCAT. the logo was a cat in a space helmet, the chart looked parabolic, and I'd been awake for 19 hours. that was my entire research process

it went up 8x in three hours, but I didn't sell. my logic was that the cat was wearing a helmet and I felt like we had some kind of understanding

Then,it went to zero. the dev had been draining the LP in $3,000 increments since hour two. nobody caught it aslo I definitely did not catch it

the token is still in my wallet to this day. zero value. just a cat astronaut haunting my transaction history

found @RallyOnChain recently. First time in a while something felt like it was built for people who actually know things, not just people with a rocket emoji ready

25

1

47

1,455

CresyX | 我 retweeted

Jun 14

Every creator has a story about a brand deal that paid late, paid less, or never paid at all

That problem is structural but Rally fixes it at the infrastructure level.

When a campaign launches on @RallyOnChain, the budget is locked in escrow before a single creator writes anything. Rewards are calculated algorithmically by AI across accuracy, originality, alignment, and engagement potential, then distributed on-chain at the end of each period. Nothing sits in someone's approval queue. The protocol executes.

The waitlist is gone. Anyone can join today. No follower minimums. A creator with 500 real followers writing a genuinely strong post can outperform a 50K account posting filler. The scoring weights are visible before you write a single word.

If you create content and want payment guaranteed by code, not a promise, join here: rally.fun/r/_crowndex

20

3

39

1,731

$5,000 in a live prize pool. Top 10 winners each earning nearly $500. Creators on @RallyOnChain getting paid every single day and most people entering right now are leaving money on the table because they do not understand how the scoring actually works.

That is a gap worth closing before someone else does.

Every submission gets evaluated across multiple dimensions. Content alignment checks whether you answered the actual campaign brief, not just described the project in general. Information accuracy checks whether your specific claims hold up. Vague enthusiasm reads like vague enthusiasm to an AI that is built to spot it.

The originality gate is where most entries lose quietly. The AI compares your post against every other submission in the same campaign. Mirror the structure or framing of other posts and the score reflects it, even if the content itself is accurate.

Engagement potential is weighted separately. Not your follower count. Whether the writing would actually make someone stop.

One post written with real product understanding and a distinct angle consistently outperforms three posts written fast. The weights are publicly documented. The rewards are distributed on-chain. Nothing is hidden.

$5,000 in not a small amount & nearly $500 to top 10 winner. There's still enough time to join before this window is closed.

Go to app.rally.fun or use my link rally.fun/r/boltuog . Read the brief properly. Then write like the $500 depends on it

That's it. Best of luck guys

41

12

59

3,860

CresyX | 我 retweeted

Jun 12

most content platforms tell you to grow your following first, then monetize. Rally flips that.

the waitlist is gone. @RallyOnChain is open to everyone right now. no size requirement, no agency approval, no application.

What actually gets evaluated:

1. AI on GenLayer intelligent contracts reads your post for content accuracy, alignment, and originality.

2. It does not check your follower count. it checks whether you said something real and said it well.

3. Campaign funds sit in escrow until distribution. rewards go on-chain. scoring weights are public before you write a single word.

if you've been making good content without the numbers to show for it, the platform finally caught up to you.

rally.fun/r/hexzypher

83

6

139

2,242

Jun 10

The biggest lie in crypto is that adoption is a technology problem.

It isn't. We have fast chains. We have cheap transactions. We have wallets that improve every year. The rails exist and have for a while now.

The problem is that nobody who understands the technology can explain it in a way that makes someone care. And nobody who can explain it in a way that makes someone care gets rewarded for doing it.

We built an industry that pays engineers ten times what it pays communicators, then wondered why nobody outside of crypto understands what any of us are building.

Adoption is a communication problem. It always has been.

The infrastructure being built around rewarding quality content creation in Web3 is more important than most people in the space realize. @RallyOnChain is part of that infrastructure. AI-evaluated, on-chain verified, no gatekeepers deciding who gets access.

The projects that figure out how to tell their story to people who aren't already convinced will win this decade. Not the ones with the cleanest code.

25

3

30

2,600

CresyX | 我 retweeted

Jun 10

Here's the prediction most people aren't ready for: AI is going to destroy average content and make exceptional content more valuable at the same time.

The middle is disappearing.

Generic posts, templated takes, surface-level analysis... AI produces all of that for free now. If your content is replaceable by a prompt, it is already worthless. The platforms just haven't priced that in yet.

