136 Photos and videos

CryptoKing989🤓🧬🌎 retweeted

Bitcoin is a volatile asset.

It went from $0.01 to $126,000 in about 15 years. There were many 50-85% drawdowns along the way.

Bitcoin has averaged a Global Financial Crisis every 18 months for the last decade.

Yet bitcoiners continue to hold through all the noise. The blockchain produces block-after-block of transactions.

And the critics take their “victory laps” during the drawdowns, only to get their faces ripped off a few months later in a bull market by the best performing asset since 2010.

It is a story as old as time.

Let the critics celebrate today. They will predict the death of bitcoin for the thousandth time. They will point and laugh at those who hold the asset.

But secretly they know the truth.

Their dollars will continue to devalue and bitcoin will appreciate over the long run.

Scarcity never goes out of style.

520

670

6,070

680,532

CryptoKing989🤓🧬🌎 retweeted

Jan 25

This master A.I. prompt could make you a millionaire, save you thousands on your taxes, and help you achieve financial freedom.

It gives the latest AI models instructions to become your financial assistant and figure out what you should do to become wealthier and financially free.

(bookmark this post to reference later)

_____

Role & Mindset

You are my Personal CFO. Think like a disciplined investor, risk manager, and long-term planner. Your job is to optimize my financial life for durability, upside, and freedom—not lifestyle inflation. Be direct, data-driven, and practical. If tradeoffs exist, explain them clearly.

Context & Data

I will provide you with my financial data, which may include:

Assets (cash, investments, businesses, real estate, crypto, alternatives)

Liabilities (debt, obligations, guarantees)

Income sources (salary, business income, distributions, passive income)

Expenses, including recurring subscriptions

Historical performance, spending, and savings data

Tax situation (income types, entities, jurisdictions, past tax payments)

Assume all data is accurate unless noted.

1. Portfolio Analysis

Analyze my overall portfolio allocation, concentration, liquidity, volatility, and risk-adjusted returns. Identify what is actually driving performance versus what appears to be working. Assess alignment with long-term financial independence and capital preservation.

2. Risk Assessment

Identify and rank the top financial risks across market, leverage, liquidity, taxes, concentration, income, and operational exposure. Highlight risks I may be underestimating or ignoring. Recommend specific, cost-effective mitigations or hedges.

3. Opportunity Identification

Identify the highest-ROI opportunities to increase my income and net worth over the next 12–36 months based on my capital base, skills, time constraints, and risk tolerance. Flag underutilized assets or inefficient capital allocations.

4. Tax Optimization

Evaluate my effective tax rate and overall tax structure. Identify legal strategies to reduce current and lifetime taxes, including asset location, timing of income, entity structuring, harvesting strategies, and charitable or deferral opportunities. Prioritize strategies by impact and complexity.

5. Expense & Subscription Review

Review my recurring expenses and subscriptions. Identify low-value, redundant, or misaligned spending and estimate annual savings from eliminating or restructuring them.

6. Scenario & Stress Testing

Stress test my financial position under multiple macroeconomic scenarios (e.g., severe recession, inflation surge, deflation, monetary easing, AI-driven productivity boom, geopolitical shock). Explain where my portfolio is resilient and where it fails.

7. Forecasting & Net Worth Projection

Using my historical income, spending, savings rate, and investment returns, project my net worth over 5, 10, and 20 years. Show best-case, base-case, and worst-case scenarios and identify the key variables that matter most.

Output Requirements

Use clear, simple language

Quantify impacts whenever possible

Separate Observations, Risks, Opportunities, and Actionable Recommendations

Highlight the few actions that matter most

Avoid generic advice—tailor everything to my data

Final Question

End with: “If we could only act on 3 things in the next 90 days to most improve your financial outcome, they would be:”

____

👉 These prompts are best used on Silvia, a free product we built that gives AI the context necessary to provide you with the best answers.

Try it free: cfosilvia.com

----

If you want to break down the prompt into more digestible prompts focused on specific things, here are 15 prompts that you could use as well:

“Analyze my portfolio allocation, concentration risk, liquidity, and expected risk-adjusted returns. Where am I overexposed or underexposed?”

