Started my new journey

Joined March 2023

- Tweets 1,168

- Following 1,621

- Followers 1,022

- Likes 1,051

46 Photos and videos

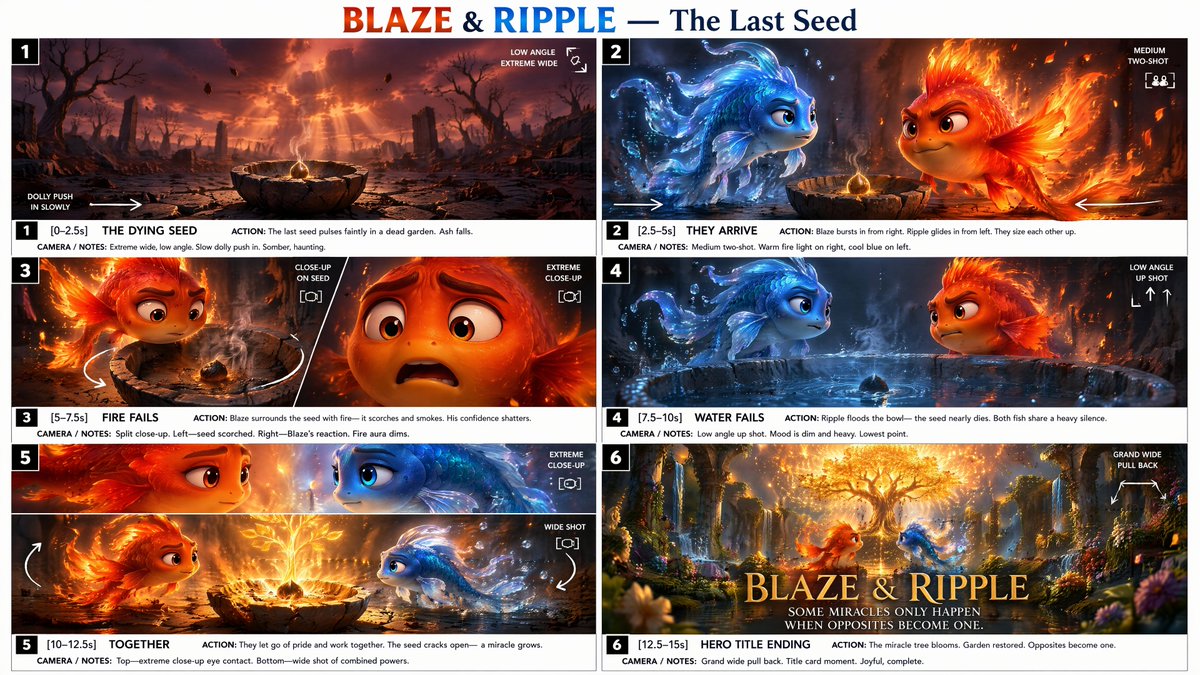

Two magical koi fish. One controls fire 🔥 One controls water 💧

They both tried to save the last magical seed alone.

Both failed.

Then came the moment neither expected

"Maybe I need you."

"And I need you."

What happened next changed everything 🌱✨

Made with @renoiseai. 15 seconds, one story, zero limits.

#renoiseai #RenoiseCanvas

66

52

366

44,555

DataRogue retweeted

Jun 15

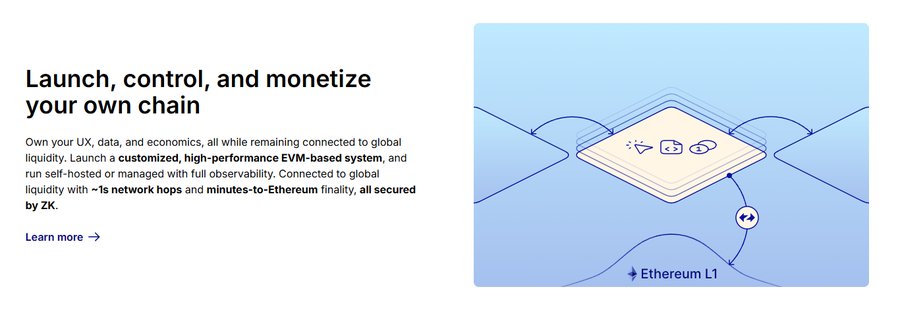

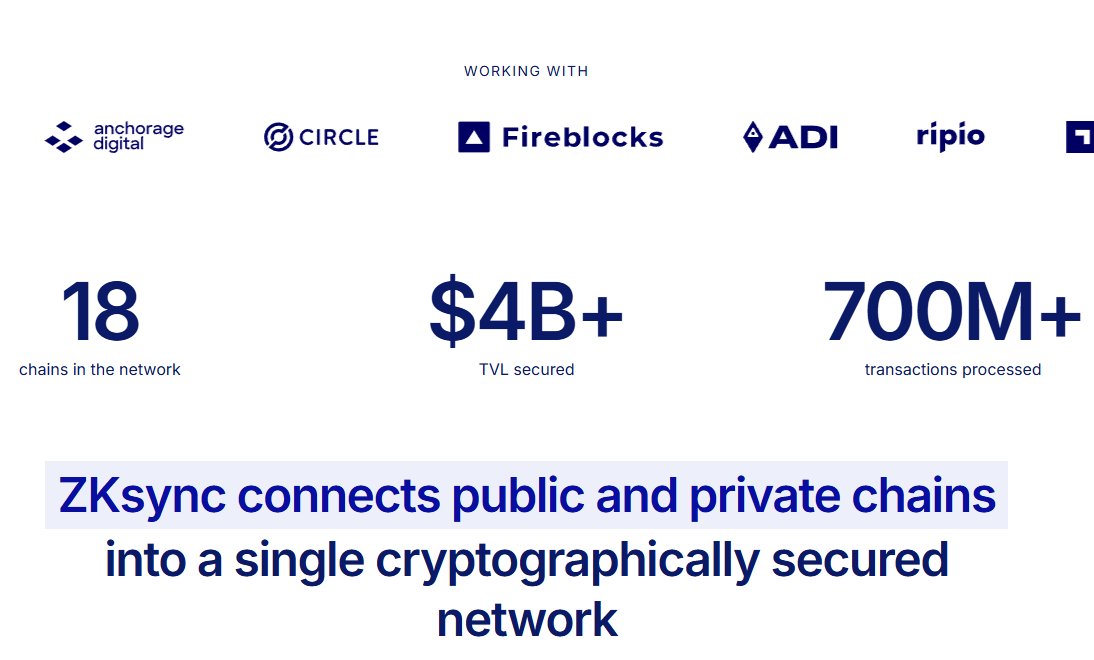

There is a specific question every risk manager at a regulated institution asks before approving infrastructure. Not: is this the most advanced? But: has this actually worked, in production, under real capital?