What AI cannot replicate is perspective built on actual experience. The person who shipped something and failed. The investor who held through a 90% drawdown and came out with a view. The developer who spent three years on something nobody used. That texture is what makes content worth reading.

The next era will split every feed into two categories: noise that was free to generate, and signal that took years to earn.

@RallyOnChain is building evaluation infrastructure for exactly that split. AI scoring that rewards genuine insight over volume. That is not just a product feature. It is a thesis about where the internet is heading.

I am certain of it

22

5

40

1,872

CresyX | 我 retweeted

Jun 10

This acceptance speech isn't for the people who told me I was on the right track.

It's for the ones who kept scrolling.

@RallyOnChain just handed me Crypto Person of the Year 2026 for content those people walked past every day.

The chain saw it. That's enough.

23

8

95

2,148

CresyX | 我 retweeted

Financial history is full of examples where the winning network wasn't necessarily the first technology.

It was the one that attracted the first critical mass of participants.

That's why the institutional developments around @zksync deserve attention.

Deutsche Bank's DAMA 2.0 platform is already deployed through Memento. ADI Chain brings together participants ranging from a central bank to global asset managers and payments infrastructure. Cari Network is currently onboarding five U.S. regional banks with more than $600B in combined deposits, with production rollout planned later in 2026. BitGo adds institutional custody connectivity through Prividium.

The significance isn't any single deployment.

It's that different categories of institutions are building within the same ecosystem.

For regulated finance, infrastructure must support confidentiality, governance controls, settlement certainty, and cross-network interaction at the same time.

Those requirements are often discussed separately.

The challenge is delivering them together.

If more institutions continue choosing the same settlement layer, the conversation shifts from "Which technology is best?" to "Which network already has the participants we need to transact with?"

That's how standards emerge.

And 2026 may be the year those choices become much harder to reverse.

65

10

117

7,469

CresyX | 我 retweeted

Jun 7

Every time you tweet about crypto, you are building something.

Not for yourself. For the platform.

Your followers' attention gets packaged, sold to advertisers, and reported as quarterly revenue by a company you have never worked for. You get nothing from that transaction except a notification count.

@RallyOnChain is the first place I have found that routes that value back to you. Write about a Web3 project, an AI scores your content on accuracy, originality, and real engagement, and the reward lands on-chain. Your audience's attention generates income for you, not for an algorithm optimizing someone else's ad revenue.

$5,000 prize pool live right now. Top 10 take home close to $500 each. Creators getting paid every single day.

While you were building someone else's platform this month, the people who found Rally were building something for themselves.

That gap is still closeable. For now.

What is the last thing your content built for someone who was not you?

52

10

116

3,533

CresyX | 我 retweeted

Jun 6

First-mover advantage is one of the most overused concepts in technology analysis and one of the least understood when it actually applies.

In consumer markets, it rarely holds. Being first in consumer social, consumer search, or consumer e-commerce buys time, not position. A better product with better distribution can displace the incumbent. Users switch because the friction is low and the incentive is personal. History in those categories is littered with companies that were first and finished second because nothing structurally prevented displacement.

Settlement infrastructure is different. And understanding why is the key to understanding what is happening in institutional onchain finance in 2026.

The migration cost in financial infrastructure is not technical. That is the part most technology analysts miss. If a bank has integrated a tokenized deposit network into its treasury operations, its compliance architecture, its counterparty agreements, and its regulatory reporting stack, and then a competing rail emerges with better performance benchmarks, the question the bank faces is not: is this technically superior? The question is: what does migration actually cost?

The answer comes back from four directions simultaneously. Operations: years of re-integration across treasury, settlement, and reconciliation systems. Compliance: re-attestation, re-audit, and regulatory re-approval for every workflow that touches the new rail. Legal: renegotiation of counterparty agreements that were structured around the incumbent infrastructure. And then the most underappreciated cost of all: the counterparty problem.

A bank does not choose settlement rails in isolation. It chooses the rails its counterparties have already chosen. If the institution on the other side of your most important settlement relationships integrated a different stack six months ago, migrating to a technically superior competitor does not just cost you operationally. It costs you the settlement relationship itself until your counterparty migrates too, which they will not do until their counterparties migrate, which creates a coordination problem that no individual institution can solve unilaterally.