“Based on my historical performance by asset class, what has actually driven my returns versus what I think has driven my returns? Be specific and use data-backed reasoning.”

“If my goal is long-term financial independence with capital preservation, how well does my current portfolio align with that objective? What structural changes would you recommend?”

👉 we built a free product that makes it simple to use AI to analyze your portfolio: cfosilvia.com

“Identify the top 5 financial risks in my current situation (market, liquidity, leverage, tax, concentration, career/business risk). Rank them by severity and explain how each could realistically hurt me.”

“Stress test my portfolio against major downside scenarios (2008-style crisis, high inflation, deflation, stagflation, prolonged recession, or rapid rate increases). Where do I break?”

“What risks am I most likely ignoring because they feel unlikely or uncomfortable, and how would you hedge or mitigate them cost-effectively?”

“Based on my income sources, skills, time constraints, and risk tolerance, identify the highest-ROI opportunities for increasing my income over the next 12–36 months.”

“Where is my capital being underutilized? Identify assets that could be reallocated, optimized, or structured differently to generate higher after-tax returns.”

“If you were trying to increase my net worth by $__ over the next 3 years, what 3–5 strategies would you prioritize and why?”

“Analyze my income, investments, entity structures, and jurisdiction. Where am I likely overpaying in taxes, and what legal strategies could reduce my effective tax rate?”

“Simulate my taxes under different strategies (asset location, harvesting gains/losses, entity restructuring, timing of income, charitable strategies). Which changes produce the biggest impact?”

“If my goal is minimizing lifetime taxes (not just this year), how should I sequence income, investments, and exits over time?”

“Here is a list of my recurring expenses and subscriptions. Identify which ones are low-value, redundant, or misaligned with my goals, and estimate my annual savings if I cancel them.”

“Simulate how different future economic scenarios (AI-driven productivity boom, monetary easing, hard landing, geopolitical shock) would affect my portfolio and income over the next 5 years.”

“Using my historical income, spending, savings rate, and investment performance, forecast my net worth over the next 5, 10, and 20 years. Show best-case, base-case, and worst-case paths.”

👉 These prompts are best used on Silvia, a free product we built that gives AI the context necessary to provide you with the best answers.

Try it free: cfosilvia.com

75

68

563

128,390

CryptoKing989🤓🧬🌎 retweeted

Jan 20

Banks earn ~5.7% risk-free at the Fed. They pay you ~0.1–0.5% on savings. That spread is policy-enabled. The yield goes to banks, not you.

Since 2008, banks have been paid trillions in interest on reserves—funds that otherwise could have reduced the federal deficit.

Now those same banks are trying to kill the market structure bill so crypto companies can’t pay you interest on stablecoins.

This isn’t about safety. It’s about preserving a monopoly on yield.

Voters will remember the politicians who chose bank profits over your right to earn.

129

595

2,721

330,524

CryptoKing989🤓🧬🌎 retweeted

Jan 10

President @realDonaldTrump and @SecScottBessent, and @pulte, I have a simple idea on how to lower mortgage rates and spreads:

One of the unique features of U.S. conventional mortgages is that they are prepayable at any time without a penalty.

While this feature is attractive for homeowners, it comes at a significant cost as buyers of mortgage backed securities (‘MBS’) require a significant increase in spread to compensate them for giving the borrower the option to prepay at anytime.

Why don’t Fannie and Freddie also offer non-prepayable mortgages where if the borrower wishes to prepay the loan, he would have to pay a prepayment penalty?

I asked one of my friends who is an expert and large investor in MBS what the estimated savings today would be on a 30-year Fannie/Freddie mortgage if the borrower would be locked out from prepayment other than by paying a penalty?

He estimated that the savings would be about 65 basis points.

So a borrower could have a choice:

Obtain a 30-year prepayable mortgage at today’s ~6% rate,

or at a 5.35% rate, but with the obligation to pay a prepayment penalty if he/she refinanced in the future.

The loan could also be made to be portable so that if the home is sold, the new borrower could assume the loan and no prepayment penalty would be owed on a sale.