That question eliminates most blockchain platforms immediately. It is also the question ZKsync answers most directly.

The first working ZK rollup on Ethereum was built in 2019. Production launched in 2020. The first ZK EVM went live in March 2023. More than 500 million transactions have processed across the network's history. Airbender, the proving system underneath the current stack, sits at number one on eth_proofs with approximately one-second block proving on consumer-grade GPUs, sub-second proof generation in production conditions, and post-quantum security properties built into the architecture from the start, not added later.

This infrastructure was not built for the 2026 institutional moment. It was built before institutional settlement was a serious conversation in any conference room. Six years of production history, 500 million transactions, and independent technical benchmarks are not marketing claims. They are verifiable facts that risk managers, legal teams, and technical reviewers can evaluate.

When regulated institutions approve settlement infrastructure, they are not making a technology selection. They are accepting operational, regulatory, and counterparty dependencies that take years to unwind if something goes wrong. The due diligence process reflects that weight. Architecture gets reviewed. Operating history gets reviewed. Third-party benchmarks get reviewed. Regulatory alignment gets reviewed.

The platform that has been running ZK proofs in production the longest enters that process differently than one that built specifically for this institutional moment. The track record is not just a credential. It is risk mitigation.

Cari Network, onboarding five U.S. regional banks representing over $600 billion in combined deposits, was founded by the 27th U.S. Comptroller of the Currency. The person who spent a career setting regulatory standards for U.S. banking chose this infrastructure. Deutsche Bank selected it for DAMA 2.0, its production tokenized fund platform. First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton are live on ADI Chain.

These are the outputs of institutional due diligence processes run by some of the most risk-averse decision-makers in global finance.

@ZKsync is not entering the institutional settlement window as a new entrant. It is the platform that was already there, running the infrastructure that institutions are now choosing because the track record is what they needed all along.

25

2

83

134

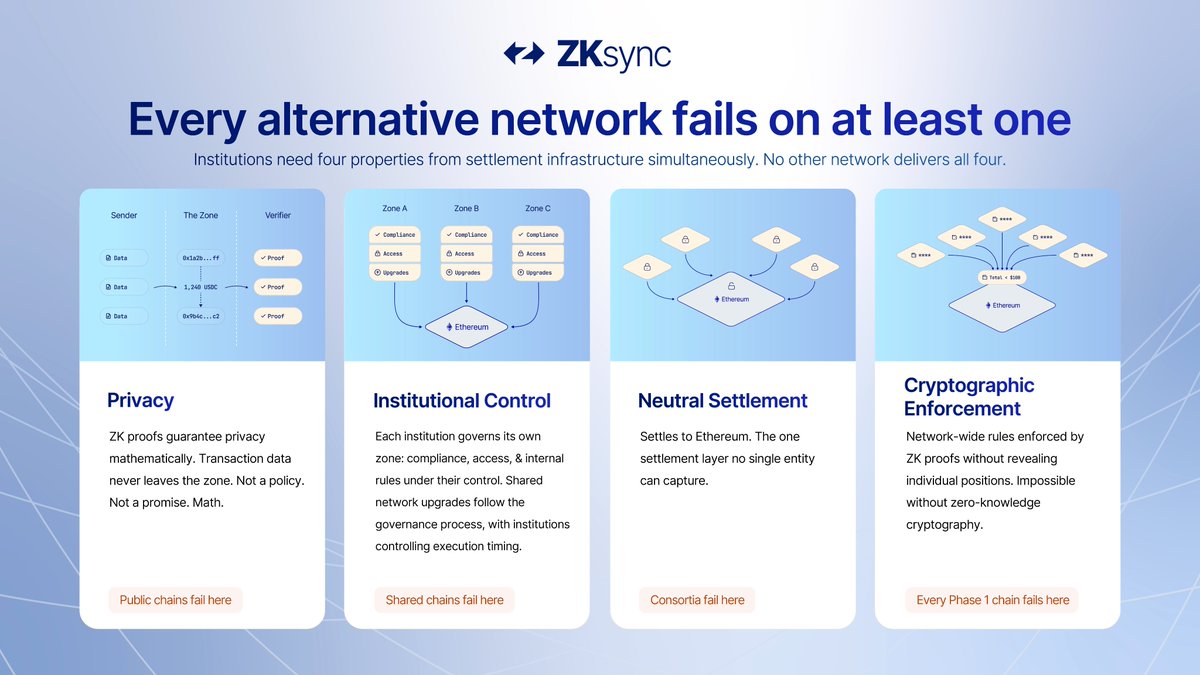

Banks don't just choose infrastructure. They inherit the counterparty graph of whoever chose first. And they inherit it under one condition that most public blockchain architectures cannot meet: the positions, counterparty data, and settlement strategy of every participant must remain invisible to every other participant.

That single constraint eliminates most options before the technical comparison begins.

JPMorgan's Kinexys has processed over $1.5 trillion on blockchain rails, averaging roughly $2 billion daily. DTCC is advancing SEC-cleared tokenization of U.S. Treasuries. NYSE is building tokenized securities rails alongside BNY and Citi. The tokenized RWA market is approaching $29 billion, with $300 billion in global stablecoin supply, 93% of U.S. tokenized assets settling on Ethereum. These are live operations with counterparties who have signed off - operationally, legally, and architecturally.

When a bank integrates into a settlement rail, exit costs operate across three distinct layers. Operational: years of integration rebuilt from the start. Regulatory: full re-attestation and re-audit of the compliance stack. Counterparty: the most underestimated layer. A bank evaluating rails in 2027 is not choosing a technology stack. It is deciding whether its existing counterparties will be able to settle with it at all.

Ten institutions create 45 settlement corridors. A hundred create nearly 5,000. SWIFT scaled from 239 banks to over 11,000 on this dynamic. Visa built global infrastructure from a regional network the same way. Each new participant made the alternative less economically viable for the next institution to consider - not through marketing, but through accumulated counterparty dependencies.

The April 2026 GFMA report catalogued what remains technically open: interbank interoperability for tokenized deposits, transaction privacy standards, settlement mechanics equivalent to RTGS, governance for digital money. The platforms that resolve this agenda in the next 18 months become the standard for the decade.