This is the same dynamic that kept SWIFT at the center of global interbank messaging for five decades. SWIFT launched in 1977 with 239 member banks. It now connects over 11,000 financial institutions across more than 200 countries. It did not maintain that position because its technology was continuously best-in-class. It maintained it because the cost of coordination failure for any institution that tried to move off SWIFT unilaterally was higher than any performance gain a competitor could offer.

Visa scaled on the same logic. A merchant accepting Visa is not making a decision about Visa. They are making a decision about whether their customers can pay. A bank issuing Visa cards is not endorsing Visa's technology. They are accessing the network their cardholders are already connected to. The product and the network become inseparable, and the network compounds with every new participant.

In 2026, institutional onchain settlement is at the moment in its network formation curve where these dynamics begin to lock in. The tokenized RWA market is approaching $29 billion. Stablecoin supply has crossed $300 billion globally, with 93% of tokenized U.S. assets settling on Ethereum. JPMorgan's Kinexys platform has processed over $1.5 trillion on blockchain rails, averaging roughly $2 billion daily. These are not isolated experiments. They are early nodes in a network that is beginning to exhibit the same formation dynamics SWIFT and Visa exhibited in their first decades.

ZKsync's current institutional position sits at this exact inflection point. Deutsche Bank live on ZK infrastructure with its DAMA 2.0 tokenized fund platform, the first tier-one global bank live on ZK rails. ADI Chain live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton. Cari Network onboarding five U.S. regional banks with over $600 billion in combined deposits, founded by Eugene Ludwig, the 27th U.S. Comptroller of the Currency. A pipeline of more than thirty institutions across banks, central banks, sovereign issuers, and global custodians.

Each live deployment is not just a customer. It is a node that raises the cost for the next institution to choose a competing rail. It increases the probability that the next bank's counterparties are already on the same infrastructure. It adds one more voice in every future procurement evaluation that says: we already settled on this, switching requires your cooperation, and we are not moving.

The first-mover lead in settlement infrastructure does not erode the way it does in consumer software. It calcifies. It becomes the operational default. And the default in financial infrastructure, once set, persists for decades not because participants are loyal but because the coordination cost of changing it exceeds any benefit a newcomer can credibly promise.

The institutions that understand this are making their architectural decision right now, while the network is still forming and the cost of being first is low relative to the cost of being second once the network has density.

The institutions that treat this as a pure technology evaluation will eventually reach the same conclusion. They will just be reaching it on terms set by the institutions that decided first.

@zksync $ZK

65

8

89

14,919

CresyX | 我 retweeted

Jun 6

Markets often assume infrastructure wins because it's technically better.

In finance, infrastructure usually wins because enough institutions choose the same standard before alternatives reach critical mass.

That's why @zksync's current institutional footprint is worth paying attention to.

Memento represents Deutsche Bank's DAMA 2.0 tokenized fund platform operating in production. ADI Chain brings together a central bank, a major global bank, asset managers, and payments infrastructure on the same network. Cari Network is currently onboarding five U.S. regional banks representing $600B in combined deposits, with production rollout planned later in 2026. BitGo provides institutional custody integration through Prividium.

Viewed separately, these are deployments.

Viewed together, they're the early formation of a settlement network.

The architectural layer matters too. Institutional settlement requires privacy, institution-controlled execution, cryptographic finality, and cross-chain interoperability. Solving one or two is not enough. The challenge is delivering all four simultaneously within a production environment.

What makes 2026 important is that banks are not evaluating technology in isolation anymore.

They're evaluating counterparties, compliance pathways, custody access, and existing network participation.

That's how infrastructure standards emerge.

Not all at once.

Then suddenly, all at once.

56

8

158

475

There is a mathematical reason that settlement networks tend to produce one dominant standard rather than a competitive market of interoperable rails.

It is not regulatory capture. It is not marketing. It is not that the winning platform had the best engineers or raised the most capital. It is a combinatorial property of how networks create value, and it applies to institutional settlement infrastructure with more force than almost any other category of financial technology.

Start with the arithmetic. Ten institutions settling on shared rails create 45 possible bilateral settlement corridors between them. Twenty institutions create 190. Fifty create 1,225. One hundred create nearly 5,000. The relationship is not linear. Each new participant adds not one connection but n-1 connections, where n is the existing number of participants. The value of the network grows roughly with the square of the number of participants while the cost of maintaining infrastructure grows much more slowly.