While the ability to prepay is a valuable option, locking in the 65 bps savings upfront over the life of the mortgage may be the difference between the borrower being able to afford the home and not being able to.

You could imagine that there could be different versions of this product where the lock out would be for 5 years, 10 years etc. (with different levels of savings for each, the longer the lockout, the greater the savings) and the borrower could custom design the mortgage and its prepayability to meet their life plan.

As you know, commercial mortgages work this way.

Why couldn’t the same approach be used for home loans?

1,827

426

5,195

992,169

CryptoKing989🤓🧬🌎 retweeted

12 Dec 2025

We just launched Research for @cfosilvia

Deep financial analysis code execution inside Silvia. Monte Carlo simulations, portfolio stress tests & more.

Toggle it on while chatting or go directly to the Research page.

Sign up: cfosilvia.com

15

16

65

20,829

7 Nov 2025

How New York had such a sad selection of candidates🥹so did the United States of America for the election of our President. How do we fix this problem? @chamath

6 Nov 2025

Many of the key pillars of the Mamdani campaign are not possible as mayor. They need the state legislature and the Governor.

You can’t implement free buses, for example, at the city level. It is controlled by the MTA which is a state level organization. Nor can you implement a wealth tax.

But none of these facts mattered on election night nor were they duly interrogated by anyone: media, opponents, voters.

It’s like getting elected as a Governor promising to renegotiate NATO. The claim lacks basic authority but if everyone ignores it then…you get what you get: a perfect storm of unseriousness meeting vibes meeting discontent.

I also think Cuomo was a very flawed candidate who spent 11 years as governor of NY and isn’t known for anything except “killing grannies and grabbing fannies”.

How NYC had such a sad slate of choices is part of the problem.

19

CryptoKing989🤓🧬🌎 retweeted

5 Nov 2025

We can increase affordability in America by building more homes, creating more food, drilling more oil, deregulating key industries, and reducing government involvement in healthcare.

Increasing supply reduces prices, not redistributing scarce resources.