@ZKsync delivers the four architectural properties institutional settlement requires simultaneously: privacy by design through private execution environments where only ZK proofs and state commitments reach Ethereum, institution-controlled execution with role-based permissioning and selective disclosure, cryptographic finality without optimistic challenge windows, and atomic cross-chain composability without external bridges. Live institutional deployments today: Deutsche Bank's DAMA 2.0 tokenized fund platform in production, ADI Chain live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton, Cari Network onboarding Huntington Bancshares, First Horizon, M&T Bank, KeyCorp, and Old National Bancorp - five U.S. regional banks with over $600 billion in combined deposits - and more than 30 institutions in active pipeline across banks, central banks, and sovereign issuers.

The counterparty graph is already forming. Every institution that commits raises the switching cost for the next one, and lowers the viable window for a competing rail. That is the asymmetric compounding that turns a first-mover position into a decade-long standard.

The window is open. It does not stay open long.

63

73

107

7,895

DataRogue retweeted

Jun 15

The reason institutional blockchain adoption stalled for a decade wasn't technical capability. It was exposure.

Banks understood the technology. What they couldn't accept was settlement infrastructure that publishes counterparty positions, transaction flows, and strategy to every other participant on the network. That single constraint eliminated most blockchain architectures before institutions even got to the finality question, the integration question, or the network effects question.

Transparency wasn't a tradeoff. It was a disqualifier.

This is why the institutional moment in onchain settlement is not simply about blockchain maturing. It is about one specific architectural problem getting solved. Zero-knowledge proofs change the constraint at the protocol level. Not through permissioned databases that recreate the centralization problem. Not through consortium chains that sacrifice interoperability with the broader Ethereum ecosystem. Through cryptographic proofs that let institutions settle on shared public infrastructure while keeping counterparty data private by default.

Only validity proofs and state commitments reach Ethereum. Positions, transaction details, and strategy never leave the institution's execution environment. The bank sees what it needs to see. Regulators access what they are entitled to see. Counterparties see nothing they shouldn't.

This is not a feature. It is the prerequisite that makes institutional onchain settlement viable at all.

The institutions that recognized this are already in production. Deutsche Bank's DAMA 2.0 tokenized fund platform is live through Memento on ZKsync infrastructure, the first tier-one global bank running on ZK settlement rails. ADI Chain is live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton. Five U.S. regional banks representing over $600 billion in combined deposits are onboarding through Cari Network, a network founded by the 27th U.S. Comptroller of the Currency. More than 30 institutions across U.S. and international banks, central banks, sovereign issuers, and global custodians are in active engagement.

Each one arriving at the same conclusion: the rails that solve the exposure problem are the rails institutional settlement can actually use.

Each new deployment also changes what the next institution decides. A bank evaluating its options in late 2026 is not choosing between technical specifications. It is choosing whether to join the network where its counterparties are already settling, or to build in isolation on rails that lack the relationships it needs to function.

93% of U.S. tokenized assets settle on Ethereum. The settlement layer is not in question. What 2026 decides is which execution layer regulated capital uses.

@ZKsync is the one built to resolve the constraint that blocked this category for a decade. Follow the institutional deployments. The window is narrowing.

32

89

85

8,094

DataRogue retweeted

Jun 15

A production deployment in banking is not the start of trust. It's what trust looks like after years of evaluation are done.

This reframes everything about the current @zksync institutional picture.

When Deutsche Bank puts DAMA 2.0 on a ZK settlement layer through Memento, that announcement follows years of closed-door process. Legal review, risk mapping, compliance assessment across jurisdictions, internal sign-off at multiple committee levels. The logo appears at the end of that process, not before it. A tier-one global bank's compliance machinery said yes to a specific stack. Not to blockchain generally. To this one.

That distinction is not replicable quickly.

ADI Chain is live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton sharing the same rails. The key institution here is the Central Bank of the UAE. Central banks do not trial experimental infrastructure. When a central bank deploys in production, it has used its own sovereign regulatory judgment to conclude the architecture meets its requirements. That judgment doesn't transfer to a competing rail at the same time.

Cari Network brings a distinctly American proof point. Founded by Eugene Ludwig - the 27th U.S. Comptroller of the Currency - it is currently onboarding five U.S. regional banks representing $600B in combined deposits, with production rollout planned for later in 2026. Ludwig didn't choose this infrastructure because he is enthusiastic about ZK technology. He chose it because it passed the regulatory standard he spent his career helping define.

BitGo's custody integration with Prividium closes the operational loop. Regulated capital doesn't just need technically capable rails. It needs custody frameworks, compliance interfaces, and audit infrastructure that fits existing institutional operations. That entry point is now functional, not theoretical.

The four architectural properties are real. Privacy by design, cryptographic finality, institution-controlled execution, atomic composability - difficult to replicate simultaneously, and built on a proving system currently ranked first on eth_proofs.

But properties alone don't create a standard. What creates a standard is when the institutions that define regulatory credibility in global finance have already made their choice. Because every institution evaluating rails in the next 12 months isn't choosing on pure technical merit. It's choosing based on what its counterparties, regulators, and settlement peers already decided.

Institutional infrastructure doesn't change once it's embedded. It extends.

64

17

129

7,962

DataRogue retweeted

Jun 15

The GFMA catalogued the open problems for institutional onchain finance in April 2026: interbank interoperability for tokenized deposits, transaction privacy standards, settlement mechanics equivalent to RTGS systems, governance for digital money. Four problems that have blocked regulated capital from committing to blockchain rails at scale.

All four have a common dependency. Privacy.

No regulated bank settles on infrastructure that exposes positions, counterparty data, or execution strategy to other network participants. This is not a product preference. It is a compliance requirement embedded in banking secrecy law, GDPR, MiFID II best-execution rules, and the basic competitive reality that no trading desk discloses its book to the market it operates in. Architectures that bolt privacy on top of public state do not solve this. The base layer exists. The history is discoverable. The structural problem remains.

This is the constraint @ZKsync solved at the architectural layer, not the product layer. Execution happens inside private environments. Only zero-knowledge proofs and state commitments are published to Ethereum. The cryptographic properties are in the design, not the configuration.

The deployment list is the proof that this works at the tier-one institutional level.

Deutsche Bank put its DAMA 2.0 tokenized fund platform, Memento, into production on ZK infrastructure. ADI Chain is live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton sharing a single ZKsync settlement layer. That combination is not a proof of concept. It is a central bank, the dominant global asset manager, and a payments network that processes trillions annually, coexisting on the same chain in production. Cari Network is currently onboarding five U.S. regional banks representing $600B in combined deposits, with production rollout planned for later in 2026. The network's founder is Eugene Ludwig, the 27th U.S. Comptroller of the Currency. Not a technologist building toward banks. The former head of the office that supervises them. BitGo has integrated institutional custody and wallet services with Prividium, closing the last gap between the settlement layer and institutions that require custody-grade infrastructure before committing capital.