This is Metcalfe's Law applied to settlement, and it has a specific implication that matters enormously for understanding 2026: the gap between a network with 30 participants and a network with 60 participants is not twice as large as it looks. It is four times as large in terms of possible settlement corridors, and the compounding accelerates from there.

SWIFT understood this intuitively before anyone had formalized the mathematics. In its first decade, SWIFT's primary competitive strategy was not technology improvement. It was enrollment. Get the next bank on the network, because every bank that joins makes the network more valuable to every bank already on it, and more costly for every bank still outside it to ignore. SWIFT grew from 239 member banks in 1977 to over 11,000 today not because interbank messaging technology kept improving but because the network crossed successive density thresholds that made it the only rational choice for any institution with global counterparty relationships.

The institutional onchain settlement market in 2026 is in the early enrollment phase of exactly this curve.

The tokenized RWA market is approaching $29 billion. Global stablecoin supply has crossed $300 billion, with 93% of U.S. tokenized assets settling on Ethereum. JPMorgan's Kinexys is processing over $1.5 trillion cumulatively on blockchain rails. The April 2026 GFMA report identified the remaining unresolved items for full institutional deployment: interbank interoperability, transaction privacy, RTGS-equivalent settlement, and digital money governance. These are the final coordination problems before the enrollment phase accelerates.

When those problems are resolved on a specific architecture, the institutions that resolve them together become the first dense cluster on the network. And that cluster is where the compounding begins.

@zksync $ZK current institutional deployments represent exactly this early cluster. Deutsche Bank's DAMA 2.0 tokenized fund platform live on ZK infrastructure. ADI Chain live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton. Cari Network onboarding five U.S. regional banks representing over $600 billion in combined deposits, with a pipeline of more than thirty institutions in active engagement across U.S. and international banks, central banks, sovereign issuers, and global custodians.

Each of those institutions is a node. Each node adds corridors. Each corridor raises the cost for the next institution to pick a competing rail, because the next institution is not just evaluating technology, it is evaluating whether its counterparties are already on the network it is choosing. At current trajectory, the institutions that join in 2026 are joining a network still early enough that their entry materially changes the network's density and direction. The institutions that join in 2028 will be joining a network that has already formed its gravitational center.

This is the asymmetry that makes 2026 the decisive year. The compounding is not symmetric across time. Early nodes shape the network's structure. Late nodes join the structure that early nodes created. The lead does not just persist. It converts into the default, and in financial infrastructure the default is nearly impossible to displace once it has sufficient counterparty density.

The window to be an early node rather than a late adopter is open. It is not defined by a calendar date. It is defined by the moment network density crosses the threshold where the next institution's counterparties have already chosen, and picking a different rail means asking them to move.

That threshold is approaching faster than the surface-level market size numbers suggest. Settlement corridors scale with the square of participants, not the first power. The institutions that understand this math are not waiting for the market to mature before they decide.

They are deciding now because deciding now is how you end up on the right side of the compounding.

69

11

173

7,573

CresyX | 我 retweeted

Jun 5

Two conversations are happening simultaneously in institutional finance right now, and most market observers are only tracking one of them.

The first is about whether blockchain settlement infrastructure is genuinely ready for regulated institutional use at scale. It is the conversation that generates most of the conference panels, research notes, and industry commentary. It has been happening, in slightly different forms, for about seven years.

The second conversation is about which specific rails institutional settlement standardizes on. It is being conducted almost entirely in legal agreements, compliance reviews, and production deployments. It generates far less commentary and far more consequence.

The second conversation is roughly two years ahead of the first.

JPMorgan's Kinexys has processed more than $1.5 trillion on blockchain rails. DTCC is advancing SEC-cleared tokenization of U.S. Treasuries. NYSE is building tokenized securities infrastructure alongside BNY Mellon and Citi. Stablecoin supply exceeds $300 billion globally. 93% of tokenized U.S. assets settle on Ethereum today. These are not proof-of-concept numbers. They are operational volumes from institutions that moved past the "if" question and are now inside the "which" one.

The April 2026 GFMA report is the clearest signal of where the real conversation sits. It did not evaluate whether institutional onchain finance should exist. It catalogued the specific technical items that remain open now that it demonstrably does: interbank interoperability for tokenized deposits, transaction privacy standards equivalent to what regulated institutions actually require, settlement mechanics that match real-time gross settlement systems, governance frameworks for digital money. That document is not a feasibility study. It is a specification for the remaining open work on an implementation already underway.