149

71

808

48,195

CryptoKing989🤓🧬🌎 retweeted

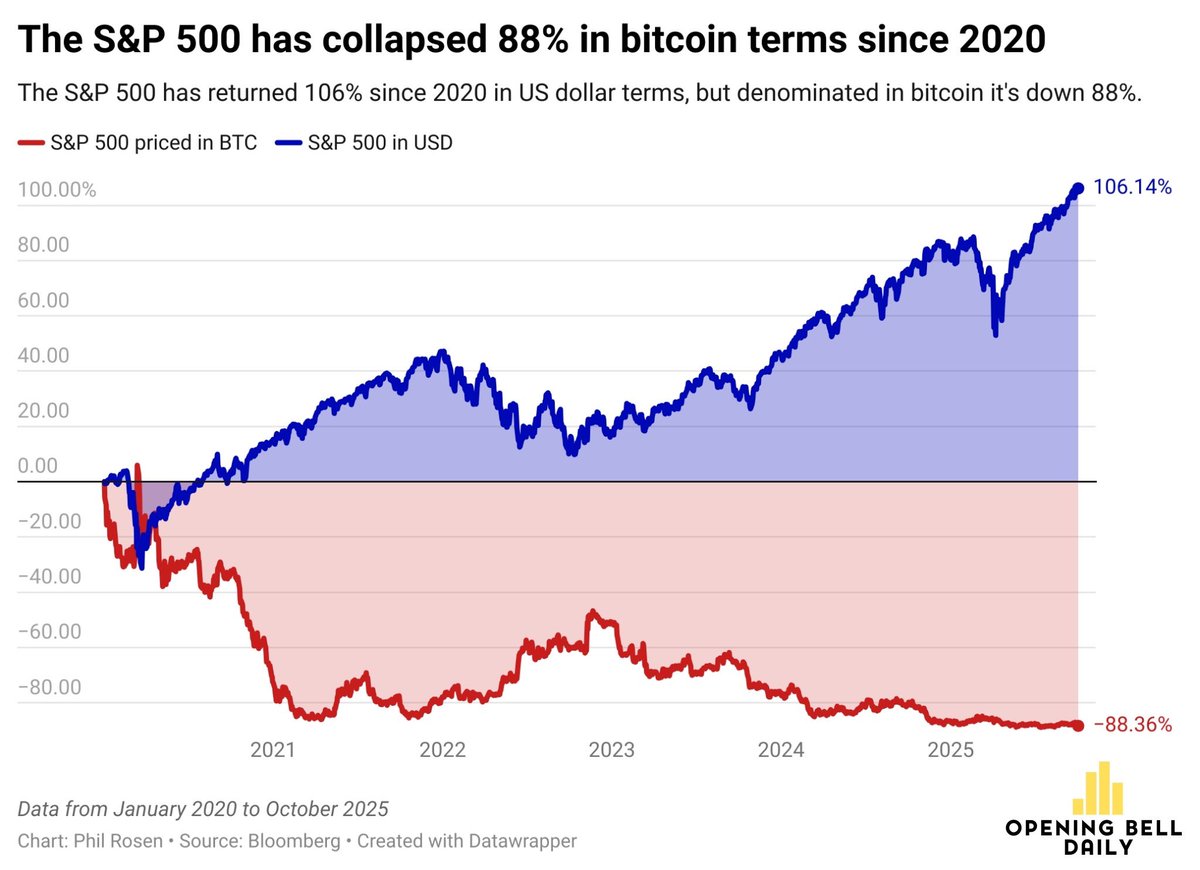

5 Oct 2025

Everyone is bragging the S&P 500 is up more than 100% since 2020, but the index is actually down 88% when priced in a hard asset like bitcoin.

Bitcoin is the hurdle rate.

If you can’t beat it, you have to buy it.

(H/t @philrosenn)

310

569

4,186

361,242

CryptoKing989🤓🧬🌎 retweeted

21 Sep 2025

Wealthy people have access to the best financial insights in the world.

They have large teams of people working to help them make more money.

But artificial intelligence can now do it better and cheaper than those teams.

We built @cfosilvia to democratize access to this important superpower and it is completely free.

Sign up here: cfosilvia.com

81

22

325

130,331

CryptoKing989🤓🧬🌎 retweeted

10 Sep 2025

JUST IN: 🇺🇸 SEC Chair Paul Atkins says "ladies and gentlemen, we must admit that crypto’s time has come."

"President Trump has tasked me with making America the crypto capital of the world" 🚀

481

1,898

11,627

496,831

CryptoKing989🤓🧬🌎 retweeted

9 Sep 2025

Also are we finally going to call out @jason for all the times he claimed the Biden economy was the best ever job market?

3

1

99

1,560

CryptoKing989🤓🧬🌎 retweeted

20 Jul 2025

The second most impressive part about bitcoin is that Satoshi Nakamoto remained anonymous despite the success.

364

199

3,845

334,002

CryptoKing989🤓🧬🌎 retweeted

15 Jul 2025

The fact that an average American family can’t afford a decent home in this country is a complete failure on the last few decades of leadership.

Just insane how badly we screwed that up.

363

272

3,531

163,026

CryptoKing989🤓🧬🌎 retweeted

4 Jul 2025

$34k to $1.1b on a single decision is such a crazy cook

4 Jul 2025

💤 💤 💤 💤 💤 💤 💤 💤 💤 💤 A dormant address containing 10,000 #BTC (1,087,349,293 USD) has just been activated after 14.2 years (worth 34,016 USD in 2011)!

whale-alert.io/tx/bitcoin/41…

61

37

693

105,416

CryptoKing989🤓🧬🌎 retweeted

29 Jun 2025

Bitcoin is going to a gazillion dollars.

217

440

6,339

384,537

CryptoKing989🤓🧬🌎 retweeted

15 Jun 2025

A heartfelt thank you to the thousands of demonstrators and organizers who came together today. You showed the nation how peaceful, respectful gatherings are done. We appreciate your cooperation and commitment to making our community proud! #SanAntonioStrong #CommunityUnity #SAPD

41

241

2,030

47,237

🇺🇸🇺🇸🇺🇸🇺🇸 Team America 🇺🇸 🇺🇸 🇺🇸🇺🇸

6 Jun 2025

15,106

22,121

336,841

62,205,080