Airbender, the underlying proving system, sits at #1 on eth_proofs. Approximately one-second block proving on consumer-grade GPUs. Cryptographic finality without optimistic challenge windows. Settlement without a multi-day wait for fraud-proof expiry.

Now the compounding argument.

SWIFT scaled from 239 banks to 11,000 on a single dynamic: each new bank increased the value of being connected, which raised the cost of building a competing network from scratch. Visa scaled from a regional card program into global payment infrastructure on the same mechanism. The network did not win by being technically superior at scale. It won by forming the network before alternatives could.

Ten institutions on shared rails create 45 possible settlement corridors. One hundred create nearly 5,000. A bank evaluating settlement infrastructure in 2027 is not choosing in isolation. It is choosing the rails its counterparties have already chosen. Every regulated institution that deploys on ZKsync raises the operational, regulatory, and counterparty cost for the next institution to go elsewhere.

The $29B tokenized RWA market is growing. $157B in regulated stablecoin supply settles on Ethereum. Ninety-three percent of U.S. tokenized assets clear on Ethereum. The institutional volume is building. The question is which settlement layer captures the network formation when it concentrates.

The architectural lead is real. The deployment lead is real. The 2026 window is real. And the mechanism that converts a current lead into a settlement standard for the decade is already in motion.

99

17

153

8,158

$5,000 in a live prize pool. Top 10 winners each earning nearly $500. Creators on @RallyOnChain getting paid every single day and most people entering right now are leaving money on the table because they do not understand how the scoring actually works.

That is a gap worth closing before someone else does.

Every submission gets evaluated across multiple dimensions. Content alignment checks whether you answered the actual campaign brief, not just described the project in general. Information accuracy checks whether your specific claims hold up. Vague enthusiasm reads like vague enthusiasm to an AI that is built to spot it.

The originality gate is where most entries lose quietly. The AI compares your post against every other submission in the same campaign. Mirror the structure or framing of other posts and the score reflects it, even if the content itself is accurate.

Engagement potential is weighted separately. Not your follower count. Whether the writing would actually make someone stop.

One post written with real product understanding and a distinct angle consistently outperforms three posts written fast. The weights are publicly documented. The rewards are distributed on-chain. Nothing is hidden.

$5,000 in not a small amount & nearly $500 to top 10 winner. There's still enough time to join before this window is closed.

Go to app.rally.fun or use my link rally.fun/r/boltuog . Read the brief properly. Then write like the $500 depends on it

That's it. Best of luck guys

41

12

59

3,858

DataRogue retweeted

Jun 12

Do you know @RallyOnChain publishes the scoring criteria publicly?

Most people post without reading it, understanding it. That's the entire opportunity.

Content accuracy, originality, engagement potential, all transparent, all adjustable per campaign. You can read the rubric, understand what the AI is looking for, and write to it. No guessing, No black box.

Creators on the platform are earning every day in actual stablecoins. No follower minimum. No KOL shortlist. The reward goes to whoever writes something that holds up.

There's a $5,000 prize pool running right now. Top 10 take home close to $500 each. And at this stage, most people posting don't know the scoring framework exists which means the ones who do have a real edge, not a luck edge.

Start at rally.fun/r/shrabonweb3 & drop a reply if you want to know how to write something that actually scores well.

35

2

112

3,937

DataRogue retweeted

Jun 10

The biggest lie in crypto is that adoption is a technology problem.

It isn't. We have fast chains. We have cheap transactions. We have wallets that improve every year. The rails exist and have for a while now.

The problem is that nobody who understands the technology can explain it in a way that makes someone care. And nobody who can explain it in a way that makes someone care gets rewarded for doing it.

We built an industry that pays engineers ten times what it pays communicators, then wondered why nobody outside of crypto understands what any of us are building.

Adoption is a communication problem. It always has been.

The infrastructure being built around rewarding quality content creation in Web3 is more important than most people in the space realize. @RallyOnChain is part of that infrastructure. AI-evaluated, on-chain verified, no gatekeepers deciding who gets access.

The projects that figure out how to tell their story to people who aren't already convinced will win this decade. Not the ones with the cleanest code.

25

3

30

2,600

DataRogue retweeted

Jun 6

Drop a prompt you want to see come to life in replies

We'll generate the best one in Renoise and tag you. 👇

8

8

27

1,084

Deutsche Bank has operated for over 150 years. It sits on the Financial Stability Board's list of globally systemically important banks. When it deploys production infrastructure for its institutional tokenization platform, the technology decision underlying that deployment has been reviewed by internal risk management committees, external legal counsel in every relevant jurisdiction, and the ECB supervisory function. It has been stress-tested against the requirements of every market in which DAMA 2.0 will process settlement activity.

Memento is that deployment. Production. Not a research project. Not a proof-of-concept architecture exploring whether institutional tokenization is feasible. A deployed product running on $ZK settlement rails.

That means the compliance review concluded positively. The risk management committee signed off. The legal team resolved the jurisdictional implications. The ECB supervisory relationship was navigated. Every internal gate that a decision of this magnitude requires at Deutsche Bank's scale was cleared.

The architecture that cleared those gates was the ZKsync stack. Privacy by architecture through Prividium's private execution environments, where Deutsche Bank holds operational control of its own chain. Cryptographic finality without challenge windows, which is the baseline any RTGS-equivalent system requires under the settlement risk frameworks the bank's operations team applies. Institutional-controlled execution that meets the control documentation requirements under BaFin and ECB supervisory frameworks. And atomic cross-chain composability that avoids the external bridge validator trust assumptions that compliance teams flag.

Airbender, the proving layer, sits #1 on eth_proofs with ~1-second block proving on consumer hardware and production economics near $0.0001 per ERC-20 transfer. That throughput is what makes the architecture usable at the transaction volumes DAMA 2.0 generates.

The decision carries an additional signal layer. Deutsche Bank's due diligence is not just thorough. It is specifically rigorous on the dimensions that other institutions' compliance teams will also review. When Deutsche Bank's review clears the architecture, it is implicitly pre-clearing it against the questions a second tier-one bank will ask when they read the deployment news.

ADI Chain is live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton. Cari Network is currently onboarding five U.S. regional banks representing $600B in combined deposits, with production rollout planned for later in 2026. BitGo has integrated institutional custody through Prividium.