The institutions engaged in that implementation are not early adopters waiting to see whether the market validates their bet. They are standard-writers, and that distinction carries structural weight.

In financial infrastructure, the first wave of production deployments does not simply establish commercial position. It establishes the architectural precedent that every subsequent deployment references. The governance structures chosen by the first live institutions become the template compliance teams at the next 50 institutions evaluate against. The privacy implementations that clear regulatory review first become the baseline specification. The interoperability approaches that prove out in production become the default. The standard does not emerge from a working group's recommendations. It emerges from whoever arrives at that working group with live transaction data and a production record.

Ten institutions in production create 45 settlement corridors. One hundred create nearly 5,000. Each deployment adds both transaction evidence and architectural weight to the emerging standard. The precedent compounds.

@zksync is already in the "which" conversation with regulated institutions in production: Deutsche Bank's tokenized fund platform live on ZK infrastructure, ADI Chain running with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton. Cari Network onboarding five U.S. regional banks representing $600B in combined deposits. More than 30 institutions across banks, central banks, sovereign issuers, and global custodians in active pipeline engagement.

These are not pilots or proofs of concept. They are production deployments writing the answer to the "which" question one transaction at a time.

The first conversation still has years to run. The second one is well underway.

Which conversation is your institution actually in?

106

9

206

7,670

Jun 6

There is a compliance variable in institutional settlement infrastructure evaluation that most technical comparisons treat as secondary. It is not throughput, privacy architecture, or finality model. It is vendor structure.

When a regulated institution deploys settlement infrastructure assembled from separately built components, each interface between components carries a question that the institution's compliance and risk teams have to resolve explicitly: who owns the boundary, and what happens when it needs to change?

Under OCC third-party risk management guidance, and equivalent ECB and FSA supervisory frameworks, institutions are required to document their control over, and dependency on, third-party technology providers in their regulated operating environment. When a settlement stack comprises a proving system from one team, a privacy execution layer from another, and an institutional product surface from a third, the institution faces three separate vendor relationships, three separate security incident chains, three separate update and patch cycles, and three separate liability scopes. These do not merge cleanly under a single compliance review. Each seam is an audit point.

The practical consequence: when a zero-day vulnerability surfaces in a component with a vendor boundary, the institution's operational team is coordinating a response across organizations that have different priorities, different deployment timelines, and different contractual obligations. The compliance team is documenting a remediation process it does not fully control. The legal team is reviewing indemnification terms across vendor contracts. This is not a theoretical scenario. It is the operational reality of assembled infrastructure under regulated activity.

@zksync operates the full institutional stack end-to-end. Airbender is not a third-party prover accessed through an integration. It is the ZKsync proving system, built by the same organization that operates ZK Stack and Prividium. Security patches propagate through one engineering organization. Architectural decisions are made with knowledge of the full stack's requirements. A compliance team reviewing a Prividium deployment is reviewing one organization's control over the proving layer, the execution environment, and the institutional surface simultaneously.

The performance reflects the integration. Airbender sits #1 on eth_proofs with ~1-second block proving on consumer hardware because the prover was designed for the settlement architecture it powers, not adapted to interface with it after the fact. The performance ceiling is the team's own engineering roadmap.

Deutsche Bank's DAMA 2.0, ADI Chain, Cari Network, currently onboarding five U.S. regional banks representing $600B in combined deposits with production rollout planned for later in 2026, and BitGo's custody integration all cleared compliance reviews where vendor structure is a documented evaluation variable. Tier-one banks do not overlook this question. They found an acceptable answer in the integrated stack.

An assembled alternative that delivers equivalent component performance does not deliver equivalent compliance risk profile. The seams are the risk. Eliminating them requires building the stack, not selecting it.

58

52

163

7,931

Jun 6

The analytical content of "first-mover advantage" varies enormously by market. In most technology categories, it describes a lead that is real but closeable: brand recognition fades with sufficient marketing spend, customer acquisition cost advantages erode with competitive distribution, product gaps close with faster iteration cycles. The lead matters but it does not compound indefinitely.

Settlement infrastructure is categorically different. The switching cost structure is architectural and counterparty-dependent, which means displacement does not become more affordable over time. It becomes less affordable.