Each is a separate organization with independent compliance judgment. Each reached the same architectural conclusion. The convergence is not coincidental and it is not coordinated. It is the output of compliance reviews that asked the same hard questions and found the same answers.

Memento is the most visible entry point into that convergence. Deutsche Bank asked the questions first. The deployment is the finding.

60

49

159

8,242

The moments when financial infrastructure standards get set are rarely obvious while they are happening. They are characterized not by announcements but by a quiet convergence of institutional decisions that, taken together, determine the operational fabric of financial markets for the following decade or more.

We are inside one of those moments.

ISO 20022 displaced legacy payment messaging formats over roughly two decades, not because it was superior in every dimension from the start but because critical mass around the new standard made the migration cost for holdouts increasingly asymmetric. FedWire's architecture has persisted for decades despite being technically superable because the operational and counterparty fabric built around it makes replacement economically irrational for any individual participant. SWIFT replaced telex in the 1970s by solving a specific coordination problem for 239 institutions and then became irreplaceable for the 11,000 that followed because each new entrant joined a network whose counterparty gravity made building outside it prohibitively expensive.

The 2026 institutional onchain settlement moment has the same structural signature, and the data confirms it is already active. JPMorgan Kinexys has processed $1.5 trillion on blockchain rails. DTCC is advancing SEC-cleared tokenization of U.S. Treasuries. NYSE is building tokenized securities infrastructure with BNY and Citi on the cash leg. 93% of tokenized U.S. assets settle on Ethereum today. The tokenized RWA market is approaching $29 billion.

The GFMA's April 2026 report identified what remains technically unresolved: interbank interoperability for tokenized deposits, transaction privacy standards, RTGS-equivalent settlement mechanics, governance for digital money. The platforms that resolve these in production over the next 18 months set the architectural requirements specification for every institution that evaluates afterward.

The constraint that eliminates most of the field before product evaluation starts is privacy. A regulated institution managing real balance-sheet exposure cannot settle on shared infrastructure that makes its positions, strategy, or counterparty relationships observable to other network participants. The architecture has to treat private execution as the default, not as an optional configuration. This is not a product preference. It is a structural compliance requirement that separates the architectures eligible for institutional deployment from those that are not.

@zksync's integrated stack treats privacy as foundational: institution-controlled private execution environments where only zero-knowledge proofs and state commitments publish to Ethereum, cryptographic finality without challenge windows, atomic composability without external bridge dependencies. Deutsche Bank's DAMA 2.0 is in production on this infrastructure. ADI Chain is live with First Abu Dhabi Bank and the Central Bank of the UAE. Cari Network is onboarding five U.S. regional banks with $600B in combined deposits. More than 30 institutions across banks, central banks, sovereign issuers, and global custodians are in active engagement.

The window closes institution by institution, not on a calendar date. By the time it is visibly closing to outside observers, the architectural decision has already been made for the institutions that anchor the network. That is how these moments have always resolved. 2026 is not an exception.

65

29

114

8,201

The most powerful design decision any system makes is what it sets as the default.

Not the options you can choose. The one you start with if you never ask.

→ The default in traditional marketing: the agency takes the cut.

→ The default in influencer platforms: reach determines reward.

→ The default in most crypto protocols: the loudest narrative wins.

Defaults are not neutral. They are the system's opinion about who matters.

@RallyOnChain changed the default: quality is the starting assumption. Not reach, not relationships, not who you know. Just the work, evaluated directly.

What default are you still running on that you never consciously chose?

73

4

83

3,932

DataRogue retweeted

Jun 5

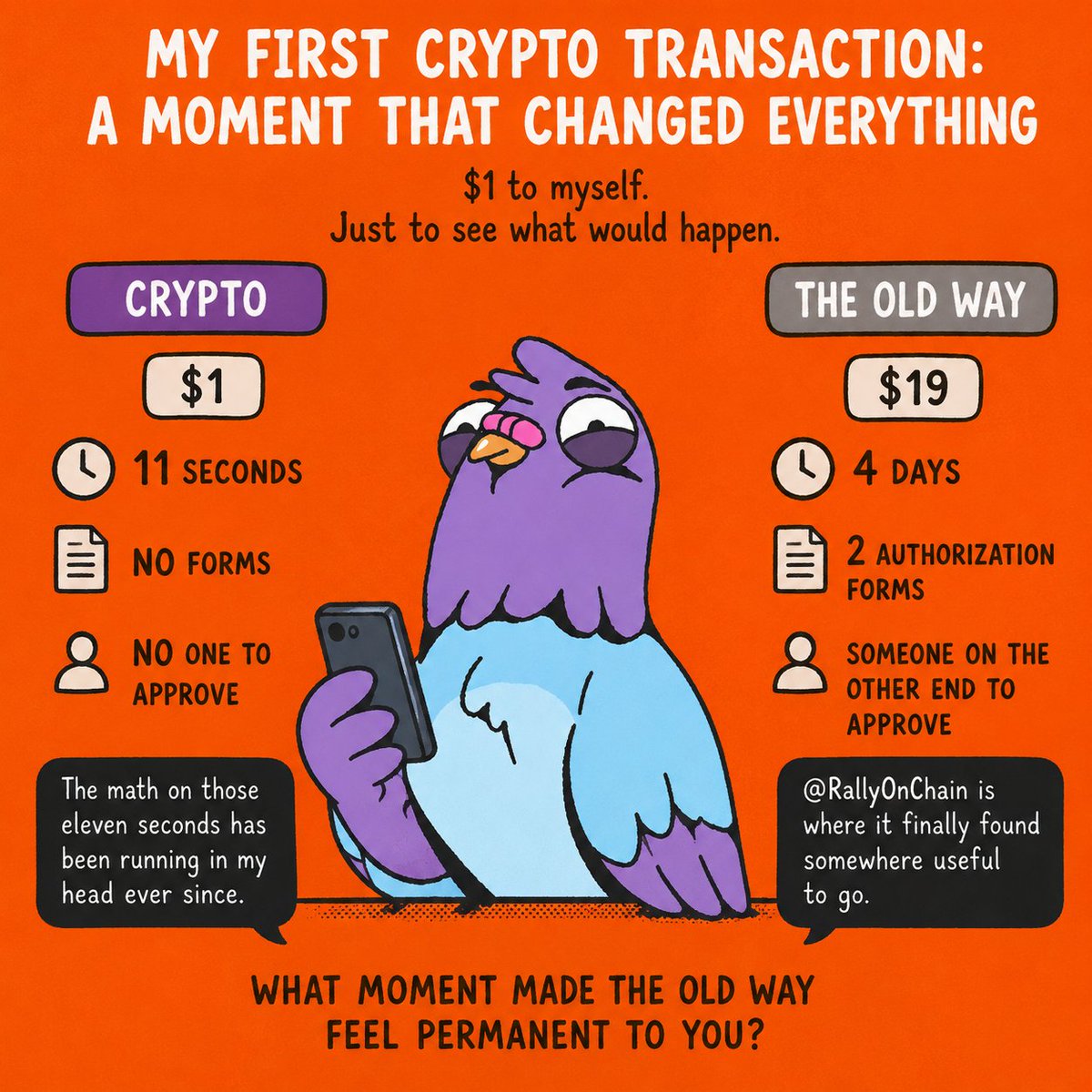

The first transaction I ever sent in crypto was one dollar, to myself, just to watch what happened.

Eleven seconds. No forms. No one on the other end who needed to approve it.

That same morning I had sent a wire transfer to the same destination. Four days. Nineteen dollars. Two authorization forms.

The math on those eleven seconds has been running in my head ever since.

@RallyOnChain is where it finally found somewhere useful to go.

What moment made the old way feel permanent to you?

54

10

81

3,900

DataRogue retweeted

May 31

80 AI tools to finish months of work in minutes.

1. Research

- ChatGPT

- Copilot

- Gemini

- Abacus

- Perplexity

2. Image

- Fotor

- Dalle 3

- Stability AI

- Midjourney

- Microsoft Designer

3. CopyWriting

- Rytr

- Copy AI

- Writesonic

- Adcreative AI

4. Writing

- Jasper

- HIX AI

- Jenny AI

- Textblaze

- Quillbot

5. Website

- 10Web

- Durable

- Framer

- Style AI

6. Video

- Klap

- Opus

- Eightify

- InVideo

- HeyGen

- Runway

- ImgCreator AI

- Morphstudio .xyz

7. Meeting

- Tldv

- Otter

- Noty AI

- Fireflies

8. SEO

- VidIQ

- Seona AI

- BlogSEO

- Keywrds ai

9. Chatbot

- Droxy

- Chatbase

- Mutual info

- Chatsimple

10. Presentation

- Decktopus

- Slides AI

- Gamma AI

- Designs AI

- Beautiful AI

11. Automation

- Make

- Zapier

- Xembly

- Bardeen

12. Prompts

- FlowGPT

- Alicent AI

- PromptBox

- Promptbase

- Snack Prompt

13. UI/UX

- Figma

- Uizard

- UiMagic

- Photoshop

14. Design

- Canva

- Flair AI

- Designify

- Clipdrop

- Autodraw

- Magician design

15. Logo Generator

- Looka

- Designs AI

- Brandmark

- Stockimg AI

- Namecheap

16. Audio

- Lovo ai

- Eleven labs

- Songburst AI

- Adobe Podcast

17. Productivity

- Merlin

- Tinywow

- Notion AI

- Adobe Sensei

- Personal AI

18. Social media management

- Tapilo

- Typefully

- Hypefury

- TweetHunter

Follow me for more.

59

588

1,805

342,432

DataRogue retweeted

May 31

5 pro tips we'd tell any creative team starting with AI video this week:

1. Stop chasing a more cinematic single clip. Build a library you can compound on.

2. Lock in the character before you lock up the script.

3. Treat generation as variation, not output.

4. Plan the shot list before generating. AI is faster, not magic.

5. You will probably still need to edit a final cut.

What else would you add?

10

14

53

1,699

DataRogue retweeted

Jun 1

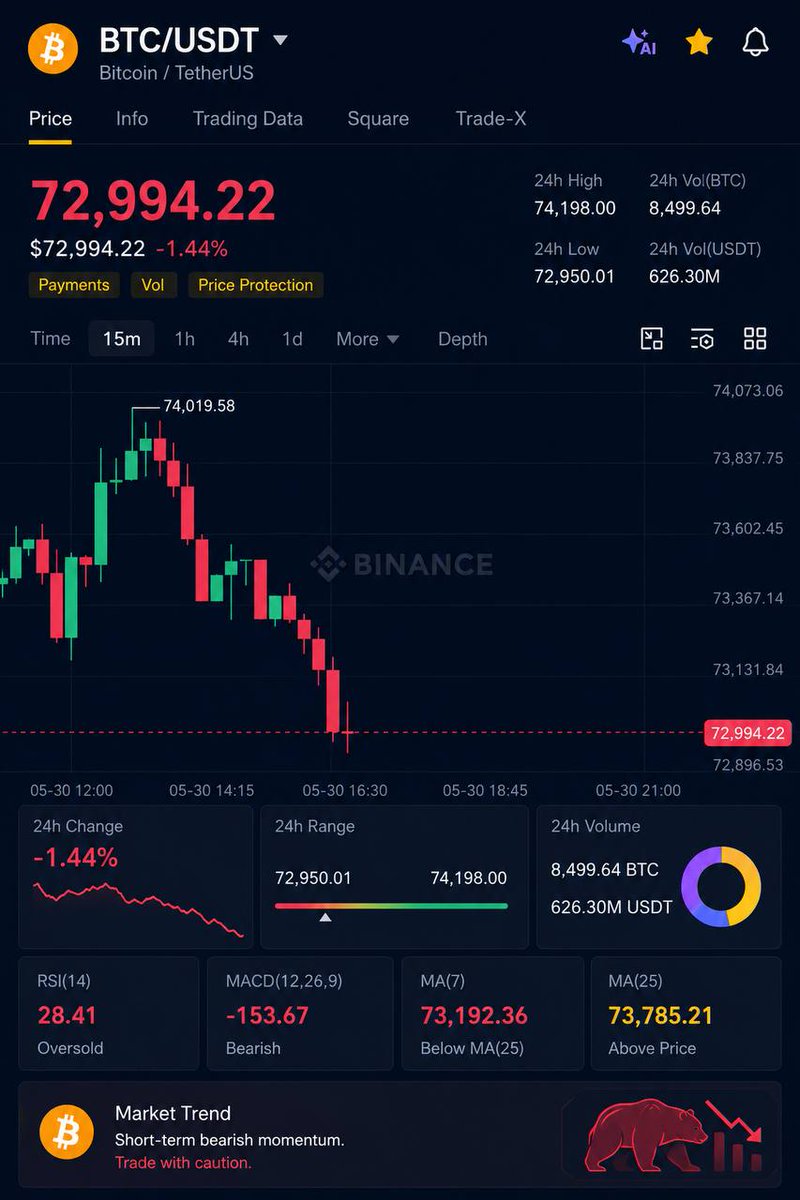

Nothing new....we always get hit hard on Mondays.