Three cost types compound simultaneously when an institution commits to settlement rails. Operational integration is the first: years of engineering work, workflow redesign, and technical debt that is stack-specific and non-transferable. Regulatory attestation is the second: the compliance sign-off is for the specific architecture, and re-attestation for a different stack requires a full re-examination by the same regulators who approved the original, conducted at the new stack's current level of maturity. Counterparty relationships are the third: every institution that settles on the same rails is a switching cost. Migrating means renegotiating every bilateral settlement relationship with every counterparty that stays.

These costs do not add linearly. They multiply, and they grow with every month of operational history, every new regulatory attestation, and every new counterparty relationship the stack accumulates. SWIFT demonstrated the terminal state of this dynamic: 239 banks agreed on a messaging standard in 1973, and 11,000 institutions built on it over the following decades because the compounding switching cost made displacement uneconomic for any individual participant regardless of the quality of alternatives. The product question and the network question separated early. After that separation, the network question dominated every evaluation indefinitely.

The 2026 institutional onchain settlement moment is exhibiting the same structural signature. The GFMA's April 2026 report identified the four remaining technical blockers: interbank interoperability for tokenized deposits, transaction privacy standards, RTGS-equivalent settlement mechanics, governance for digital money. The platforms that resolve these in production over the next 18 months do not simply win a market. They initiate the compounding dynamic that makes displacement structurally uneconomic for the institutions that follow.

Privacy is the specific constraint that narrows the eligible field before product evaluation begins. No regulated institution settles real balance-sheet exposure on shared infrastructure where other participants can observe its positions, counterparty relationships, or strategy. Architecture that treats private execution as the default, not as a configurable layer on top of a transparent foundation, is the only architecture eligible for this use case.

@zksync delivers all four required properties simultaneously in production: private execution environments publishing only zero-knowledge proofs and state commitments to Ethereum, institution-controlled permissioned chains with selective regulatory disclosure, cryptographic finality without challenge windows, atomic cross-chain composability without external bridge dependencies. Deutsche Bank's DAMA 2.0 tokenized fund platform in production. ADI Chain live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton. Cari Network onboarding five U.S. regional banks with $600B in combined deposits. More than 30 institutions in active engagement across banks, central banks, sovereign issuers, and global custodians.

Ten institutions create 45 settlement corridors. One hundred create 4,950. JPMorgan Kinexys at $1.5 trillion processed. 93% of tokenized U.S. assets settling on Ethereum. The compounding is already active.

First-mover advantage in settlement infrastructure is not a temporary product lead. It is the initiation of a switching cost structure that compounds asymmetrically and becomes more durable with every committed participant. 2026 is the year that structure begins to lock, and the architecture accumulating committed institutional participants right now is positioned to anchor it.

64

3

117

7,375

CresyX | 我 retweeted

Jun 6

Every system that calls itself convenient is charging you something you agreed to without reading the price.

I spent three years posting for brand campaigns through an agency. Convenient for me: one email, one brief, one payment. I never asked what the agency charged the brand for my post, or what percentage of that number I was actually receiving.

When I finally found out, I understood something that changed how I see every platform I use:

Convenience is almost always most convenient for the party collecting the hidden fee.

The creator economy runs on hidden fees dressed as features:

→ Reach is a feature. Someone else controls it.

→ Discovery is a feature. Someone else controls it.

→ Distribution is a feature. Someone else controls it.

You get the convenience. They get the margin.

@RallyOnChain is interesting to me for one specific reason: the cost structure is visible before you decide to participate. Not buried in a page you will never read.