Welcome to Monday morning trades, where hope gets liquidated in 15 mins.

$74,019 Friday, $72,994 Monday.....the weekend traders did their thing.

Dump on Monday, Pump on Wednesday.

Crypto is not normal after 10 Oct crash in my opinion so.

Welcome to the BEAR MARKET since Oct 25.

We are not SO back.

70

16

89

11,607

The best web3 & crypto investigators in the space 👽

- @zachxbt

- @morsyxbt

- @tanuki42_

- @zarvxbt

- @detheactive

If you're not following these guys yet, you definitely should

They can help you spot red flags early and avoid a lot of potential scams and bad actors in the space 🙌

11

1

28

1,053

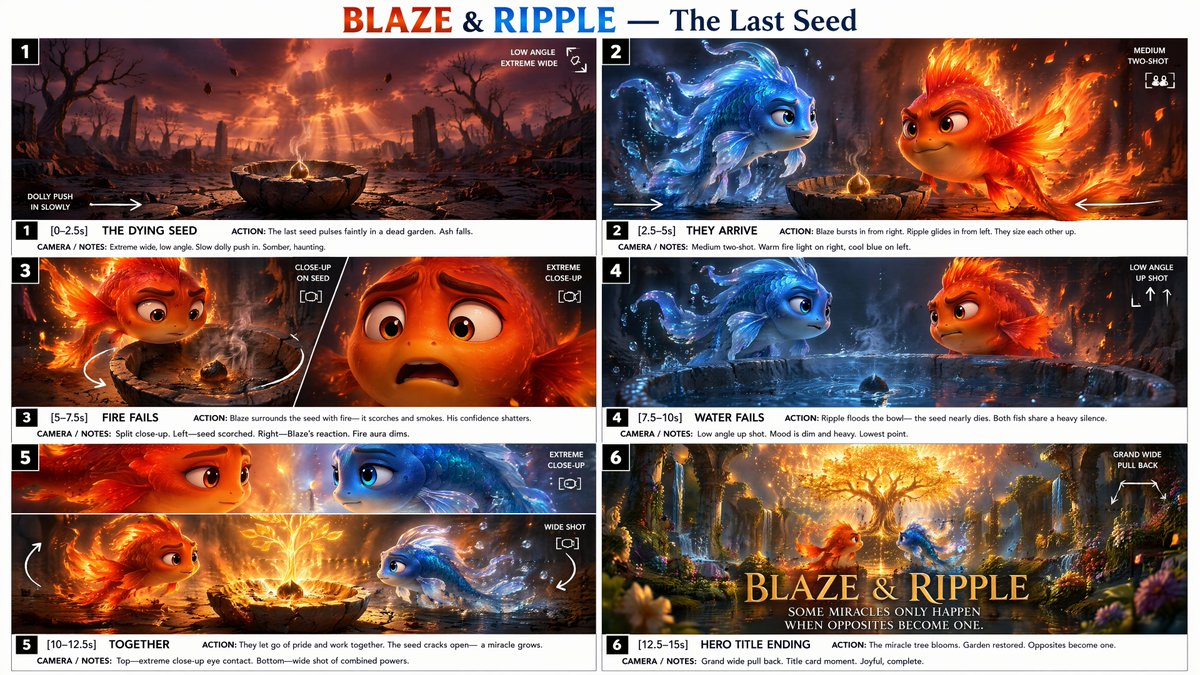

Two magical koi fish. One controls fire 🔥 One controls water 💧

They both tried to save the last magical seed alone.

Both failed.

Then came the moment neither expected

"Maybe I need you."

"And I need you."

What happened next changed everything 🌱✨

Made with @renoiseai. 15 seconds, one story, zero limits.