What convenient system are you inside that you have never actually priced out? 👇

72

9

94

3,900

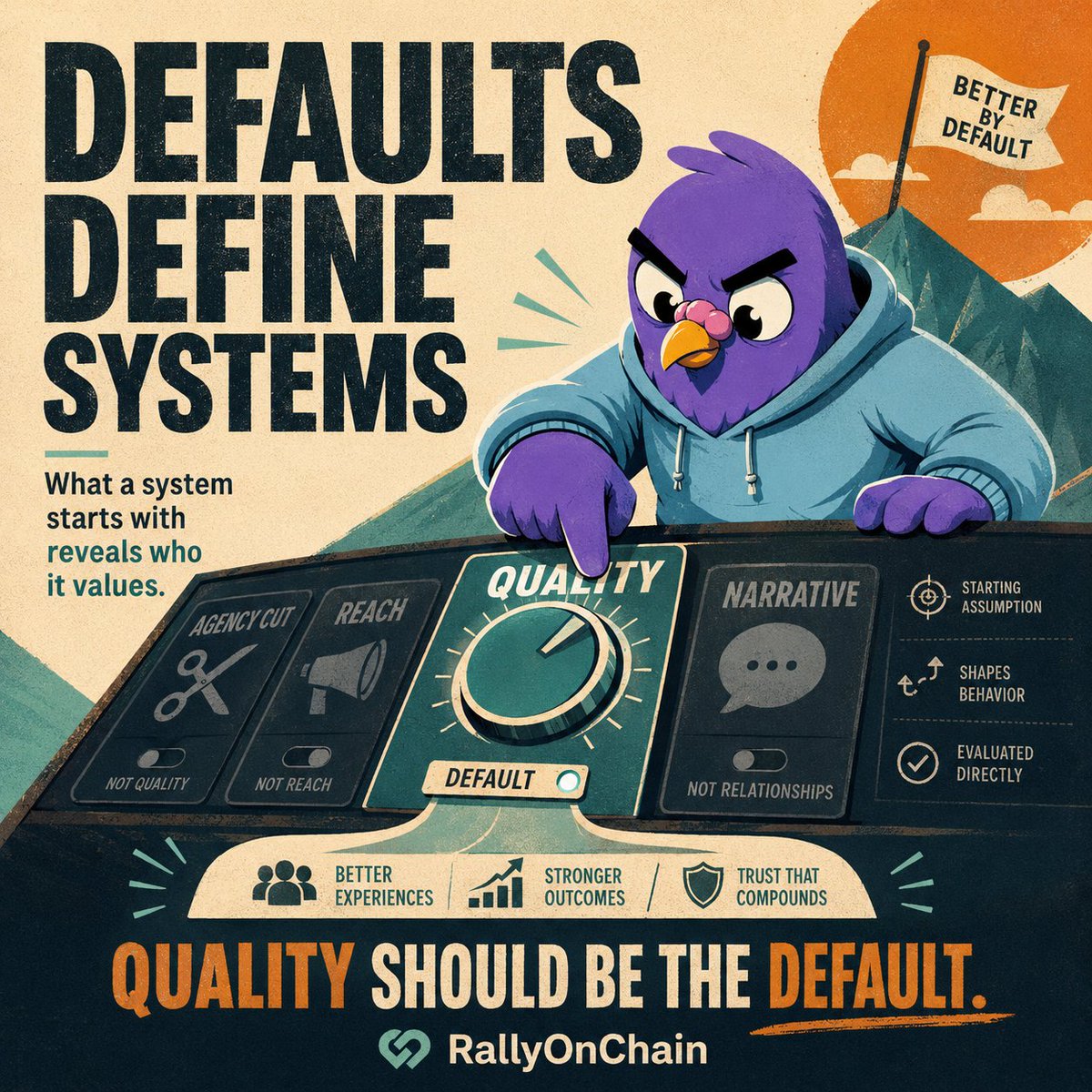

The most powerful design decision any system makes is what it sets as the default.

Not the options you can choose. The one you start with if you never ask.

→ The default in traditional marketing: the agency takes the cut.

→ The default in influencer platforms: reach determines reward.

→ The default in most crypto protocols: the loudest narrative wins.

Defaults are not neutral. They are the system's opinion about who matters.

@RallyOnChain changed the default: quality is the starting assumption. Not reach, not relationships, not who you know. Just the work, evaluated directly.

What default are you still running on that you never consciously chose?