#renoiseai #RenoiseCanvas

66

52

366

44,555

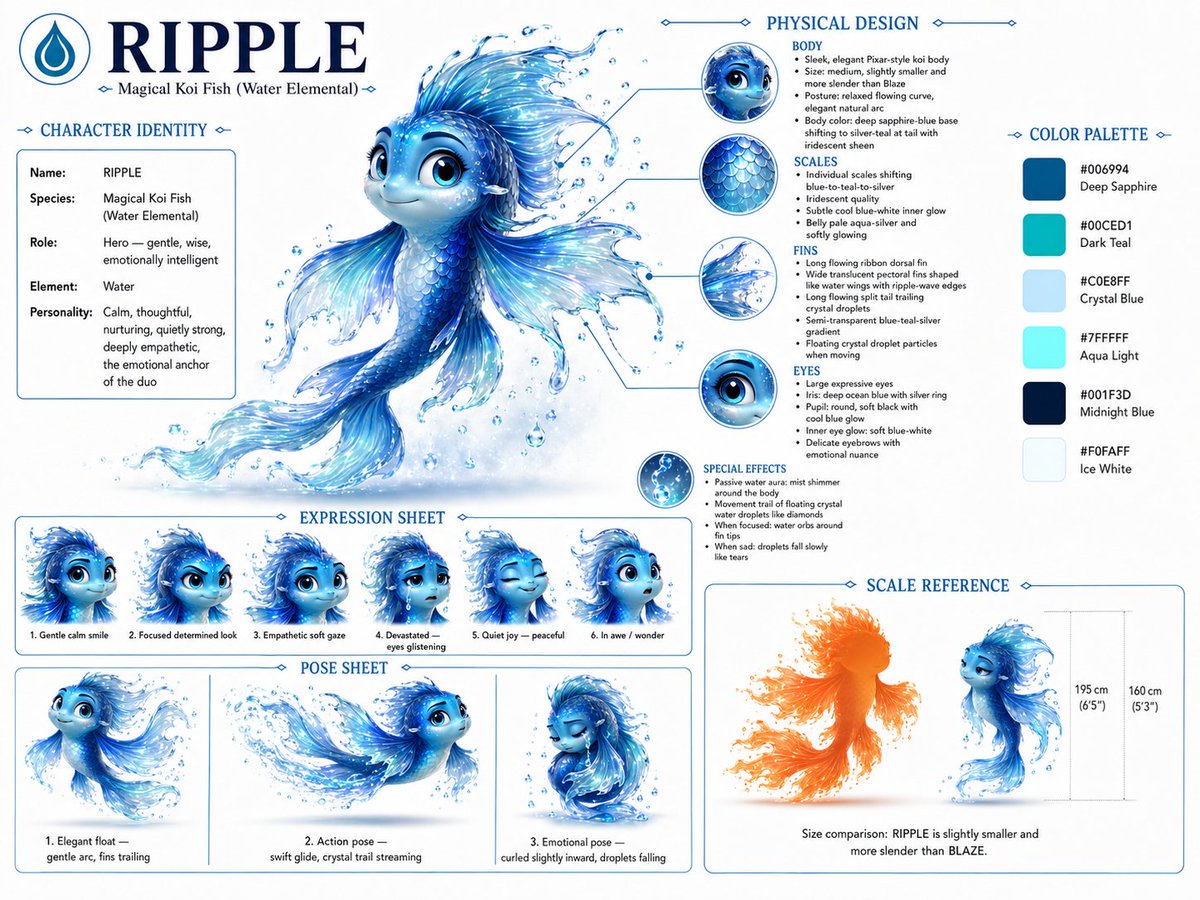

🐟 Character Descriptions

BLAZE 🔥

A fire koi who swims through air leaving ember trails. Bold, loud, acts before he thinks. His flames can warm a world — or burn it down. Learns that strength without gentleness destroys what it loves most.

RIPPLE 💧

A water koi who glides through mist leaving crystal droplets. Calm, precise, quietly confident. Her water can heal anything — or drown it. Learns that patience without warmth can never truly nurture.

2

6

36

Hey @renoiseai team 👋

Just wanted to say that Creator Challenge 5 genuinely pushed me to think differently about storytelling with AI , i tried to make something different from others, don't know how far i can make but

Building BLAZE & RIPPLE from scratch designing characters, writing voice lines, crafting a story with a real emotional arc — all inside Renoise Canvas felt like something new.

The 15-second limit isn't a constraint. It's a creative challenge. And that's what makes this special.

Thank you for building a platform that makes creators feel like directors.

Can't wait to see what Challenge 6 looks like. 🔥💧

6

26

Pixar 3D animated cinematic short film, exactly 15 seconds, continuous

with seamless scene transitions. Title: "BLAZE & RIPPLE — The Last Seed"

CHARACTER GUIDE — keep 100% consistent across all scenes:

BLAZE: round-faced koi fish, vivid orange-red-gold scales glowing like

hot coals, flame-shaped fins with ember particle trails, large expressive

ember-gold eyes, bold confident build, warm orange fire aura.

RIPPLE: elegant graceful koi fish, iridescent blue-silver-teal scales,

long flowing ribbon fins trailing crystal water droplets, soft glowing

ocean-blue eyes, cool blue-white mist aura, smaller and more slender.

THE SEED: tiny magical seed glowing faint gold, resting in a cracked

ancient stone bowl at center of a dead circular garden.

SCENE SEQUENCE:

[0:00–0:02.5] SCENE 1 — THE DYING SEED

Extreme wide low-angle slow push-in. A tiny magical seed pulses faint

dying gold light inside a cracked stone bowl at center of a dead silent

garden. Ash leaves fall. No characters yet. Deep amber-purple dusk sky.

Volumetric god rays. Mood: somber and haunting.

VOICE — Narrator (warm, cinematic): "In a forgotten garden... the last

magical seed was dying."

[0:02.5–0:05] SCENE 2 — THEY ARRIVE

BLAZE bursts in from upper right with blazing fire trails, lands

confidently beside the seed, puffs up proudly. RIPPLE glides in

silently from the left through cool silver mist, crystal droplets

floating around her. They notice each other — a brief competitive

sizing-up look. Warm fire light on left, cool blue light on right.

VOICE — Blaze (bold, cheerful): "Don't worry little one. Fire fixes

everything." Ripple (calm, dry): "...Or maybe it doesn't."

[0:05–0:07.5] SCENE 3 — FIRE FAILS

BLAZE circles the seed confidently releasing warm fire toward it.

The seed's edges scorch black and smoke. His expression crashes from

heroic to horrified. He jolts back. Close-up on his face — ember eyes

wide, filled with guilt. His fire aura dims.

VOICE — Blaze (panicked): "Wait— no, no—" Ripple (firm): "Move.

I'll save it."

[0:07.5–0:10] SCENE 4 — WATER FAILS

RIPPLE wraps the seed tenderly in cool water mist. But water floods

the bowl, drowning the seed's last ember glow — it nearly goes dark.

Ripple freezes, devastated. Both fish float face to face in tense

silence staring at the barely breathing seed between them. The whole

garden feels dimmer.

VOICE — Blaze (frustrated): "Now you drowned it!" Ripple (quietly

horrified): "...I didn't mean to." Both fall silent.

[0:10–0:12.5] SCENE 3 — TOGETHER

Extreme close-up. Blaze looks at Ripple, all bravado completely gone —

just honest vulnerability in his eyes. She meets his gaze with equal

softness. They turn to the seed together. Blaze's gentle warmth wraps

around it like cupped hands. Ripple's cool mist drifts softly inside

the warmth. Where fire and water blend — a perfect golden glow forms

around the seed. It pulses strongly. Then CRACKS OPEN — a brilliant

golden shoot bursts upward, rapidly blooming into a radiant small tree

filled with golden blossoms. Camera orbits slowly as it blooms.

VOICE — Blaze (quietly, vulnerable): "...Maybe I need you."

Ripple (gentle smile): "And I need you."

[0:12.5–0:15] SCENE 6 — HERO TITLE ENDING

Grand slow pull-back reveal. The miracle tree now towers magnificent

and glowing at center of the fully restored garden — green grass,

golden flowers, warm light everywhere. BLAZE and RIPPLE float side

by side before it, small against its grandeur. Ember sparks and crystal

droplets drift from them, rise and merge into golden sparks floating

upward. Both faces: completely peaceful, joyful, complete. Camera

pulls back slowly. Edges vignette to deep cinematic black. Elegant

gold serif title fades in: "BLAZE & RIPPLE" — subtitle beneath in

soft silver: "Some miracles only happen when opposites become one."

VOICE — Narrator (slow, reverent): "Some miracles only happen...

when opposites become one." Gentle orchestral swell to close.

OVERALL ART DIRECTION:

Pixar 3D render quality. Cinematic 16:9. Color temperature shifts

warm-to-cool-to-golden across the film. Smooth motivated scene

transitions. Subsurface scattering on all organic surfaces. Volumetric

lighting throughout. Fire embers, water droplets and golden spark

particle systems. Expressive character faces showing pride, guilt,

devastation, vulnerability, wonder and peace. Emotional, warm,

cinematic tone overall.

2

9