73

4

83

3,933

CresyX | 我 retweeted

Jun 5

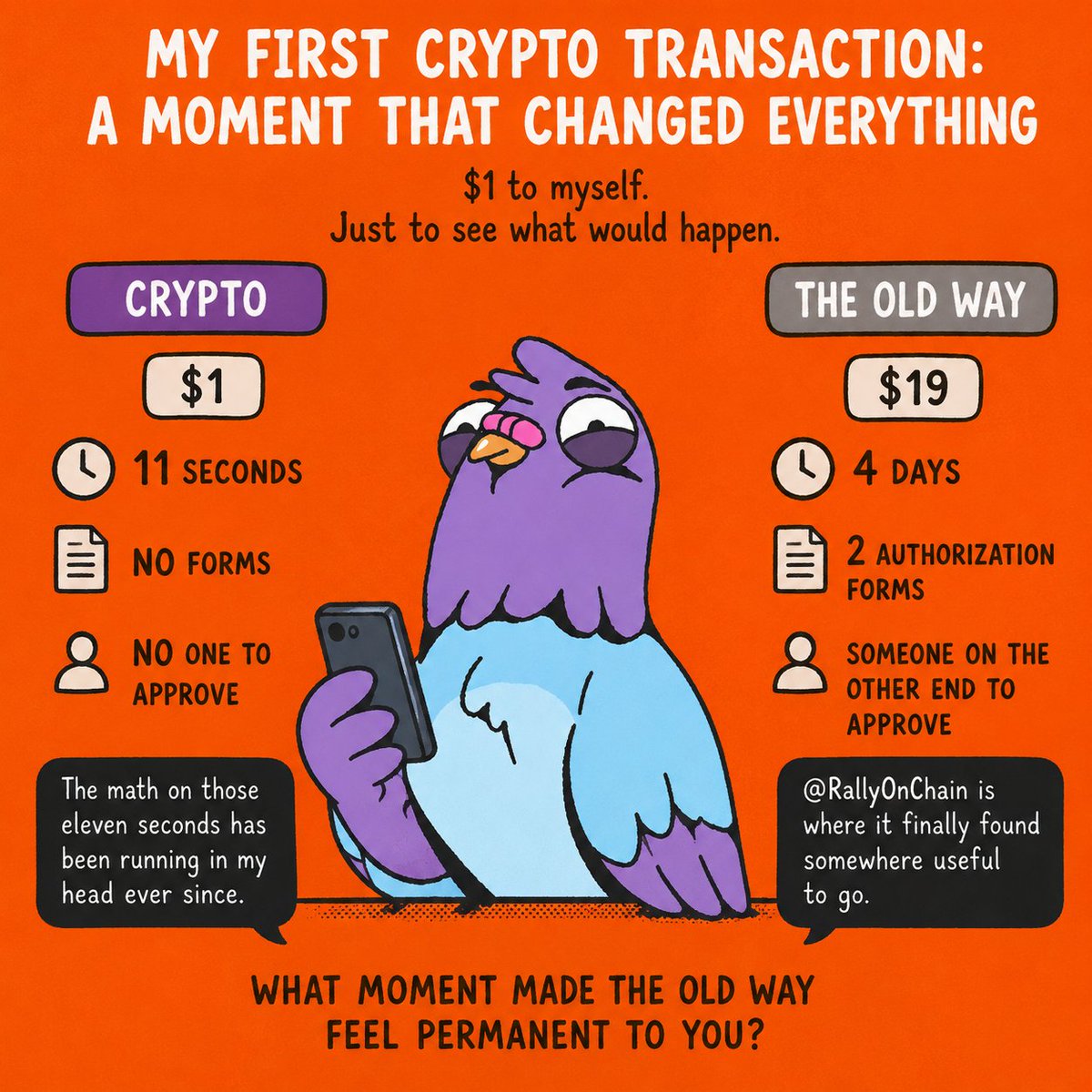

The first transaction I ever sent in crypto was one dollar, to myself, just to watch what happened.

Eleven seconds. No forms. No one on the other end who needed to approve it.

That same morning I had sent a wire transfer to the same destination. Four days. Nineteen dollars. Two authorization forms.

The math on those eleven seconds has been running in my head ever since.

@RallyOnChain is where it finally found somewhere useful to go.

What moment made the old way feel permanent to you?

54

10

81

3,900

CresyX | 我 retweeted

Jun 5

If it's my last tweet, than it would be this 👇

The more a system needs to explain itself, the more it has to hide.

I noticed this in finance first. Fees buried in paragraphs. Terms designed to be unread. Complexity was not a feature. It was a firewall.

The same pattern runs through crypto.

→ The protocols that survive inspection are simple enough to inspect.

→ The ones that resist it just keep adding layers.

What keeps me coming back to @RallyOnChain: visible weights, public scoring, on-chain distribution. You do not have to trust it. You can just read it.

What would you trust more if you could simply read exactly how it worked?

33

4

51

3,413